The traditional packaging materials market is expanding rapidly, driven by strong demand for sustainable, durable, and cost-efficient packaging across industries. In 2025, Asia Pacific led the market with over 43% share, while the paper & paperboard segment contributed 28%, and rigid packaging accounted for 55%. The market’s growth outlook from 2026-2035 is supported by rising e-commerce trade, enhanced packaging quality requirements, and AI-enabled supply chain optimization.

Our report covers full market size forecasting, regional analysis across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, competitive intelligence on 20+ global leaders including International Paper, WestRock, Smurfit Kappa, Amcor, Crown Holdings, and complete value chain and trade flow insights for raw materials, manufacturers, and suppliers.

The traditional packaging materials market refers to the market for long-established, non-synthetic, and typically non-degradable materials used for packaging across industries. These materials include paper, cardboard, glass, metals (like aluminum and steel), and conventional plastics (non-biodegradable, petroleum-based). Unlike sustainable or advanced materials, traditional packaging materials have been widely used due to their durability, versatility, and cost-effectiveness.

| Metric | Details |

| Primary Drivers | Demand for sustainable, durable, and customizable packaging |

| Leading Region | Asia Pacific |

| Market Segmentation | By Material Type, By Packaging Format, By End-use Industry, By Distribution Channel and By Region |

| Top Key Players | International Paper, WestRock, Smurfit Kappa, Mondi Group, DS Smith, Amcor, Crown Holdings, Ball Corporation, Ardagh Group. |

The incorporation of AI in the traditional packaging materials market plays an important role in revolutionizing the industry with advanced patterns and quality of the packages. It has improved operational efficacy, supply chain optimization, and sustainability of the packages. It is used for analysing the data about the replacement of materials and many other factors to enhance the scope of development. AI and machine learning remove manual mistakes in data labelling, product info, consumer details, and a lot in between. AI makes packaging resolutions with graphic and textual content that’s tailored for each purchaser.

Rising Demand for Natural Materials

The rising demand for natural materials such as lotus leaves, shells of shellfish, tree leaves, ceramics, and several other resources boosts the traditional packaging materials market. Treated skin like leather has been utilized for many nations as a non-fragile ampule or bottle. Wine and water are often transported and stored in leather ampules (pig, camel, and kid goat hides). Flour and hardened sugar are also packaged in leather pouches and cases. Traditional packaging skill not only delivers the function of defensive and transportability but also offer safety and taste in the invention. The resources such as bamboo and leaves not only make a presence in traditional packaging materials look more usual, but also mark the smell and the flavor in products.

Increasing Ecological Concerns

The increasing ecological concern has hindered the demand for the traditional packaging materials market. The growing ecological issues due to packaging materials like single-use plastics and many others have limited the expansion of the market. Continuous fluctuation in the charges of the raw materials has also restricted the development of the market.

Rising E-Commerce Industry

The growing e-commerce sector has influenced the opportunities in the traditional packaging materials market. With the growth of the e-commerce industry, there is a huge demand for enhanced packaging that can provide high-end protection while transporting. Innovation in packaging materials has raised the demand for this sector to fulfill the changing requirements of consumers. The continuous investment in research and development of this sector by the major market players has raised numerous opportunities in this market. Enhancing demand for the introduction of new technologies has supported the growth of the market expansion.

")

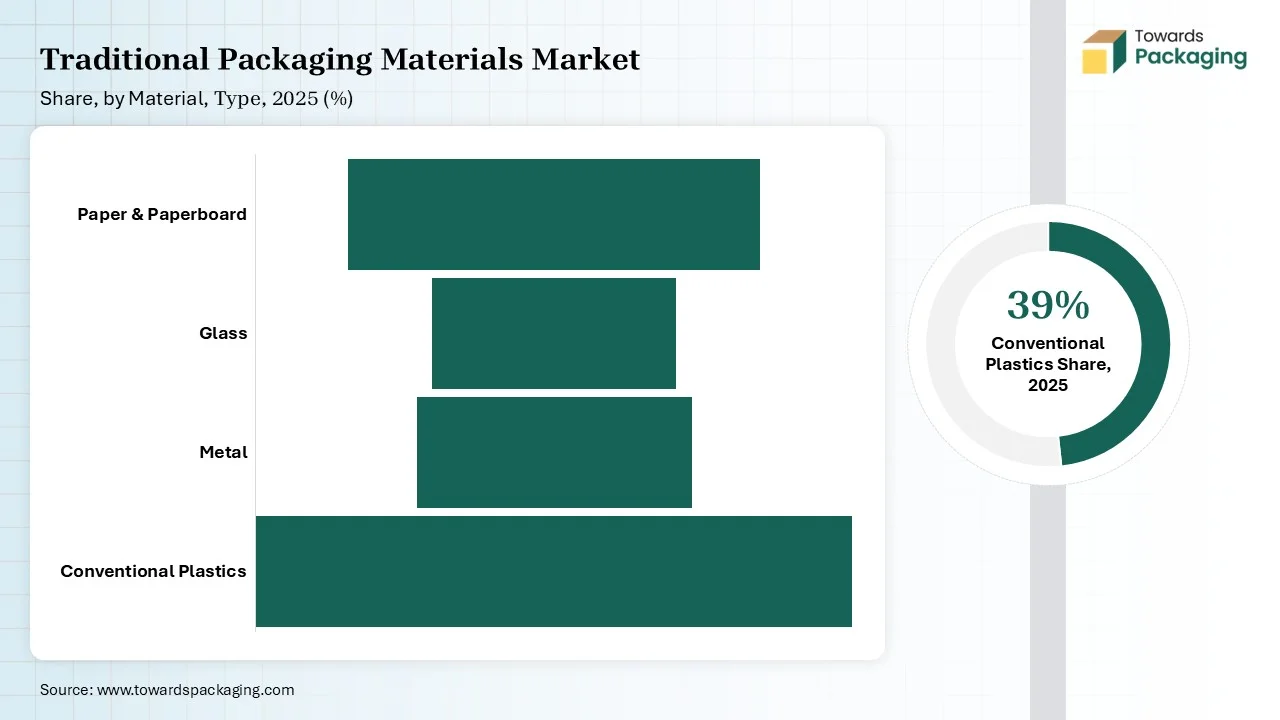

The paper & paperboard segment contributed a considerable share of the traditional packaging materials market in 2025 due to their flexibility, sustainability, and strength. These are extensively utilized for manufacturing folding cartons, corrugated boxes, and many other packages with a huge variety of shapes and sizes. The growing demand for customization of packages has majorly influenced the development of this segment. Such packages are utilized in industries like food & beverages, electronics, healthcare, and several others.

The conventional plastics segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. These are widely accepted due to their durability, versatility, and cost-effectiveness. These materials are lightweight weight which has raised the demand for such packaging as it reduces transportation charges. Transparency in this segment has raised the reliability of consumers toward this market.

The rigid packaging segment is expected to have a considerable share of the traditional packaging materials market in 2025 due to the growing demand for enhanced protection and aesthetic packaging. The rising concern for packages with high quality that look aesthetically appealing has raised the demand for this segment. There is a huge demand for packaging that can preserve the integrity of food products has helped this segment to grow exponentially. It helped brands to generate an aesthetic look and attract huge consumers towards this industry.

The flexible packaging segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. This segment is progressively developing due to enhanced product protection, lightweight and space-saving, and cost-effective packaging demand by consumers. Huge customization options in this sector have evolved the market by fulfilling consumers’ demand.

")

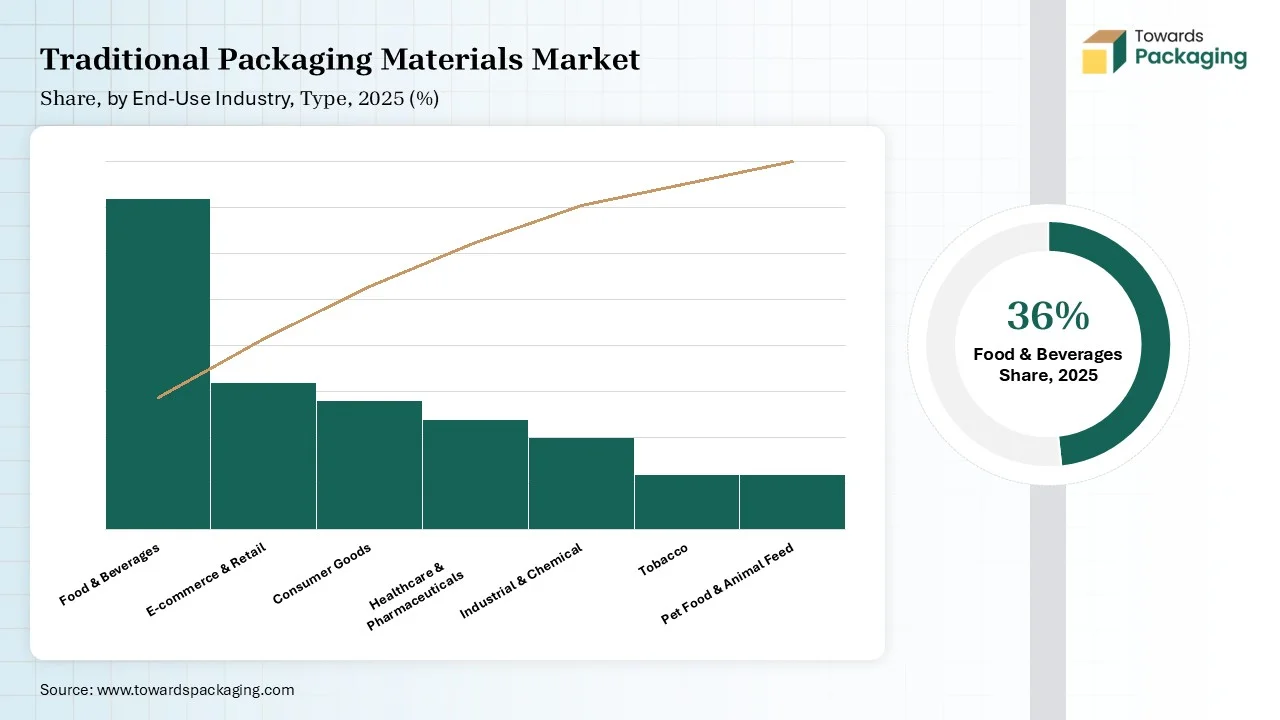

The food & beverages segment is expected to have a considerable share of the traditional packaging materials market in 2025 due to its capacity for storage and handling. There is a continuous demand for sustainable packaging options, which has raised the demand for this market in the food & beverages sector. The important service of traditional packaging materials is their capacity to acceptance to the outlines of the good. This type of packaging protects against external pollutants and upholds the sanitation and security of the food products. Traditional packaging helps to store food products for a longer period.

The e-commerce & retail segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. There is a huge demand for personalization in the packaging of products in this sector to attract a huge number of consumers. The capacity to hold a large volume of products has influenced the demand for such packaging in this industry. Innovation in traditional packaging materials has influenced the demand for this market in the e-commerce and retail segments.

The B2B segment is expected to have a considerable share of the traditional packaging materials market in 2025 due to its capacity to prevent products from spoilage and damage. This helps sellers to connect directly with manufacturing companies, which raises innovation and consumer satisfaction. This segment is useful in connecting brands with consumers directly and enhancing the demand for superior quality packaging. The requirement for bulk packaging in this segment has raised the production process of the market. This segment is concentrated on the functionality of the packaging, which has also contributed significantly to the development of the market.

The B2C segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. This segment is growing significantly to provide an enhanced experience to the consumers. Informative and convenient packaging are the major factors behind the growth of the market. Businesses are looking for a sustainable substitute that enhances the demand for the packaging type.

")

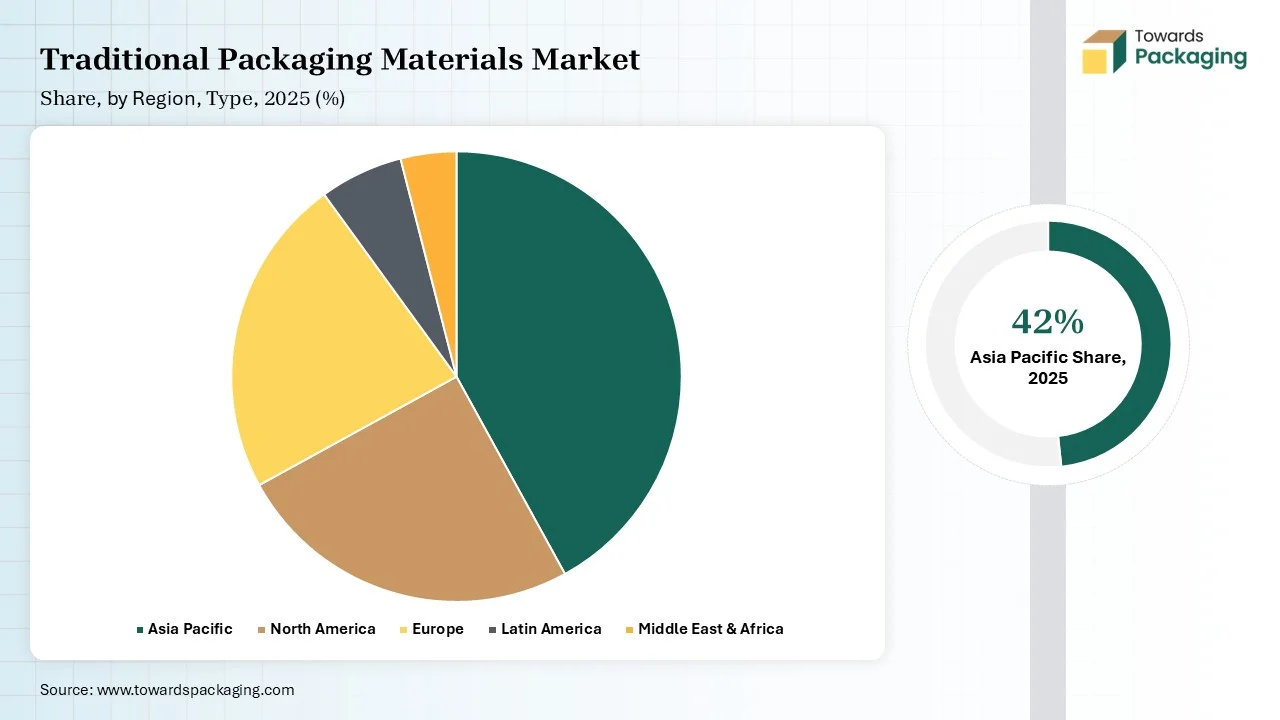

The Asia Pacific region held the largest share of the traditional packaging materials market in 2025, due to the rising demand for packaged food, consumer convenience, and hygiene packaging. The changing lifestyle of people in countries like India, Japan, China, South Korea, Thailand, and many other countries has influenced the demand for this type of packaging in the food & beverages sector. Presence of major market players such as Shanghai Yifu Packaging, Jiangsu Hongda Packaging Materials Co., Ltd, Anhui ZJ Plastic Industry Co., Ltd, and many others is investing profoundly in research and development activities. Such investment led to innovation in this market and raised the demand of the consumers.

The North America region is estimated to grow at the fastest rate in the traditional packaging materials market during the forecast period. The rising agricultural packaging demand has influenced the growth of the market. The rising demand for storage of fruits and vegetables has influence the demand for production of high-quality packages. The growing inclination towards durable and sustainable packaging has influenced the demand for this market.

By Material Type

By Packaging Format

By End-use Industry

By Distribution Channel

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarTraditional Packaging Materials Market