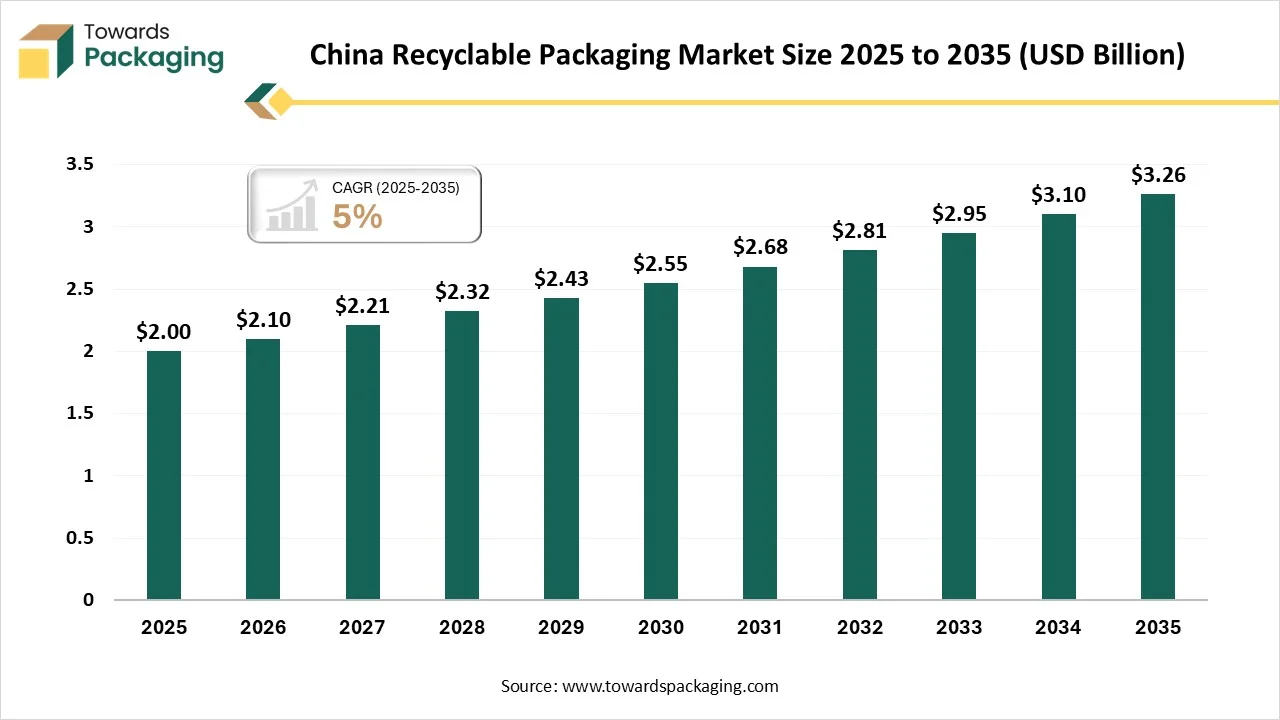

The China recyclable packaging market is projected to grow from USD 2.1 billion in 2026 to USD 3.26 billion by 2035, registering a CAGR of 5% during 2026–2035. The report provides detailed statistical insights including market size data, segment-wise analysis by material type, packaging format, and end-use industries, along with regional demand data across major provinces in China. It also includes competitive analysis of leading companies, manufacturers and suppliers, value chain assessment, and trade data covering imports and exports, offering a complete view of the recyclable packaging industry in China.

Recyclable packaging is material that can be conveniently collected, classified, or reused and made for recycling as secondary raw materials. Some of the materials include cardboard, paper, glass, aluminum, as well as plastics which are recyclable and are chosen as eco-friendly packaging options to single-use plastics. They assist brands in reducing the application of new links and lowering total carbon emissions.

A compelling technological development is EPS recycling, which is widely accepted as EPS densifiers are a type of machine that compresses EPS packaging into compact blocks, creating economically reliable recycling and transportation. On the other hand, artificial intelligence (AI) technology is currently utilized in recycling plants globally to develop sorting accuracy and productivity. By precisely recognizing and classifying materials like cardboard, EPS, and different plastics, AI-driven machinery ensures a cleaner recycling process, which points to developed recycling rates and lower pollutants.

Package Design and Prototyping: The main aim of designing for recycling is to make sure packaging can be smoothly processed in the recycling systems. By developing the material updation, the design for recycling develops both the quantity and quality of changed materials, which makes recycling smoother and economically more suitable.

Recycling and Waste Management: Recyclable packaging lessens the environmental impact of packaging waste. It overall assists in lowering the pollution and protects natural resources by storing waste far from oceans and landfills. By using recycled materials, whether they are paper, plastic, or glass, it releases lower carbon emissions instead of generating single-use plastics from the beginning.

Logistics and Distribution: As per the Association of Supply Chain Management (ACSM) Dictionary, the green logistics inside the supply chain are defined as supply chains that use surrounding effects on their running mode and take some action within the supply chain to align with eco-friendly security regulations and talk to suppliers and collaborators.

The paper & paperboard segment dominated the market in 2025, as they are a kind of sheet material that includes an interlinked network of cellulose fibres sourced from wood. Cellulose fibers have the potential of making physico-chemical links at such points of contact under the fibre network, as they result in a sheet. The power of the sheet relies on the starting and type of fibre used, the weight calculated per unit area, how they are manufactured, and the thickness too.

The bio-based segment is projected to witness the fastest CAGR during the forecast period. These materials come directly or indirectly in nature that come from cardboard, paper, and wood. Utilizing such materials for packaging is not compulsory and not a perfect idea. There are many other types of plastics that are created from bio-based elements, such as sugarcane or sugar beets and corn. Such plastics are also known as bioplastics. Biobased packaging factors have exceptionally different properties from regular packaging materials.

The primary packaging segment dominated the market in 2025 because it is a kind of packaging that is directly connected to the products. Its aim is to secure them and track their perfect features. The primary packaging of any product is the initial layer that surrounds it and the one that signifies its smallest space of sale. The working of primary packaging is to classify, protect, prevent, and communicate elements and expiry, which attracts commitment and attention.

The tertiary packaging segment is projected to witness the fastest CAGR during the forecast period. The main goal of tertiary packaging is to make unit loads that group different kinds of primary packaging and to make transport, storage, and handling convenient. Such packaging incorporates reinforcement to gather and protect the units of sale. Due to this, user products are also being marketed clubbed together, so they should be communicative and attention-grabbing.

The rigid packaging segment dominated the market in 2025, as it is convenient to recycle as compared to flexible packaging. One of the crucial reasons for such a case is that rigid materials usually consist of a mono-polymer mono-layer design, which is easier to recycle compared to the multi-layer polymer multi-layer design that is frequently used in flexibles. Rigid packaging materials, specifically recyclable glass and plastics, align with the developing importance of sustainable practices while serving reliability.

The flexible packaging segment is expected to witness the fastest CAGR during the forecast period. These packaging produced from PP, PET, EPP, PA, PLA, and PS are not presently sub-optimally recyclable and result in the officially called mixed field after being categorized, at every stage, as they can no longer be utilized to make new flexible packaging. In the current scenario, only pure PE film can be reused and recycled to create the latest packaging film. Recycled PE cannot be applied to food packaging.

The boxes and cartons segment dominated the market in 2025, as several collected cartons are being sent to paper mills, where the fibers are reused and recovered in products such as office paper, cardboard boxes, and tissues. The polyAL surfaces are being shifted into pellets, which has provided them a second life in products such as outdoor furniture and crates. By storing valuable materials in circulation, one brand can lower waste and assist in a sustainable circular economy.

The pouches & sachets segment is projected to experience the fastest CAGR during the forecast period. Recyclable pouches and sachets have been the main solution previously. They have become a crucial choice for food and beverage (F&B) organizations that seek sustainability goals while also developing brand engagement and cost effectiveness. Like rigid packaging or multi-layer plastic bags, recyclable pouch packaging utilizes fewer resources to generate and leave behind a lower carbon footprint. Mono-material pouches made from PE or PP are recyclable through unloading or curbside collection in many countries in China.

The food & beverages segment dominated the market in 2025 as fiber and paper-based solutions are finding strong development, which is being driven by their user requests and recyclability. Producers are making oil-resistant and water coatings that come from natural polymers like chitosan or cellulose, which lowers dependency on fluorochemicals. Molded fiber packaging is heavily used for ready-to-eat beverages and meals, which have gained advantages from material science developments that improve durability and heat resistance. Edible coatings and films are gaining attention as a path to lessening single-use plastics.

The pharmaceutical / healthcare segment is expected to experience the fastest CAGR during the forecast period. The application of PCR in healthcare packaging carries relevant eco-friendly benefits. Apart from the economic advantages it serves producers, it comes as a main player in lessening plastic waste and avoiding carbon emissions. Such trending advantages are in support of the healthcare sector, which intensifies sustainable practices. Producers are actively accepting PCR in the manufacturing of plastic bottles, enabling the use of packaging materials that have space for recycled plastic.

The China Recyclable Packaging Market is expected to grow notably as the use of recycled plastics in the packaging industry is being driven by the urge from international brands. Big brands use environmentally friendly recycled products as a path to complete their social responsibility and market the usage and recycling of waste plastics through various actions. In the Chinese sector, international brands have been testing little blocks of plastic for the last two years. In Southeast Asia, the Macau and Hong Kong region, they have started to reveal recycled plastic packaging products. Several international brands also have manufacturing sites in China and their respective export products that have begun to utilize recycled plastics.

By Material Type

By Packaging Type

By Packaging Format

By Product Type

By End-Use Industry

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarChina Recyclable Packaging Market