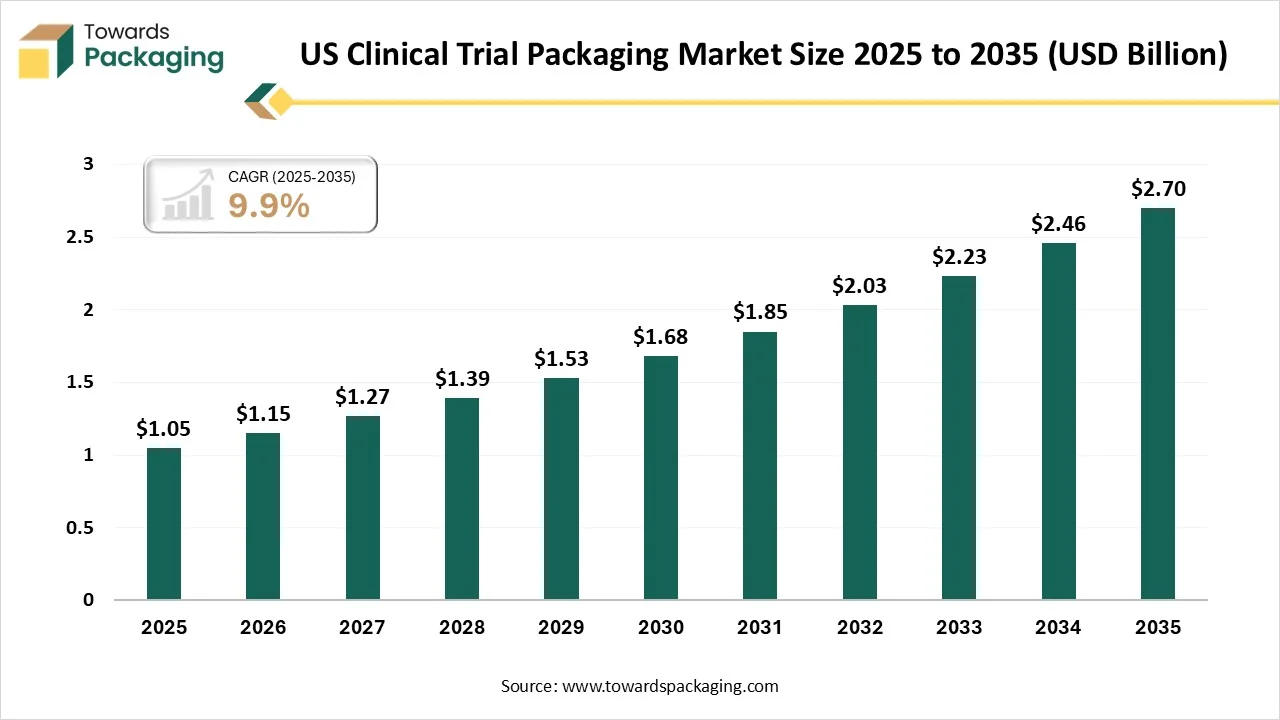

The U.S. clinical trial packaging market is forecasted to expand from USD 1.15 billion in 2026 to USD 2.7 billion by 2035, growing at a CAGR of 9.9% from 2026 to 2035. There is a developing commonness of chronic diseases like cancer, diabetes, and cardiovascular disorders, along with new infectious diseases like COVID-19, which has grown the urge for clinical trials whose goal is to develop the latest vaccines and treatments.

The U.S. clinical trial packaging market is a critical subset of the pharmaceutical supply chain, ensuring that investigational medicinal products (IMPs) reach clinical sites and patients with their chemical integrity, stability, and blinding protocols intact. In 2026, the market is characterized by a surge in demand for temperature-sensitive biologics packaging and the rise of decentralized clinical trials (DCTs), which require specialized direct-to-patient delivery solutions.

The trends in this industry are accompanied by a smart packaging craze and increased adoption of eco-conscious, sustainable materials to modernise the healthcare sector. The unification of QR codes, NFC tags, and RFID promotes the safety check and seriousness towards patients’ good health. The continuous monitoring of the humidity level keeps the drugs and other suitable items safe. Whereas the home-based trials are highly popular and are accelerating the demand ratio for direct-to-patient (DtP) packaging.

Regarding this demand, the seamless designs for quick unboxing and powerful cold chain solutions in the U.S. are skyrocketing. Just-in-Time (JIT) manufacturing is another sustainable trend that cuts waste volume. These kinds of smart, sustainable ideas have attracted more companies to prepare packaging and JIT labelling models. These trends are an encouragement to the sponsors to invest in different methods and ideas that push the industry in an upward direction for more development in the field.

The modernised serialisation process is smartly equipped to cooperate best with the U.S. Drug Supply Chain Security Act (DSCSA). This is a regulatory underlined growth factor, which is a boon and a validation to the U.S. clinical trial packaging line.

The AI dedication in this industry introduces intelligent operations which brings smooth supply chain to the limelight and improve patient safety. The AI-powered vision systems have upgraded the inspection level with their non-contact packaging methods, detection potential and real-time checks. The AI systems are capable enough to create dosage instructions according to each patient's health condition or concern.

Alongside the AI-based platforms creates evident packages and digital eCOA. AI also helps to maintain a strong critical logistics base for clinical trial supplies; additionally, the tracking feature promotes the use of AI-improved systems and IoT sensors.

Key Players - Sharp Services, LLC, Almac Group and PCI Pharma Services.

Key Players - Daniels Health, Stericycle (Waste Management) and Triumvirate Environmental

Key Players - Marken (a UPS Company), Catalent, Inc., and Parexel International.

Clinical packaging inventions have shifted far beyond simple translation of labels into multiple languages. Current multi-language labelling displays a standard mixing of linguistic, professional, human, engineering, and regulatory knowledge, too. Advanced systems currently have semantic tracking to make sure that converted content completely maintains not just literal precision but a regulatory and contextual meaning across cultures and languages. Multilingual clinical labelling systems should be responsible for overall regulatory needs that change mainly across jurisdictions.

Plastics segment dominated the market, changing the packaging with their reliability. High-Density Polyethylene (HDPE), Polyethene Terephthalate (PET), and Polyvinyl Chloride (PVC) are widely used. It has an unbreakable and lightweight nature and the potential to be turned into different shapes, which makes it perfect for a series of products. Such products include blister packs, bottles, and dropper bottles. Developments in terms of plastic technology also include biodegradable plastics that align with surrounding sustainability goals.

The metal (aluminium/foil) segment is expected to witness the fastest CAGR during the forecast period. Aluminium is well known for its perfect barrier characteristics, as aluminum is initially used in blister packaging. It also prevents fragile products from oxygen, moisture, and light, hence it stretches their overall shelf life too. Aluminium foils are frequently used in integration with plastic and paper to make a multi-layered package which is both user-friendly and durable too.

The vials and ampoules segment dominated the U.S. clinical trial packaging market in 2025 as pharmaceutical vials are small containers that are used initially for storing the medications in liquid form, though they are also used for capsules and powders. Such vials make sure that medications are protected from external elements like moisture, air, and light that can lower the quality. Vials should be strong, which tracks the sterility and the quality of the ingredients until they are administered. The correct vial not only protects the quality of its contents but also ensures the safety of the patients who will suddenly use such medications.

The syringes (Prefilled) segment is predicted to experience the fastest CAGR during the forecast period. Prefillable syringes ensure accurate safety for both healthcare workers and patients. As the medicine is packed and ready to use, it lessens the chances of accidental needle injuries or contact with overall toxic drugs, but risks occur while moving from vials. The fixed dose is a prefilled syringe that also assists in protecting against measurement error, which improves diagnosis precision. They are even convenient to use as they are available with the exact dose already inside, which is ready for injection. PFS injection means it saves time, particularly in emergencies or in busy clinics.

Phase III trials segment dominated the market in 2025 as they are the final and most complicated stage before a drug or biologic reaches the market. It checks if a treatment is viable at scale or not, and also just under specific conditions, but in huge and real-world populations. In this scenario, investigational products should display statistically significant and clinically meaningful results. Trials often recruit 1,000 participants, with designs that are being constructed for racial, geographic, and age diversity in order to show the future that describes the population.

The phase II segment is expected to witness the fastest CAGR during the forecast period. It includes a bigger group of participants (100-300), which is generally fewer than a hundred patients who have the condition that the drug is being designed to treat. The aim here is to check the drug’s effectiveness while staying constant to check its safety. Phase 2 has frequently compared the latest drug to an inactive drug or a standard, checking and assisting in changing dosing regimens.

The clinical research organization (CROs) segment dominated the market in 2025 as they are a company that serves clinical trial management for the biotech, pharmaceutical, and medical device sectors. There are various types of CRO’s and different levels of specialization ( which differ from therapeutic spaces). CRO services include site selection, regulatory affairs, pharmacovigilance, medical writing, and project management, too. In a clinical trial, CROs are being rented by sponsors to complete a set of tasks that take on different administrative and technical responsibilities on the sponsor’s behalf.

The drug manufacturing facilities segment is expected to experience the fastest CAGR during the forecast period. Clinical trial packaging points are a crucial element in the pharmaceutical sector that fills the gap between drug development and market readiness. The growth of technologies such as smart solutions and cold seal packaging underlines the sector’s loyalty to efficiency, invention, and patient safety. The future of a pharmaceutical achievement depends not just on a drug discovery, but also on the capability to smoothly package and serve such inventions in a way that aligns with strong standards and solves the complicated demands of clinical trials.

The U.S. Clinical Trial Packaging market is seen to grow notably in California, as this state is home to a large number of clinical research organizations and a diverse population, which makes it a clinical region for patent recruitment and the same clinical supply demands. To align with the growing localized urge, servers are stretching the facilities within the state. Latest FDA regulations related to child-resistant packaging and serialization, and lastly, the Drug Supply Chain Security Act (DSCSA), are driving the California producer to accept more high-level and protected packaging technologies. Furthermore, a move towards “decentralized” trials is growing the urge for packaging that is convenient for patients to utilize at home and can be delivered quickly from a local centre.

Trend of Clinical Trial Packaging in Texas: In this state, there is a developing need for direct-to-patient packaging solutions. These count patient-friendly and tamper-evident kits that are being crafted for home delivery, which assist Texas’s big and geographically diverse participant population. The growth of cell therapies, biologics, and gene therapies in the Texas research environment has developed the urge for temperature-controlled packaging, which can track the stability across different climate zones.

By Material

By Product Type

By Clinical Trial Phase

By End-User

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarU.S. Clinical Trial Packaging Market