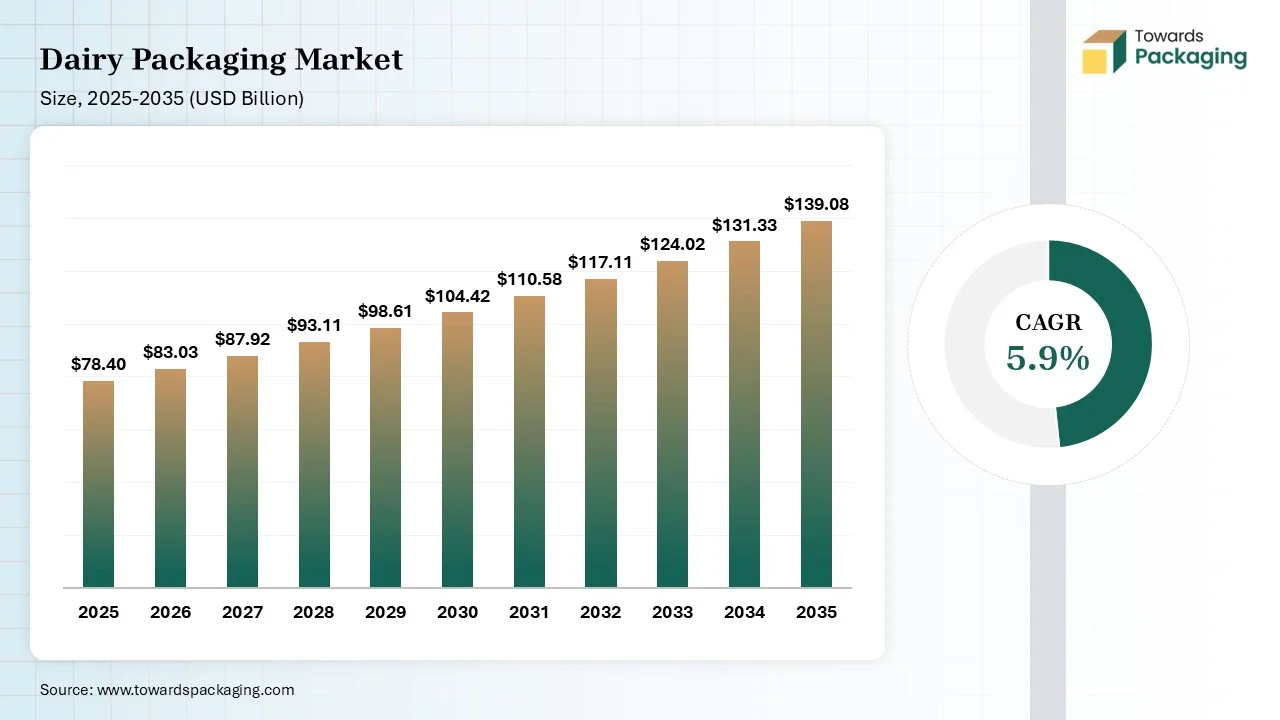

The dairy packaging market is projected to grow from USD 83.03 billion in 2026 to USD 139.08 billion by 2035, registering a CAGR of 5.9% during the forecast period. The report provides detailed insights into market size, along with comprehensive segment data based on material type, packaging format, and application. It further includes in-depth regional analysis across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The study also covers key company profiles, competitive landscape, value chain analysis, trade data, and detailed information on manufacturers and suppliers, offering a complete view of the industry.

Market Size (2025): USD 78.4 Billion

Revenue CAGR (2025–2035): 5.9%

Market Volume (2025): 42.6 million Tons

Volume CAGR (2025–2035): 4.8%

Pricing Data (2025):

The dairy packaging sector is experiencing a major update, and one of the most highlighted shifts is milk packaging. This packaging points to tailored materials, which are initially cardboard, plastics, and glass, crafted to protect, contain, and preserve dairy products like yogurt, milk, butter, and cheese from pollutants, oxidation, and light. It ensures security and delivers tamper-proof logistics. Some of the prevalent packaging formats include bottles, pouches, and aseptic cartons.

AI plays an impressive role in the market as safety standards and a keen eye on production and other operations have become an essential part of the dairy sector. While the intelligent systems and AI-sponsored computer vision serve quality check services and deliver commendable real-time monitoring to the dairy operative settings. Maybe not so modernized, but the market is evolving and the demand of consumers.

Automation is being used from the stage at which the milk arrives at the processing plant. Automated systems for testing and sampling enable fast and accurate analysis of the further milk, which ensures effective processing and sorting.

Control systems automatically count and log the bulk quantity of further milk. They smoothly collect showcased samples, and fastly track crucial quality elements such as protein levels, fat content, and bacteria counts. Such machines accurately track necessary factors such as pressure, temperature, and flow rates during pasteurization to ensure accurate and constant heat diagnosis that avoids toxic pathogens.

Plastic segment dominated the market with a 52% share in 2025 because polypropylene 5 is a daily applicable product. As number 5 shows, it does not leave any kind of wastage after degradation. Its chemical formula C3H6 suggests that it is a hydrocarbon, which has greater importance in milk product packaging due to its high compatibility for packaging purposes. The yearly manufacturing rate of PP-5 is 45 million tons, and 30% of these are used for dairy packaging. It puts a higher number of bases for any type of polyethylene, as it has less density and a barely porous composition.

The paper & paperboard segment held the 21% market share in 2025 and is also expected to develop at the fastest CAGR of 6.4% during the forecast period. Paper cartons are one of the most widely used selections. They are lightweight, convenient to store, and likely environmentally friendly in nature. Cratons generally have a thin inner lining in order to prevent leakage and maintain freshness. Hence, they can be less reliable than other selections, and once they are opened, they have a minute shelf life. For instance, Tetra Pak cartons have a latest solution that integrates several layers of paper, aluminum, and plastic.

The glass segment held the 9% market share in 2025 as it is one of the oldest types of packaging materials for dairy products. They are chemically inert, which means they will not communicate with acidic ingredients of fermented milk. Glass delivers perfect barriers against moisture and gases and is completely recyclable in nature. They also protect the actual flavor of the product, which is perfect compared to other materials. Several luxury artisanal fermented milks and yogurts are still being sold in glass jars for such reasons.

The metal segment held the 8% market share in 2025 because metal cans are a relevant and widely used form of food packaging around the globe. From fruit juices to canned vegetables and carbonated beverages to cooking oils, they protect food from pollutants, extend the shelf life, and firmly stand with strong forms of industrial processing. They are initially created from two materials, such as aluminium and tinplate, with a steel coating that has a thin layer of tin selected based on the products being packaged and the processing conditions.

The rigid packaging segment dominated the market with 46% share in 2025, as metal cans and glass bottles retain their form overall, even when they are empty. Semi-rigid materials come between these two extreme cases. They track enough structural reliability to handle, stack, and serve smoothly, while tracking mainly lighter than their strong equivalent. In the dairy sector, the crucial rigid designs include lined cartons, folding cartons, thermoformed containers, and aseptic cartons as each one is matched to dairy products and serving conditions.

The flexible packaging segment held the 34% market share in 2025 and is also expected to develop at the fastest CAGR of 6.8% during the forecast period. It drastically lowers the complete packaging weight. For the dairy industry, which is frequently shipped in cold weather or has advanced shipping volumes, even a little avoidance of material weight shifts results in reduced transportation costs. Flexible packaging assists with automatic dosing, form-fill-seal systems, vacuum sealing, and cold or hot filling, as necessary to lower contamination while developing productivity.

The semi-rigid packaging segment held the 20% market share in 2025 because it hits an ideal balance between flexibility and design. It generally tracks its shape but can fold and compress under heavy pressure. Prevalent materials include aluminum foil, thermoformed plastics, paperboard, and laminated films. Such packaging is well known for its reliability, lightweight, and online appeal. It delivers a more updated appearance than flexible packaging while serving accurate protection against air, moisture, and handling.

The milk segment dominated the market with 38% share in 2025 as milk bottle packaging provides the primary point of communication between a product and its users, which makes it an important factor in designing buying decisions. Apart from its functional aim, it plays a step-by-step role in brand positioning, which serves as a substantial reflection of the brand’s dedication and values to quality. Additionally, smooth packaging prevents milk from external elements like light exposure and contaminants, which ensures product safety and freshness.

The yogurt segment held the 19% market share in 2025 and is also expected to develop at the fastest CAGR of 6.9% during the forecast period. One of the crucial reasons that plastic yogurt cups are gaining popularity is their unbreakable durability and convenience. Like regular or glass paper cups, plastic yogurt containers are unbreakable, lightweight, and ideal for on-the-go consumption. Users are currently seeking packaging that can firmly stand the precision of every life. Plastic yogurt cups deliver that. They serve a convenient-to-carry solution, which makes them perfect for busy individuals who want a reliable and fast snack.

The cheese segment held the 14% market share in 2025 because polyethylene is one of the most widely used plastics in terms of food packaging worldwide. They are flexible, lightweight, and serve as a practical moisture barrier. As per the USDA, polyethylene is one of the three main plastic types utilized for storage bags and food wraps. For mozzarella, PE films are frequently used in a vacuum-sealed structure, in which the films are tightly formulated against the cheese layer after air surface removal. Such a direct connection lowers the capacity where microbes can develop.

Butter & Cream segment held the 10% market share in 2025 as they are widely used dairy products in the globe, and in what way they are packaged plays an important role in protecting their texture, flavor, and overall quality. As the butter has a fat content of approximately 80-85%, they are highly susceptible to light, oxidation, and odor absorption. The correct packaging design not only protects butter from such risks but also checks how easily it reaches users and food service discovery.

The ice cream segment held the 12% market share in 2025 because it is a combination of water, fat, air, and sugar. Such sensitive designs are highly susceptible to eco-friendly factors. Freezer burn comes as moisture runs away from the refrigerator and refreezes, producing ice crystals on the surface, resulting in a grainy, dry, and dull taste. Temperature changes during transport and storage develop such procedures. Packaging provides the beginning shield against such contamination. It should block moisture loss, preclude contamination from external smells, and insulate the product against temperature changes.

Conventional packaging dominated the market with 41% share in 2025 because the dairy industry excessively depends on conventional packaging materials to ensure product safety, affordability, and shelf life. Low-density polyethylene (LDPE) plastic pouches lead to urban milk distribution that is responsible for nearly 75% of the industry. High-density polyethylene (HDPE) bottles are widely utilized for probiotic beverages, milk that delivers strength and user convenience. At the current time, Tetra Pak cartons deliver a stretched shelf life for ultra-high temperature (UHT) milk and fruit-dependent drinks.

The aseptic packaging segment held the 27% market share in 2025 and is also expected to develop at the fastest CAGR of 6.7% during the forecast period. Aseptic packaging materials are being crafted to serve an advanced level of prevention against fungi, bacteria, and other microorganisms. They generally count several layers, as each has a particular function. The inner layers are generally in direct contact with the product and are made of food-grade material that is resistant to oxygen and moisture. This assists in protecting the product from being polluted due to the growth and oxidation of mold.

The MAP segment held the 12% market share in 2025 as it is a method of leveraging a fragile packaging atmosphere to develop product longevity. It lowers the implemented oxygen volume in the packaging to protect against aerobic contamination and microbial formation. Such a procedure also protects water vapor, making substitutes for oxygen with remaining gases in the packaging to serve further product advantages, such as tracking quality and expanding the shelf life. Organizations use MAP to develop nutritional appearance, product image, and texture.

Retail segment dominated the market with 58% market share in 2025, as dairy products need tailored packaging because of their fragile nature to oxygen, light, and temperature. Milk packaging films should solve several protections demands simultaneously. Oxygen barriers protect against oxidative degradation, which is responsible for off-flavors and lowers the nutritional value. Light barriers prevent vitamins from being degraded under UV exposure. Moisture barriers protect against condensation and track product consistently. Current milk packaging consists of several layer films that integrate polymers for overall protection. Such films allow for expanded shelf life, developed distribution of flexibility, and perfect product availability.

The foodservice segment held the 25% market share in 2025 and is also expected to develop at the fastest CAGR of 6.3% during the forecast period. They need tailored dairy packaging solutions initially to track the highly sensitive nature of dairy products, which ensures food safety and develops operational efficiency. Due to dairy products, which are extremely fragile to oxygen, light, and temperature changes, high-level packaging is necessary to extend the shelf life, track hygiene, and lower waste in a quick-paced environment.

The industrial/bulk segment held the 17% market share in 2025 because the shelf life of dairy products relies on intrinsic and extrinsic factors. The intrinsic elements count nutrient content, pH, the presence of antimicrobial elements, and the oxidation capability of the milk. Condensation, pasteurization, and drying are prevalent procedures to create dairy products perfect for packaging and storing. Air ingredients and storage conditions are extrinsic factors of dairy packaging. Laminated paperboard, plastic, glass, and metal serve the need for isolation to dairy products like milk powder, milk, and cheese.

Asia Pacific dominated the market with 36% share 2025 and is expected to grow at the fastest CAGR of 7.1% during the forecast period. The sector's top brands in this region are designing the competitive scenario with concentrated methods and perfectly defined importance. Their centers are the center point for developing product inventions, developing operational efficiency, and growing high-level technologies to develop user engagement and performance. Organizations are giving importance to sustainability programs, data-driven insights, and strong compliance frameworks to address developing market urges and regulatory requirements.

India Dairy Packaging Market Trends:

The dairy processing industry in India is witnessing favorable disposable incomes, as they update usage patterns, and growing supplements. Main government schemes and regulations play an important role in developing milk manufacturing, processing, and productivity design in the dairy industry. Such factors have altogether invested in the strong development and growth of India. It carries the classification of being the globe’s biggest producer of milk, which changes the dairy processing ecosystem.

Which Factors Drive the Dairy Packaging Market in North America?

North America is expected to grow at a notable CAGR in the foreseeable future, driven by the eco-conscious materials involvement that introduces cardboard plastic combinations and mono-material structures. The vacuum-sealed packaging alleviates waste and confirms safety in the food and beverage sector. The modernized materials and smart packaging trend is the talk of the town, promoting the development of the MAP that ensures freshness to the dairy products. While the transition to resealable packaging, easy-to-use tubs, and pouches is bolstering the e-commerce businesses.

Europe Dairy Packaging Market Trends

Europe held the 24% market share in 2025 because it was initially pushed by growing user demand for sustainability, convenience, and product safety. Growing health consciousness has led users to choose fresh, hygienically packed dairy products, hence it has developed demand for high-level packaging solutions. Additionally, inventions like recyclable and biodegradable packaging materials match with developing eco-friendly awareness and regulatory compulsions on reducing plastic waste, which poses environmentally friendly packaging as the main market driver.

How is Latin America Growing in the Dairy Packaging Market?

Latin America is expected to grow at a considerable CAGR in the upcoming period. The flexible packaging and extended shelf life decorate the storage space with more power and sincerity. Comprehensive refrigerated warehousing cooperates best with dairy products due to the smart and responsible packaging that indicates additional attentiveness towards the temperature. The modernized barrier technologies are specially used to safeguard the liquid milk and yoghurt products. The storage potential is possible through the strong and loyal packaging that promotes the storage capacity.

Italy Dairy Packaging Market Trends:

The urge for dairy packaging in Italy is initially driven by the move towards convenience-focused designs, sustainable materials, and the development of the plant-based choices market. While regular dairy consumption has experienced some of the historically lower phases, tailored and high-value segments such as fresh dairy and cheese export products have continued to meet packaging demands. There is a rising demand for single-serve designs for flavored milk, yogurt, and snacking cheese to assist on-the-go consumption. Italy is top in cheese manufacturing along with France and Germany, which drives the main demand for personalized packaging for artisanal and processed segments.

By Material:

By Packaging Type:

By Product Type:

By Packaging Format:

By End-Use:

By Regions:

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarDairy Packaging Market