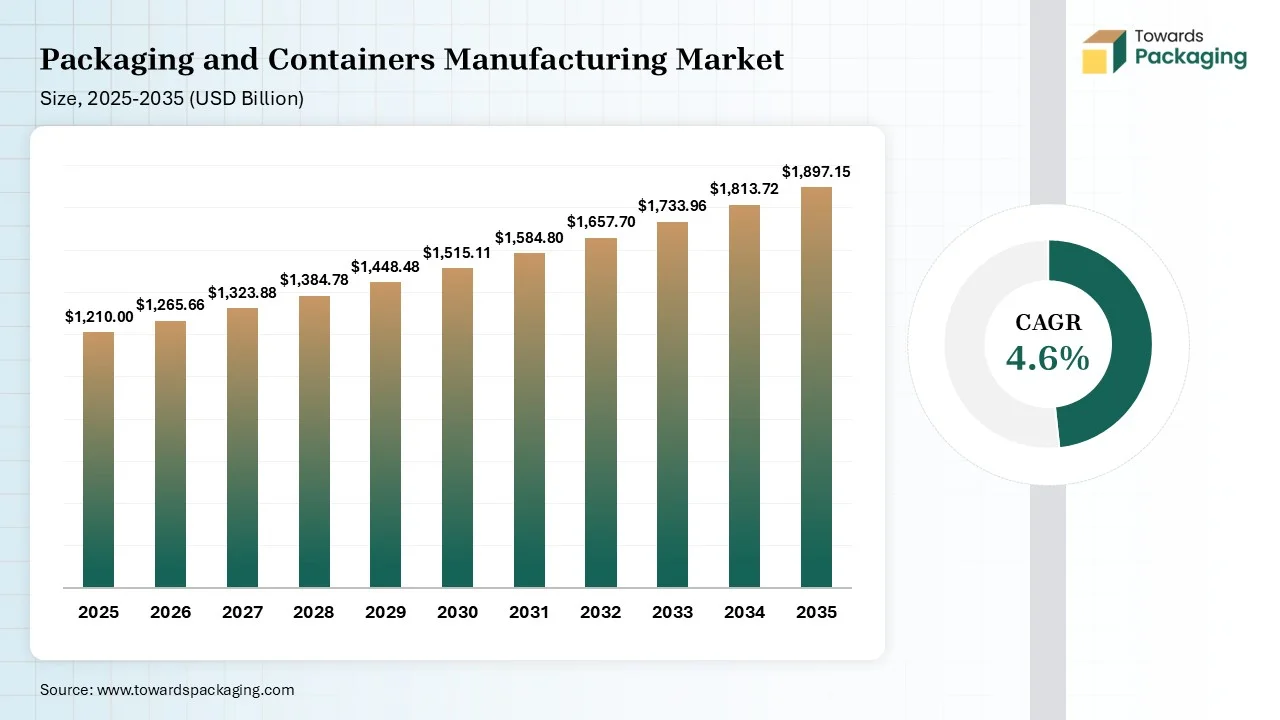

The packaging and containers manufacturing market is projected to grow from USD 1265.66 billion in 2026 to USD 1897.15 billion by 2035, expanding at a CAGR of 4.6% during the forecast period. The packaging and containers manufacturing market report provides detailed insights into market size, growth trends, segment-wise analysis, regional performance, company profiling, competitive landscape, value chain analysis, trade statistics, and manufacturers and suppliers data. The study also highlights rising demand driven by e-commerce expansion, changing consumer lifestyles, sustainable packaging adoption, and technological innovations across global markets.

Market Size (2025): USD 1,210 Billion

Market CAGR (2025–2035): 4.6%

Market Volume (2025): 1,420 Million Tons

Volume CAGR (2025–2035): 3.9%

Pricing Data (2025):

Packaging plays a necessary role in marketing and branding. Perfectly designed packaging can grab attention, communicate brand logos and values, and classify products from competitors. Attention-grabbing logos and labels can help brand classification and develop the complete user experience. Manufacturing packaging serves as a stage to showcase important product information, such as usage instructions, ingredients, and safety warnings. This assists in business matching regulatory requirements, constructs trust in the brand, and ensures user safety.

One of the main updates that shapes the future of packaging technology is the importance of sustainability. With rising eco-friendly issues, users are urging environmentally friendly packaging solutions that lower waste and lessen the carbon footprint. Brands are giving feedback by accepting practices such as lightening and lowering the material application without any adjustment to packaging reliability, and in-depth evaluation of choices like compostable, biodegradable, and recyclable materials. Packaging developers are choosing materials that come from renewable sources like mushroom-based packaging, edible packaging, and plant-based plastics.

Sustainable packaging is constructed on circularity that stores materials in applications as large as possible to lower virgin inputs that reduce waste from landfills and lessen the environmental effects. Like regular opinions that frequently value convenience, cost, and aesthetic over eco-friendly care, environmentally sustainable packaging concentrates on developing designs for recyclability.

Standardized packaging makes the procedure simple and lowers the materials costs. At the same time, singular packaging solutions can be compulsory to secure fragile elements or tailor-made products. Processes can also be developed in the warehouse. Digital aids, automated packing stations, and precise labeling systems make sure there are fewer errors and higher speeds.

The packaging effect also relies on whether facilities can actually reduce it. Recycling facility regulations display that inks, labels, designs, and closures have directly affected yield and classification, which checks whether a product becomes usable for raw materials or a residual waste.

Plastics Segment Dominated the Market with 42% Market Share in 2025

The plastics segment dominated the packaging and containers manufacturing market with 42% share in 2025, as recyclable plastic comes under a plastic material type space that can necessarily be transformed and recycled into the latest products. Several plastic material types are recyclable plastics, which can be most greatly recycled plastics that include PET (polyethylene terephthalate) and HDPE (high-density polyethylene). Recyclable plastics are extremely useful as they are elastic material types that play a crucial role in the circular economy, with the assistance of reprocessing to create various products.

The paper & paperboard segment held the 34% market share in 2025 because solid bleached sulfate is prevalently pointed to as SBS board, that are produced by using 1005 virgin bleached wood pulp, that delivers a pure white color and a different smooth layer. This board is overall bleached while manufacturing to ensure brightness, consistency and high print readability. Some of the prevalent uses of SBS include cosmetic boxes, skincare boxes, watch boxes, and perfume boxes. Solid leached sulfate can be leveraged for every kind of e-commerce and retail product.

The metal segment held the 9% market share in 2025 because aluminum containers are utilized for carbonated drinks to manage the pressure of CO2 in terms of soda drinks and make sure of an perfect taste. They are secure packaging choices for food and beverages as they do not react with or release chemicals into the contents. Aluminium containers are produced from 5052, 3004, and 3104 aluminium plates, which are also utilized for packaging different products, that contain cosmetic packaging, drugs, industrial products, and personal care products, etc.

The rigid packaging segment dominated the packaging and containers manufacturing market with 49% share in 2025, as prevalent products that specifically demand rigid packaging solutions in the pharmaceutical industry are frequently available in capsule, powder, and liquid formats. Rigid packaging is generally used in this industry, which is chosen for durability and quality, as well as aesthetics and function. Since several pharmaceutical products are dependent on safety and quality, security packs and child-resistant caps are often linked with rigid packaging.

The flexible packaging segment held the 38% market share in 2025 because it assists in good-quality printing, tailored shapes, and different outcomes such as gloss, matte, or a soft touch. It delivers brands more freedom to communicate their actual identity and attract users. As sustainability has become more crucial, flexible packaging offers more options like PCR-dependent films, mono-material designs, and compostable solutions that match eco-friendly goals.

The semi-rigid packaging segment held the 13% market share in 2025 because these packaging are used in ready-to-eat meals, which are also known as made meals or RTE meals, that are precisely why they must sound like food products that are completely or partially cooked and are ready to consume or require less reheating. Significantly, mad for military options, such meals are being packed in semi-rigid packaging like clamshells and tubes to serve hot meals.

The food & beverages segment dominated the packaging and containers manufacturing market with 52% share in 2025, as the food manufacturing procedure is subject to the link of operations that transform raw materials into complete food products. The main challenge of this procedure is sourcing high-quality raw materials that use different processing techniques and ensure that the final product aligns with quality and safety standards. The significant components can be smashed down into main factors like raw material procurement, quality control measures, and processing operations.

The healthcare and pharmaceuticals segment held the 14% market share in 2025 because the chemical and physical elements of packaging materials can degrade over time. This shapes the packaging’s potential to manage a secure and constant barrier. Furthermore, the compatibility of the sterilization procedure is another factor. The selected packaging should withstand the sterilization procedure. While handling and transporting, the packaging should be reliable enough to withstand effects, compression, and vibrations.

The personal care & cosmetics segment held the 11% market share in 2025 because, as more companies are loyal to cruelty-free rules and sustainability, tailored cosmetics packaging frequently includes recyclable materials or less-carbon ones. Natural fibers that come from sources such as rice husks, sugarcane bagasse, and bamboo are gaining popularity as sustainable choices. Such plant fiber-based materials are biodegradable in nature; it mitigates dependency on plastics and significant amounts of paperboard, which mostly have unique natural textures.

The primary packaging segment dominated the packaging and containers manufacturing market with 61% share in 2025, as they showcase the basic layer of product presentation and protection that delivers as the main and most complicated packaging link between a product and its surroundings. Apart from security, primary packaging delivers the main marketing and communication work. It develops the initial visual touchpoints for users, directing complicated information like ingredients, product details, expiration dates, nutritional facts, and brand identity.

The secondary packaging segment held the 24% market share in 2025 because brands that give their fresh food products to many retailers can concentrate on the safety advantages of secondary packaging. It has two crucial aims. The primary one is to help the delivery and shifting of fresh food products by providing the packaging that allows shipping altogether. Fragile foods frequently need modified-atmosphere film packaging or barrier, along with perfect secondary packaging to ensure sufficient shelf life to be effective.

The tertiary packaging segment held the 15% market share in 2025 because it focuses on moving products smoothly through the supply chain. Packaging, such as crates, pallets, protective materials, and stretch wrap, is necessary for logistics and distributors' teams. Despite users rarely watching them, tertiary packaging is important for preventing damage while shipping and for smoothing management, stacking, and storage. Types of tertiary packaging include shrink film or stretch wrap, strapping or pallets, plastic crates, outer corrugated boxes, and metal or plastic drums.

The recyclable packaging segment dominated the packaging and containers manufacturing market with 46% share in 2025 as material which are willingly collected, recovered, or classified and made for reuse or recycling, which are secondary raw materials. Some of these materials include cardboard, paper, aluminum, glass, and plastics, which are recyclable in nature and are scrutinized as eco-friendly packaging choices to single-use plastics. Virgin fibres are necessary to remain in the recycling loop by delivering fresh, good-quality inputs that demand the storage of recycled packaging materials in circulation. When such fibers are obtained from responsibly managed FSC-certified forests, they deliver a sustainable option to fossil-based plastic packaging.

The reusable packaging segment held the 21% market share in 2025 because these covers are specifically smooth in the industry, with big shipment volumes and traditional return flows. Retail manufacturing, distribution, food logistics, and automotive supply chains all benefit from constant load preservation and resumption. They are insightful in environments in which damage risk is high, such as long-distance logistics or multi–drop delivery paths. By tracking the secured journey within the journey, reusable packaging covers and lowers the cumulative risk of managing the pollutants.

The biodegradable packaging segment held the 33% market share in 2025 because both compostable and biodegradable are particularly being designed to break down into more non-dysfunctional components. It gets decomposed quicker as compared to other biodegradable packaging, which are more typically used in food service uses like hospitality and restaurants. These materials develop upon remaining options because they come from the wastage of agricultural operations, which delivers producers a lower-cost foundation material and minimizes resource waste.

Asia-Pacific held a major market share of 41% in 2025 and is expected to have the fastest growth in the market with 5.3% CAGR during the forecast period. Macroeconomic elements, including inflationary pressures and currency volatility, continue to encourage import-export profit within the sustainable packaging sector. To align with these risks, brands are excessively accepting currency management in working and flexible pricing designs to make constant margins and track financial results. ESG-concentrated and sustainability regulations are also designing trade rules that affect the sustainable plastic packaging industry, which has carbon-liner measures and sustainability -source trade demands that push greener manufacturing practices.

Trends of Packaging and Containers Manufacturing Market in India

In India, government principles have played a crucial role in pushing businesses to shift towards effective packaging and container manufacturing. With rising issues about plastic waste and pollution, many rules have been introduced to lower plastic use and promote the use of eco-friendly and recyclable packaging materials. In the year 2022, India revealed a complete ban on many single-use plastic products to manage plastic pollution. Such a ban has covered the product like straws, cutlery, stirrers, and particular packaging.

North America held the second-largest market share of 23% in 2025, as the growth of grocery delivery and e-commerce services has also developed the urge for packaging and container manufacturers in this region. As online retailers make logistics of products directly to users’ houses, they experience the mounting pressure to avoid unwanted packaging and substitute plastic with recyclable options. Fiber-based mailers, such as correctly sized corrugated boxes and molded pulp trays, have become popular choices over plastic foam and poly mailers.

Trends of Packaging and Containers Manufacturing Market in the U.S.

The U.S. market is driven by high-level digital design, highlighted innovative systems, and a huge spread of company acceptance and correct funding in green technologies, which has collectively kept the country as a main leader in the environmentally friendly packaging innovation. Such factors develop fast involvement, implementation of eco-friendly packaging solutions, and fast deployment across several uses, which validates the industry's resilience and development capability. As an outcome, application-driven urge remains the initial catalyst that is designing the future scenario of the environmentally friendly packaging industry in the U.S.

By Material Type

By Packaging Type

By End-use Industry

By Functionality

By Sustainability Type

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarPackaging and Containers Manufacturing Market