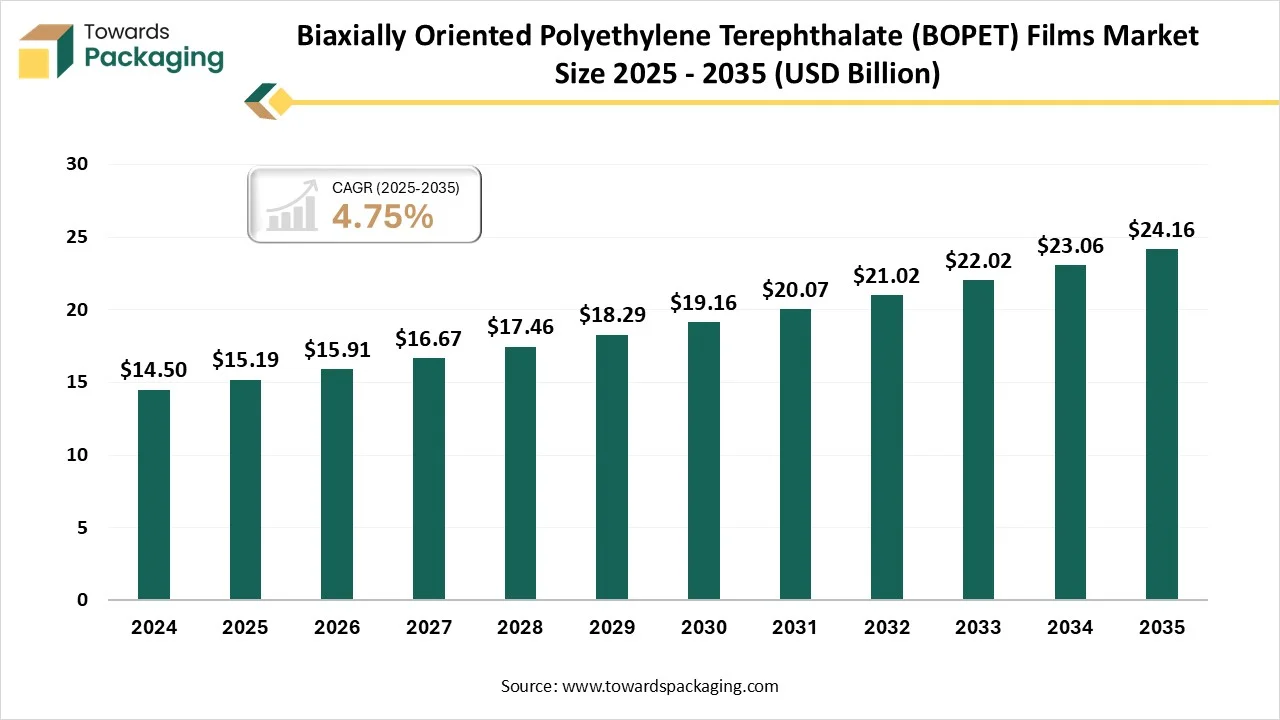

The biaxially oriented polyethylene terephthalate (BOPET) films market is projected to grow from USD 15.19 billion in 2025 to USD 24.16 billion by 2035, with a CAGR of 4.75%. This market is driven by rising demand in packaging, electrical, and industrial applications. North America leads with a strong packaging industry, while Asia-Pacific is the fastest-growing region. The key segments include metallized BOPET films, coated BOPET films, and thin to medium gauge films. Major players include DuPont Teijin Films, Toray Industries, and UFlex.

Films Market Size 2025 - 2035")

The biaxially oriented polyethylene terephthalate (BOPET) films market is witnessing steady growth driven by rising demand from packaging, electrical, and industrial applications. North America dominated the market due to its strong manufacturing base, advanced film processing technologies, and increasing use of flexible and sustainable packaging materials. The region’s well-developed food and beverage sector, coupled with growing adoption in electronics, solar, and automotive industries, further supports market expansion. Continuous R&D investments and recyclability initiatives enhance product innovation and regional competitiveness.

The biaxially oriented polyethylene terephthalate (BOPET) films market is driven by growing demand for durable, high-barrier, and recyclable materials in packaging, electrical, and industrial applications. BOPET films are polyester films produced by stretching polyethylene terephthalate in both the machine and transverse directions, which enhances their strength, clarity, and dimensional stability.

This biaxial orientation gives the films superior mechanical, thermal, and chemical resistance compared to standard plastic films. They are widely used in food packaging, labels, electronics, insulation, and solar applications due to their excellent barrier properties, glossy appearance, and ability to maintain performance under varying environmental conditions.

")

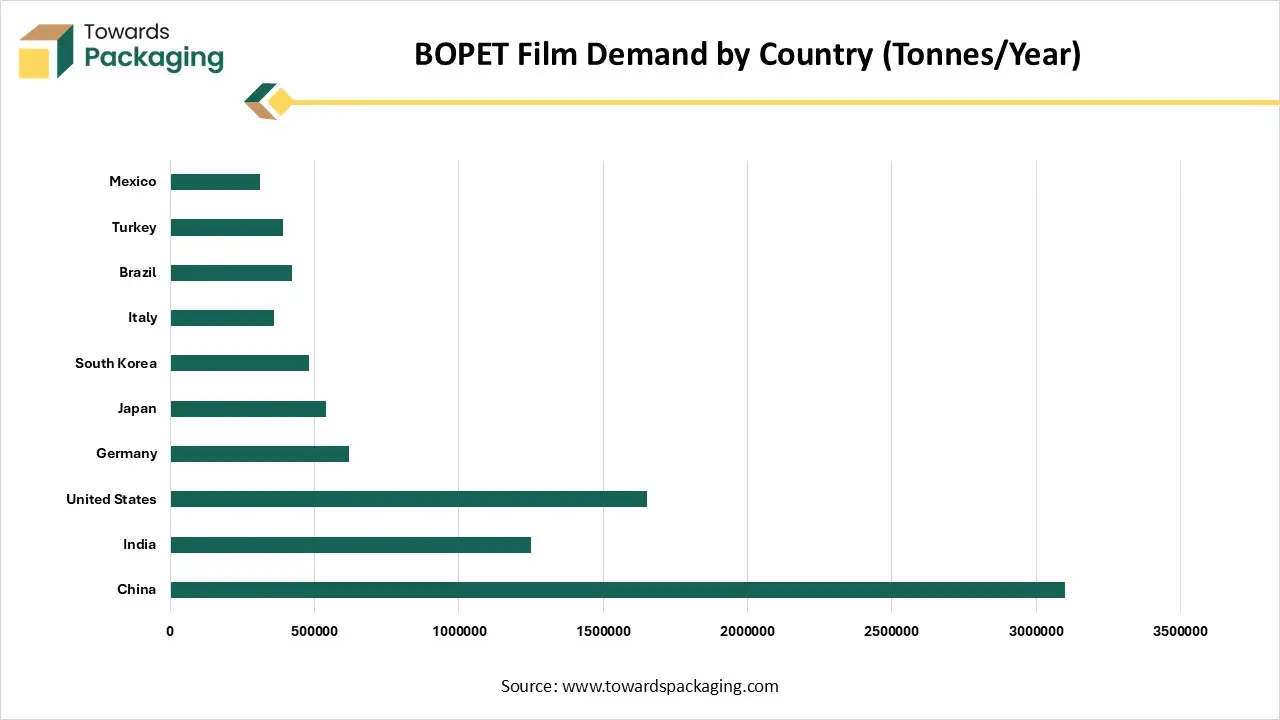

| Country | Demand |

| China | 3100000 |

| India | 1250000 |

| United States | 1650000 |

| Germany | 620000 |

| Japan | 540000 |

| South Korea | 480000 |

| Italy | 360000 |

| Brazil | 420000 |

| Turkey | 390000 |

| Mexico | 310000 |

| Metric | Details |

| Market Size in 2025 | USD 15.19 Billion |

| Projected Market Size in 2035 | USD 24.16 Billion |

| CAGR (2026 - 2035) | 4.75% |

| Leading Region | North America |

| Market Segmentation | By Film Type / Product Type, By Application, By End-User, By Thickness / Grade, By Revenue Model and By Region |

| Top Key Players | DuPont Teijin Films, Toray Industries, Inc., Mitsubishi Polyester Film, Inc., Garware Hi-Tech Films Ltd., Terphane, Foshan Jingxin Plastic Co., Ltd., Zhejiang CIFU Group |

")

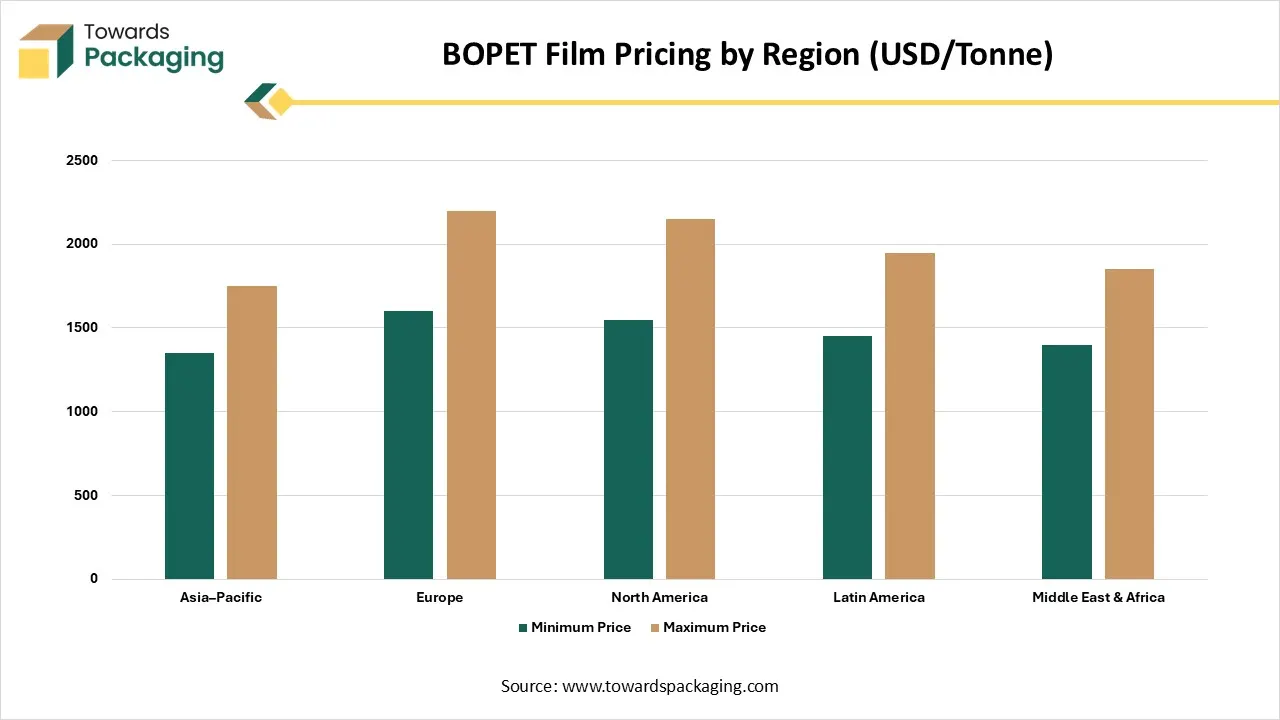

| Region | Minimum Price | Maximum Price |

| Asia Pacific | 1350 | 1750 |

| Europe | 1600 | 2200 |

| North America | 1550 | 2150 |

| Latin America | 1450 | 1950 |

| Middle East & Africa | 1400 | 1850 |

AI integration can significantly enhance the biaxially oriented polyethylene terephthalate (BOPET) films industry by optimizing production processes, improving quality control, and reducing material waste. Predictive analytics enable manufacturers to anticipate demand, streamline supply chains, and adjust production in real-time. AI-driven research accelerates development of high-performance, sustainable films with better barrier, thermal, and mechanical properties.

Additionally, AI supports market insights, identifying emerging trends, regional demands, and customer preferences, allowing companies to innovate strategically, expand applications, and strengthen competitiveness across packaging, electronics, and industrial sectors.

| Region | Key Developments |

| North America |

- Polyplex commissioned a new 50,000-ton BOPET film production line in Decatur, Alabama, increasing resin capacity to 86,000 tons, enhancing supply reliability and reducing lead times. UFlex Limited invested USD 200 million in Egypt to enhance backward integration and market reach, allocating USD 70 million for a PET chips facility, a key raw material for BOPET films. |

| Asia-Pacific | - China and India are witnessing significant growth in BOPET film production, driven by increasing demand in packaging and electronics sectors. |

| Europe | - Germany and Italy are focusing on sustainable BOPET film production, with advancements in recycling technologies and eco-friendly manufacturing processes. |

| Latin America | - Brazil is investing in BOPET film production facilities to cater to the growing demand in the packaging industry, focusing on both domestic supply and export opportunities. |

| Category | Advancement | Key Benefits |

| Material Innovation | Development of BOPE-HD and MDO-HDPE resins by NOVA Chemicals. | Enables fully recyclable, all-PE laminates with high stiffness, excellent heat resistance, and outstanding optical properties. |

| Process Enhancement | Introduction of advanced biaxial stretching technology for BOPE films. | Results in films with superior mechanical strength, transparency, gloss, low fish-eye counts, contamination-resistant sealing, puncture resistance, low-temperature impact performance, printability, and sustained wetting tension. |

| Sustainability Focus | Emphasis on reducing material usage and enhancing recyclability. | Achieves up to 50% reduction in packaging substrate thickness, conserving resources, lowering costs, and aligning with global sustainability goals. |

| Application Expansion | Adoption of BOPE films in niche markets such as frozen food packaging. | Addresses limitations of traditional PE films in low-temperature applications, reducing bag breakage rates from 7%-8% to nearly 0%. |

| Technological Integration | Integration of automated gauge control, infrared heating, and low-friction rollers in manufacturing lines. | Increases line efficiency and reduces downtime, enabling the production of multi-layer films with specific functions. |

| Monomaterial Solutions | Development of all-PE film structures using HD-BOPE technology. | Facilitates the creation of recyclable multi-layer films that perform as well as traditional mixed-material structures, supporting the transition to a circular economy. |

| Trial and Testing | Conducting extensive trials of PureFive™ resin in BOPP film production. | Demonstrates the feasibility of using new resins in BOPP film manufacturing, paving the way for innovative materials and processes. |

Metallized biaxially oriented polyethylene terephthalate (BOPET) films dominate the market due to their excellent barrier properties, high tensile strength, and superior gloss and printability. These films effectively protect against moisture, oxygen, and light, making them ideal for food, beverage, and pharmaceutical packaging. Additionally, their lightweight nature and recyclability enhance sustainability, while their aesthetic appeal supports premium product presentation.

Coated Biaxially Oriented Polyethylene Terephthalate (BOPET) films are specialized films treated with surface coatings to enhance specific properties such as adhesion, printability, heat resistance, and barrier performance. These coatings allow the films to be used in high-performance applications including flexible packaging, labeling, electronics, and industrial uses. They offer improved durability, chemical resistance, and compatibility with inks, adhesives, and laminates, making them versatile for various industries.

The packaging segment dominates the biaxially oriented polyethylene terephthalate (BOPET) films market due to its superior barrier properties, high tensile strength, and versatility across food, beverage, and pharmaceutical applications. Its ability to ensure product safety, extend shelf life, and support attractive printing makes it essential. Rising e-commerce and consumer demand for sustainable, durable packaging further drive growth.

The Electrical and Electronics segment is the fastest-growing application in the BOPET films market due to the films’ excellent dielectric strength, thermal stability, and dimensional accuracy. These properties make them ideal for insulating capacitors, transformers, and flexible printed circuits. Rapid advancements in consumer electronics, increasing demand for lightweight and high-performance components, and the growth of electric vehicles are driving adoption, positioning this segment for accelerated growth in the global market.

The packaging industry is the dominant end-user segment in the biaxially oriented polyethylene terephthalate (BOPET) films market due to the films’ exceptional barrier properties, durability, and versatility. They effectively protect products from moisture, oxygen, and light while enhancing shelf life. Additionally, their excellent printability and transparency support attractive branding and labeling. Growing demand for convenient, sustainable, and high-performance packaging in food, beverage, and pharmaceutical sectors further reinforces this segment’s dominance.

The Electrical and Electronics industry is the fastest-growing segment in the biaxially oriented polyethylene terephthalate (BOPET) films market due to the films’ excellent electrical insulation, thermal stability, and dimensional precision. These properties make them ideal for capacitors, transformers, flexible printed circuits, and other electronic components. Rapid growth in consumer electronics, increasing adoption of electric vehicles, and the demand for lightweight, high-performance materials are driving the accelerated expansion of this segment globally.

The medium gauge segment dominates the BOPET films market due to its optimal balance of strength, flexibility, and processability, making it suitable for a wide range of applications. It offers excellent barrier properties, durability, and dimensional stability while remaining cost-effective. Its versatility supports packaging, electrical, and industrial uses, meeting both performance and economic requirements. This adaptability across multiple end-use industries reinforces the medium gauge segment as the preferred choice in the market.

The Thin Gauge segment in the BOPET films market is gaining attention due to its lightweight, flexible, and cost-effective characteristics. Thin gauge films offer excellent clarity, printability, and barrier properties while reducing material usage, making them ideal for food and beverage packaging, labels, and flexible laminates. Their adaptability for high-speed processing and compatibility with advanced coatings and printing technologies further drives their growing adoption across multiple industries.

The direct product sales segment dominates the BOPET films market due to its ability to provide manufacturers with stronger customer relationships, customized solutions, and reliable supply chains. Direct sales enable better communication regarding product specifications, quality requirements, and delivery schedules, ensuring high customer satisfaction. Additionally, this approach reduces dependency on intermediaries, allows competitive pricing, and strengthens brand loyalty, making it the preferred distribution strategy for high-performance and specialized BOPET films.

The customized solutions and services segment is the fastest-growing in the BOPET films market due to increasing demand for tailored films that meet specific barrier, thickness, coating, and printing requirements across industries like packaging, electronics, and automotive. Manufacturers are offering specialized coatings, metallization, and surface treatments to enhance functionality and performance. Rising consumer preference for premium, high-quality, and application-specific products drives the adoption of these customized solutions, accelerating growth in this market segment.

Films Market Size 2025 - 2035")

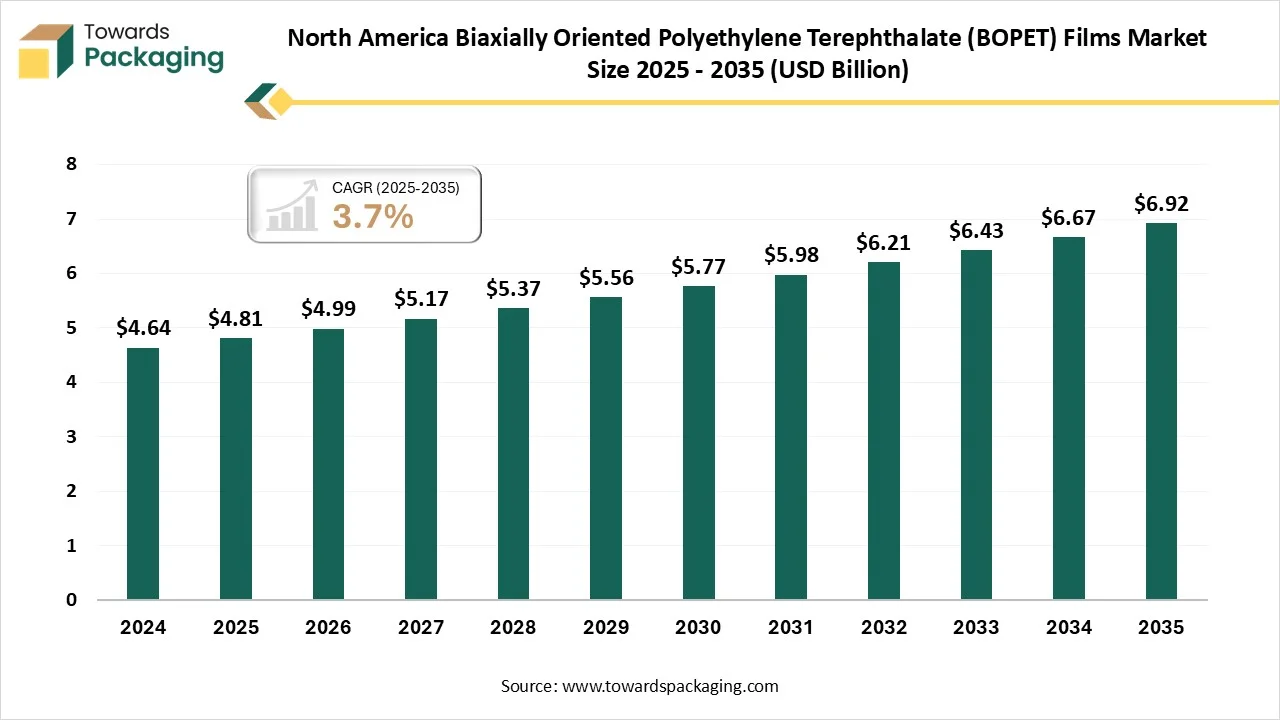

North America dominates the BOPET films market due to its well-established packaging, electrical, and electronics industries, which demand high-performance films with excellent barrier, tensile, and thermal properties. Strong consumer preference for convenient, sustainable, and visually appealing packaging drives adoption. Advanced manufacturing infrastructure, rapid technological innovations, and stringent quality standards further support market leadership. Additionally, growing e-commerce, food, and pharmaceutical sectors in the region contribute to robust demand, reinforcing North America’s position as the dominant market for BOPET films. The United States and Canada are pivotal players in the North American Biaxially Oriented Polyethylene Terephthalate (BOPET) films market, driven by significant investments from leading manufacturers and a robust demand across packaging, electronics, and pharmaceutical sectors.

The U.S. is a major hub for BOPET film production, hosting several key manufacturers:

Canada's BOPET films market is expanding, with notable investments from key players:

")

| Region | BOPET | BOPP | CPP |

| Asia-Pacific | 4200000 | 8900000 | 3600000 |

| Europe | 2100000 | 3600000 | 1500000 |

| North America | 1850000 | 3100000 | 1300000 |

| Latin America | 620000 | 780000 | 460000 |

| Middle East & Africa | 480000 | 720000 | 340000 |

Films Market Size 2025 - 2035")

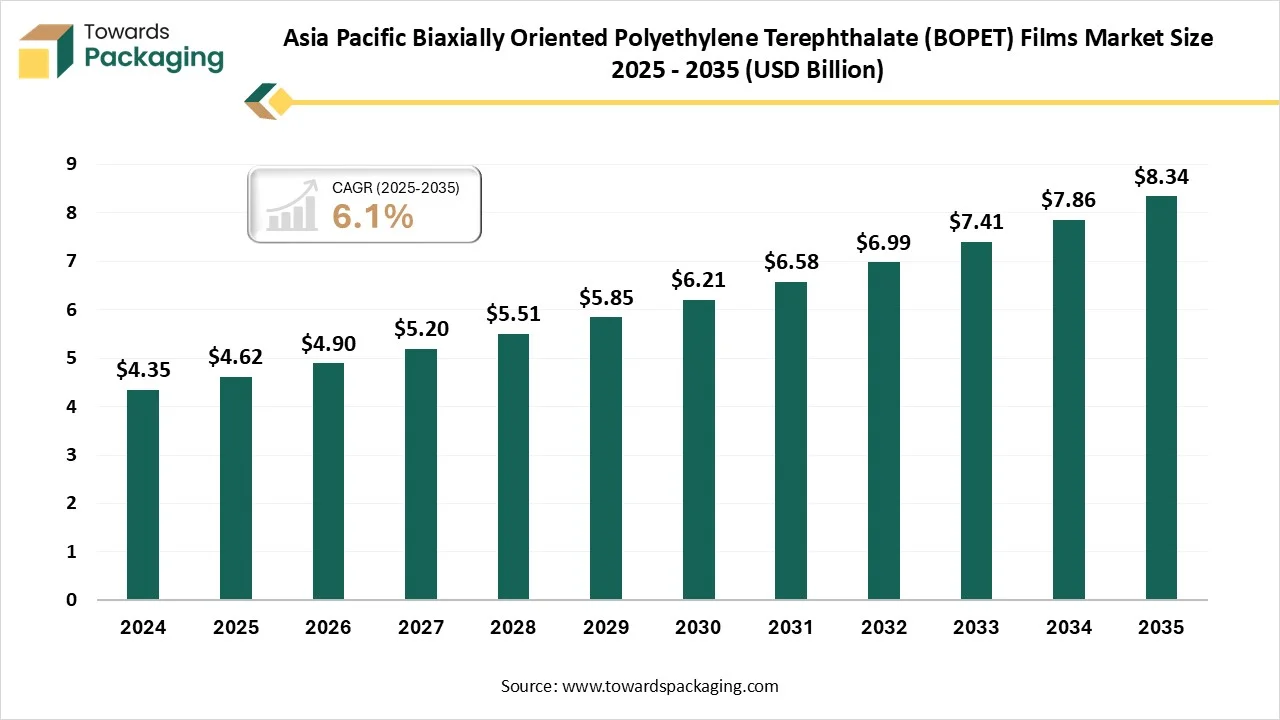

The Asia-Pacific region is the fastest-growing market for biaxially oriented polyethylene terephthalate (BOPET) films due to rapid industrialization, rising disposable incomes, and expanding packaging, electronics, and automotive sectors. Growing demand for convenient, durable, and sustainable packaging, coupled with increasing e-commerce and food and beverage consumption, drives adoption. Additionally, the presence of major manufacturers, government initiatives supporting advanced manufacturing, and investments in modern production facilities enhance regional capacity, making Asia-Pacific a hub for high-performance BOPET films and fostering accelerated market growth. China and India are pivotal players in the Asia-Pacific Biaxially Oriented Polyethylene Terephthalate (BOPET) films market, driven by robust industrial growth and significant investments from leading manufacturers.

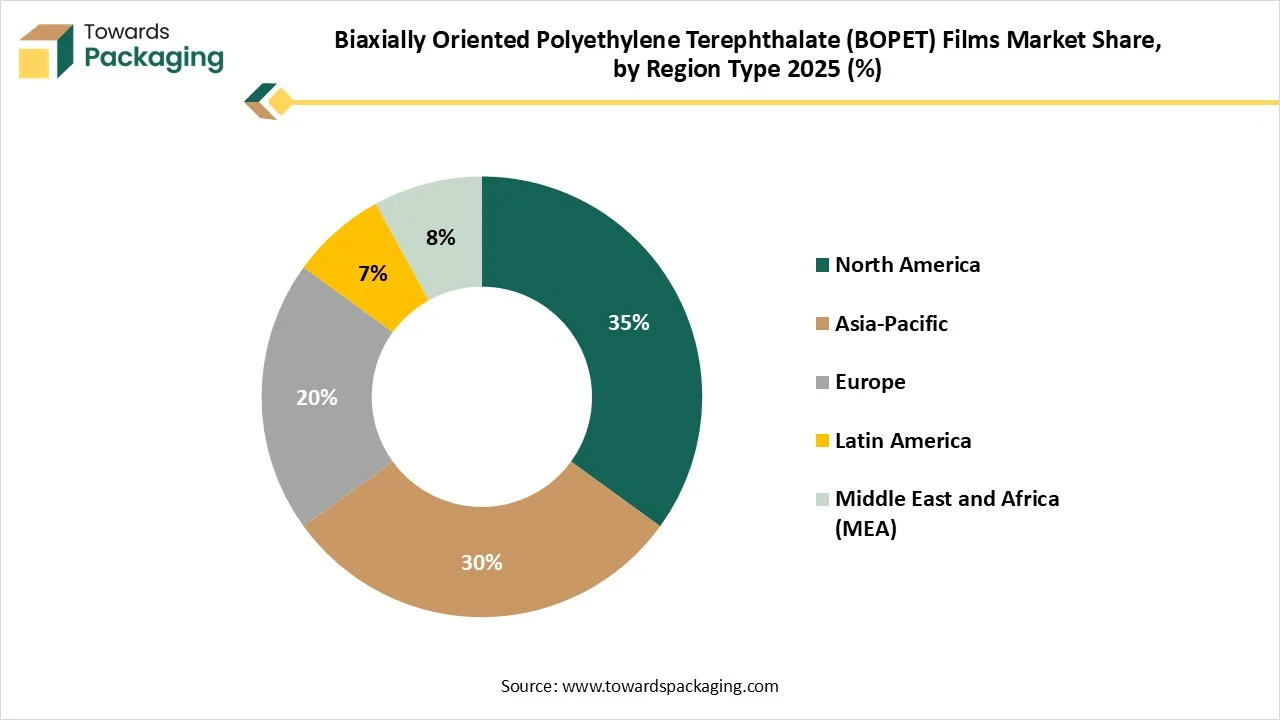

Films Market Share, by Region Type 2025 (%)")

China stands as a global leader in BOPET film production, with major manufacturers such as Hengli Group, Jiangsu Yuxing Film Technology, Fuwei Films, and Zhejiang Haibin Film Technology. These companies specialize in producing a wide range of BOPET films for applications in packaging, electronics, and industrial sectors. For instance, Jiangsu Yuxing Film Technology is noted for its medium and thick special polyester films, catering to industries like IT, LCD, and solar cell modules.

The Chinese government supports the BOPET film industry through favorable policies and investments in advanced manufacturing technologies. This support has led to the establishment of state-of-the-art production lines and testing equipment, enhancing the quality and competitiveness of Chinese BOPET films in the global market.

India's BOPET film market is characterized by significant investments from both domestic and international players. Polyplex Corporation, a leading manufacturer, has announced an investment of ₹558 crore to establish a new BOPET film plant, aiming to increase production capacity by 52,400 metric tonnes per annum. Jindal Poly Films, another major player, is investing US$ 7.89 million through its subsidiary, JPFL Films, to set up new BOPP, PET, and CPP lines in Nashik, Maharashtra. Additionally, Dhunseri Poly Films, part of the Dhunseri Group, plans to invest US$11.27 million (₹1,000 crore) to establish two polyester film manufacturing units in West Bengal.

These investments underscore India's growing prominence in the BOPET film industry, driven by increasing demand in packaging, electronics, and automotive sectors. The country's strategic initiatives, including infrastructure development and policy support, further bolster its position in the global BOPET film market.

Tier 1

Tier 2

Tier 3

By Film Type / Product Type

By Application

By End-User

By Thickness / Grade

Byf

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarBiaxially Oriented Polyethylene Terephthalate (BOPET) Films Market