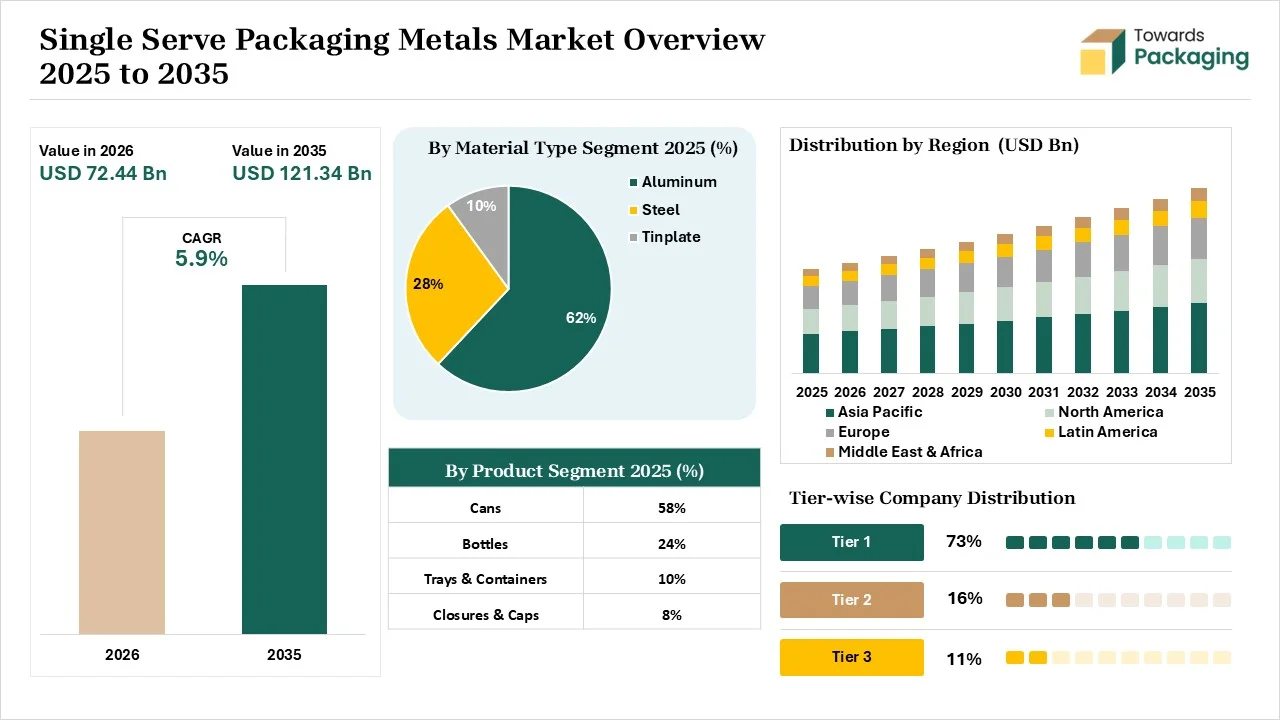

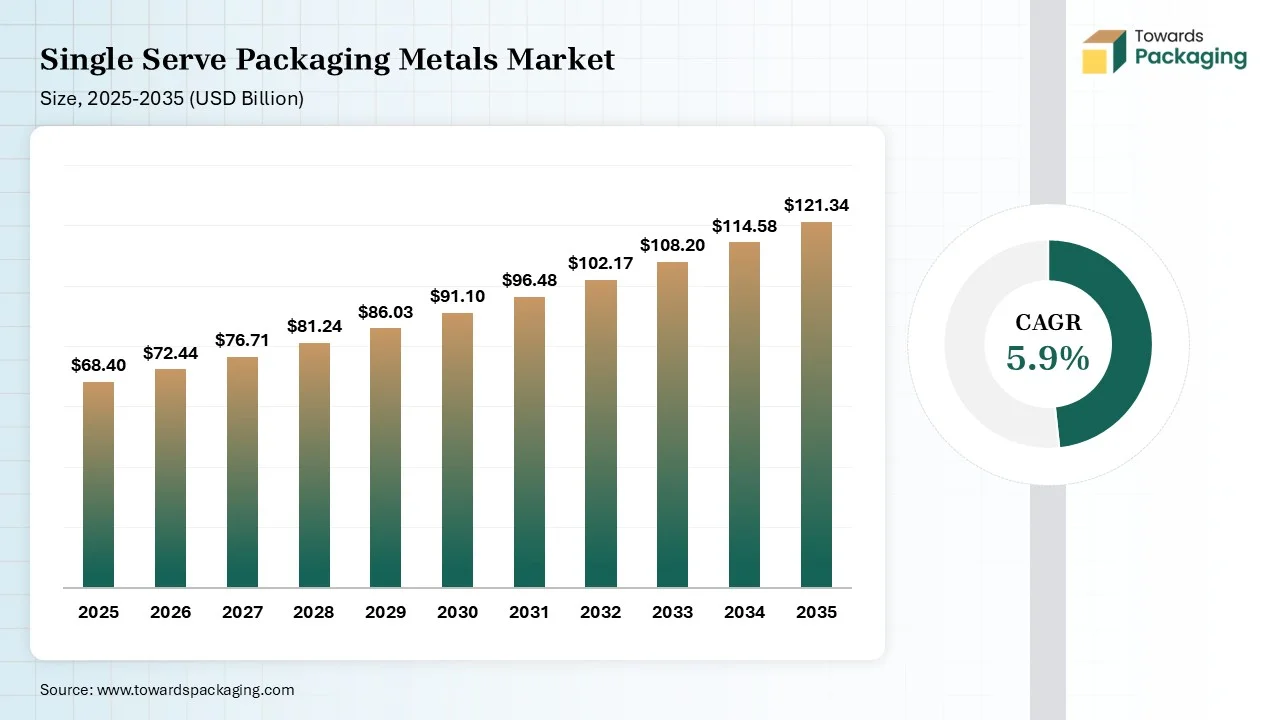

The single serve packaging metals market is projected to grow from USD 72.44 billion in 2026 to USD 121.34 billion by 2035, registering a CAGR of 5.9% during the forecast period. The report provides a complete breakdown of market size along with detailed segment data by material type, packaging format, and end-use industries. It also includes comprehensive regional analysis, key company profiles, competitive landscape assessment, value chain evaluation, trade data, and detailed information on manufacturers and suppliers. Growth is driven by rapid urbanization and rising demand for high-barrier, convenient packaging solutions.

Single serve packaging metals are mainly tinplate (tin-coated steel) and aluminum, offer impermeable resistance, durable, and lightweight for separate portions of food & beverages, safeguarding against oxygen, light, and moisture. Universal examples comprise tear-off coffee pods, beverage cans, snack foil, and yogurt lids, all selected for their limitless recyclability and capability to be simply shaped.

AI has transformed the process that involves steel tubes, specialized foil seals, and aluminum cans. Smart, eco-friendly, and data-driven comfort has bolstered the market ecosystem, while smart packaging is at the heart of the AI-driven approaches aligned best with the awareness and safety measures. AI addresses new alloy coverings and mergers, which work wonders for the barrier properties. While the AI generative design encourages infinite design variations for the strong metal closures and aluminum containers.

Technological transformation in the single serve packaging metals market plays a significant role in enhancing consumer experience with digital integration. The increasing lightweight packaging demand advancement in the manufacturing process. The incorporation of AI support in the production of packaging with monitoring freshness of the products. The rising adoption for digital printing and huge customisation has fuelled the demand for this industry.

The major raw materials utilised in this market are aluminum, tinplate, tin-free steel, stainless steel, and Electrolytic Chromium Coated Steel (ECCS). These are useful in enhancing the quality of the packaging that offer enhanced protection to the packaged products.

The component manufacturing in this market comprises aluminum foil & lids, cans, tin containers, steel cans, and trays. These are useful in preserving the quality of the packaged products.

This segment ensures the reduction of carbon emission and low transport charges. It assures high quality control of the packaged products.

Key Players: Sonoco Metal Packaging, Pipeline Packaging

The aluminum segment dominated the market with 62% share in 2025, and it is expected to experience the fastest growth in the market with 6.40% CAGR during the forecast period. Due to its infinite recyclable potential, lightweight, and enhanced corrosion resistance. It is widely used in the pharmaceutical industry as it has excellent protection capacity. The rapid shift towards aluminum packaging of the beverage companies has fuelled the growth of this industry.

The steel segment held the 30% market share in 2025. Due to its cost-effectiveness, durability, and high strength. These are considered as an ideal solution for the packaging and preservation of food, beverages, and dairy products. These are widely used for the packaging of aerosols and carbonated drinks.

The other metals segment held the 8% market share in 2025. Due to its high recyclability properties, lightweight nature and enhanced corrosion resistance. The increasing adoption of sustainable packaging of majority brands fuelled the demand for this segment. It ensures the preservation of freshness of the packaged products.

The cans segment dominated the market with 58% share in 2025. Due to its capacity to protect freshness of the products and its enhanced recyclability. There is a huge growth in the portable packaging which has raised the demand for this segment. The rising consumption of canned food and beverages ha raised its production process.

The bottles segment held 14% market share in 2025 and expected to experience the fastest growth in the market with 6.3% CAGR during the forecast period. Due to enhanced consumer convenience and huge area for branding. It is considered as a suitable option for the packaging of on-the-go food and beverages. It is majorly used for the packaging of premium beverages.

The trays & containers segment held the 18% market share in 2025. Due to increasing demand for protective packaging solution with high durability and portability. It has enhanced moisture barrier properties which has protected packaged products against light, oxygen, and moisture. It has enhanced the shelf life of the products and raised convenience for on-the-go food products.

The foils & wraps segment held the 10% market share in 2025. Due to its high recyclability and enhanced moisture barrier properties. These are extensively used for the packaging of ready-to-eat food products, snacks, and candy. It is highly versatile that has raised customisation option in the food packaging sector.

The 250–500 ml segment dominated the market with 46% share in 2025. Due to increasing portion control demand and on-the-go consumption of food products. These can be easily recyclable and protect products form damage. These are cost-effective packaging solutions due to its mass production.

The above 500 ml segment held 14% market share in 2025 and expected to experience the fastest growth in the market with 6.2% CAGR during the forecast period. Due to the rising demand for huge size family beverage packages has enhanced the production of these packaging. The increasing consumption of beverages among people has fuelled the production of this segment. It is cost-effective solution as it has less per unit production charge.

The 100–250 ml segment held the 28% market share in 2025. Due to the rising demand for premium packaging and branding of the products. The increasing adoption of premium personal care products has raised the production of these containers. The rising demand for portion control among youth has also raised the adoption of these packaging.

The below 100 ml segment held the 12% market share in 2025. Due to increasing premium skincare brands. The huge utilisation of premium perfumes has also raised the production of these containers. It provides digital printing space to build a unique identity of the brand.

The beverages segment dominated the market with 44% share in 2025, and it is expected to experience the fastest growth in the market with 6.60% CAGR during the forecast period. Due to its superior potential to preserve freshness of the food products. The beverages industry has raised the utilisation of aluminum cans which has raised its production process. There is a huge demand for packaging that support in enhancing the shelf life of the packaged products.

The food segment held the 34% market share in 2025. Due to changing lifestyle of the people and rapid urbanisation. These packaging ensure the safety of the products from external agent like moisture, oxygen, and light. It has the potential to store products contamination-free and fresh for longer period.

The pharmaceuticals segment held the 8% market share in 2025. Due to its impermeable barriers, non-toxic, and enhanced protection properties. These are moisture-proof, air-tight, and light-tight containers which are suitable for packaging of sensitive drugs. The rapid shift for unit-dose packaging improves patient security and drug supply accessibility in home and hospital settings.

The personal care & cosmetics segment held the 7% market share in 2025. Due to the presence of strict guidelines in the packaging industry. The upsurge in luxury brands has fuelled the demand for this segment. It provides superior protection with light-proof resistance. These are premium substitute such as tin and aluminum which is used to establish unique pattern.

The industrial segment held the 7% market share in 2025. Due to its enhanced durability and high reusability. These are considered ideal for the transportation of hazardous materials, chemicals, and liquid. It offer enhanced barrier protection and sustainability with excellent corrosion resistance.

Asia Pacific dominated the single serve packaging metals market with 38% share in 2025, and it expects the fastest growth in the market with 6.80% CAGR during the forecast period. Due to rapid urbanization and rising middle class earning has fuelled the demand for huge production of these containers. There is a huge shift towards lightweight and innovative packaging has fuelled the demand for this sector. The rapid expansion of e-commerce sector has fuelled the demand for packaging with enhanced safety assurance boost the development in this industry.

China Single Serve Packaging Metals Market Trends

The rapid shift towards recycled packaging material has fuelled the development of the market in China. The presence of huge manufacturing capacity has fuelled the demand for high adoption of these packages. These are low-cost and high-efficiency packaging used in a wide range of industries. The rising sustainability in the packaging sector has pushed this industry to grow significantly.

North America held the 24% market share in 2025. The increasing demand for recyclable packaging has pushed the demand for the single serve packaging metals market in the North America. The rising demand in the pharmaceutical and processed food packaging. The rapid enhancement in the demand for convenient packaging and changing lifestyle of the people.

The U.S. Single Serve Packaging Metals Market Trends

The rising demand for convenient packaging has fuelled the development of the market in the U.S. The presence of strict packaging guidelines has fuelled the production demand of this packaging as a sustainable alternative. It has enhanced barrier properties has fuelled the research and development in this sector. It has high barrier properties which has boosted the development of this industry.

Latin America is expected to grow at a notable CAGR in the foreseeable future, due to exceeding demand for sustainable alternatives to finally say no to plastic. The upcoming OneCan International Metal Packaging Congress event, planned by ABEACO, Abralatas, and ABAS for April 2027 schedules the best-in-class, accurate detailing on the whole metal packaging value chain. The company's initiatives are extending the potential of aluminum aerosol to serve promising solutions to the personal care and cosmetic packaging lines.

Argentina Market Trends

Argentina revolutionized, leaving traditional methods and approaches behind, and now stepping into the green packaging marks a valuable upgradation into the materials and processes as well. The ‘on-the-go’ consumption trend is promoting the lightweight alternatives to manage the busy lifestyle of individuals and help them carry their ready-to-eat food with no extra weight of the container.

Europe is considered to be a significantly growing area, due to the expansion in this industry, which is exceeding with the creative growth in craft breweries and thinner metal. The ready-to-drink cocktails are a big cheer for the designs and fascinating innovations on the pack/can. The sustainable automated production is attracting acquisitions. This takes the regional market approaches and excellence overseas with more expertise and accuracy, driving the effective expansion.

Germany Market Trends

Ready-to-eat meals are attracting more business to the regional market, with the massive use of metal containers confirming heavy revenue for the market. Germany's government rule of deposit return systems has accelerated the purchases of metal cans, driving smart profit to the consumers and sellers both.

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Ball Corporation | Westminster, Colorado | USA | Global leader in aluminum beverage cans and single-serve packaging solutions | Beverage cans and specialty metal packaging |

| 2 | Crown Holdings | Tampa, Florida | USA | One of the world's largest manufacturers of beverage and food cans | Beverage cans, food cans, closures |

| 3 | Ardagh Metal Packaging | Luxembourg City | Luxembourg | Major supplier of aluminum beverage cans for global brands | Beverage cans and specialty metal containers |

| 4 | CANPACK | Kraków | Poland | Leading producer of beverage cans and metal packaging solutions | Aluminum beverage cans |

| 5 | Silgan Holdings | Stamford, Connecticut | USA | Global supplier of food cans, closures, and metal containers | Food cans and metal packaging |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Toyo Seikan Group | Tokyo | Japan | Major supplier of beverage and food metal packaging in Asia and globally | Beverage cans and food containers |

| 2 | CPMC Holdings | Hong Kong | China | Significant producer of metal packaging products and beverage cans | Beverage and food cans |

| 3 | Baosteel Packaging | Shanghai | China | Leading packaging steel and metal can manufacturer | Metal beverage and food packaging |

| 4 | Massilly Group | Mâcon | France | Specialist in food cans, aerosol cans, and metal closures | Food packaging and closures |

| 5 | Colep Packaging | Vale de Cambra | Portugal | Producer of aerosol and specialty metal packaging formats | Aerosol and consumer packaging |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Envases Universales | Mexico City | Mexico | Major regional supplier of beverage and food metal packaging | Metal containers and cans |

| 2 | Tecnocap Group | Cava de' Tirreni | Italy | Specialist in metal closures and specialty containers | Closures and metal packaging |

| 3 | Huber Packaging Group | Öhringen | Germany | Producer of industrial and specialty metal packaging | Metal containers |

| 4 | Jamestrong Packaging | Melbourne, Victoria | Australia | Manufacturer of beverage and specialty metal packaging | Beverage cans and containers |

| 5 | Sonoco Metal Packaging | Hartsville, South Carolina | USA | Supplier of metal food packaging and specialty containers | Metal food cans and containers |

By Material Type

By Product Type

By Capacity

By End-Use Industry

By Closure Type

By Distribution Channel

By Regions

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarSingle Serve Packaging Metals Market