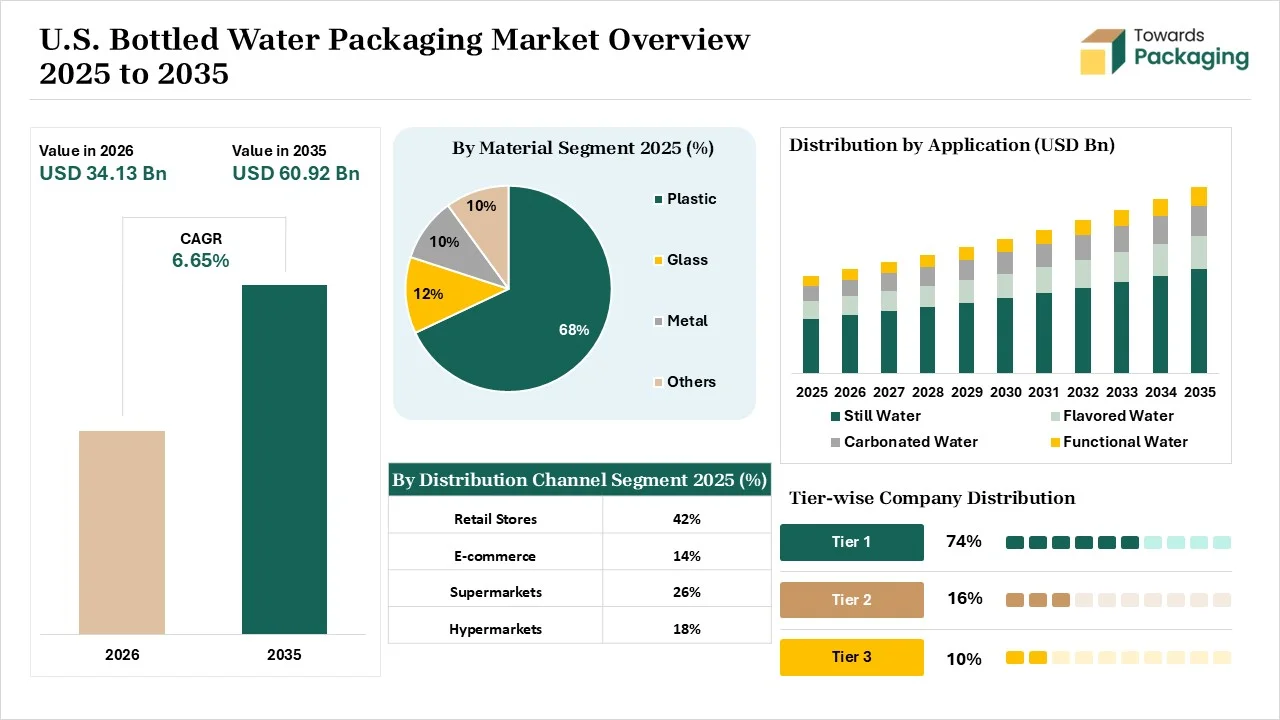

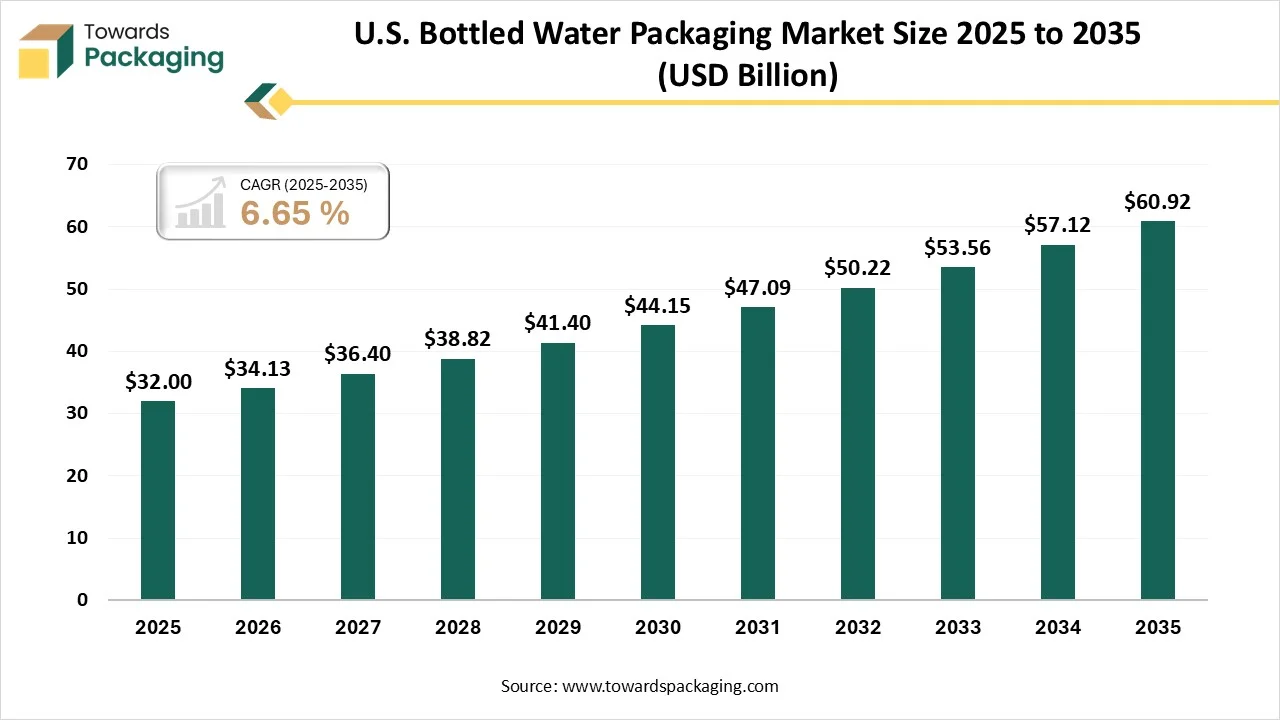

The U.S. bottled water packaging market is projected to grow from USD 34.13 billion in 2026 to USD 60.92 billion by 2035, expanding at a CAGR of 6.65% during 2026-2035. The report provides detailed insights on market size, growth trends, and rising demand driven by increasing consumption of electrolyte-infused, alkaline, and premium bottled water. It includes comprehensive segment data by material, packaging type, and end-use, along with company profiles of leading manufacturers and suppliers, competitive landscape analysis, value chain assessment, and trade flow statistics to help stakeholders understand industry dynamics and future opportunities.

U.S. bottled water packaging consists of plastic, metal, and glass and is designed for a low environmental footprint through 100% recyclability and lightweight, energy-efficient production, according to the International Bottled Water Association (IBWA). The industry heavily utilizes PET for single-serve bottles, which have seen a 51% weight reduction since 2000, alongside reusable polycarbonate for larger containers and highly recyclable HDPE for jugs. The market growth is driven by lightweight and cost-effective PET plastic, which offers excellent portability for applications ranging from single-serve to bulk, alongside growing segments in aluminum and sustainable, eco-friendly materials. The market is rapidly expanding, supported by factors like high-demand for functional water, increased adoption of recycled content (rPET), and strong e-commerce growth.

Technological transformation in the U.S. bottled water packaging market plays a significant role by driving efficiency, enhancing quality control, and promoting sustainability. Advanced computer vision systems are utilized for real-time, high-speed inspection of bottles and caps, reducing defect rates, ensuring safety, and minimizing material waste. AI algorithms also optimize production, using predictive maintenance to prevent machinery downtime and streamlining supply chains through precise, data-driven demand forecasting. AI supports eco-friendly initiatives by optimizing bottle design to reduce plastic usage and aiding in the development of sustainable materials to meet consumer demand for environmentally responsible packaging.

AI is rapidly transforming the market by improving manufacturing efficiency, water quality monitoring, supply chain management, consumer engagement, and sustainability efforts. Bottled water companies are using AI-powered sensors and machine learning systems to monitor filling lines, bottling equipment, filtration systems, and packaging machinery in real time. Advanced AI systems can analyze water purity, mineral content, contamination risks, and filtration performance. AI-driven analytics can optimize purification processes, helping companies reduce water waste and energy consumption during production. Machine learning models analyze weather trends, seasonal consumption behavior, retail sales data, and regional demand fluctuations to optimize inventory and distribution planning. Companies are using AI-powered design software to develop lightweight bottles, reduce plastic usage, and improve recyclable packaging structures.

This initial stage involves the procurement of raw materials, primarily Polyethylene Terephthalate (PET) resin, Aluminum for cans, and high-density polyethylene (HDPE) for caps.

This stage involves transforming raw materials into preforms or final bottles, labels, and closures, often utilizing blow molding technology.

The packaged products are moved from bottling plants to distribution centers and finally to retail, on-trade (restaurants), or direct-to-consumer channels.

The plastic segment dominated the U.S. bottled water packaging market with the highest share in 2025 due to its unmatched manufacturing scale and cost-efficient, lightweight nature, which significantly lowers logistical overhead. Its functional durability and high-speed production compatibility allow it to dominate single-serve, on-the-go consumption across diverse retail channels. While sustainability concerns persist, the rapid shift toward rPET and BPA-free alternatives is repositioning plastic as a core component of a circular economy. The balance of operational high-performance and evolving environmental accountability.

The metal segment is expected to grow at the fastest CAGR during the forecast period of 2026 to 2035. This segment is growing due to the application of aluminum and metal packaging, which is surging as brands leverage its premium positioning and superior barrier protection against light and oxygen to ensure product purity. With the stringent plastic regulations and mandatory recycled-content laws, the market is shifting toward these infinitely recyclable materials to meet aggressive corporate ESG goals. The shatterproof, insulating properties of metal make it the preferred choice for high-end outdoor and fitness applications, where durability is as critical as environmental impact.

The retail stores segment dominated the U.S. bottled water packaging market with the highest share in 2025 due to its strong distribution networks and a profound consumer shift toward health and wellness over sugary beverages. Retailers are successfully leveraging premiumization, offering functional and flavored waters, while transitioning to rPET and biodegradable packaging to align with intensifying sustainability trends. This synergy between immediate accessibility in urban centers and a diverse product variety ensures that bottled water remains the primary choice for convenient, eco-conscious hydration.

The e-commerce segment is expected to grow at the fastest CAGR during the forecast period of 2026 to 2035. This segment is growing due to rapid evolution in logistics and subscription models, which have turned bulky, heavy water delivery into a seamless, front-door convenience. As consumers increasingly prioritize health over sugary alternatives, online platforms provide the ideal landscape for price comparison and frictionless bulk purchasing. The integration of next-day shipping and eco-conscious "Ships in Own Container" (SIOC) packaging is further bridging the gap between traditional retail and digital accessibility.

The still water segment dominated the U.S. bottled water packaging market with the highest share in 2025 due to permanent consumer migration toward zero-calorie, natural hydration over sugary soft drinks. The portable PET formats that cater to on-the-go lifestyles, alongside a critical reliance on bottled water as a safe, trusted alternative to municipal tap water. The premiumization, where high-end spring and glacial waters utilize rPET and plant-based materials to capture the eco-conscious luxury demographic.

The functional water segment is expected to grow at the fastest CAGR during the forecast period of 2026 to 2035. This segment is growing due to an aggressive consumer shift toward performance-enhancing hydration containing electrolytes, vitamins, and antioxidants. This shift from sugary sodas is being met with premium, niche offerings like alkaline and protein waters, specifically designed for high-intensity, active lifestyles. Brands are securing loyalty through innovative, resealable packaging and eco-friendly materials that resonate with the on-the-go, health-conscious demographic.

Material

Distribution Channel

Application

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarU.S. Bottled Water Packaging Market