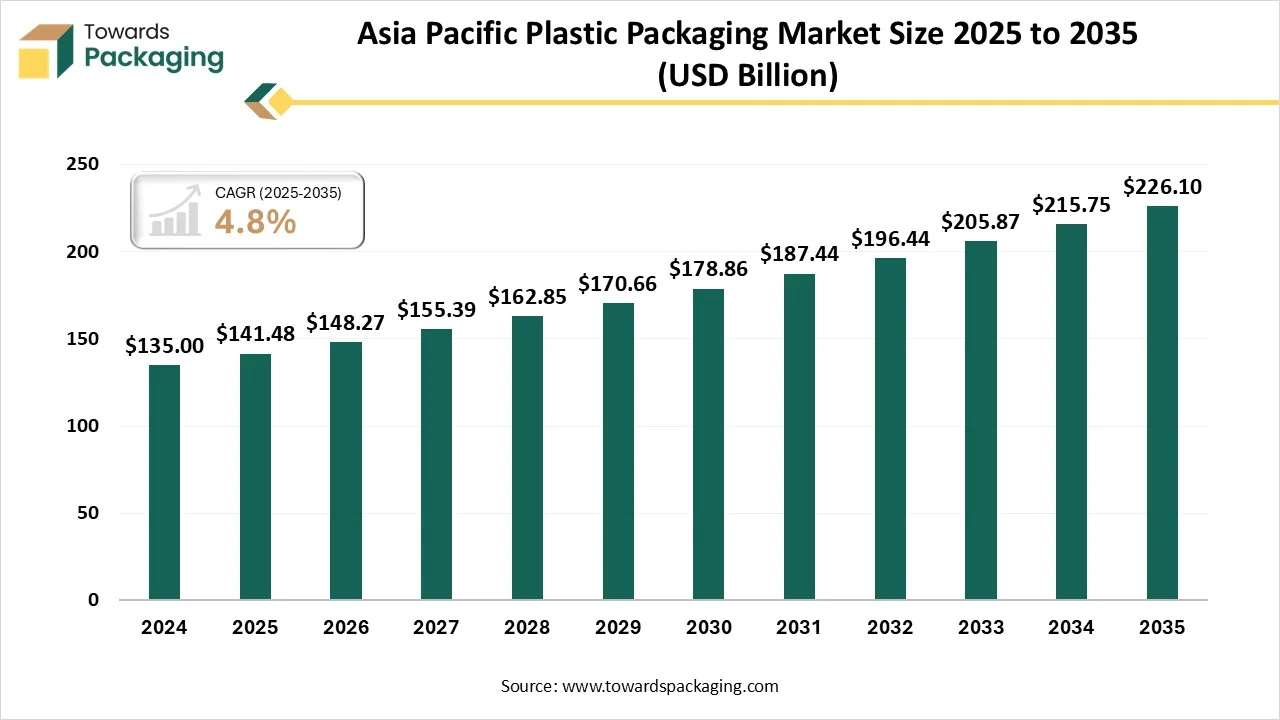

The Asia Pacific plastic packaging market is projected to grow from USD 148.27 billion in 2026 to USD 226.1 billion by 2035, registering a CAGR of 4.8% during 2026-2035. Our report provides in-depth coverage of market size, growth trends, and segment-wise data by material type, product type, application, and end-use industry. It delivers detailed regional analysis across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, along with comprehensive company profiling, competitive landscape assessment, value chain evaluation, and trade flow analysis.

The study also reviews transportation and logistics performance such as shipping costs, handling time, and distribution networks, as well as consumer demand trends, regional preferences, and sustainability regulations shaping packaging development. In addition, it includes competitive analysis of major companies, innovation in recyclable and bio-based plastics, and evolving packaging technologies, helping businesses understand market dynamics and identify growth opportunities in the Asia Pacific plastic packaging market.

Asia Pacific plastic packaging refers production and sale of polymer-based containers, films, bottles, trays, closures and multilayer laminates used to protect, transport and present food, beverages, personal care, pharmaceutical, industrial and e-commerce products. It covers rigid and flexible formats, barrier and recyclable structures, and conversion technologies (blow/fill/seal, extrusion, thermoforming, injection molding). Demand is driven by convenience, lightweighting, extended shelf life and e-commerce; sustainability and circular-economy innovations (PCR, mono-materials, recyclable films) increasingly shape product design and investment.

Technological transformation in the Asia Pacific plastic packaging market plays a significant role in its expansion. The integration of AI technology has influenced the advancement in the resources, enhancement in recycling process, and creating eco-friendly designs. This process is undergoing noteworthy development because of its capacity to generate precise, thin-wall usages for luxury food and healthcare items. The increasing incorporation of robotics in the packaging industry has reduced labour charges and made packaging process cost-effective.

The major raw materials utilized in this market are polyethylene (PE), polyethylene terephthalate (PET), polypropylene (PP).

The component manufacturing in this market comprises resins, polyethylene, blisters, and trays.

This segment is growing focus on expansion retail substructure, and production capabilities.

")

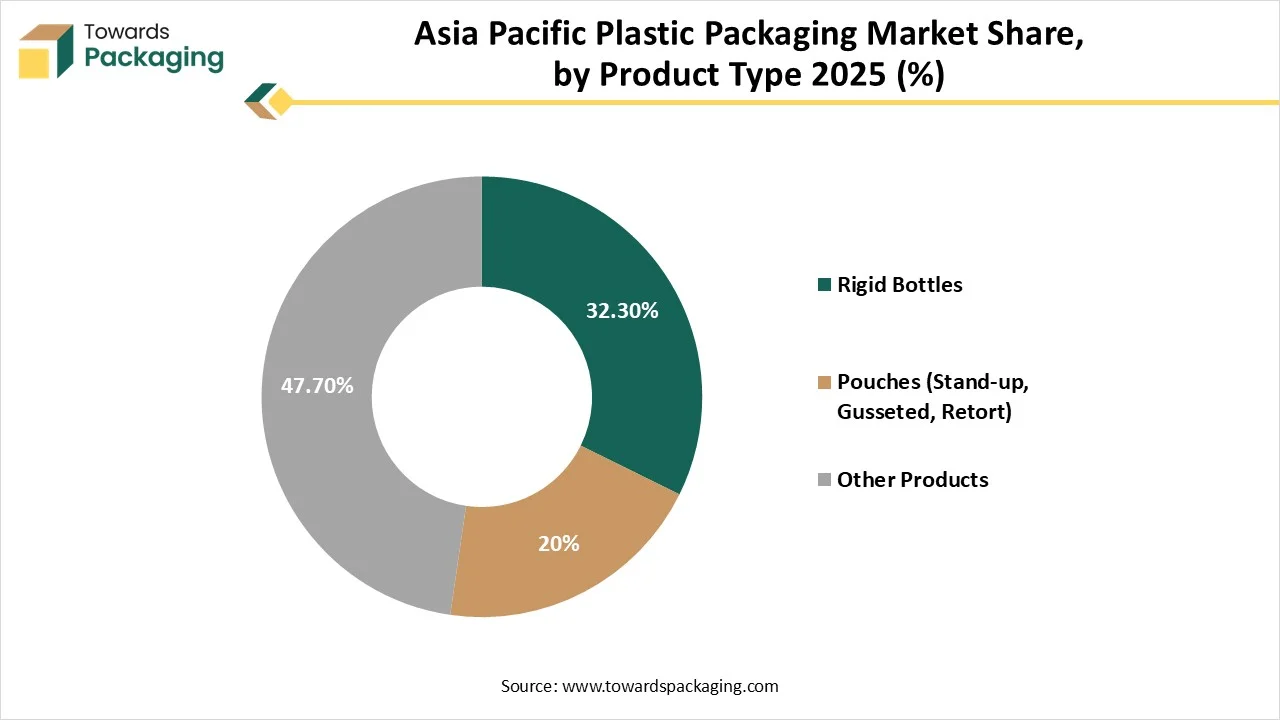

The rigid bottles segment dominated the market with highest share in 2024 due to strong demand for safe packaging. Its manufacturing process includes a huge variety of resin type such as polyethylene terephthalate (PET), polyethylene (PE), and polypropylene (PP). This segment is highly in-demand due to rising food & beverages industry, pharmaceuticals, personal care and toiletries, and industrial market. A main process utilized in the manufacturing of rigid plastic packaging. A noteworthy customer of rigid bottles for goods like mouthwash and cosmetics.

The pouches (stand-up, gusseted, retort) segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to changing lifestyle and rapid urbanization. It is majorly influenced by rising demand for packed foods, increasing disposable earnings, and the change in the direction of sustainable, convenient, and lightweight packaging options. It offers prolonged volume and steadiness for items such as pet food, coffee, and industrial products. It is manufactured to endure high-temperature handing out for shelf-steady food products, providing a substitute to old-style glass jars and metal cans.

The jars & containers is the fastest-growing in the market, as it comprises durability, product visibility, and cost-effectiveness in the packaging sector. The rising trend for such as sustainability are affecting development and growth. The increasing demand for preservation of food products has raised the demand for this segment in the food & beverages sector. The strength and visibility properties of this segment has enhanced its demand in luxurious packaging.

| Material Type Segments | Market Share 2025 (%) |

| Polyethylene (HDPE, LDPE, LLDPE) | 34.70% |

| Bioplastics / Bio-PET / Bio-PE | 25% |

| Other Materials | 40.30% |

The polyethylene (HDPE, LDPE, LLDPE) segment dominated the market with highest share in 2024 due to rapid urbanization and industrialization. HDPE offers huge tensile strength, chemical inertness, and effective resistance. These are extensively utilized for rigid drums, containers, and bottles where strength and durability are important. LDPE packaging is flexible, lightweight, and resistant to influence and moisture. It is mainly utilized for flexible packaging, comprising bags, films, and few containers. It is influenced by the development of e-commerce, which depend on strong and safe packaging options.

The Bioplastics / Bio-PET / Bio-PE segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to feedstock availability and government initiatives. These are utilized in both rigid as well as flexible packaging, like films, bottles, jars, and cups, and seamlessly incorporated into present recycling streams. These planned to be compostable or biodegradable, providing a diverse end-of-life option than old-style plastics. Strict Government guidelines in countries like China, India, Japan, South Korea, and several others encourage the usage of biodegradable substitutes.

The polyethylene terephthalate (PET) is the fastest-growing in the market, as it comprises enhance shelf-life packaging and government initiatives. Growing demand for packed food & beverages because of increasing disposable earnings and tiring lifestyles. The development of online retail influences demand for this material convenient and protective packaging qualities for shipping. Initiatives encouraging recycling and the usage of recycled PET (rPET) are generating a strong industry for sustainable options.

")

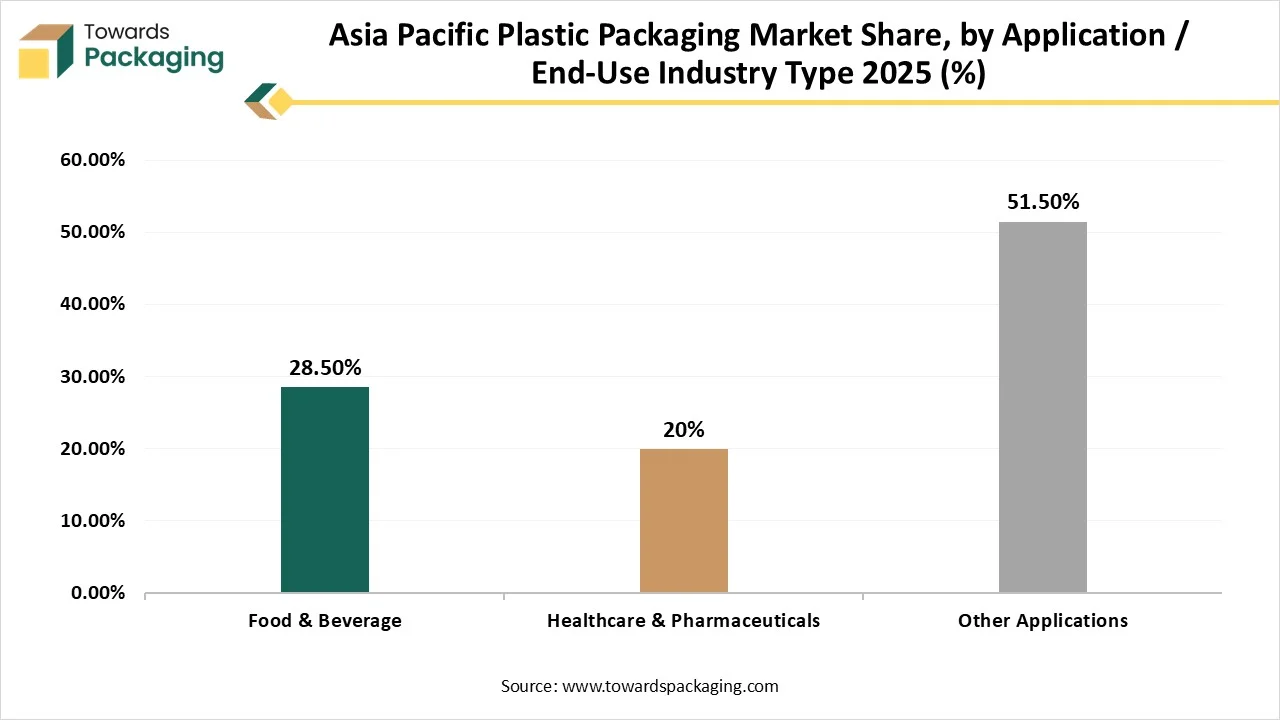

The food & beverage segment dominated the market with highest share in 2024 due to rising e-commerce sector, convenience, and growing middle class population. A wide range of food products such as bakery and confectionery, dairy, frozen and fresh food, confectionery and snacks, seafood and meat packaging influence the development of this market. The rapid growth in the alcohol market has influenced the bottled packaging with protection. These is a need for safe storage from air, moisture, and light without degrading the quality of food products has raised the adoption of this market.

The healthcare & pharmaceuticals segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to huge demand for storage and transportation. The increasing drug delivery portals has raised the demand for such packaging for safe transportation. Increasing emphasis on protective transportation and management of medicines for injectable, transdermal routes, and oral. It is influenced by increasing government programs and pet ownership for animal health.

The personal care & cosmetics is the fastest-growing in the market, as it comprises bottles, jars, tubes, pouches, and many other. It also includes development in refillable and sustainable packaging, influenced by customer consciousness and e-commerce sector. There is a robust influence for sustainable packing, comprising the usage of recyclable plastics as well as refillable choices, to decrease ecological influence. Amplified customer consciousness regarding personal dressing and appearance is a major aspect influencing the complete market's extension.

| Packaging Type Segments | Market Share 2025 (%) |

| Rigid | 68.50% |

| Flexible | 20% |

| Other Types | 11.50% |

The rigid packaging segment dominated the market with highest share in 2024 due to increasing demand for strong packaging for protective storage as well as transportation. It is highly preferred for the packaging of fragile products. Rising e-commerce sector has influenced the demand for rigid packaging of the products. It includes packaging such as bottles, jars, trays, tubes, caps & closures. Increasing shift towards urban areas has influenced the demand for rigid packaging profoundly.

The flexible packaging segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to its versatility and huge customization options. It comprises pouches, stretch films, shrink films, liners, wraps & film rolls for packaging of a wide range of products. The rapid growth in travelling due to presence of working individual the demand for such packaging is growing. The increasing need of small batch packaging of products has raised the demand for this segment.

China held the largest share in the Asia Pacific plastic packaging market in 2024, due to presence of huge manufacturing hub and customer base. This region is important in the acceptance of new technologies, comprising robotics, smart packing, and sustainable resources, which allows effectual innovation and production. Advance recycling technology for plastic packaging waste has raised the demand for this market. Huge demand for packaged products due to changing lifestyle of the consumers has evolved this market to grow rapidly. The rapid growth of pharmaceutical, food & beverage, cosmetic, and electronics sector has fuelled the demand for this market.

Rising disposable earning and increasing consumption of packaged products have enhanced the demand for the market. The rapid extension of the e-commerce sector directly influences the requirement for varied, strong, and visually attractive packaging option to help online purchases. It is frequently more cost-operative and provides a mixture of advantages such as durable, lightweight, and offering a good shelf-life for packaged products. The increasing demand for long-lasting and convenient packaging, and also rising emphasis on innovative and sustainable packaging option facilitate suggestively to the expansion of the market.

Australia mandates that 100% of packaging be reusable, recyclable, or compostable by 2025, with strong emphasis on reducing problematic single-use plastics. This initiative is pushing companies toward redesigning plastic packaging formats and investing in recyclable and compostable material innovation.

India requires at least 30% recycled content in PET bottles and packaging from 2025, increasing progressively to 60% by 2029. This policy accelerates demand for recycled plastics and forces FMCG and beverage companies to integrate circular economy practices into packaging design.

Countries such as Indonesia, Malaysia, and the Philippines are rolling out EPR systems that make producers responsible for post-consumer plastic packaging waste. These programs shift financial and operational responsibility to brands, incentivizing the reduction, reuse, and improved recyclability of packaging.

Thailand is advancing a comprehensive regulatory framework covering the full lifecycle of packaging materials, including plastics. The law aims to enforce eco-design, waste reduction, and recycling requirements, making it one of the region’s most holistic packaging regulations.

Several Asia-Pacific economies have adopted targets such as recycling 50% of plastic packaging by 2025 and moving toward 100% by 2030. These targets are driving infrastructure investment, waste collection systems, and innovation in recyclable plastic packaging formats.

Thailand and other regional governments are implementing bans on plastic scrap imports (e.g., Thailand by 2025) to control domestic waste streams. This policy encourages local recycling capacity development and reduces reliance on imported plastic waste for processing.

By Product Type

By Material Type

By Application / End-Use

By Packaging Type

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarAsia Pacific Plastic Packaging Market