The Nonwoven Fabrics Market is projected to grow from USD 62.96 billion in 2026 to USD 97.09 billion by 2035, registering a CAGR of 4.93% during the forecast period from 2026 to 2035. The report provides detailed insights on market size, segment data by material, technology, function, and end-use industries, along with regional data across major global markets.

It also includes competitive analysis, key company profiles, manufacturers and suppliers data, trade statistics, and value chain analysis. Market growth is supported by the increasing demand for disposable hygiene products, expanding healthcare expenditure, sustainable and recyclable nonwoven solutions, and rising applications in automotive lightweighting and construction.

The nonwoven fabrics industry is experiencing massive growth driven by technological advancements, innovations, creativity, and increased adoption of advanced technologies, which are a boon to the industry. The noteworthy investments from various regions show the interest of the giants and respective nations. For instance, Europe’s sustainability and innovation factor involves a fair number of acquisitions, such as Fibertex Nonwovens and Texol.

While Fitesa’s launch of the Swedish spunmelt line and Ahlstrom’s smart expansion for filtration in Italy are robust investments for the nonwoven fabrics sector. Alongside, MEA sincerely invests in operating independently without any import dependency. For the same reason, PFNonwovens has expanded its business in Egypt and South Africa. North America's focus on modernised industrial and medical applications brings billions of investment to the vast nonwoven fabrics industry.

Moreover, the alliances of giants and ample business ideas introduce certain cultural differences, but close recognition of this industry. The potential extension of Berry Global marks the success of China. The massive development of new facilities and reconsideration of production potential are justifying the heavy investment volume across regions.

The nonwoven fabrics market encompasses engineered fabrics manufactured by bonding fibers through mechanical, chemical, or thermal processes rather than traditional weaving or knitting. These fabrics are widely used in hygiene products, medical textiles, filtration, automotive, construction, and packaging due to their lightweight nature, cost-effectiveness, durability, and versatility.

At the research frontline, companies like the National Institute of Standards and Technology 9NIST) are making autonomous laboratories, in which robotics and AI execute, design, and track experiments without human involvement. X-ray images and microscopy, which once needed meticulous manual review, are now analyzed by machine -learning models, which have the potential of flagging faults or structural characteristics in real time.

For nonwovens, these points of view at a future in which AI could grow and develop the biodegradable fibers, which are PFAS-free, free diagnosis, or antimicrobial finishes that speed up the R&D cycles from years to months. In reality, it serves as a space for how material invention may be redeveloped.

Furthermore, to align with the urgent needs of sectors like construction and automotive, high-performance synthetic fibres have been developed. These fibres serve durability, superior power, and resistance to heat and chemicals.

")

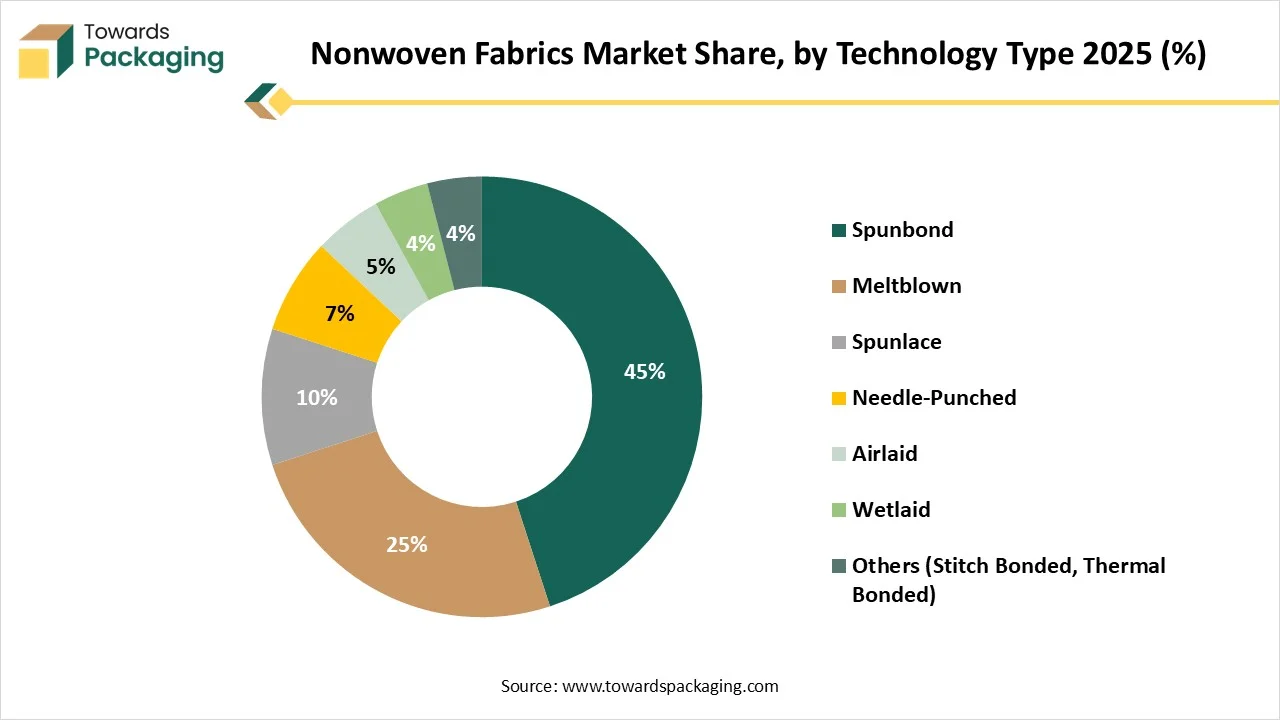

The spunbond segment has dominated the nonwoven fabrics market with a 45% share in 2024, as the spunbond procedure is widely used to generate nonwoven fabrics. The procedure of creating spunbond fabrics integrates the manufacturing of fabrics with the production of filaments. Elements of a spunbond procedure typically include an extruder, polymer feed, a die assembly, a web formation, and winding too. High procedure smoothness and perfect properties of these fabrics have made them acceptable in various areas of application, such as in medical and disposable uses, filtration, automotive industry, packaging, civil engineering, and carpet backing too. As it avoids fast steps, it is the shortest textile path from fabrics to polymer in one stage and offers possibilities for developing manufacturing and reducing costs. In the past years, spun bond nonwoven has grown rapidly due to its perfect characteristics and high process smoothness.

The meltblown segment is expected to grow at the fastest CAGR during the forecast period. The meltblown technology is one of the most productive techniques for manufacturing fine, highly smooth filter media. Meltholon fibres can receive diameters of less than 10 microns, accurate to 12th the size of the human hair and 15th the size of the cellulose fibre, which enables perfect filtration performance. The procedure starts with raw synthetic thermoplastic materials such as polyethylene tetraphthalate, polypropylene, or polybutylene terephthalate 9PBT). These kinds of materials are being extruded and melted through a die having various microscopic nozzles.

| Material Segments | Market Share 2025 (%) |

| Polypropylene (PP) | 55% |

| Polyester (PET) | 20% |

| Polyethylene (PE) | 10% |

| Rayon/Viscose | 5% |

| Wood Pulp & Natural Fibers | 5% |

| Biodegradable Polymers (PLA, PHA, etc.) | 5% |

The polypropylene segment has dominated the nonwoven fabrics market with a 55% share in 2024, as they are material created from polypropylene fibers that are integrated together through different techniques instead of being knitted or woven. This bonding can be achieved through chemical, mechanical, or thermal procedures, which results in a fabric with unique properties. Just like regular fabrics, which are made by knitting or weaving threads, non-woven fabrics are made from fibres. The polypropylene fibres are being organised, which serve the fabric with its exceptional characteristics and texture.

The biodegradable polymers segment are predicted to rise at the fastest CAGR during the forecast period. Biodegradable nonwoven fabric shows an inventive strategy in the textile sector, which is a replica of the rising awareness of environmental sustainability. Just like regular woven fabrics, which count interlaced threads, nonwoven fabrics are created by bonding fibers collectively through thermal, mechanical, and chemical procedures. This comes in a fabric that is perfect for a huge range of uses, such as medical supplies, hygiene products, and environmentally friendly bags. The different patterns of nonwoven fabrics enable adaptability in functionality and design, which makes them a preferred choice in different sectors.

")

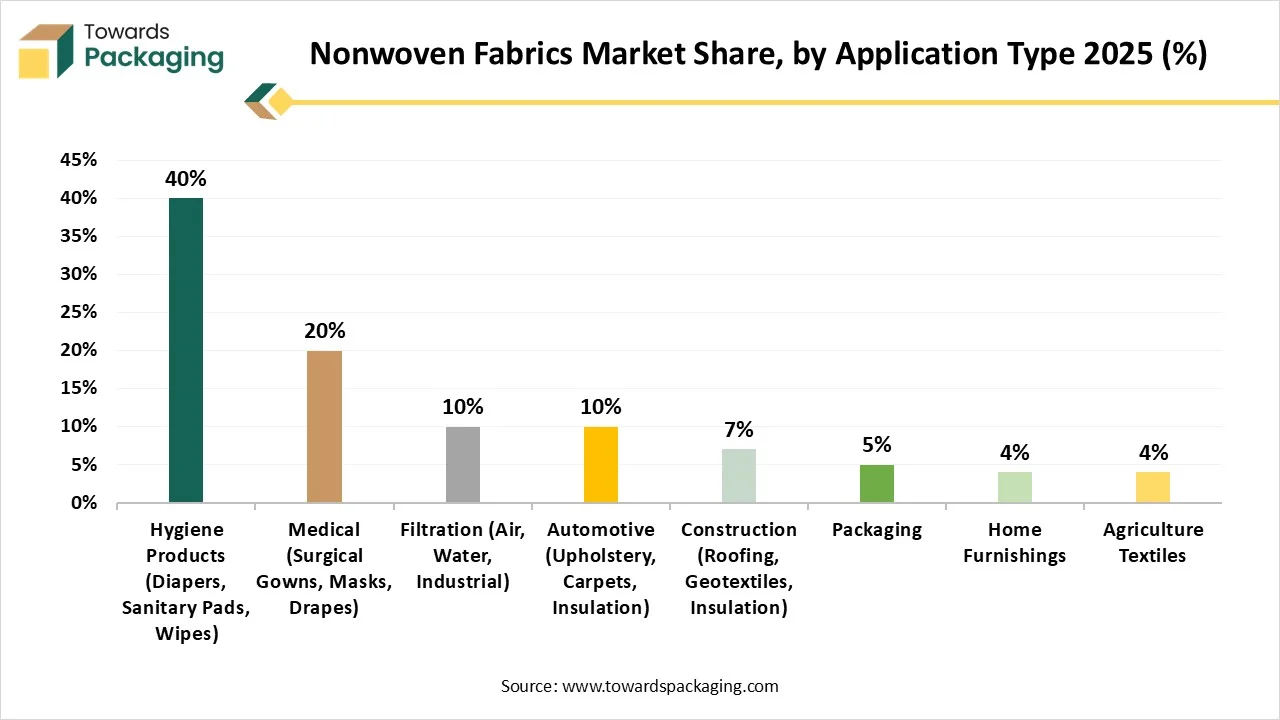

The hygiene products segment has dominated the market with a 40% share in 2024, as these fabrics are crafted textures designed particularly for healthcare and personal care applications. Just like woven fabrics, nonwovens are created by integrating fibres collectively through different procedures. This production flexibility enables personalised characteristics such as absorbency, softness, breathability, and barrier protection too. These fabrics are utilised in products like wipes, disposable masks, surgical drapes, and incontinence products. The urge for hygiene nonwovens is driven by rising health awareness, strict hygiene standards globally, and aging populations, too. Their disposable nature assists infection control and lowers cross-pollution risks.

The medical textiles segment is expected to rise at the fastest CAGR during the forecast period. The medical industry is constantly developing, with inventions proposed to improve safety, patient care, and hygiene. One of the most updated materials in this field is non-woven fabric, which has changed the manufacturing of medical disposables. From surgical masks to gowns, wipes, drapes, and non-woven fabrics are now indispensable in ensuring effectiveness and safety in medical textiles. As technology develops, these materials are meant to play an even more complicated role in healthcare, making sure sustainable and safer solutions for professionals and patients.

| End-Use Industry Segments | Market Share 2025 (%) |

| Healthcare & Hygiene | 48% |

| Automotive | 15% |

| Construction & Infrastructure | 12% |

| Filtration & Industrial Processing | 10% |

| Consumer Goods & Home Care | 7% |

| Agriculture | 8% |

The healthcare and hygiene segment has dominated the market with a 48% share in 2024 as nonwoven fabrics are utilised to generate gowns which protect healthcare workers and patients from cross-pollutants. These gowns are crafted to be lightweight yet provide complete comfort and coverage. With the growing demand for personal protective equipment 9PPE0, nonwoven fabrics have been widely used to produce face masks and complete PPE kits. These masks serve protection and filtration while being breathable and comfortable. Nonwoven fabrics are a perfect choice for bath wipes and wound care products, which serve comfort and softness while also being disposable and absorbent. Other necessary items, such as show covers, medical gloves, and bed sheets, are also prevalently created from nonwoven fabrics, ensuring patient safety and hygiene too.

The Automotive segment is predicted to rise at the fastest CAGR during the forecast period. Nonwoven materials are heavily utilised in the automotive sector, driven by the rising demand for lighter, more sustainable materials that develop both comfort and vehicle performance. As automotive designers concentrate on lowering weight, developing acoustics, and assisting eco-friendly goals, nonwovens are heavily classified as a solution. The development of electric vehicles also opens up new possibilities for these materials, as top manufacturers and suppliers predict an intensified role for nonwovens in the future.

Asia Pacific dominated the market with a 50% share in 2024, as this region is witnessing a fast trend, driven by growing demand in the medical, hygiene, and automotive fields. Market expansion is further developed by technological development in production and a rising focus on sustainability. India and China are the main players in the region due to their robust manufacturing bases and substantial populations. Growing health consciousness and growing disposable incomes in the Asia Pacific are fulfilling the urge for disposable hygiene products such as sanitary napkins, diapers, and adult incontinence products. The COVID-19 pandemic has also led to an increase in the use of nonwovens for medical supplies, such as face masks and surgical gowns. The reliability and acceptability of nonwoven fabrics, specifically polypropylene-dependent materials, make them perfect for a huge range of uses. The spunbond technology is known for its high efficiency, which dominates the market.

The nonwoven fabrics market in China is sizable and expanding. Key growth drivers include rising healthcare infrastructure, increasing demand for eco-friendly and high-performance nonwovens, and innovation in green technologies like biodegradable and nanofiber nonwovens. However, environmental pressures and regulatory policies are pushing manufacturers toward more sustainable raw materials.

North America is expected to be the fastest-growing in the market during the forecast period. The medical and hygiene industries are the biggest drivers of nonwoven fabric usage in North America. The market is being fulfilled by growing health awareness, specifically in the post-pandemic era. An ageing population, which drives the consumption of adult non-constant items. Urge for disposable items like feminine hygiene products, diapers, wipes, and surgical gowns. Manufacturers are moving new capacity towards “long-life sustainable uses”, such as reliable materials that are crafted for recyclability, as per the Association of the Nonwoven Fabrics Industry.

North America’s advancement in this industry involves modernised manufacturing technologies like nanotechnology, AI, digitisation, and Spunlaid technology. These are the core technical advances in handling the mechanism of nonwoven fabrics manufacturing. The groundbreaking smart nonwoven fabrics allow integration of electronic components for real-time data, mainly for wearables and healthcare.

The nonwoven fabrics market in the United States is sizable and steadily growing. Key drivers include disposable nonwovens, especially for hygiene and medical applications, which are the largest revenue segment. Polypropylene is a major raw material.

Europe expects the notable growth in the market. Europe’s nonwoven fabrics market is also increasingly driven by sustainability: manufacturers are under pressure from EU circular economy policies and consumer demand to use bio-based and recycled fibres. Demand is diversified: disposable nonwovens (like hygiene and medical) dominate revenues, while applications in construction, filtration, and automotive are expanding.

The eco-friendly materials are the fundamental innovation of this region in this industry. The rPET, Lenzing’s wood-derived specialty fibres, and bio-based fibres are applauding specialization in the nonwoven fabrics making process. The manufacturer's willingness to experiment with material replacement has helped the region introduce sustainable innovation to the vast nonwoven fabrics industry. The challenging projects helped this region to prove its skill in intelligent functional nonwovens.

The UK nonwoven fabrics market is projected to grow significantly. Disposable nonwovens (e.g., hygiene, medical) dominate the market. Increasing demand for sustainable nonwovens including biodegradable and recycled materials is a key trend, driven by environmental awareness and regulatory pressures.

The nonwoven fabrics market in the Middle East & Africa (MEA) is growing strongly. Growth is largely driven by the disposable segment, especially in hygiene and medical applications. In Africa, expanding healthcare infrastructure (rising hospital-acquired infections) and construction investments are key demand drivers. In the automotive sector, MEA’s nonwoven fabrics market (especially spunbond) is also rising, supported by the need for lightweight, cost-efficient materials.

The UAE nonwoven fabrics market is estimated to grow at notable rate. Demand is driven largely by hygiene and healthcare applications like diapers, medical gowns, and masks as well as filtration and automotive uses. Spunbond technology is especially important, but meltblown is growing rapidly, largely due to its use in filtration and medical products.

The nonwoven fabrics market in Latin America is projected to grow significantly. Disposable nonwoven fabrics (used in hygiene and medical) are the largest and fastest-growing segment. Brazil is expected to show the strongest growth in the region. Demand is driven by rising healthcare infrastructure, hygiene awareness, and import activity, especially in countries like Mexico and Brazil.

Brazil’s nonwoven fabrics market is strong and growing. Growth is largely fueled by the disposable segment, especially hygiene and medical applications. Polypropylene nonwovens are especially prominent, driven by rising demand for diapers, PPE, and other hygiene products. Other key application areas include automotive interiors, construction geotextiles, and filtration.

Berry Global Group, Inc

Corporate Information

History and Background

Mergers & Acquisitions

Acquisition by Amcor (2024–2025)

Partnerships & Collaborations

Product Launches / Innovations

Key Technology Focus Areas

R&D Organisation & Investment

Strengths:

Weaknesses:

Opportunities:

Threats:

Recent News & Strategic Updates

By Technology

By Material

By Application

By End-Use Industry

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarNonwoven Fabrics Market