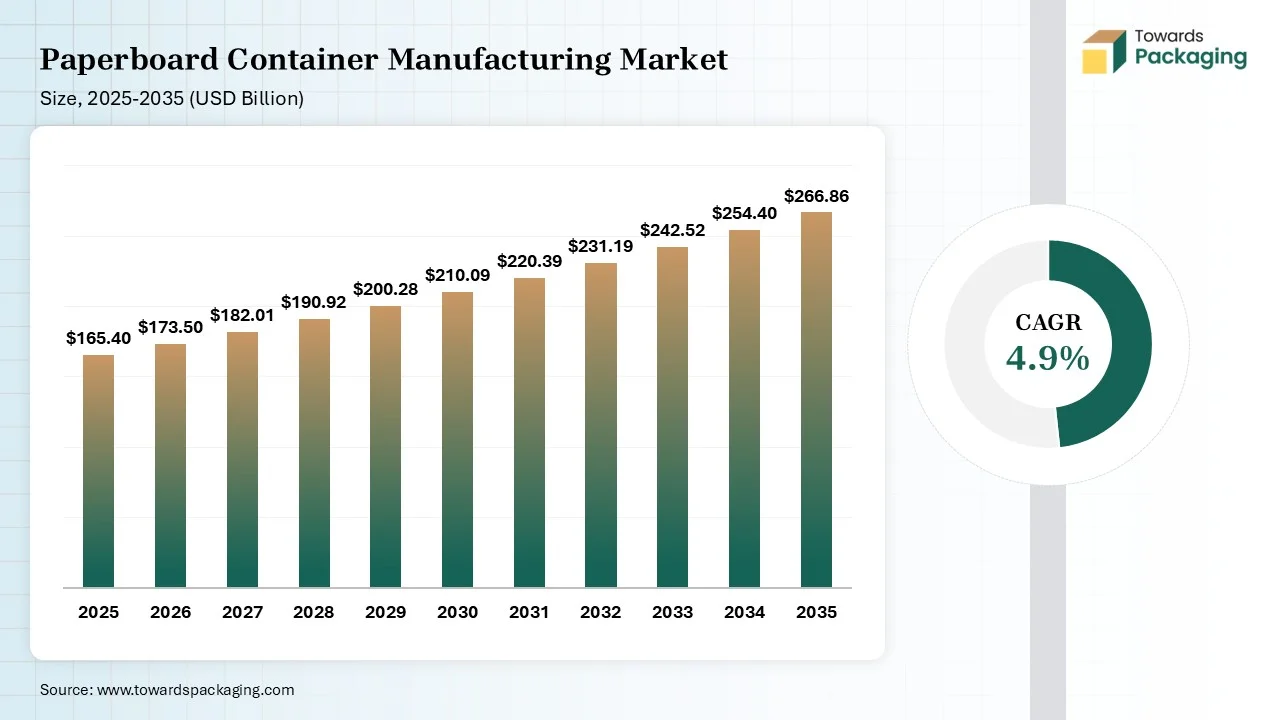

The paperboard container manufacturing market is projected to grow from USD 173.5 billion in 2026 to USD 266.86 billion by 2035, registering a CAGR of 4.9% during the forecast period. The report provides a comprehensive analysis of market size along with detailed segment data by product type, material, and end-use industries. It further includes in-depth regional insights across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Additionally, the study covers key company profiles, competitive landscape analysis, value chain mapping, trade data, and detailed information on manufacturers and suppliers shaping the market.

Market Size (2025): USD 165.4 Billion

CAGR (2025–2035): 4.9%

Market Volume (2025): 245.6 Million Tons

Volume CAGR (2025–2035): 4.2%

Pricing Data (2025):

Paperboard container manufacturing includes converting obtained paperboard which is a thick, robust, and lightweight paper-based resource, into several folding or rigid containers. This market utilises specified machinery to cut, crease, fold, and glue resources into goods such as shipping containers, cereal boxes, and food packaging, emphasising on packaging branding and design.

Technological transformation in the paperboard container manufacturing market plays a significant role with the upsurge in the digital printing and customisation. The huge demand for customization with the growth in e-commerce sector has fuelled the incorporation of advanced technology. These advanced manufacturing technologies support in recognising the micro-imperfections which enhance the reliability of the industry. It supports in structural innovation and decreases transportation charges with strong paperboard.

The major raw materials utilised in this market are starches for adhesives, softwoods of pine and eucalyptus, clay coatings, polypropylene, and polyethylene. These are the materials support in the production of high-quality packaging.

The component manufacturing in this market comprises recycled fibre, kraft paper, stitching wire, and polymers. It supports in the production of durable packaging that can help in long-term storage.

This segment ensures the rapid expansion of supply chain efficiency and production to meet the demand of the consumers. Advanced technology support in real-time tracking of the products.

The folding cartons segment dominated the market with 38% share in 2025. Due to rapid shift from traditional plastics to sustainable packaging solution. These are highly versatile which is widely accepted to meet the huge customisation process. It is extensively utilised in the pharmaceutical, food and beverages sector.

The corrugated containers segment held 32% market share in 2025 and expected to experience the fastest growth in the market with 5.2% CAGR during the forecast period. Due to its enhanced recyclability potential, high strength, and low charges. This segment is majorly driven due to rapid shift towards sustainable packaging, e-commerce sector, and food delivery facilities. The rising sustainability packaging services with lightweight has fuelled the demand for this segment.

The liquid packaging cartons segment held the 18% market share in 2025. Due to its protective properties, lightweight nature, and sustainability. The increasing consumption of plant-based drinks, juices, and dairy products has fuelled the demand for this segment. The rising concern towards enhanced shelf life of the products has fuelled the demand for this sector.

The paperboard trays & clamshells segment held the 12% market share in 2025. Due to rising adoption of biodegradable and sustainable packaging for a huge variety of products. It offers strong protection to the packaged products and high recyclability. These are useful in customisation to a huge extend which has fuelled the demand for this sector.

The Folding Boxboard (FBB) segment dominated the market with 34% share in 2025, and it is expected to experience the fastest growth in the market with 5.1% CAGR during the forecast period. Due to its lightweight nature, high stiffness, and excellent printability. This is considered as suitable packaging for cosmetics, pharma, and food industry. The huge demand for enhanced printing capacity and durability has fuelled the demand for this sector.

The Solid Bleached Sulfate (SBS) segment held the 29% market share in 2025. Due to its aesthetic appearances, enhanced printability capacity, and enhanced protection. The rapid shift towards high-quality, sustainable, and hygienic packaging in pharmaceutical, food, and cosmetics industry. It supports in premium packaging of the products.

The Coated Unbleached Kraft (CUK) segment held the 21% market share in 2025. Due to its enhanced durability and strength which ensure the safety of the products. The rising acceptance of strong and durable packaging has fuelled the demand for this sector. These are the eco-friendly packaging options available in the packaging sector.

The White Lined Chipboard (WLC) segment held the 16% market share in 2025. Due to its enhanced versatility and cost-effectiveness. These can be used for the packaging of pharmaceutical products and frozen food items. These are highly recyclable and sustainable packaging sector. It offers high-quality, competitive charges, and great printability.

The food & beverage segment dominated the market with 46% share in 2025. Due to its cost-effectiveness, enhanced safety, and sustainable packaging. These are lightweight as well as rigid packaging that offer excellent packaging for a wide range of products. There is a huge demand for hygienic, sustainable, and protective packaging has pushed the adoption of this industry.

The personal care & cosmetics segment held 12% market share in 2025 and expected to experience the fastest growth in the market with 5.3% CAGR during the forecast period. Due to increasing demand for eco-friendly, sustainable, and lightweight packaging. It has huge requirement for premium packaging that has raised the adoption of this sector. The rising ecological concern among major manufacturer has raised the adoption of this segment.

The industrial packaging segment held the 18% market share in 2025. Due to the increasing demand for huge transportation of fragile products. There is a huge demand for versatile packaging which has raised the demand for this industry. These are cost-effective, durable, and standardized packaging which has fuelled the innovation in this industry.

The pharmaceuticals segment held the 14% market share in 2025. Due to increasing demand for recyclable, biodegradable, and sustainable packaging. These are tamper-evident and safe packaging that has attracted to a huge consumer base in this sector. It preserves the integrity of highly sensitive drugs and helps in long-term storage.

The 200–350 GSM segment dominated the market with 48% share in 2025. Due to its rigidity, printing surface, and durability of the packaging. It plays an important role in protecting products and branding. The increasing focus towards highly recyclable and superior printing has fuelled the adoption of this sector. These are widely used in the e-commerce, food and beverages industry.

The above 350 GSM segment held 30% market share in 2025 and expected to experience the fastest growth in the market with 5.2% CAGR during the forecast period. Due to its premium packaging, enhanced strength, and rigidity. These are extensively used in the packaging of premium products in the food, pharmaceutical, and electronics sector. It enhances the unboxing experience of the consumers which has fuelled the demand for this sector.

The below 200 GSM segment held the 22% market share in 2025. Due to its suitability for high-volume production, lightweight nature, and cost-effectiveness. It offers enhanced flexibility and personalised designs of the packaging. It supports in maintain the integrity of packaged bakery products, retail bags, and cereal boxes. These are considered as standard form of packaging which has raised the demand for this sector.

Asia Pacific dominated the paperboard container manufacturing market with 41% share in 2025, and it expects the fastest growth in the market with 5.8% CAGR during the forecast period. Due to massive growth in the e-commerce sector, and rapid urbanization. The rising sustainability trend has fuelled the demand for this industry. There is requirement for high-volume packaging production that has influenced the demand for innovation in the manufacturing process. There is a huge shift from plastic packaging towards advanced packaging of the products.

China Paperboard Container Manufacturing Market Trends

The rapid growth in the e-commerce sector has raised the demand for the market in China. The presence of huge manufacturing capacity has fuelled the demand for this industry. The rapid innovation in this sector has attracted huge consumer based towards this industry. Huge export demand as well as domestic use has fuelled the production of these containers.

North America held the 24% market share in 2025. The huge demand for e-commerce friendly, sustainable, and recyclable packaging has raised the adoption of the paperboard container manufacturing market. The increasing demand for durable and strong paperboard has pushed this industry to grow significantly. It is majorly used for consumer goods packaging and in food & beverages industry.

The U.S. Paperboard Container Manufacturing Market Trends

The rapid growth towards sustainable packaging sector have fuelled the demand for the market in the U.S. The presence of major market players has fuelled the research and development in this sector. The rising inclination towards compostable and biodegradable packaging has fuelled the demand for this industry. The rapid growth in online shopping among consumers has fuelled the adoption of this industry.

By Product Type

By Material Grade

By End-Use Industry

By Thickness / GSM

By Printing Technology

By Regions

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarPaperboard Container Manufacturing Market