The liquid packaging board market provides a complete view of global market size, growing from USD 44.71 billion in 2026 to USD 86.07 billion by 2035 at a 7.55% CAGR. This report covers segment-level insights including SBS leading with 61.1% share, cartons dominating with 52.5%, and dairy applications holding 46.8% along with regional data showing Europe at 37.6% share and APAC growing fastest at 8.5% CAGR. It includes value chain analysis, trade flows, top exporters (U.S., India, Brazil), import–export patterns, and competitive intelligence on leading market players such as Stora Enso, WestRock, Billerud, Nippon Paper, and Tetra Pak.

Liquid packaging boards are multi-layer paperboards designed to safely package and preserve liquids such as milk, juice, soups, and other beverages. It is made from high-quality bleached chemical pulp with polyethylene or aluminum coatings to provide barrier protection against moisture, oxygen, and light. Known for durability, stiffness, and printability, liquid packaging board supports aseptic and sustainable packaging solutions. Increasing demand for recyclable and renewable fiber-based materials is driving growth in food and beverage packaging applications.

The enhancement of productivity and increased production efficiency have driven technological advancement in the liquid packaging board market. Progressive engineering procedures make the creation of liquid packaging boards more effective and cost-effective. Technology is being developed to produce boards with a smaller carbon footprint and to help develop recyclable and renewable resources to replace plastic. Inventions are also emphasizing the enhancement of recycling procedures for these complex resources to close resource cycles. Techniques now comprise three-layer coverings with useful fillers to fill fibre gaps, advance surface density, and improve water barrier and operational stability.

Trade in liquid packaging boards sits at the intersection of pulp & paper commodity flows and food-packaging value chains.

Coated/laminated specialty board with barrier layers (PE, EVOH, PLA coatings) and functional seals.

HS proxies in trade datasets commonly sit under coated/uncoated paper & paperboard headings, with some specialty items reported under food-grade/packaging sub-codes.

The major raw materials utilized in this market are paper pulp, plastic coatings, and aluminum foil.

The component manufacturing in this market comprises Paperboard, printing ply, polyethylene (PE).

This segment is involving a network of manufacturers, distributors, and end-users.

| Grade Segments | Market Share 2025 (%) |

| Solid Bleached Sulfate Board (SBS) | 61% |

| Coated Unbleached Kraft Board (CUK) | 18% |

| Uncoated Kraft Board | 21% |

The solid bleached sulfate board (SBS) segment dominated the market, accounting for a 61.1% share in 2025, due to its strength and excellent printability. The smooth, white board’s surface is ideal for high-quality printing, enabling vibrant graphics and complete branding on beverage containers and cartons. It is recognized for its excellent stiffness and strength, which are important for a liquid package that requires withstanding filling, transportation, and handling without distorting. Coated grades of board can offer high-level moisture resistance, an important need for containing liquids and protecting them from the environment.

The coated unbleached kraft board (CUK) segment is expected to grow at a 7.2% CAGR during the forecast period of 2025 to 2035. This segment is growing due to its high strength and durability. It is produced from virgin kraft pulp, unbleached, and has an organic brown color that demands to sustainability-emphasized branding. The coated surface provides a barrier against grease and moisture, which is important for packaged liquids and frozen food products. It is generally used for beverage carriers, frozen food cartons, and other applications that require wet-strength properties.

The uncoated kraft board is the fastest-growing in the liquid packaging board market, as it offers strength and superior barrier properties. It is primarily influenced by demand for natural-looking, sustainable, and environmentally friendly packaging choices. These are recognized for excellent tensile strength, superior folding endurance, and resistance to tearing, and are packed, which confirms the packaging remains integral during filling, shipping, and storage of weighty liquids.

")

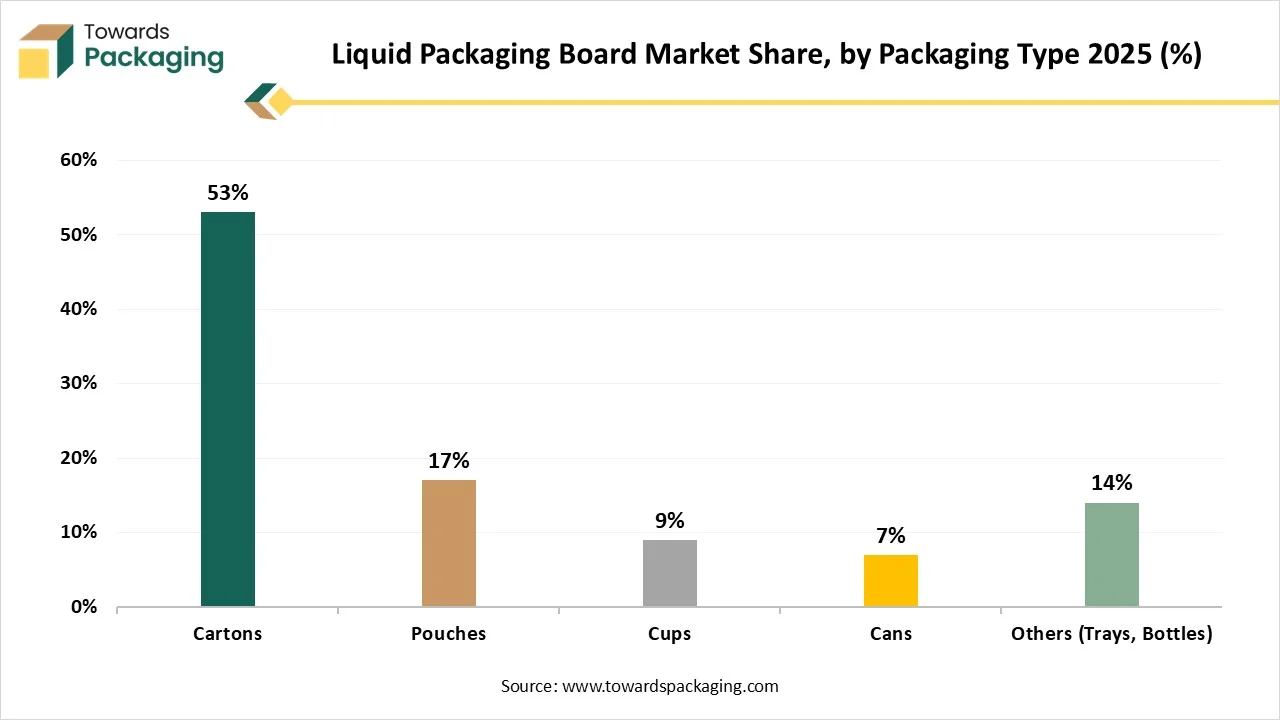

The cartons segment dominated the market, accounting for a 52.2% share in 2025, driven by bulk transportation and storage. A wide variety of cartons is used for a wide range of goods, such as juice and milk, providing advantages such as specialized designs, extended shelf life, and resealable features. The main applications for this segment include liquid juices, dairy products, and non-carbonated beverages. The cartons are patterned for both short-term and long-term shelf life, with extended cartons containing an aluminum layer to shield against oxygen and light.

The pouches segment is expected to grow at a 7.8% CAGR during the forecast period of 2025 to 2035. This segment is growing due to its portability, convenience, and lightweight design. These are gaining market share by providing a cost-effective, lightweight, and convenient alternative to outdated rigid packaging setups such as cartons, plastic bottles, and glass. Major drivers include rising customer demand for lightweight, convenient, and portable packaging that reduces transportation costs and storage space requirements. The rise of e-commerce favors pouches because of their compactness, durability, and lightweight nature, which reduces shipping costs and the risk of damage or leakage during transportation.

The cups segment is the fastest-growing in the liquid packaging board market, as it comprises single-use cups and containers. It protects liquid penetration, preserves product quality, and confirms functionality. It is coated or lined with barrier resources. Concerns about sustainability and the single-use plastic ban are boosting demand for environmentally friendly cup materials and coatings. The rise of cafe chains and quick service restaurants (QSRs) is a major influencer for this segment.

| Application Segments | Market Share 2025 (%) |

| Dairy Products | 47% |

| Juices & Beverages | 22% |

| Liquid Food (Soups, Sauces, etc.) | 10% |

| Alcoholic Beverages | 7% |

| Others (Pharmaceutical, Household Liquids) | 14% |

The dairy products segment dominated the market with a 46.8% share in 2025 due to its capacity to absorb moisture. It has excellent barrier properties against oxygen, light, and several other pollutants while transporting. These packages also provide strength for long-term storage of the products. It comprises a huge variety of products, like cream, flavored milk, liquid milk, yogurt, and various other value-added dairy-based beverages. The growth of this segment is influenced by rising customer demand for plant-based substitutes and dairy products across several countries, varying lifestyles, and the need for safe, convenient, and sustainable packaging.

The juices & beverages segment is expected to grow at a 7.4% CAGR during the forecast period of 2025 to 2035. This segment is growing due to its leak-proof and protective properties. It offers crucial protection and sealability for juices and several other beverages. It supports maintaining the integrity and safety of the goods inside. It is a recyclable resource, which brings into line with growing customer and supervisory demand for sustainable packing. Excellent moisture resistance protects against leaks, which is important for liquid goods.

The alcoholic beverages segment is the fastest-growing in the liquid packaging board market, driven by brand appeal and premiumization. A growing trend in the alcoholic beverage sector is driving demand for premium, high-quality packaging that enhances brand image. The drive for ecologically friendly packaging is influencing demand for easily recyclable materials such as glass and paper-based options.

")

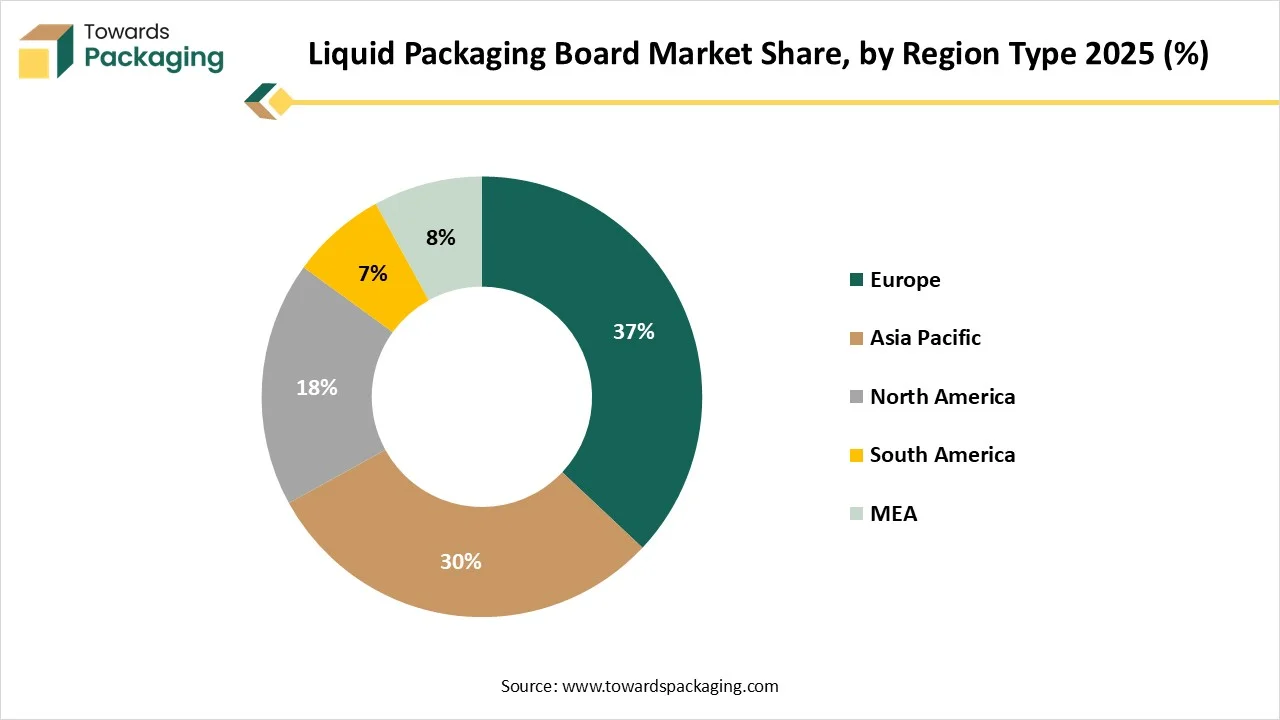

Europe held a 37.6% share of the liquid packaging board market in 2025, driven by increasing demand for recyclability and renewability in packaging. Customers are increasingly aware of environmental issues and are choosing sustainable packaging, driving demand for this packaging and positioning it as a more environmentally friendly alternative to plastic. These are more eager to recompense for extremely recyclable goods and look for on-pack data highlighting the environmentally friendly content of the packaging. These consumers are highly eager to buy highly recyclable goods and to seek on-pack data that highlights the packaging's environmental friendliness.

Advanced, innovative manufacturing infrastructure has driven demand for liquid packaging board in Germany. It has a strong production base and robust technological proficiency, enabling the production of high-quality, advanced liquid packaging boards. These customers are increasingly seeking environmentally responsible choices, and liquid packaging boards are seen as a sustainable option. Major corporations are at the forefront of emerging packaging technologies, comprising sustainable and functional materials that fulfil developing customer requirements for products such as plant-based and practical beverages.

")

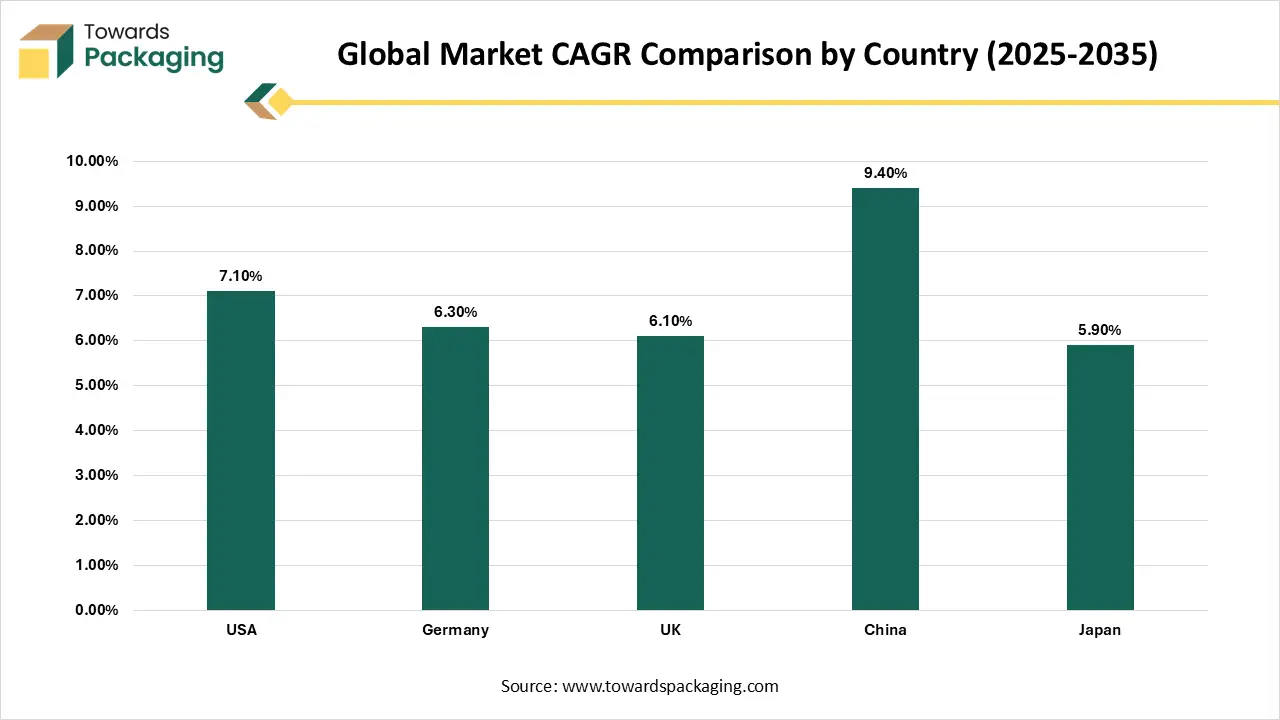

| Country | CAGR (2025-2035) |

| USA | 7.10% |

| Germany | 6.30% |

| UK | 6.10% |

| China | 9.40% |

| Japan | 5.90% |

The rising middle-class population and urbanization have increased demand for liquid packaging board. Fast urbanization in countries such as China, India, and others has resulted in a larger population in areas with higher disposable incomes and a growing demand for packaged products. There is a significant surge in demand for packaged dairy products, drinks, and other foods, driven by changing lifestyles and rising consumer awareness of product convenience and safety.

The demographic and economic shifts have accelerated development in the liquid packaging board market in China. Inventions in aseptic coating and processing technologies have extended the shelf life of goods packaged in boards, broadening their applications and expanding their use cases. The two major advantages of water-based inks and new barrier technologies make the packing more suitable and functional for sensitive items. The rapid development of e-commerce and modern trade channels across China requires effective, durable packaging solutions for supply. Liquid packaging board fulfils these requirements by being eco-friendly, lightweight, and easy to transport, making it a perfect fit for current logistics demands.

| Country | Unit | Mar 2019 Qty | Mar 2019 Value (INR) | Apr 2018–Mar 2019 Qty | Apr 2018–Mar 2019 Value (INR) |

| China P RP | KGS | 326,950 | 58,912,400 | 4,602,480 | 787,954,000 |

| Hong Kong | KGS | 17,420 | 5,028,600 | 544,880 | 191,684,300 |

| Sri Lanka DSR | KGS | 125,360 | 18,742,900 | 897,540 | 167,014,600 |

| Vietnam | KGS | 19,510 | 3,846,200 | 924,120 | 139,998,700 |

| South Africa | KGS | 240,380 | 23,812,900 | 1,093,980 | 110,936,200 |

| Israel | KGS | 1,430 | 55,672,900 | 2,260 | 55,813,900 |

| U Arab Emirates | KGS | 35,980 | 1,886,700 | 300,920 | 45,148,900 |

| USA | KGS | 670 | 803,900 | 141,320 | 39,257,800 |

| Germany | KGS | 8,860 | 2,104,300 | 153,240 | 36,942,900 |

| Korea RP | KGS | 1,710 | 1,014,900 | 125,900 | 19,742,300 |

| Sweden | KGS | 1,630 | 1,575,900 | 19,820 | 16,402,800 |

The major factors influencing the growth of the liquid packaging board market are customer environmental consciousness, stringent regulations, extended shelf life, product protection, technological advancements, convenience, and the e-commerce sector. Customers are increasingly seeking packaging that is biodegradable, recyclable, and made from renewable resources. This consciousness has enabled food & beverage brands to evolve from traditional glass and plastic containers to cartons made from other materials.

The rising consumer convenience initiatives and changing lifestyle in the U.S. which fuelled the development of the liquid packaging board market. The rising demand for ready-to-consume beverages, driven by on-the-go and busy lifestyles, is making portable, lightweight packaging options like cartons increasingly popular. This comprises products such as nutritional shakes, juices, and coffee drinks. Increasing consumer consciousness has driven significant shifts towards environmentally friendly packaging choices. Liquid packaging board is frequently produced from renewable materials like paper and is recyclable, aligning with both customer preferences and the growing regulatory focus on sustainability.

By Grade

By Packaging Type

By Application

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarLiquid Packaging Board Market