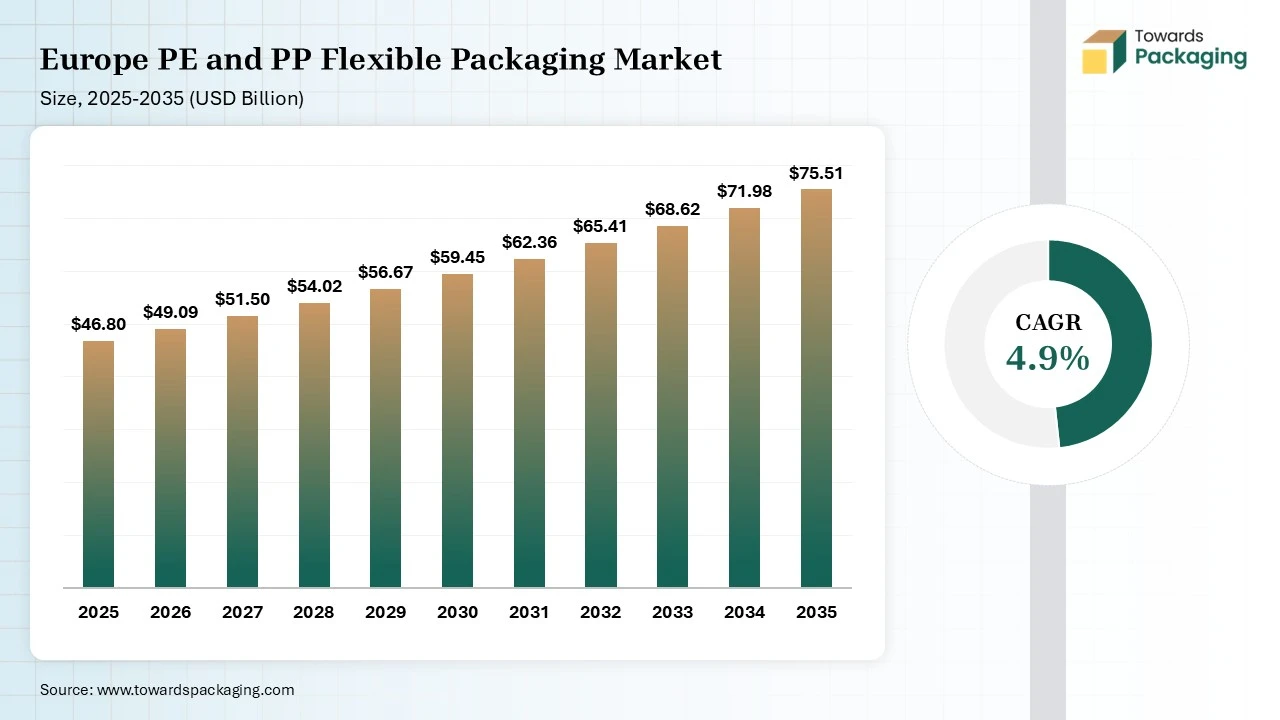

The Europe PE and PP flexible packaging market is projected to grow from USD 49.09 billion in 2026 to USD 75.51 billion by 2035, registering a CAGR of 4.9% during the forecast period. The report provides comprehensive coverage of market size, detailed segment data by material and application, and region-wise performance across Europe. It also includes in-depth competitive analysis, key company profiling, value chain insights, and trade data. Additionally, the study highlights manufacturers and suppliers data while examining how cost-efficiency, lightweight properties, and sustainability advantages over rigid packaging are driving market demand.

Market Size (2025): USD 46.8 Billion

CAGR (2025–2035): 4.9%

Market Volume (2025): 12.6 Million Tons

Volume CAGR (2025-2035): 4.3%

Pricing Data (2025):

Flexible packaging are constructed around invention. It integrates the science of materials that are crafted with a consumer-centric design. Packaging manufacturers mix foil layers, polymer films, coatings, and adhesives to generate packaging designs that deliver barrier protection, strength, and product power. Several of these crafted structures include flexible packaging materials such as polypropylene (PP), polyethylene (PE) ,aluminium foil, and polyester (PE), which altogether make multilayer films. Such multilayer films enable sensitive products like pharmaceuticals, snacks and medical machines to stay fresh and secure while storage, transport, and consumption.

Biotechnology will also have a developing role in packaging materials and material science. Furthermore, current plant-based plastics and scientists are seeking paths in which microbial engineering can make biodegradable polymers or agricultural waste that can be redeveloped into current types of packaging. The innovations can deliver sustainable packaging choices as choices to regular fossil-dependent plastics. AI can be utilized in transforming packaging design to lower material consumption, as the simulation of this behavior is under various conditions, and smoothing the manufacturing lines to create less wastage. Additionally, AI -filled classifying machines in the recycling sector are creating differentiation of more precise and smooth working, which points to more flexible packaging that can be recycled and penetrate again of the value chain, which lessens contamination.

The LDPE segment dominated the market with 28% share in 2025 as the current aim of this material in flexible packaging is central to any significant areas. Primarily, there is encouragement for developed sustainability, whose aim is to make completely recyclable LDPE packaging solutions and lower the carbon footsteps of the manufacturing procedure. Secondly, producers are standing strong to develop the regular elements of LDPE films, which count perfect seal reliability, developed puncture resistance, and high-level printability for high-quality graphics.

The LLDPE segment held 22% market share in 2025 because polyethylene linear low is a kind of grade in polyethylene that is produced with copolymerization of butene and ethylene. This manufacturing procedure develops puncture resistance, toughness, and flexibility as compared to regular low-density polyethylene (LDPE). It has classified balance of cost-effectiveness and mechanical elements which creates accurate material selection for uses by giving user packaging to an urging agricultural application.

The HDPE segment held 15% market share in 2025 because it is one of the most greatly used recycled plastics. Several HDPE flexible packaging designs are totally eligible for storage drop-off recycling initiatives, that enable the material which needs to be reprocessed, collected and reused too. Such recyclability assists brands to lower dependency on virgin materials while still utilizing packaging which carries in-demand conditions.

Films & Wraps segment dominated the market with 30% share in 2025 as they protect products from moisture, oxygen, contaminants and UV light that protects freshness and make sure safety. With an barrier-developed elements, food products are perfectly protected, that assist in lowering waste. As per the worldwide studies, developed packaging can capably lower food waste by up to 30%. Such BOPP films usually utilize lesser materials and outcomes in lower releases while transport and manufacturing.

Pouches segment held 28% market share in 2025 because frozen food pouches are crafted to serve high outcomes down to -25 degree Celsius, that is ideal for both industrial and home freezing. They are created from PP and PE with an EVOH barrier; flexible pouches have protected ingredients from moisture, oxygen, heat, and UV rays. This results in long time shelf life and prime protection of freshness, flavor and food quality.

The bags & sacks segment held 24% market share in 2025 because cost savings not only advantage flexible packaging with respect to the retail sector. Flexible designs enable half control, stand-up showcase, re-packing designs, and market user experience. Retailers also get delighted by the benefit of high-level shelf quantity, that lowers breakage and pushes visual merchandising. Brands have received further space for regulatory information, printable material for storytelling, as well as marketing messages.

Mono-layer films segment dominated the market with a 42% share in 2025 as this film has used a single polymer variety, or a polymer from the exact family, that comes across each layer of structure. In an regular multi-layer laminae, we can witness PET as an outer layer for print quality and strong nature as an EVOH barrier layer, adhesive layer, and for another adhesive too. They are also available for PE sealant surfaces. This design has at least three various polymer families, that make them non-recyclable with a current procedure. Its design substitutes all such layers with various grades of polyethylene. The outer layer has used medium-density or high-density PE for strong nature.

Multi-layer films segment held 38% market share in 2025 because multilayer film are flexible material created by linking many layers of different types of plastics, like as BOPP ( biaxially oriented polypropylene), PET ( polyethylene terephthalate) or PA ( polyamide ).Every layer of such film completes and particular technical working, that funds to developing the elements of an financial packaging ,like as power, prevention against eco-friendly factors and barrier against pollutants.

Semi-rigid structures segment held 10% market share in 2025 are packaging designs that mix both flexible and rigid packaging designs. One instance of a semi-rigid packaging design are present in bag-in-box, that highlights an outer corrugated (rigid) box which protects the flexible bag which keeps the product inside it. An aluminium is another material which is frequently used as semi-rigid packaging.

Food & Beverage segment dominated the market with 46% share in 2025. As user urge develops sustainability, convenience and invention, food and beverage producers are excessively shifting to an flexible packaging solutions. Flexible packaging is being crafted to align with current demands by developing the product shelf life, lowering the waste and serving environment-friendly choices, as product should be classified in this competitive industry. With a developing popularity of e-commerce and the demand for a lower eco-friendly effect, flexible packaging is more crucial than before.

The industrial packaging segment held the 17% market share in 2025. In this sector, packaging is used for wrapping, as it is stacking, protecting, repeating, and storing the procedure on repeat mode. But regular options like corrugated boards, wood, or foundational plastics have restrictions. Flexible packaging here points to crafted boards that serve power without any protection or bulk, which are added to waste. Flexible packaging is a sustainable choice over rigid and unprotected containers. A truckload of flexible packaging materials is the same as 35 truckloads of rigid materials.

Healthcare & Pharmaceuticals segment held 14% market share in 2025 as multi-layer materials with barrier elements secure against UV light, oxygen, contamination and moisture. This protects product reliability and ensures the stability of active ingredients over a period of time. Sachets and stick packs are perfect for granules, oral powders and liquid supplements. Such designs allow for accurate dosing, higher ease for the patients, that are matched with move towards personalization in healthcare.

The Personal Care & Cosmetics segment held 13% market share in 2025 because cosmetic packaging bags are a flexible container which manages, secures, showcases and transports the cosmetic products. Packaging bags have a long time of survival for their basic aim in the current beauty sector, that delivers main carriers of brand identity. Several brands utilize small self-incorporated bags and flat bags, etc. which are trial or marketing packaging for items like lotions, serums and shampoos, etc.

Blown film extrusion segment dominated the market with 36% share in 2025 as the procedure of blown film extrusion are milestone procedure for manufacturing a huge variety of flexible packaging materials. Their extrusions are reliable production procedures which are used to make plastic films of changing properties and thickness. It includes the constant extrusion of liquid plastic with the assistance of a circular die that makes tube-like designs which are known as bubbles. As the bubble stretches, air is discorded to include the tube into a wanted diameter, as cooling systems' goal are changing the material.

Cast film extrusion segment held 24% market share in 2025 as it includes encouraging molten plastic with the help of Coles roller, where it quickly cools down and gets harden into a thin sheet. Like blown films, cast films do not count air inflation or bubble making. Instead, Thai film is crucially developed along the tool direction. In terms of manufacturing, cast films are generated by melting the plastic resin and revealing it through a flat die in a chilled roller.

Printing & lamination segment held the 16% market share in 2025. The prevalently used laminates in the flexible packaging industry include two significant webs. One web is a co-extrusion film, which are mostly dependent on polyethylene, with different layers, and in between are a tie-layer and a barrier layer, which are against gases and humidity, such as oxygen. The second web is cases which are extended as BOPET or BOPP film that delivers final film due to its mechanical power, strength, and stiffness.

Injection molding segment held 14% market share in 2025 as the cycle period for this processing technology is relatively less compared to other production procedures. Plastic spaces for automotive injection molding and medical injection molding, as well as across remaining sectors, can be manufactured in couple of seconds to minute, depending on the complications of design. This enables fast transformation time, which makes injection molding perfect for sectors that need quick production to align with industry urges.

Germany has dominated the market, has subjected to use high level data analytics, actual-time market tracking and AI-driven predictive analysis. This further methodology ensures an overall understanding of user choices, technological inventions, and sustainable packaging trends. By developing machine learning and big data, brands can classify growing designs and user behaviors that push marketing procedures and product development.

Spain expects the fastest growth in the market during the forecast period. It is one of the top European countries in terms of frozen vegetable manufacturing and is classified as one of the European Union's initial agricultural centers. Its agricultural center stretches to various servings, which includes vegetables, cereals, grapes, and almonds. Furthermore, Spain has experienced fast industrialization and urbanization, as its users are excessively developing towards the easiness of packaged food like frozen foods. This move has developed by growing buying power and a rising desire for developing luxury food products.

By Material Type:

By Product Type:

By Packaging Type:

By End-Use Industry:

By Processing Technology

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarEurope PE and PP Flexible Packaging Market