The extra high-performance linerboard market is booming, poised for a revenue surge into the hundreds of millions from 2026 to 2035, driving a revolution in sustainable transportation. This market is highly influenced by high-strength kraft linerboard, which is primarily used for durable packaging, particularly in e-commerce and heavy-duty applications. The major factors driving the growth of the extra high-performance linerboard market are increasing demand for strong, sustainable packaging and the expanding e-commerce sector.

Extra-high-performance linerboard is a category of containerboard produced to meet precise, demanding strength requirements beyond those of standard linerboard. This material is engineered with higher basis weights, stronger fiber compositions, and tighter quality controls to support heavy-duty performance in challenging transport conditions. Manufacturers design it to withstand compression, puncture risk, moisture exposure, and stacking pressure, making it suitable for industries that require reliable protection for valuable or sensitive goods.

These liners are often used for specialized applications such as HazMat packaging and are considered stronger than standard linerboard. They help ensure compliance with strict safety regulations by offering consistent structural integrity during handling, shipping, and storage. Products that fall into hazardous or high-risk categories benefit from linerboard that resists tearing, prevents leaks from box failure, and maintains shape even under stress. This reliability supports safer logistics and reduces the likelihood of product loss or transport-related incidents.

Market Growth Overview: The extra high-performance linerboard market is expanding due to growing demand for e-commerce expansion, consumer preferences, durability, technological innovations, industrialization, and urbanization. The increase in parcel shipments and the need for packaging that withstands long-distance transport are further supporting the upward trend. Manufacturers are also investing in improved fiber blends and advanced production systems that help maintain strength and sustainability.

Global Expansion: Regions such as Latin America, North America, Asia Pacific, Europe, South America, the Middle East, and Africa are witnessing rising demand for innovative, sustainable, durable, and protective packaging. These regions benefit from rapid trade flows and stronger retail networks that rely on packaging with predictable performance. Growing awareness about waste reduction and material efficiency is also encouraging the adoption of high-performance grades.

Major Market Players: The extra high-performance linerboard market includes International Paper Company, Mondi Plc, Stora Enso Oyj, D S Smith Plc, Smurfit Kappa Group Plc, and many others. These companies are focusing on product innovation, capacity upgrades, and partnerships that support long-term supply commitments. Their efforts help meet rising expectations from logistics providers, retailers, and industrial users who require consistent strength and reliability.

Startup Ecosystem: The startup industries play an important role in developing special chemical additives, novel fiber sourcing, automation software, sustainable solutions, and various other advancements. These startups introduce fresh design ideas and technical experimentation that accelerate performance improvements. Their contributions help established producers adopt new methods that enhance strength, reduce weight, and improve environmental outcomes across the value chain.

Technological transformation in the extra high-performance linerboard market plays a significant role by introducing advanced fiber processing, digital printing integration, circular-economy integration, coatings, and nanotechnology. These progressions emphasize enhancing performance while decreasing ecological impact and increasing operational efficiency. Manufacturers are capitalizing heavily on advanced pulp purification and processing to produce high-value, lightweight grades that enhance or maintain durability and strength. Progressions in the digital printing process are enabling cost-effective modification and superior-quality visuals on linerboard.

Kraft paper and paperboard exporters reported substantial trade values in 2023. The United States, Sweden, and Finland were among the largest exporters of kraft paper and paperboard in 2023, with the United States reporting at about USD 3.11 billion, Sweden USD 2.39 billion and Finland USD 0.83 billion for the broader kraft paper grouping. These volumes reflect the large-scale production of liner grades and specialty kraft products used in industrial packaging.

For finished paper packing articles, China is a dominant global supplier of cartons, trays and other packing containers, accounting for very large export volumes in 2022–2023 and supplying both low-cost and mass-market thermoformed and corrugated solutions to global buyers.

Major importers of kraft liner inputs and linerboard-based finished packaging include manufacturing and retail hubs in Germany, Italy, the United States, and other high-value consumer markets that require high-strength corrugated solutions for industrial, appliance, and beverage sectors. These markets import both liner rolls and finished corrugated formats, depending on local converting capacity.

Shipment trackers and customs logs show concentrated exporter lists for liner proxies. For tracker snapshots, countries such as the United States, Sweden, Finland, and selected European producers appear near the top by export value. For finished packing containers, China and a set of East Asian converters dominate shipment counts and tonnage into global import hubs.

Volza and other shipment trackers record frequent, recurring export consignments from US and European liner producers and high shipment counts from Asian converters for finished cartons. These shipment-level signals are useful to identify active suppliers and typical trade lanes.

Traded forms include jumbo liner rolls (high basis-weight kraftliner), coated linerboard, and finished corrugated cartons and trays. Jumbo rolls are the typical imported form when a destination has local converting capacity, while finished cartons are shipped where local converting is limited or where finished printed packs are required.

Unit value differs strongly by form. High-performance, coated or white-top linerboard trades at a notable premium to commodity kraft. Public export summaries show much higher per-tonne values for coated or specialty liner grades exported from Europe and North America than for plain commodity rolls from lower-cost regions.

The major raw materials utilized in this market are recycled paper and plant fiber. Producers depend on stable sourcing networks to secure consistent fiber quality that supports strength performance.

The component manufacturing in this market comprises pulp preparation, forming, pressing and drying, innovation, and enhancement. Advanced mechanical and chemical pulping techniques help improve fiber bonding and structural strength, which is essential for high-performance grades.

This segment is growing focus on high-strength packaging material and sustainability. Distribution networks prioritize efficient handling, optimized storage, and safe delivery to converters and end users across global and regional markets.

")

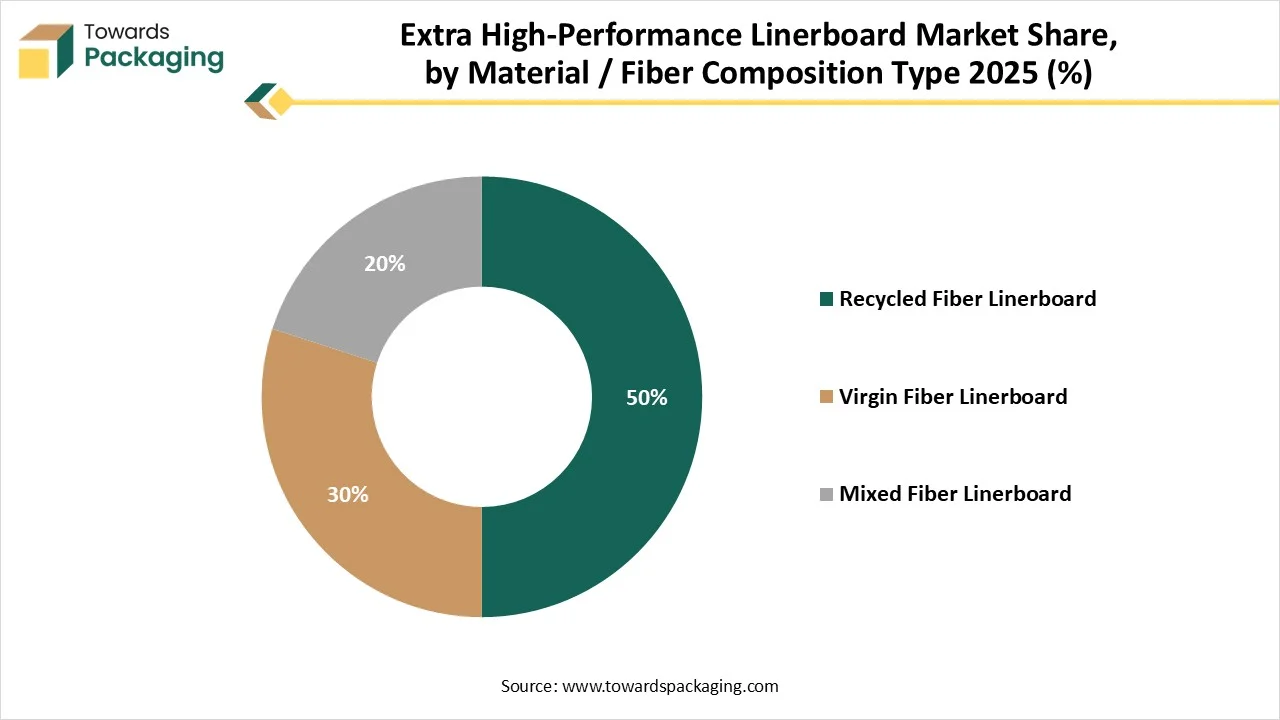

The recycled fiber linerboard segment dominated the market, accounting for the highest share in 2025, due to its sustainability and cost-effectiveness. This supremacy is influenced by cost-effectiveness, robust sustainability standards, and improvements in fiber handling that enable recycled materials to meet demanding presentation requirements. Growing ecological concerns, government recycling mandates, and business sustainability goals are driving firms to incorporate recycled content. Recycled waste paper is commonly less expensive than virgin pulp, helping reduce raw material costs for packaging producers.

The mixed fiber linerboard segment is expected to grow at the fastest CAGR during the forecast period of 2025 to 2035. This segment is growing due to its balanced performance and increasing adoption. Mixed-fiber compounds blend the surface strength and smoothness of virgin kraft with more cost-effective, recycled core layers. This permits producers to meet essential strength requirements for transportation packaging while controlling costs.

The virgin fiber linerboard is the fastest-growing in the extra high-performance linerboard market, as it offers performance, reliability, and superior strength. Its extended fibers offer excellent strength and predictable performance compared to recycled materials, making it ideal for demanding applications such as heavy-duty shipping and long-distance transport. Virgin fibers are stronger and longer, providing superior bursting strength and edge crush resistance, which are important for preserving structural integrity in high-performance applications.

| Product Type / Grade Segments | Market Share 2025 (%) |

| Kraft Linerboard (Kraftliner) | 45% |

| Testliner | 20% |

| White-Top Linerboard | 10% |

| Coated / Specialty Linerboard | 25% |

The Kraft linerboard (kraftliner) segment dominated the market with the highest share in 2025, driven by high performance and alignment with sustainability. It is mainly used as the intermediate and outer plies in corrugated fiberboard, creating a strong, durable base for transportation boxes and containers used across several sectors, including food & beverages, industrial, and e-commerce goods. The rise of e-commerce has underscored the need for robust packaging that can protect products throughout complex logistics chains. The inherent superior strength of kraft liner, combined with its role in the expansion of the e-commerce and logistics industries and its alignment with sustainability trends, solidifies its dominant position in the market.

The coated / specialty linerboard segment is expected to grow at the fastest CAGR during the forecast period of 2025 to 2035. This segment is growing due to sustainability mandates and performance necessity. The drive for high-performance features, such as amplified force-to-weight ratio, durability, and moisture barrier, is fast-tracking the adoption of coated and specialty linerboard products. These resources are important for shielding products in demanding usages such as industrial, e-commerce, and food delivery machinery. The business is progressively emphasizing the development of lightweight, high-value grades that fulfil sustainability aims and regulatory standards.

The white-top linerboard is the fastest-growing in the extra high-performance linerboard market, as it offers enhanced graphics and superior-quality packaging. It is progressively valued for e-commerce and luxury retail packing. This emphasizes visual appeal, which promotes rapid development and greater effectiveness for producers. This segment is a rapidly evolving, high-value role, but the absolute capacity and recognized utilization of traditional linerboard uphold its entire market.

")

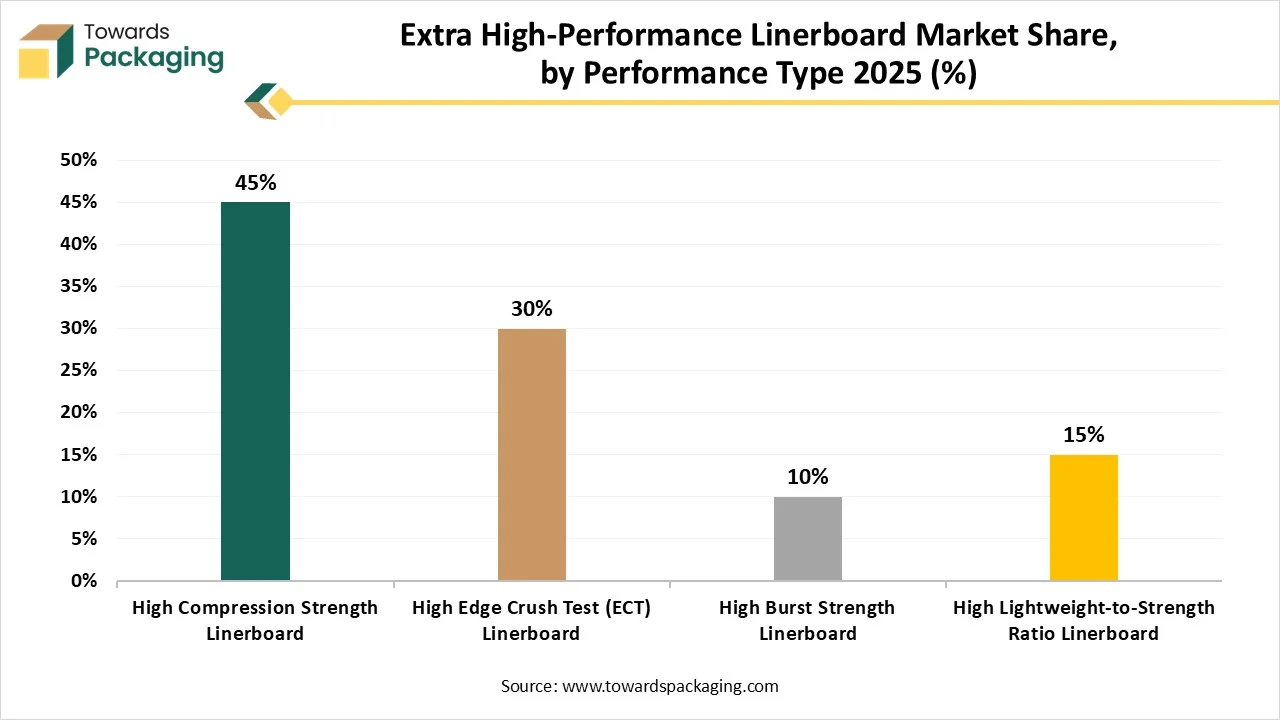

The high-compression-strength linerboard segment dominated the market, accounting for the highest share in 2025, driven by enhanced demand for protection, rigidity, and durability. The exponential growth of e-commerce requires robust packaging that can withstand complex distribution chains and multiple management points. High solidity forte linerboard safeguards product security during transportation, directly addressing this essential requirement. Inventions in engineering enable lightweight linerboards that preserve or even enhance strength.

The high lightweight-to-strength ratio linerboard segment is expected to grow at the fastest CAGR during the forecast period of 2026 to 2035. This segment is growing rapidly due to the e-commerce sector's expansion. The need to reduce transport weights to protect logistics costs and reduce carbon emissions further promotes the acceptance of these progressive, lightweight resources. This dominance is determined by the significant demand for packaging that is sturdy enough for transportation and light enough to reduce transport costs and environmental impact.

The high-burst-strength linerboard is the fastest-growing in the extra high-performance linerboard market, as it offers excellent strength, superior performance, and durability. It is mainly used for the outer coatings of rigid packaging, especially for shipping high-value or heavy products that need maximum protection during long transportation routes. The reliable value of virgin fibers offers more predictable performance, which is important for sectors that cannot risk delivery damage over longer distances. Sturdy demand from industries such as pharmaceuticals, consumer goods, e-commerce, and automotive, which require strong, reliable packaging, further reinforces this segment's dominance.

| End-Use Industry Segments | Market Share 2025 (%) |

| E-commerce Packaging | 40% |

| Consumer Goods (Electronics, Appliances, Retail Packaging) | 30% |

| Food & Beverage Packaging | 15% |

| Industrial Packaging | 10% |

| Agricultural / Bulk Packaging | 5% |

The e-commerce packaging segment dominated the market in 2025, with the highest share, driven by protective, durable packaging. The rapid and consistent growth of worldwide e-commerce, enhanced by the rapid spread of the internet and changing customer habits, is the main driver of packaging resources, including high-presentation linerboard. Customers and guidelines are driving more environmentally friendly choices. It permits the formation of lightweight and strong boxes. It also reduces transportation costs and weight, which is a primary advantage for e-commerce processes.

The consumer goods (electronics, appliances, retail packaging) segment is expected to grow at the fastest CAGR during the forecast period of 2026 to 2035. This segment is growing due to its strength and durability. These are the most widely used products, as their sturdy structure provides critical cushioning and firmness resistance during transportation. There is a growing emphasis on sustainable packaging options, with a shift toward biodegradable and recyclable materials, such as high-performance paper-based linerboard, to meet customer preferences and environmental guidelines.

The food & beverage packaging segment is the fastest-growing in the extra high-performance linerboard market, as it offers sustainable, safe, and strong packaging. The resource supports in maintaining the essential hygiene measures and can be planned with waterproof or greaseproof resistance, important for food usage. Increasing ecological concern among customers and strict government guidelines are prompting brands to avoid using plastics and to increase the use of biodegradable and recyclable paper-based packaging options, such as linerboard.

Asia Pacific held the largest share of the extra high-performance linerboard market in 2025, driven by increasing demand for high-quality, durable packaging. The rapid expansion of the e-commerce sector requires robust packaging to ensure products reach customers undamaged. Rising ecological awareness is prompting companies to adopt more sustainable packaging options, such as cardboard and paper, which are often preferred by customers over plastic. Major industries in this region are innovating with new skills, such as smart sensors and nanocoatings embedded in containerboard, to create more advanced packaging options.

Strong manufacturing potential and rising focus on sustainability have driven demand for extra-high-performance linerboard in China. The massive, swiftly rising e-commerce sector is a major driver, generating enormous, continuous demand for strong, reliable packaging to manage parcel capacity. A rising emphasis on sustainability, driven by customer demand and government mandates to reduce plastic use, is shaping the market toward more environmentally friendly, recyclable packaging options.

The increasing demand for lightweight, durable packaging has driven the extra high-performance linerboard market. The huge growth in online shopping has generated high demand for strong, reliable packaging to protect products during transportation. Extra-high-presentation linerboard provides the essential durability and strength to safeguard products for undamaged delivery, which is important for consumer approval in the competitive e-commerce sector. Rising ecological concerns and stringent government guidelines on plastic waste have prompted firms to adopt environmentally friendly substitutes.

Enhanced technological advancement has boosted the development of the high-performance linerboard market in Canada. The notable growth of the online sector in Canada has driven increasing demand for lightweight yet durable packaging to ensure product protection during shipping. It directly influences the necessity for enhanced-performance linerboard. This emphasis on a high strength-to-weight ratio is important for improving logistics and reducing transportation costs.

The major factors influencing the growth of the extra high-performance linerboard market are increasing recyclability mandates, sustainability, and consumer preferences. The surge in online shopping has created a strong demand for safe, durable, and lightweight packaging to protect products during transportation. It is a perfect resource for these boxes used in e-commerce because of its strength-to-weight ratio, which helps reduce transportation costs while ensuring product quality. Inventions in containerboard manufacturing technology, such as progressive fiber manufacturing and the use of bio-based coatings, have led to stronger yet lighter boards. These technical enhancements enable producers to meet high-performance requirements.

The rapid growth of the e-commerce sector and the demand for premium packaging have fuelled the development of the extra high-performance linerboard market. Its strong commitment to sustainability and the reduction of plastic waste generation are significant drivers. These linerboards provide a sustainable alternative to plastics, and their recyclability is a major advantage in a circular economy. Inventions in printing technology, nanotechnology, and digital skills are enhancing the potential of linerboard.

By Material / Fiber Composition

By Product Type / Grade

By Performance Type

By End-Use Industry

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarExtra High-Performance Linerboard Market