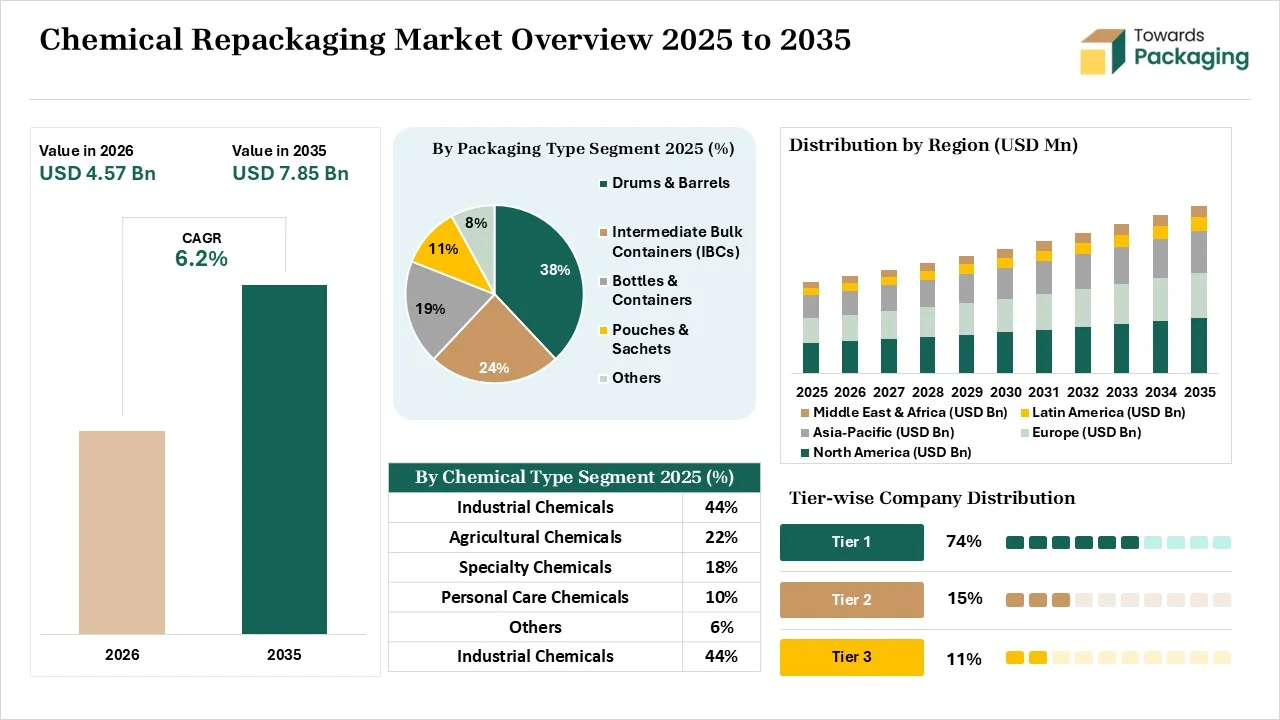

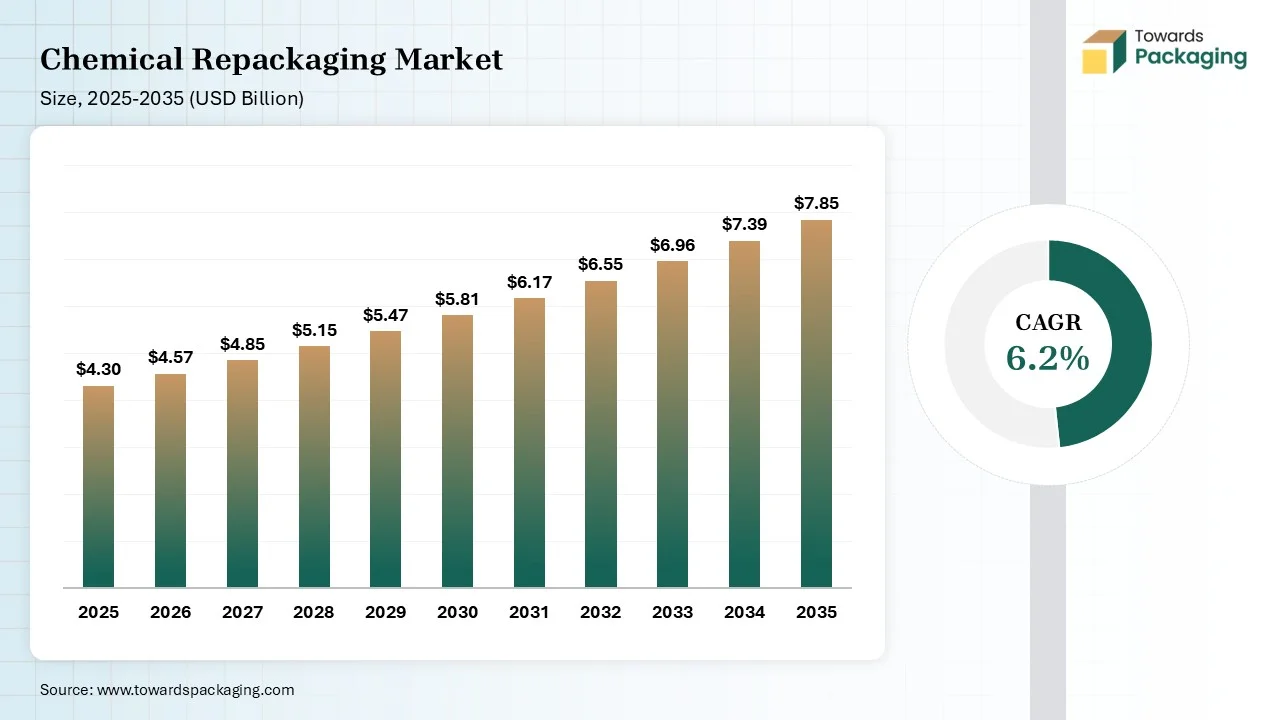

The chemical repackaging market is forecasted to expand from USD 4.57 billion in 2026 to USD 7.85 billion by 2035, growing at a CAGR of 6.2% from 2026 to 2035. This report covers complete market statistics including 2024 base-year metrics where North America held 33% share, drums & barrels contributed 38%, and industrial chemicals accounted for 44% of global revenue. It also includes segment-wise forecasts, regional analysis across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, competitive landscape of leading companies like Brenntag, Univar, and Safapac, full value chain evaluation, trade flows, and detailed supplier/manufacturer profiling.

The chemical repackaging market focuses on the transfer of chemicals from bulk containers into smaller or customized packaging units to suit distribution, regulatory, or customer-specific requirements. It supports industries like pharmaceuticals, agriculture, personal care, food & beverage, and industrial manufacturing. The market is driven by growing demand for safety, traceability, regulatory compliance (GHS, REACH), convenience packaging, and private labeling.

| Metric | Details |

| Market Drivers | - Demand for customized & compliant packaging - Regulatory mandates (OSHA, GHS, REACH) - Rise in specialty chemicals and eco-packaging demand |

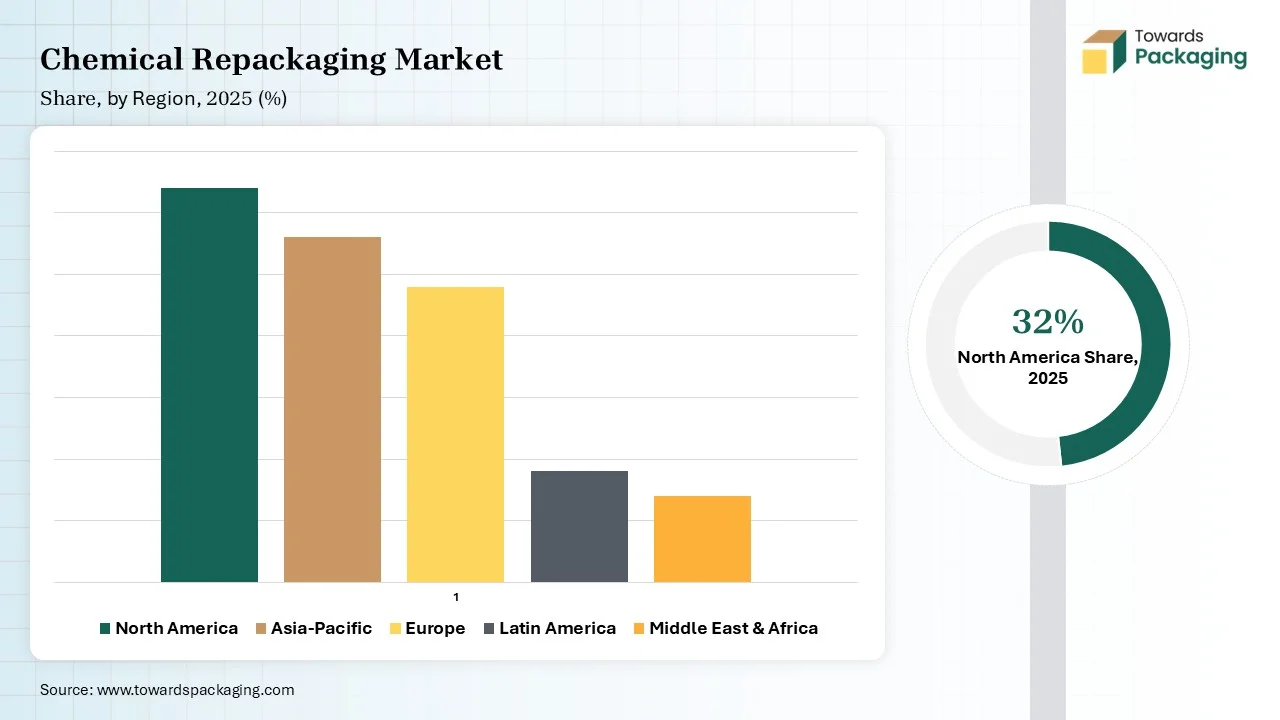

| Leading Region | North America |

| Market Segmentation | By Packaging Type, By Chemical Type, By Packaging Material, By Function, By End-Use Industry and By Region |

| Top Key Players | Brenntag AG, Safapac Ltd., Royal Chemical, SolvChem, Caldic B.V., Univar Solutions, Azelis, Avantor, Hydrite, Biesterfeld, Thermo Fisher, etc. |

The incorporation of AI in the chemical repackaging market plays an important role in enhancing operational efficacy, regulatory guidelines, and safety during the production process. This repackaging process becomes easy with the integration of AI, as it supports enhancing the speed of the production procedure. The incorporation of advanced technology, such as machine learning algorithms, helps to predict the demand of the market. Such a process helps to produce within limits and reduce the wastage of materials. Robotics technology helps in repetitive work, which reduces labour costs and helps to make these packages affordable.

Rising Demand for Customized Packaging Solutions

The continuous demand for customized packaging solutions in various industries has driven the development of the chemical repackaging market. The requirement of industries like specialty chemicals, agriculture, and pharmaceuticals has raised the demand for easy and safe maintenance of the products, which makes a repackaging facility essential for them. The rising strictness in the packaging necessities for labelling, chemical handling, and transportation. This repackaging market ensures compliance with worldwide standards like OSHA, GHS, and REACH, which decreases the risk of safety incidents and non-compliance penalties. The change in the direction of circular choices has prompted producers to accept reusable containers and sustainable resources in repackaging procedures.

Stringent Regulatory Landscape Hindered the Market Growth

The stringent regulatory landscape and transportation issues have hindered the growth of the chemical repackaging market. There is a huge risk for contamination, cross-reaction, or spillage during the time of repackaging process. Moreover, cost sensitivity is another major factor that has hindered the expansion of this market.

Rising Technological Innovation in the Repackaging Industry

Rising technological innovation in the repackaging sector has boosted several opportunities in the chemical repackaging market. The increasing demand for fine chemicals and specialty products in every sector has raised the scope for innovation, which ultimately enhances opportunities for this market. The rising demand for eco-friendly packaging has enhanced the innovation technology to produce chemical repackaging in an eco-friendly way. Automation and digitalization have enhanced the development scope of this market. The growing chemical consumption and huge storage infrastructure have boosted the development of the chemical repackaging market.

")

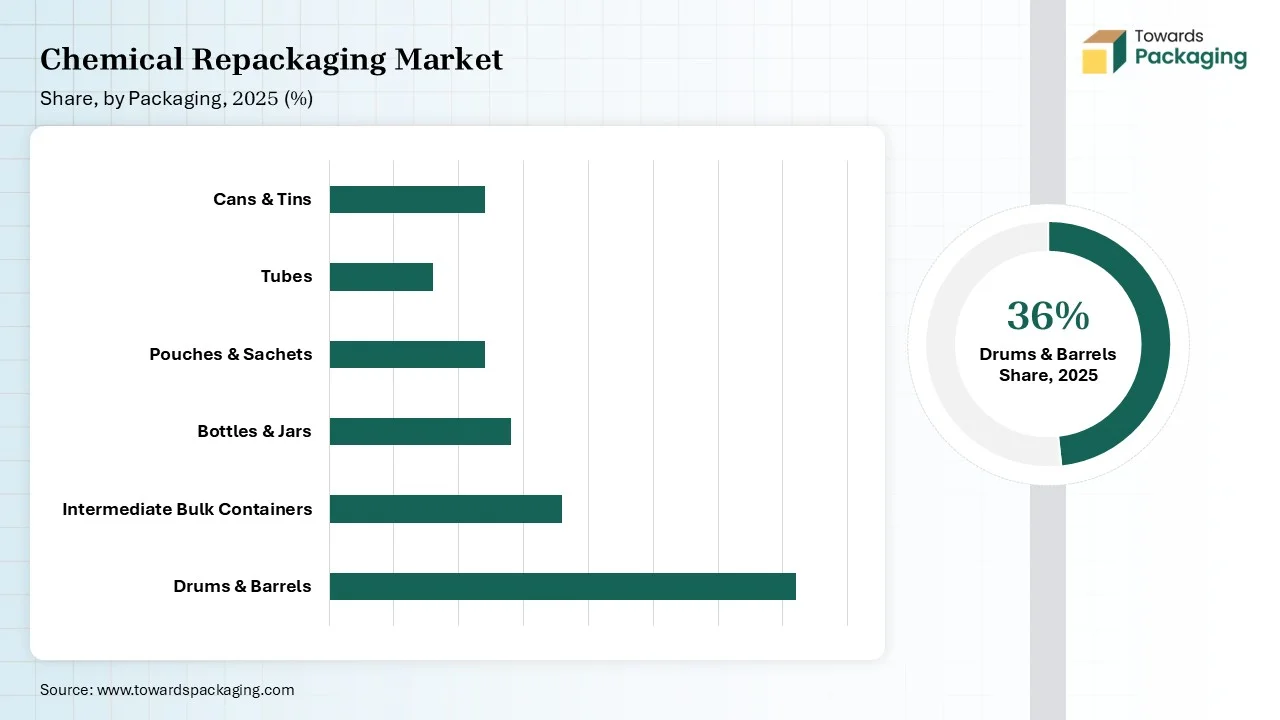

The drums & barrels segment contributed a considerable share of the chemical repackaging market in 2025 due to the compliance features, huge capacity, and strength of the drums. These are widely used for storage and transportation purposes of both hazardous and non-hazardous solids and liquids. Drums and barrels have high durability and are suitable for flammable and corrosive chemicals. The rising regulatory pressure, tamper-evident, and leak-proof packaging demand has enhanced the demand for this market.

The pouches & sachets segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. This segment is growing rapidly due to its cost-efficiency, rising alignment with sustainability requirements, lightweight, and convenience. Sachets provide single-use facilities such as lab reagents, fertilizers, and detergents.

The industrial chemicals segment is expected to have a considerable share of the chemical repackaging market in 2025 due to its scale, strong safety demand, and diversity. Industrial chemicals like gases, polymers, acids, and solvents are created in bulk and require safe and strong repackaging for storage purposes. The rising chemical trade worldwide has raised the demand for reliable repackaging. The increasing worldwide trade dynamics, huge volume, and regulatory requirements have influenced the demand for this market.

The personal care chemicals segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. The growing demand for customer dynamics, unique products, and packaging. The cost and packaging efficacy of personal care packaging attract brands and customers. The rising demand for enhanced protection from air, moisture, and other pollutants has influenced the demand for such packaging in this sector.

The industrial manufacturing segment is expected to have a considerable share of the chemical repackaging market in 2025 due to the rising demand for reliable packaging. There is a huge consumption of chemicals in the production of gases, petrochemicals, acids, solvents, and polymers. The increasing favour towards cost-efficacy, stackability, and reusability has improved the demand for repackaging. Strong safety standards have enhanced the demand for repackaging in the industrial manufacturing segment. Invention in smart packaging, sustainable resources, and barrier coating has influenced the demand for this market.

The pharmaceuticals segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. This segment is growing rapidly due to rising demand for safe and tamper-evident repackaging. The production of refillable packages to minimize the wastage of raw materials in the pharmacy sector has influenced the growth of this industry. This segment includes tamper-evident, serialization, clear labelling, and traceability facilities during the repackaging of products.

")

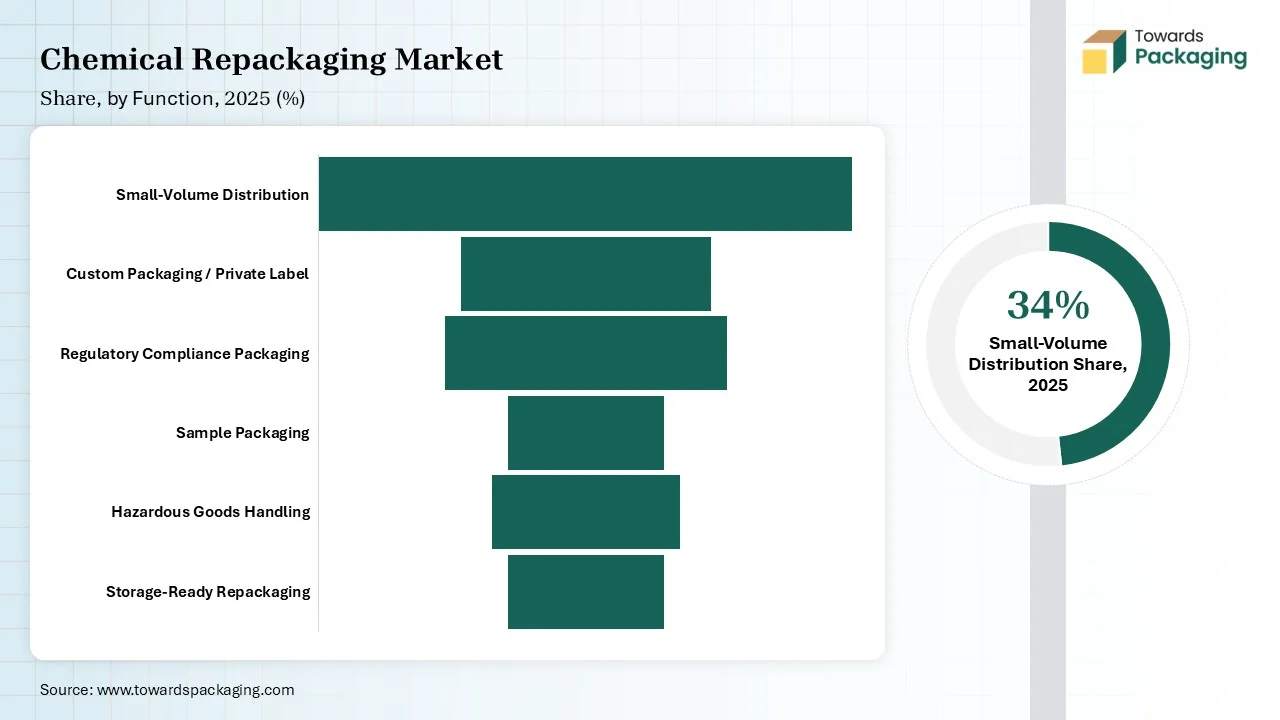

The small-volume distribution segment is expected to have a considerable share of the chemical repackaging market in 2025 due to its wide customization options and agile logistics. The availability of tailored packaging solutions for packages such as small containers, bottles, and bags has raised the demand for this market. This segment helps to decrease wastage of materials, inventory overstock exposure, and storage requirements. The regulatory acquiescence and security are boosting the development of this sector.

The regulatory compliance packaging segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. This segment is growing significantly because of its crucial role in confirming market access, safety, and compliance. Assurance of prevention from contamination, leaks, and spills has raised the growth of the market. This segment is rising because of advancements in the technology of packaging.

The plastic segment is expected to account for a considerable share of the chemical repackaging market in 2025 due to its exceptional versatility, cost-efficacy, and strength. Plastic containers are highly durable and lightweight, which reduces the transportation cost and makes them a cost-efficient packaging option. Plastics fit in several industries and do not react easily with any chemicals, which raises their adoption. Both rigid and flexible forms of plastics are utilized in this market for manufacturing pouches, sachets, drums, vessels, and many other forms of packaging.

The paperboard & fiberboard segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. The rising search for eco-friendly materials in the chemical repackaging sector has raised the demand for this segment. The growing consciousness about ecological issues has led to a huge demand for biodegradable materials in the packaging sector.

")

The North America region held the largest share of the chemical repackaging market in 2025, due to the rising demand for biodegradable and recyclable products. This region is dominating because of diversified chemical segment, tech innovation, scale, regulatory rigor, and sustainability drive. It results in growing packaging standards in various sectors such as petrochemicals, pharmaceuticals, and agriculture. The increasing pressure towards developing environment-friendly packaging has influenced the growth of this market.

U.S. Market Trends

The U.S. market remains one of the largest globally, supported by a developed chemical manufacturing industry and strict laws controlling the transportation, labeling, and storage of chemicals. Repackaging services are becoming increasingly important to industries like pharmaceuticals, personal care, food processing, and specialty chemicals to meet customer-specific packaging requirements and enhance supply chain efficiency. Reusable and recyclable packaging options are becoming more popular due to the increased emphasis on sustainability.

The Asia-Pacific region is estimated to grow at the fastest rate in the chemical repackaging market during the forecast period. The rising ecological consciousness, rapid industrialization, and infrastructure expansion. Government in this region has strict regulations across ecological protection, chemical handling, and labelling, endorsing huge investment in compliant repackaging services. Countries such as India, Japan, China, Thailand, and South Korea are capitalizing on recycling competencies and environment-friendly packaging.

India Market Trends

India is witnessing steady growth in the market due to growing demand from the industrial manufacturing, pharmaceutical, agrochemical, and specialty chemical industries. Businesses are being encouraged to use professional repackaging services by the growth of local chemical manufacturing, rising exports, and the increasing demand for safe transportation of both hazardous and non-hazardous chemicals. Additionally, market expansion is being strengthened by government programs that promote the chemical industry and advancements in logistics infrastructure.

Europe is expected to grow at a considerable CAGR in the upcoming period, owing to its robust chemical manufacturing industry and stringent safety and environmental laws. Businesses in the area are increasingly contracting out repackaging tasks to specialized service providers to lower operating expenses and guarantee regulatory compliance. The market is expanding throughout European nations thanks to the increased focus on sustainable packaging materials and circular economy methods.

Germany Market Trends

Germany represents a key market within Europe because it is one of the major centers for producing chemicals worldwide. Repackaging services are in high demand due to the existence of large chemical producers, sophisticated logistical networks, and large export volumes. Furthermore, ongoing investment in chemical repackaging operations is driven by the need for specialized packaging solutions due to stringent quality control standards and the growing demand for specialty chemicals.

Latin America is considered to be a significantly growing area, as the region's levels of industry, agriculture, and chemical consumption all continue to climb. Flexible packaging and repackaging solutions are in high demand due to rising imports and exports of specialist goods, fertilizers, and industrial chemicals, to raise operational effectiveness and safety requirements, market players are also making investments in state-of-the-art handling and storage facilities.

Brazil Market Trends

Brazil dominates the Latin American market due to its vast logistics network, robust chemical industry, and sizable agriculture sector. Repackaging services are in high demand for consumer goods, industrial chemicals, and agrochemicals. Market expansion across the nation is being further supported by increased investments in storage and distribution infrastructure and an increase in chemical product exports.

The Middle East and Africa region is expected to grow at a notable CAGR in the foreseeable future, driven by increasing investments in petrochemicals, industrial manufacturing, and infrastructure development. The need for chemical handling and repackaging services is rising as nations in the region increase their chemical production capacities to diversify their economies. The use of cutting-edge packaging solutions is also being encouraged by increased commercial activity and more stringent safety regulations.

UAE Market Trends

The UAE is emerging as a major chemical logistics and distribution hub in the Middle East due to its excellent port infrastructure and advantageous geographic location. The demand for repackaging services that adhere to international shipping regulations is being driven by the expansion of commerce in industrial products, petrochemicals, and specialty chemicals. Furthermore, the nation's standing in the regional chemical repackaging market is being reinforced by investments in free zones, logistics parks, and industrial clusters.

By Packaging Type

By Chemical Type

By Packaging Material

By Function

By End-Use Industry

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarChemical Repackaging Market