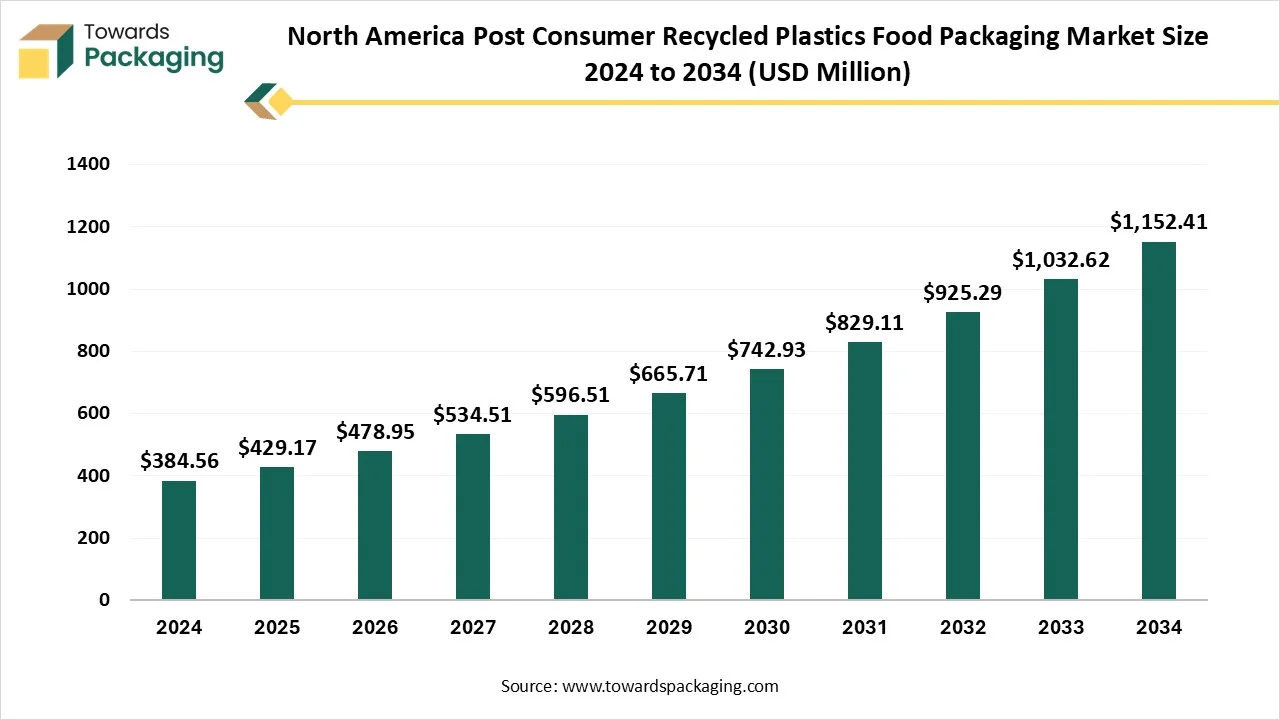

The North America post-consumer recycled plastics food packaging market is forecasted to expand from USD 478.95 million in 2026 to USD 1,286.09 million by 2035, growing at a CAGR of 11.60% from 2026 to 2035. This growth is driven by the rising demand for sustainable packaging solutions across various industries, particularly food and beverages. The market is segmented by material type, packaging type, raw materials, and end-use industries, with key materials including PET and HDPE. The food segment holds the largest share, while the beverage segment is expected to grow the fastest. The report also includes detailed regional analysis, trade data, value chain insights, and a competitive analysis of top companies such as Amcor, Eastman Chemical Company, and DOW, Inc.

Post-consumer recycled content ,which is often pointed to as a PCR, is an material which is made from the products that users recycle each day, like cardboard boxes, aluminum ,paper and plastic bottles. These materials are specifically collected by the local recycling programs and transported to the recycling facilities which need to be stored into bales, depending on the material.

The balls are then buyed and melted into molded into new items and small pellets. The new PCR plastic material can then be utilised for a variety of complete products, counting packaging.

| Metric | Details |

| Market Size in 2025 | USD 429.17 Million |

| Projected Market Size in 2035 | USD 1,286.09 Million |

| CAGR (2026 - 2035) | 11.60% |

| Market Segmentation | By Material / Resin Type, By Packaging / Product Type, By Raw Material / Waste Stream Source and By End-Use / Application |

| Top Key Players | Amcor plc, Eastman Chemical Company, Exxon Mobil Corporation, DOW, Inc., Plastic Energy, Sabic Innovative Plastics, Green Dot Bioplastics, Flexibles & Packaging, and Amcor Flexibles. |

AI systems are filled with the deep learning and computer vision models, which can classify between the different types of plastics, even those that appear deceptively alike. This accuracy make sure that every type of plastic is being directed to the accurate recycling stream, which develops the quality of the recycled materials and the amount of waste collection and recycling credits.

AI doesn’t need to just sort, but by tracking the data in actual time, AI systems can track the smoothness of waste processing, suggest improvements and identify bottlenecks. This has led to constant updation of the recycling procedure and plastic neutrality.

By implementing AI into the Material Recovery Facilities which automates the sorting procedure, lowering down the dependency on manual labour and lowering the errors. This automation develops operations and cuts down costs, that makes recycling and resource updation more economically viable.

By developing the solvolysis to carry the composite materials and enzymatic recycling for the PET, these machines smoothly recover raw materials with great purity. The AI-powered sorting machines classify the plastic types with great accuracy ,that allows the smooth integration of chemical and mechanical recycling lines in the large-scale facilities.

According to the global data, North America Food Packaging has imported during the period April 2025 to March 2025.These imports were being supplied by the 24 exports to 26 buyers, having an market development of 139% as compared to the preceding twelve months.

World has imported most of its North America Food Packaging from United States , China and Japan. Globally , the top three importers of the North America Food Packaging are United States, Colombia and Vietnam too.

Colombia is at the forefront with 149 shipments ,which is being followed by the United States having the 106 shipments, and Vietnam taking the third position having the 4 shipments.

Complex Patterns Gets Addressed By Mono-Material

One of the biggest issue in food packaging recycling is the protection of the multi-layer materials which integrate various papers, polymers and metallized films to receive compulsory barrier properties. These complicated pattern, while smoothness for the food preservation are online impossible to recycle in convenient machine.

The mono-material updation solves this challenge by crafting single-material packaging which receives comparable performance with the assistance of high level structural design and polymer science instead of material lamination. By concentrating on polyethylene (PE), or polypropylene films with developed barrier characteristics, or by making paper-based solutions having an bio-based coverings, producers can now make fully recyclable packaging without adjusting product protection.

Cost Of Sustainable Material Lacks In Food Packaging

Despite these inventions, there are still issues. Sustainable materials are more costly to generate as compared to regular plastic, which can be an barricade for medium and small -sized organizations. There’s also cultural opposition. The shortage of design for recycling or composting makes it even rigid. Without the correct systems, several compostable materials end up in landfills or incinerated ,that canvas out their surrounding benefit.

")

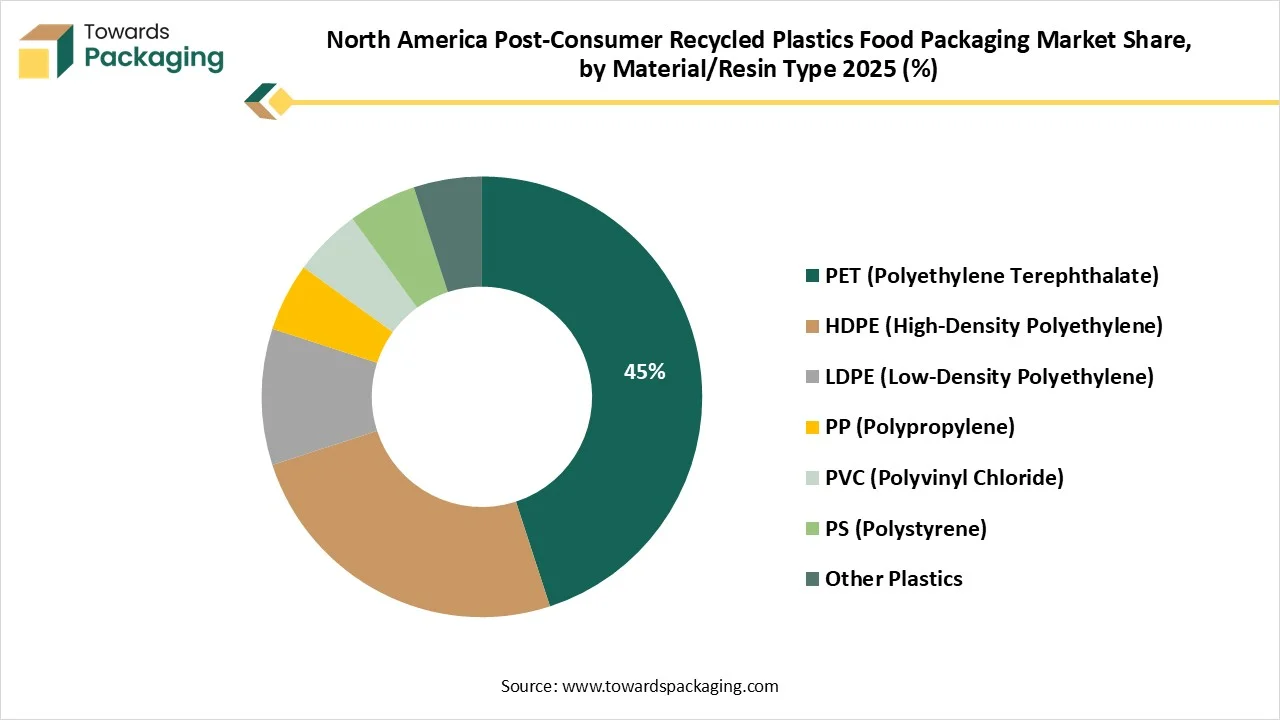

The polyethylene terphthalate (PET) segment has dominated the North America post-consumer recycled plastics food packaging market in 2025 as it not only prevents the product but also makes it attractive to the users, and PET sheets are exported in both. PET is a strong material which is visually attention grabbing. Its crucial clarity make sure visible. This is especially inside as users choose to look at what they are encouraging. PET Sheets serve protection from different environmental factors, like moisture -that vanishes the food. It makes sure that the food remains fresh for longer and tracks its texture, mixture and nutritional value.

The High-Density Polyethylene (HDPE) segment are predicted to be fastest -growing during the forecast period. The intrinsic power and durability of the HDPE are main factors that invest to its huge spread acceptance as food-safe plastic. HDPE have rigid intermolecular forces and big tensile power due to its heavily linear molecular pattern with less branching. This pattern coverts into different rigidness, for instance, an mere 60-gram HDPE container can accurately carry over a gallon of liquid or accurately eight pounds of product. This outstanding power ,which is integrated with its opposition to affect and tearing which means that HDPE containers can prevent food smoothly from external damage and contamination

The bottles and jars have segment dominated the market in 2025 as glass jar packaging are an ideal choice, which is for their clarity and clearance. They are ideal for displaying luxury products like gourmet sauces, artisanal honey and luxury skincare creams too. Glass is also 100% recyclable, which makes it a sustainable option for the eco-conscious Australian users. Also, the glass bottles serves an airtight, inert surrounding that stores the deliciousness of nay jams, protects sound and safe ,also chutney too. Storing the freshness of any product tracks the shelf life too -without adding preservatives that is also rigid branding message and enough for suers wo want to get the best use for their storage.

The pouches and bags segment are expected to be fastest growing in the market during the forecast period. The demand in pouch packaging acceptance is being drive by its surrounding advantage and smoothness. As compared to strong packaging, pouches use less space, are very lighter in weight ,and lower down the transport -linked cots. This meets with the rising under demand for the eco-friendly packaging options.

Bags became famous in food packaging due to the development of automation, materials and moves in user culture. Starting with simpler paper designs and transforming to high level plastics, bags served with hygienic, cost-effective and easy solutions for a huge-market society.

")

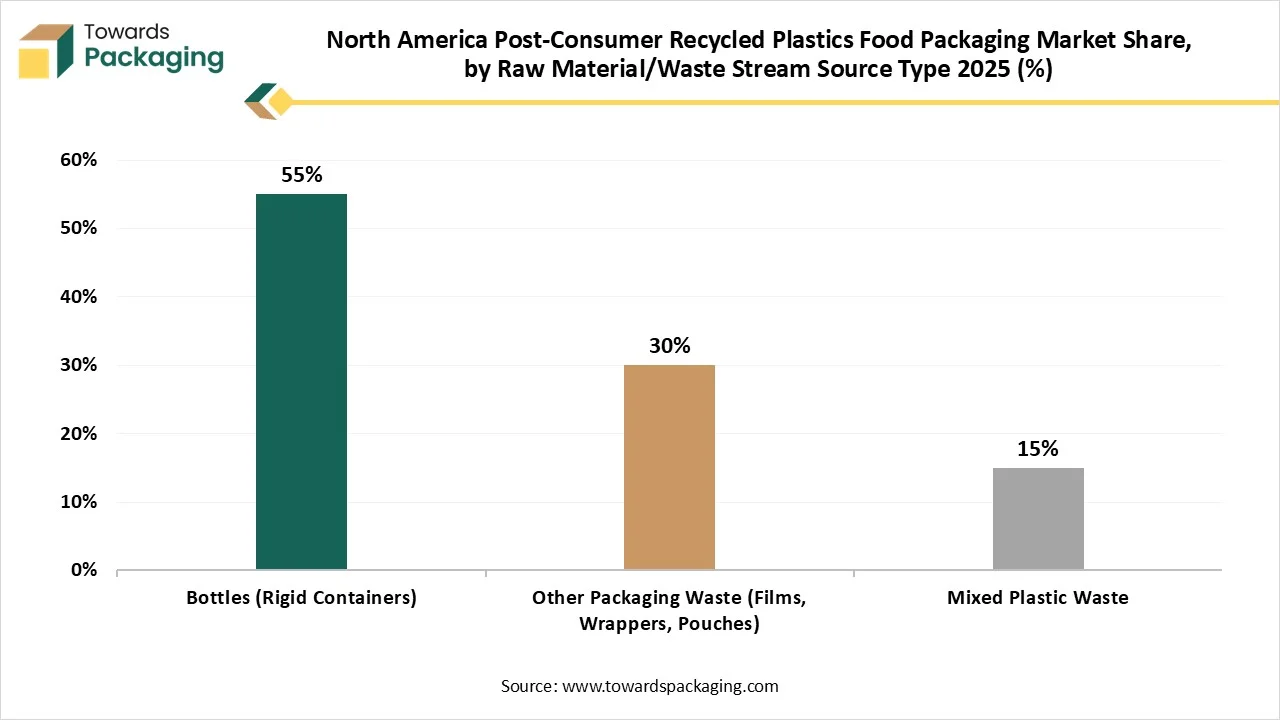

The bottles (rigid containers) segment has dominated the market in 2025 as it has materials with strong rigidity, such as metal, glass and particular plastics like HDPE and PET. There are a lot of sectors which use rigid packaging for its functionality, power and aesthetics. Rigid packaging is of advantage for the food and beverage ,particularly in tracking their freshness and quality. Prevalent packaging for soda, wine and juice count glass bottles to maintain their quality.

Plastic containers are very prevalent for butter, soft drinks and ready meals for their ease and light-weight opposition.

The other packaging waste (film, pouches and wrappers) segments are predicted to be fastest growing during the forecast period. Plastic films score high in terms of safety over conventional materials for the food packaging. The material is very less relevant to pollutant as well as pilferage. The shelf life of food become huge. The material serves the items attractive appearance and is developed for branding aim. Plastic film is very lightweight. It is convenient to print information on it. Furthermore, the films have great barrier characteristics and can be recycled as well as reused.

The food segment has dominated the market in 2025 as plastics recycling is a main element to reduce waste and receiving the aim of a plastic’s circular economy. While all thermoplastic materials are technically "recyclable", the capability to be smoothly reused and recycled into current uses goes beyond the kind of plastic it is. The capability of a material to be recycled in actual thing and at scale depend on the several counts that includes the permission to collection machine, as the industry value which is to be recycled material.

The beverage segment is expected to be fastest-growing during the foretell period. Beverage are being packed in recycled materials by processing the collected products, like as glass bottles, aluminum cans and plastics back into new containers. Additionally, by using the single-material recyclates, producers are also developing muti-layer paper-based cartons and other inventive and sustainable designs. Aluminum is one of the most greatly used and consistently recycled beverage materials in the world. They are stripped, shredded of any coatings and then being melted down in a surface.

The United States dominated the market in 2025 and is expected to sustain during the forecast period. Sustainable food packaging have a huge range of materials that are crafted to lower down the surrounding effect, which includes the compostable, biodegradable, reusable and recyclable materials options. These solutions are heavily being accepted across the catering, restaurant and food delivery industries, as businesses depend to balance convenience with eco-conscious practices.

Developing public issues about the climate update and plastic pollution continues to shape purchasing hobbies. Users are increasingly selecting products which use the packaging made from the recycled paper ,biodegradable polymers and plant-based plastics that encourages food and beverage producers to update.

The growth of online grocery shopping , food delivery services and meal kit subscriptions that need durable, inventive and temperature-controlled packaging solutions. With heightened surrounding awareness, a big space of users are willing to pay more for the sustainable options. This makes an urge for the eco-friendly like paper and paperboard to have value for its biodegradability and recyclability.

Tier 1

Tier 2

Tier 3

By Material / Resin Type

By Packaging / Product Type

By Raw Material / Waste Stream Source

By End-Use / Application

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarNorth America Post-Consumer Recycled Plastics Food Packaging Market