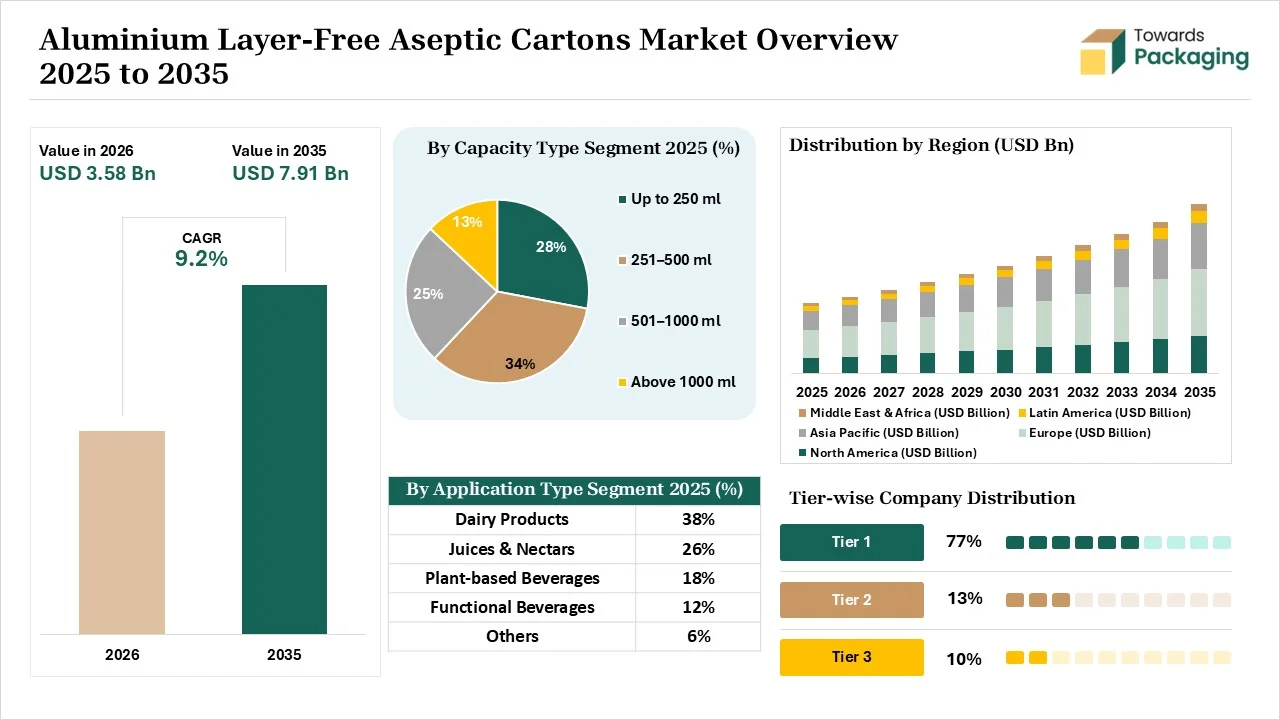

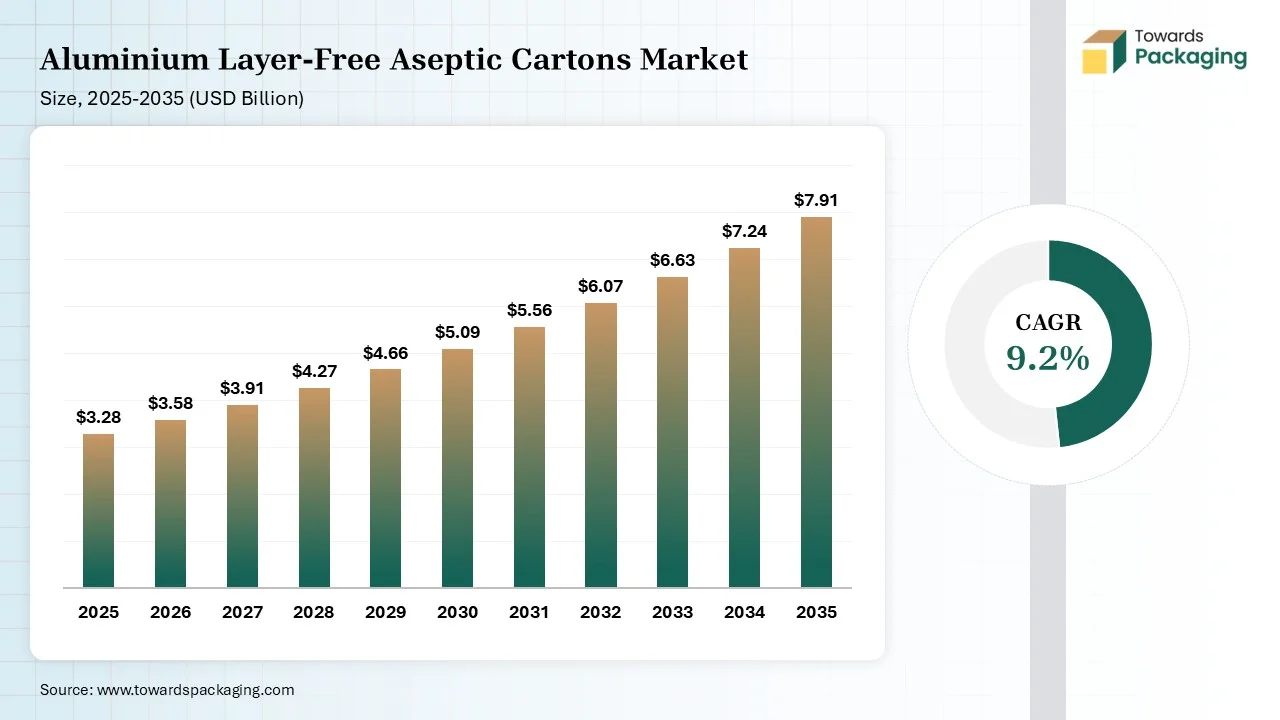

The aluminium layer-free aseptic cartons market is projected to grow from USD 3.58 billion in 2026 to USD 7.91 billion by 2035, registering a CAGR of 9.2% during the forecast period. The study covers detailed market size estimations, market share analysis, growth drivers, restraints, opportunities, segment-wise performance, regional outlook, competitive benchmarking, company profiles, value chain assessment, trade flow analysis, manufacturing trends, supplier evaluation, pricing analysis, and strategic developments shaping the global industry landscape.

Aluminium layer-free aseptic cartons are packaging solutions made from sustainable material that does not contain an aluminium foil barrier. The packaging has a paper-heavy structure and contains polymer barriers. It is compatible with plug-and-play and requires simplified recycling. The benefits like maintained shelf life, substantial carbon reduction, and optimized packaging structure, are offered by the packaging format. Aluminium layer-free aseptic cartons are used across juices, liquid creams, plant dairy, nectars, whipping toppings, flavored dairy, and many others.

The aluminium layer-free aseptic cartons packaging market is growing due to the advancements in barrier technologies, huge popularity of plant-based beverages, burgeoning retail infrastructure, focus on fuel emission savings, higher demand for affordable beverages, expanding paper content, and massive carbon reduction goals.

The aluminium layer-free aseptic cartons market is experiencing several technological developments like predictive maintenance, digital twin, computer vision, predictive barrier modeling, and machine learning. The demand for optimizing speeds of filling lines, streamlining recycling, and maximizing renewable content is responsible for ongoing technological developments in the market. Artificial intelligence is the leading technological development in the market.

AI minimizes the thickness of polymer layers and performs machine synchronization. AI optimizes throughput and prevents machine failures. AI finds perfect combinations of polymer barrier and natural fiber. AI detects inconsistencies in production and improves recyclability. AI offers manufacturing precision and easily finds new barrier materials. Overall, AI enhances sorting optimization and offers sustainable design.

Raw materials like plant-based polymers and paperboard are required for aluminium layer-free aseptic cartons.

Material processing involves steps like paperboard manufacturing, polymer extrusion, and barrier coating formulation. Conversion includes steps like printing, lamination, and creasing.

Package design focuses on material selection, choosing a polymer barrier, structural adaptation, graphic design, sterilization, and End-of-Life optimization. Prototyping focuses on LCA, commercial-scale trials, material substitution, and recyclability validation.

The 251-500 ml segment dominated the market with 34% share in 2025 due to its suitability for coffee consumption. The growing consumption of diverse drinks outside the home and the rise in single-serving increases the use of the 251-500 ml range. The popularity of protein shakes and the awareness of sugar intake have increased the use of the 251-500 ml range. The compatibility of 251-500 ml size with cup holders and the rise in portion-controlled nutrition drives the segment growth.

The up to 250 ml segment held the 28% market share in 2025 due to the growing use by busy consumers. The increased production of functional-shot packs and the rise in portion-controlled households increase the adoption of up to 250 ml sizes. The expansion of flavored milk and sugar tax evasion increases adoption of up to 250 ml sizes. The fast-paced routines and the burgeoning energy shots industry support the segment growth.

The 501-1000 ml segment held the 25% market share in 2025 due to the growing use in multi-person households. The expansion of oxygen-sensitive products and the focus on minimizing extra capital expenditure increase the use of the 501-1000 ml range. The growing number of beverage producers and the rise in weekly household purchases of beverages increase the adoption of 501-1000 ml size, boosting the segment growth.

The dairy products segment dominated the market with 38% share in 2025 due to the flavor degradation in liquid milk. The growing consumption of eco-conscious dairy and the rising UHT milk transportation increase the use of aluminium layer-free aseptic cartons. The photosensitiveness of milk ingredients and the focus on storing milk for a longer time increase the adoption of aluminium layer-free aseptic cartons. The expansion of dairy beverages drives the segment growth.

The juices & nectars segment held the 26% market share in 2025 due to interest in consuming fruit juices. The juice consumers' preference for clean-label and the EPR targets in the juice industry increases the use of aluminium layer-free aseptic cartons. The focus on protecting fruit juices and the presence of oxygen-sensitive contents in nectars increase the adoption of aluminium layer-free aseptic cartons, supporting the overall segment growth.

The plant-based beverages segment held the 18% market share in 2025 due to the consumer focus on environmental health. The high soy milk consumption and the focus on shelf-stability in plant-based beverages drive the adoption of aluminium layer-free aseptic cartons. The increased purchasing of plant-based products and the lactose-free alternatives demand boost the overall segment growth.

The paperboard-based barrier coated cartons segment dominated the market with 52% share in 2025 due to its uncompromised food safety. The focus on packaging emission reduction and the need to lower the refrigeration of the product increases the adoption of paperboard-based barrier coated cartons. The development of circular-economy products and long-distance distribution increases the use of paperboard-based barrier coated cartons. The structural integrity and optimized recyclability of paperboard-based barrier coated cartons drive the overall market growth.

The polymer-coated fiber-based cartons segment held the 33% market share in 2025 due to the focus on packaging structure simplification. The food protection needs and the shift away from metallic layers in packaging increase the use of polymer-coated fiber-based cartons. The reduction of cartons’ carbon footprint and the focus on shelf-stability of perishable goods increase the adoption of polymer-coated fiber-based cartons. The improved moisture resistance supports the overall segment growth.

The bio-based barrier cartons segment held the 15% market share in 2025 due to the brand's focus on cutting emissions. The strong paper recycling streams and the focus on the safety of perishable liquids increase the adoption of bio-based barrier cartons. The established specialized facilities and the transition away from metallic waste increase the use of bio-based barrier cartons. The expanded renewable packaging solutions boost the segment growth.

The brick-shaped cartons segment dominated the market with 55% share in 2025 due to its excellent storage efficiency. The focus on high-density displays in supermarkets and the need to lower the overhead of shelf management increases the adoption of brick-shaped cartons. The rise of quick restocking in the retail industry increases the use of brick-shaped cartons. The maximum space utilization, superior stackability, easy handling, and cube optimization of brick-shaped cartons drive the segment growth.

The gable top aseptic cartons segment held the 25% market share in 2025 due to the major manufacturers' shift to eco-friendly materials. The growing dairy distribution and the higher production of plant-based beverages increase the use of gable top aseptic cartons. The eco-friendliness, enhanced convenience, improved recyclability, and technological advancements in the gable top aseptic cartons boost the segment growth.

The slim/edge-shaped cartons segment held the 20% market share in 2025 due to its optimized palletizing. The increased buying of fortified beverages and the focus on the premium shelf in crowded retail shelves increase the use of slim/edge-shaped cartons. The growing demand for visually differentiated packaging helps with expansion. The enhanced portability, space efficiency, and optimized packing of slim/edge-shaped cartons support the segment growth.

The retail segment dominated the market with 62% share in 2025 due to the demand for ambient shelf stability. The circular-economy goals of the retail industry and modern shoppers' preference for natural foods increase the use of retail distribution. The growing perishable beverage consumption and the expanding supermarkets help with expansion. The transition to ultra-thin polymer drives the segment growth.

The foodservice segment held the 18% market share in 2025 due to the shift away from using preservatives. The regulations in food service brands and the growing modernization of cartons increase the use of aluminium layer-free aseptic cartons. The rise in institutional beverage dispensing and the expanded culture of cafes support the segment growth.

The institutional supply segment held the 12% market share in 2025 due to the shift away from multi-layer cartons. The burgeoning number of public institutions and the elimination of metal foils increase the use of aluminium layer-free aseptic cartons. The expansion of plug-and-play production helps with the growth. The expanded private institutions boost the overall segment growth.

Europe dominated the market with a 40% share in 2025 due to the shift away from high-carbon resources in the packaging sector. The developed carton recycling systems and the interest in aluminium-free solutions increase the adoption of aluminium layer-free aseptic cartons. The aggressive packaging regulations and the transitioning away from foil-lined cartons in the food industry increase the use of aluminium layer-free aseptic cartons. The strong juice sector drives the overall growth of the market.

Asia Pacific held 27% share in the market and is expected to grow at the fastest CAGR of 9.80% during the forecast period due to the focus on enhancing the packaging industry's sustainability metrics. The rise in packaging of plant-based drinks and the high consumer demand for convenient packaged food increase the adoption of aluminium layer-free aseptic cartons. The increased spending on natural juices and the move towards fiber-based structures support the overall market growth.

North America held the 22% market share in 2025 due to the strong recycling targets. The high consumption rate of RTD and the focus on minimizing GHG emissions in the carton manufacturing increase the use of aluminium layer-free aseptic cartons. The vast continental distribution and the preference for lighter packaging structures increase the use of aluminium layer-free aseptic cartons. The interest in convenient beverage formats boosts the market growth.

Latin America held the 7% market share in 2025 due to the shift away from traditional aseptic cartons. The established cold-chain infrastructure and the popularity of plant-based milks increase the adoption of aluminium layer-free aseptic cartons. The preference for using renewable content in packaging and the need to maintain a constant cold chain increase the use of aluminium layer-free aseptic cartons. The interest in healthy beverages supports the market growth.

The Middle East & Africa held the 4% market share in 2025 due to the need to reduce cartons’ carbon footprint. The higher requirement for preservatives and the presence of urbanized centers increase the production of aluminium layer-free aseptic cartons. The strong domestic waste management ecosystem and green initiatives increase the use of aluminium layer-free aseptic cartons. The expansion of RTE packaging items boosts the market growth.

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products and Services |

| 1. | SIG Group AG | Schaffhausen, Switzerland | Switzerland | The company offers this packaging for oxygen-sensitive products. |

|

| 2. | Tetra Pak International S.A. | Pully, near Lausanne, Switzerland | Switzerland | The company manufactures the first paper-based barrier and focuses on advancing recyclability. |

|

| 3. | Elopak ASA | Oslo, Norway | Norway | The company is developing low-carbon alternatives and manufactures aluminium-free cartons. | Pure-Pak eSense |

| 4. | Amcor plc | Zurich, Switzerland | Switzerland | The company provides AmLite technology for the Alu-free industry and focuses on the utilization of bio-based barriers. |

|

| 5. | Greatview Aseptic Packaging Co., Ltd. | Beijing, China | China | The company is a leading distributor of aseptic packaging materials and focuses on eco-packaging innovation. |

|

By Capacity

By Application

By Material Structure

By Packaging Type

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarAluminium Layer-Free Aseptic Cartons Market