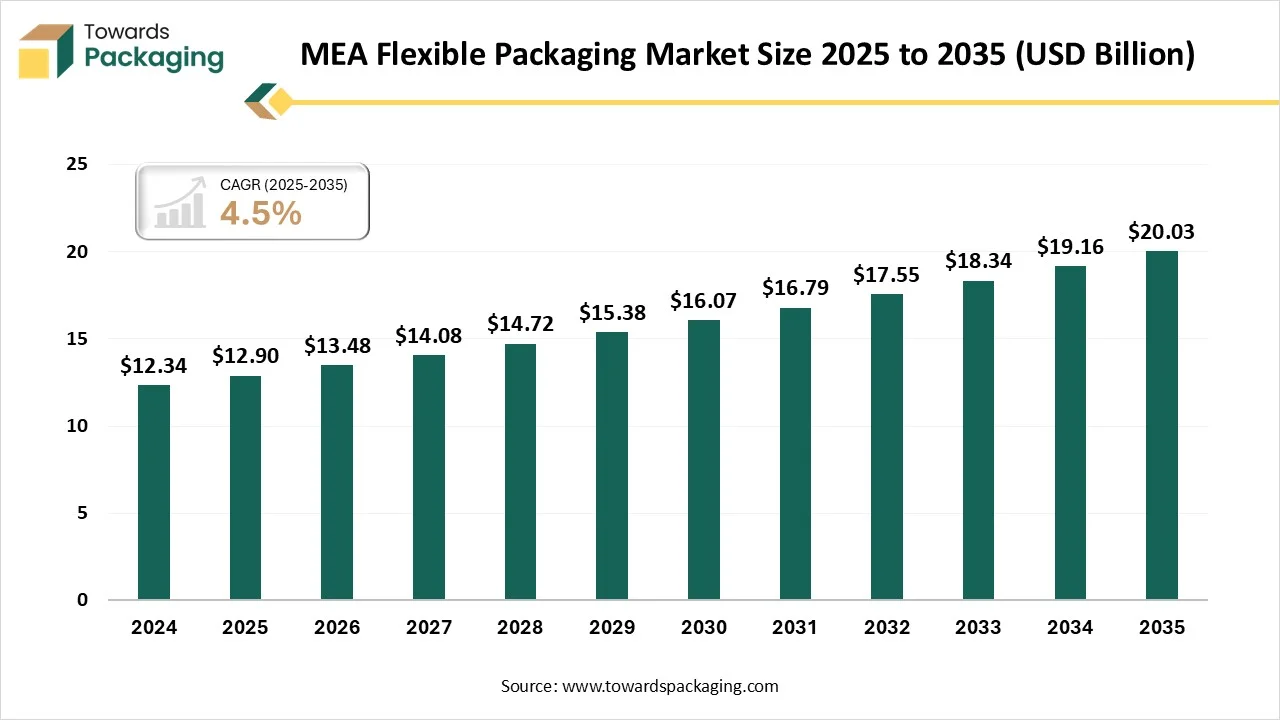

The MEA flexible packaging market is projected to grow from USD 13.48 billion in 2026 to USD 20.03 billion by 2035, expanding at a CAGR of 4.5% during 2026–2035. The market is driven by rising e-commerce demand across the Middle East & Africa, increasing need for lightweight plastics such as padded envelopes, bubble wraps, and custom-fit pouches that reduce shipping costs and improve product safety.

This report covers detailed market size data, segment-wise analysis, regional insights across NA, EU, APAC, LA, and MEA, along with company profiles, competitive landscape, value chain analysis, trade statistics, and comprehensive manufacturers and suppliers data.

The Middle East and Africa (MEA) flexible packaging market is defined by its application of materials such as paper, plastic, bioplastics, and aluminium foil to make acceptable packages such as pouches, bags, blisters, and wraps. Main factors that shape the industry include rising demand from end-user industries like pharmaceuticals, food, and beverages, which is driven by the growing urban middle class and increasing e-commerce.

One of the main advantages is the crucial development in productivity. The automated systems include filling, feeding, and labelling into a single flow that reduces the cycle times, limits manual labor, and lowers downtime. This not only lessens operational costs but also decreases the risk of fatigue and human errors. In industries like pharmaceuticals and food, this smoothness is important for aligning with fewer deadlines and tracking the product integrity.

Raw Material Sourcing: The main raw material sourcing for the Middle East and Africa (MEA flexible packaging is plastics, which include biobased polymers and fossil- along with other materials like aluminium and paper foil for tailored uses. Because of developing sustainability efforts in the MEA region, producers are typically sourcing more recyclable and bio-based plastics while continuously using conventional polymers.

Component Manufacturing: Flexible packaging manufacturing plays a crucial role in making durable, versatile, and visually appealing packaging solutions for a huge range of products across different sectors such as beverages, food, personal care, pharmaceuticals, and household items.

Logistics and Distribution: Flexible plastic packaging plays a main role in the logistics and e-commerce sectors, in which protection, precision, and presentation are crucial. Prevalent uses count Stretch hood film and pallet wrap, which are used to protect big shipments on planets. They assist in protecting movement during transportation and protect goods from dirt, dust, and moisture in transport and storage, too.

")

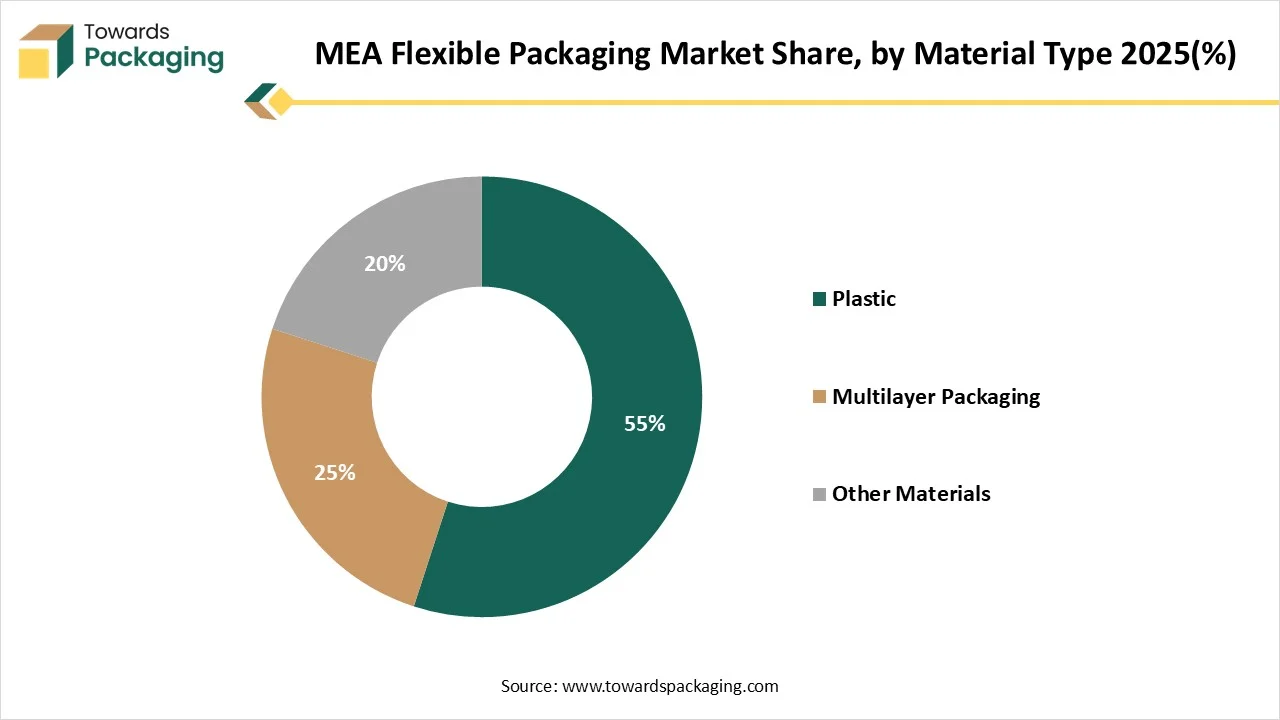

The plastic segment dominated the MEA flexible packaging market in 2025 as PE packaging, or the polyethylene packaging, is created from the most prevalently manufactured plastic in the world and is valued for its durability, low cost, and versatility too. The kind of PE packaging totally relies on the polyethylene’s density and its molecular pattern, with the most common variants being HDPE, LDPE, and LLDPE. On the other hand, polypropylene is an evergreen plastic that is prevalently used for a variety of work and is one of the most used plastics in plastic packaging. It is specifically famous in the pharmaceutical sector due to its reliable and chemical-opposite characteristics.

The multilayer packaging segment is predicted to witness the fastest cagr during the forecast period. This packaging is sustainable, it does not need much material, and can currently also be manufactured from chemically recycled material. It includes up to 11 single and ultra-thin layers that make it specifically thinner and lighter than comparable packaging. In addition to lowering the amount of raw materials utilised, this also includes selectively lowering C02 emissions during transportation.

| Product Type Segments | Market Share 2025 (%) |

| Pouches | 45% |

| Sachets & Stick Packs | 30% |

| Other Products | 25% |

The pouches segment dominated the MEA flexible packaging market in 2025 because flexible pouches have developed as one of the fastest-developing packaging designs across sectors due to their convenience, versatility, and sustainability advantages. Pouches use less material, which results in lower manufacturing costs as well as decreased transportation expenses. Flexible pouches also have a lesser environmental footprint, creating less greenhouse gas emissions during transportation and production.

The sachets & stick packs segment is expected to witness the fastest cagr during the forecast period. Flexible packaging continues to develop in favor among the consumer packaged goods 9CPG) producers due to several built-in benefits. The barrier properties, compact size, and cost-effectiveness of the flexible packaging create a packaging design selection for many kinds of products. Whereas, stick packs are tube-like and narrow flexible packaging pouches, which are perfect for the single-serve uses designed by busy users for convenience. They are prevalent; they are used for everything from powdered drink mixes and nutritional supplements to condiments, sweeteners, probiotics, and more.

| Film Type Segments | Market Share 2025 (%) |

| Multi-layer Films | 50% |

| Single-layer Recyclable Films | 30% |

| Other Films | 20% |

The single-layer films segment dominated the market in 2025 as they are economical and simpler. They are generally created from one kind of polymer, which makes them convenient to recycle and accurate for direct uses, such as agricultural films and shrink wraps, too. They are even recyclable, which makes them ideal for short-term or lesser urgency applications but restricted for long-term or heavy barrier uses.

The multi-layer films segment is expected to witness the fastest CAGR during the forecast period. This packaging remains at the front step of current packaging invention, changing how products are protected, preserved, and presented across industries. As users' urges for longer shelf life and sustainable results, and perfect protection continue to develop, multilayer film packaging has grown as a complicated technology that manages these complicated needs.

")

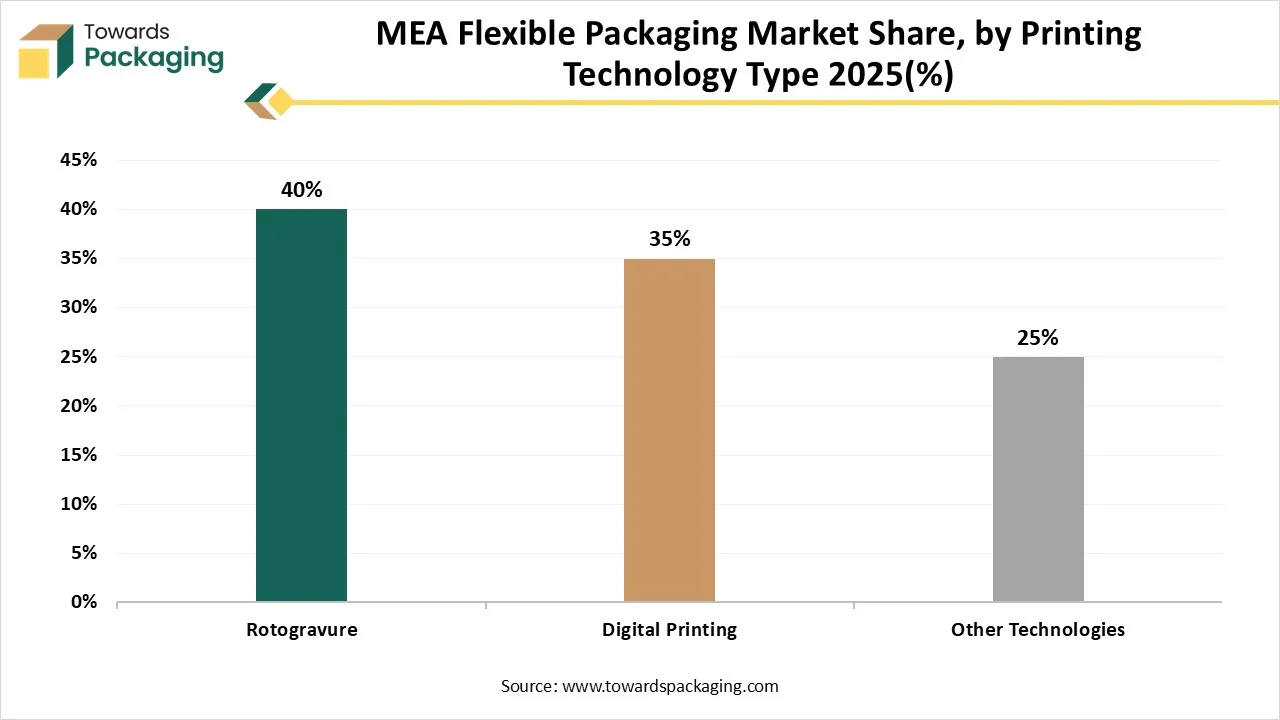

The rotogravure segment dominated the market in 2025, as this printing is a highly effective printing technique that is specifically perfect for long periods in flexible packaging. Its direct shift strategy of updating the pattern from the cylinder to the ground enables high-quality print quality, even at very high manufacturing speeds. This makes it the selected choice for bulk printing of flexible packaging, which ensures high productivity and sharpness on each reproduction print.

The digital printing segment is predicted to witness the fastest CAGR during the forecast period. It is a current, plate-free procedure of printing directly onto the flexible packaging foundation, such as rollstock films and pouches, too. Alike regular methods which use the fixed printing plates, digital printing utilises a computer file to print he respective image directly, which makes it perfect for personalization, fast turnaround, and shorter print runs too. By excluding the demand for production printing plates, digital printing mainly condenses the production procedure.

| Application Segments | Market Share 2025 (%) |

| Food & Beverage | 60% |

| E-commerce Packaging | 20% |

| Other Applications | 20% |

The food and beverages segment dominated the market in 2025 as by using non-rigid materials to package food and beverage, producers are perfect that are enabled to tailor the container to fit the brand and the product. Flexible packaging is accessible in a variety of sizes, shapes, and materials, which can be made in either formed or unformed arrangements. Formed packaging is being pre-shaped and can be packed and sealed in-house, whereas unformed packaging comes on a platform that is sent to co-packers for filling and making.

The e-commerce segment is predicted to experience the fastest CAGR during the forecast period. The growth of e-commerce has updated packaging demands. The flexible designs, like bags and pouches, serve a space-saving and lightweight selection that reduces shipping costs and enhances the shelf appearance. Characteristics such as spouts, resealable zippers, and easy-tear notches are heavily prevalent and need compatible premixed products that do not adjust mechanical honesty or aesthetics.

| Distribution Channel Segments | Market Share 2025 (%) |

| Direct Sales | 50% |

| Online B2B Platforms | 30% |

| Other Channels | 20% |

The direct sales segment dominated the MEA flexible packaging market in 2025, as direct sales of the flexible packaging include producers that sell their products directly to organizations, which bypass mediators like wholesalers and distributors. A direct sale design can lower total costs by avoiding the middleman’s routine. The material -effective nature of the flexible packaging also lowers the storage and transportation expenses. It works directly with the producer that gives clients permission to technical expertise for selecting materials and developing the smoothest packaging design.

The online B2B platforms segment is expected to have the fastest CAGR during the forecast period. Flexible packaging is hugely useful for online sales with the assistance of main e-commerce sites, tailored business-to-business industry, and directly from the producers and suppliers who serve online ordering and personalization. Several producers serve direct online ordering for the high-volume flexible packaging that includes custom printing and pouches online, from the coffee bag to stand-up pouches.

The Middle East has dominated the market in 2025 as the demand for it in this region is developing mainly due to rising disposable incomes, urbanization, and the expansion of food, beverage, and pharmaceutical industries. Market Development is filled by user choice for sustainability, convenience, and cost-effective packaging solutions, too.

Saudi Arabia is heavily funding healthcare infrastructure, and the urge for flexible packaging, which ensures integrity and product safety, is increasing. On the other hand, the UAE causes confusion for dual-language packaging -Arabic and English both. Flexible laminate pouches serve a huge space to count both languages precisely, along with nutritional data, barcodes, safety symbols, and expiration dates too.

The MEA Flexible Packaging industry is predicted to have the fastest compound annual growth rate in Africa and Nigeria because the demand for flexible packaging in Africa is growing and developing, fueled by fast urbanization, increasing usage of packaged goods, and a growing middle class. Flexible packaging is utilised to protect and extend the shelf life of pharmaceutical products such as powders, creams, tablets, and wipes, too. As healthcare infrastructure develops, so does the urge for this kind of packaging. The move of people to the urban centres and the development of a middle class are increasing the demand for ready-to-eat, packaged, and on-the-go food and beverage products.

By Material Type

By Product Type

By Film Type

By Printing Technology

By Application

By Distribution Channel

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarMEA Flexible Packaging Market