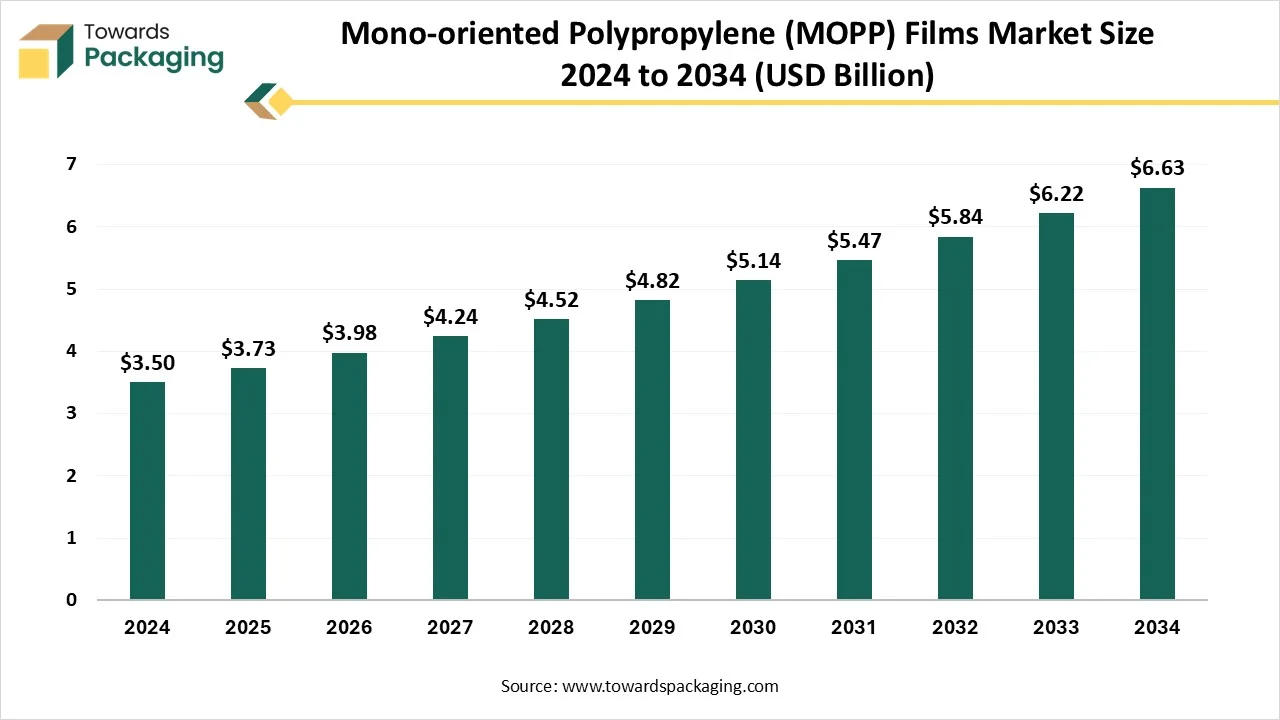

The mono-oriented polypropylene (MOPP) films market is forecasted to expand from USD 3.73 billion in 2025 to USD 7.07 billion by 2035, growing at a CAGR of 6.6% from 2026 to 2035. The rising demand for lightweight and recyclable packaging in industries such as labelling, pharmaceutical, and food & beverages.

The major development comprises mono-material packaging, enhanced mechanical properties, and sustainability of the packaging. Major drivers of this industry are increasing consumers’ awareness, sustainability goals, technological advancements, and growing food & beverages sector. The market is dominating in Asia Pacific region due to presence of large-scale production.

Films Market Size 2024 - 2034")

Mono-oriented polypropylene (MOPP) films are the plastic films which are made up of polypropylene which is stretched highly and oriented in one direction while manufacturing. These films provide tear resistance and high tensile strength, these features made it appropriate for several usage such as packaging tapes, labels, and several types of straps. These are lightweight and durable films used for packaging purpose and are considered as highly suitable for printing. These films are cost-efficient solution for industrial packaging purpose as it offers high dimensional stability.

| Metric | Details |

| Market Size in 2024 | USD 3.5 Billion |

| Projected Market Size in 2035 | USD 7.07 Billion |

| CAGR (2026 - 2035) | 6.6% |

| Leading Region | Asia Pacific |

| Market Segmentation | By Thickness, By Application, By End-Use Industry and By Region |

The incorporation of AI technology in the market plays an important role in operational efficacy with automated control, predictive maintenance. It helps in the development of product with the integration of smart packaging, accelerated R&D, and tailored properties. AI is widely used for waste reduction and generation recyclable formulas for manufacturing of MOPP films. It supports in enhancing opportunities and cost saving properties.

The major raw materials utilized in this market is polypropylene resins, renewable and recycled materials.

The major components used in this market are polymerization, monoaxial stretching, extrusion.

This segment plays an important role in enhancing strategic partnership of the major market players.

Increasing Demand For Sustainable Packaging

The increasing demand for sustainable packaging has influenced the demand for the market. The market has encouraged move in the direction of biodegradable and recyclable options. MOPP films are being decomposable, bring into line well with these ecological initiatives, creating them a favoured choice among producers and customers alike. MOPP films provide superior barrier belongings, defending food items from contaminations and moisture, thus improving their safety and longevity. This rising trend in the direction of accessibility in food packing suggestively uplifts the market.

Volatile Raw Materials Charges

Volatile raw material charges in the packaging sector have hindered the growth of the market. The creation of MOPP films depends on polypropylene, that is dependent on variations in charges because of factors like geopolitical stress and fluctuations in crude oil charges. This contradiction can restrict the acceptance of MOPP films, as producers may be cautious to capitalize in resources that are not extensively recyclable in their goal markets.

Burgeoning E-commerce Industries

Burgeoning e-commerce industries has raised the opportunities for the market. Huge demand for effective packaging choices has enhanced the scope of development in this market. The incorporation of technology in the packaging resolutions like QR codes and moisture pointers can improve consumer interface and offer useful data about the freshness of the product. This trend is currently acquisitioning momentum, according to indication by the Food and Drug Administration (FDA), which shows the rising customer interest in clear and enlightening packaging.

Films Market Share, by Thickness Type 2025 (%)")

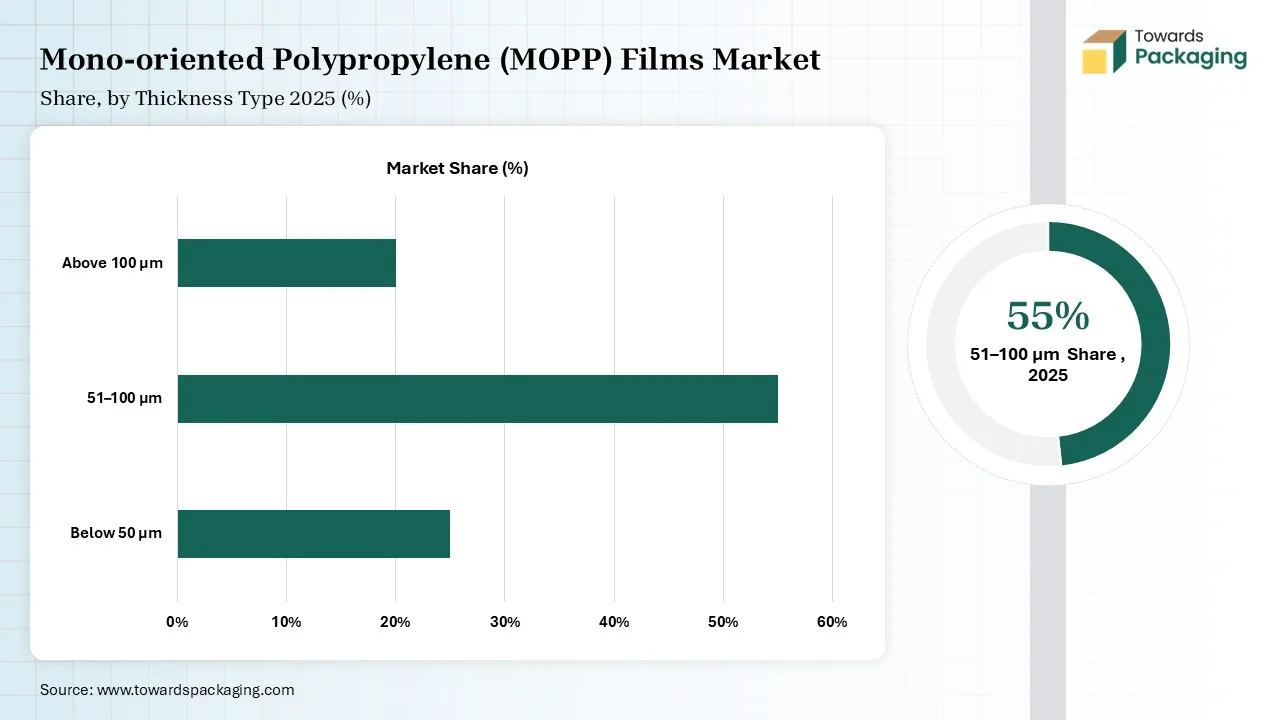

The 51–100 µm segment dominated the market in 2024 due to its barrier properties, flexibility, and strength. It is used for applications like tapes, rolled stocks, labels and tags. Films with this thickness are widely used in food & beverages, pharmaceuticals, and cosmetic industries. It meets the specific requirement of the packaging industries.

The below 50 µm segment is expected to grow at the fastest rate in the market during the forecast period. This segment is growing due to its cost-effectiveness and flexibility. These are used in food packaging, tapes, and labels as these are thin yet strong which is required for these purposes. Constant innovation with this segment has boosted the development of these films.

The packaging films segment held the largest share of the market in 2024 due to its high clarity and cost-effective solution for packaging. These packaging films are widely accepted for their superior strength and oxygen barrier properties. With the increasing demand for recyclable and sustainable packaging solution has influenced the growth of this segment. It is widely used for the protection of freshness of food products and extend its shelf life.

The labels & tags segment is expected to grow at the fastest rate in the market during the forecast period. This segment is growing rapidly due to its water-resistance and printability. Soft texture of this segment improves the aesthetic appeal and handling of the labels. Innovation in the opacity and thickness of the films has boosted the development of this segment.

Films Market Share, by End-Use Industry type 2025 (%)")

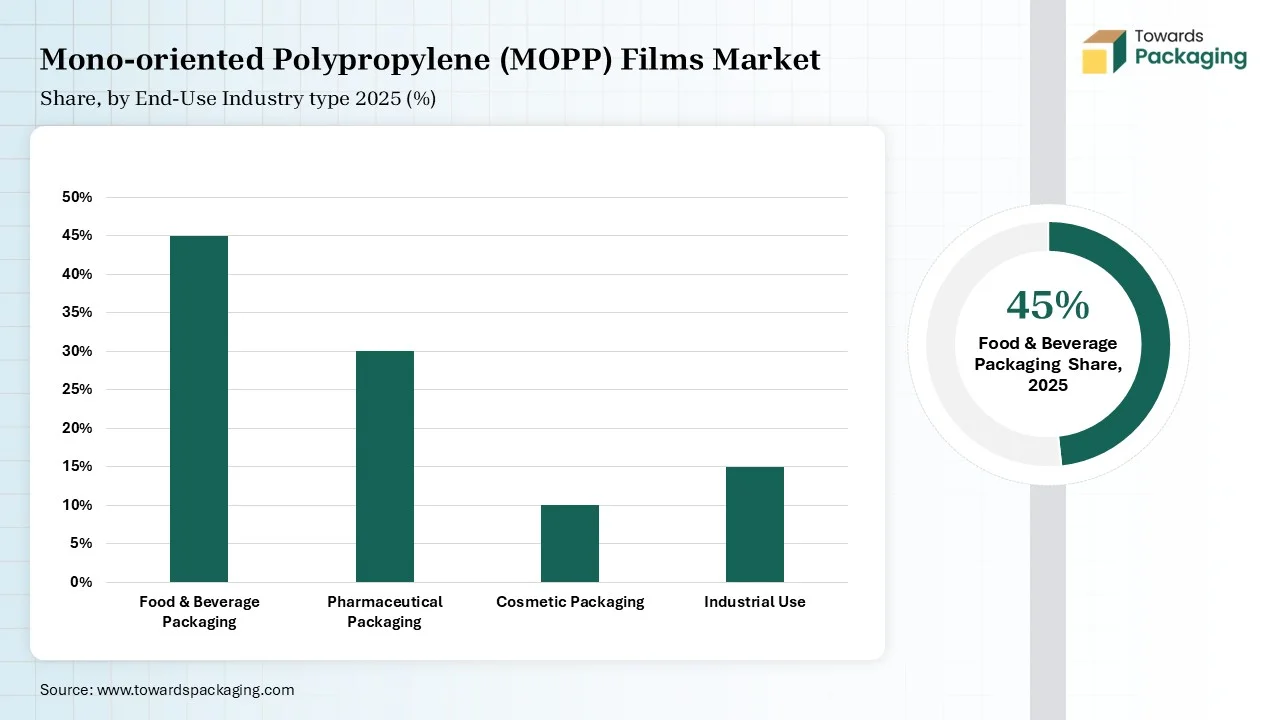

The food & beverage packaging segment held the largest share of the market in 2024 due to its sustainability, durability, and cost-effectiveness. It protects against ecological factors and meets consumers requirements for convenience. The inherent hygiene and strength have made these films widely accepted by several food & beverages brands. Rising consumption of packaged food products such as ready-to-eat meals and snacks has promoted the demand for this segment. Increasing necessity for packaging of frozen food products for convenience promote the development of this segment.

The pharmaceutical packaging segment is expected to grow at the fastest rate in the market during the forecast period. This segment is growing rapidly due to fulfilling strict regulatory needs. These films play an important role in producing multilayered packaging which protect drugs from oxygen and moisture barrier. The rising focus on mono-material and recyclable solution packaging development has evolved this market.

Films Market Share, by Region Type 2025 (%)")

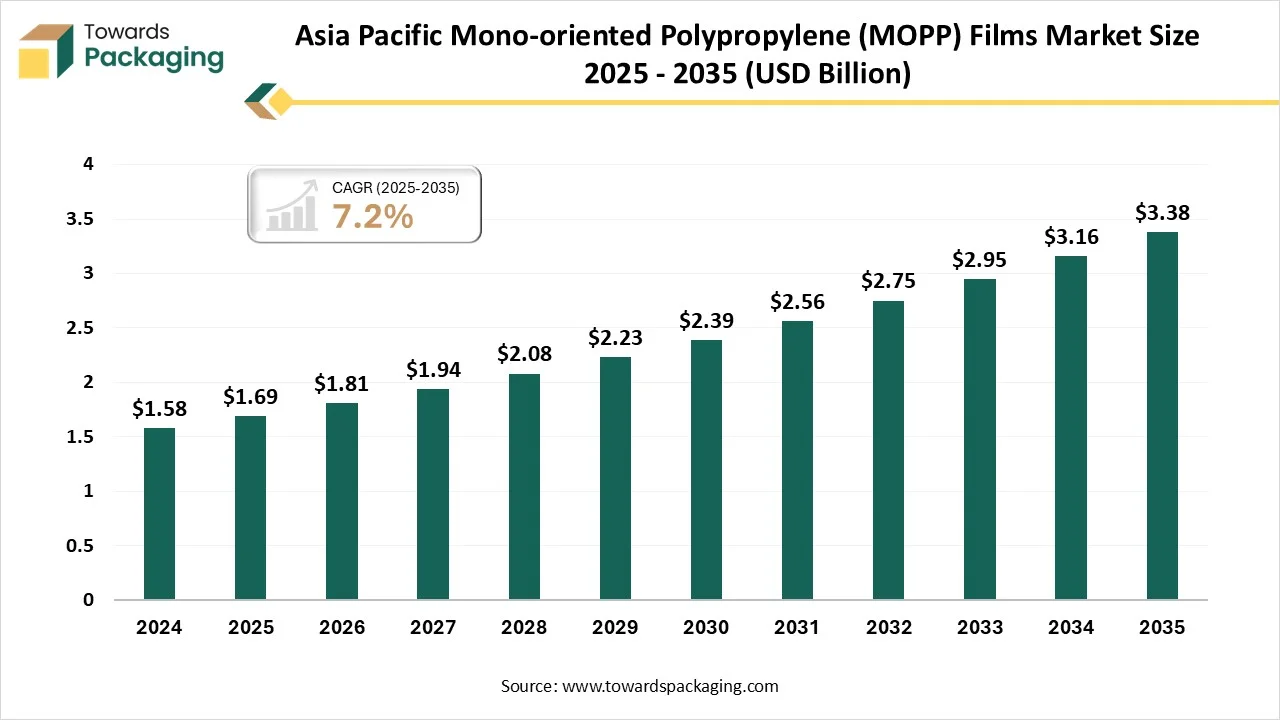

Films Market Size 2025 - 2035")

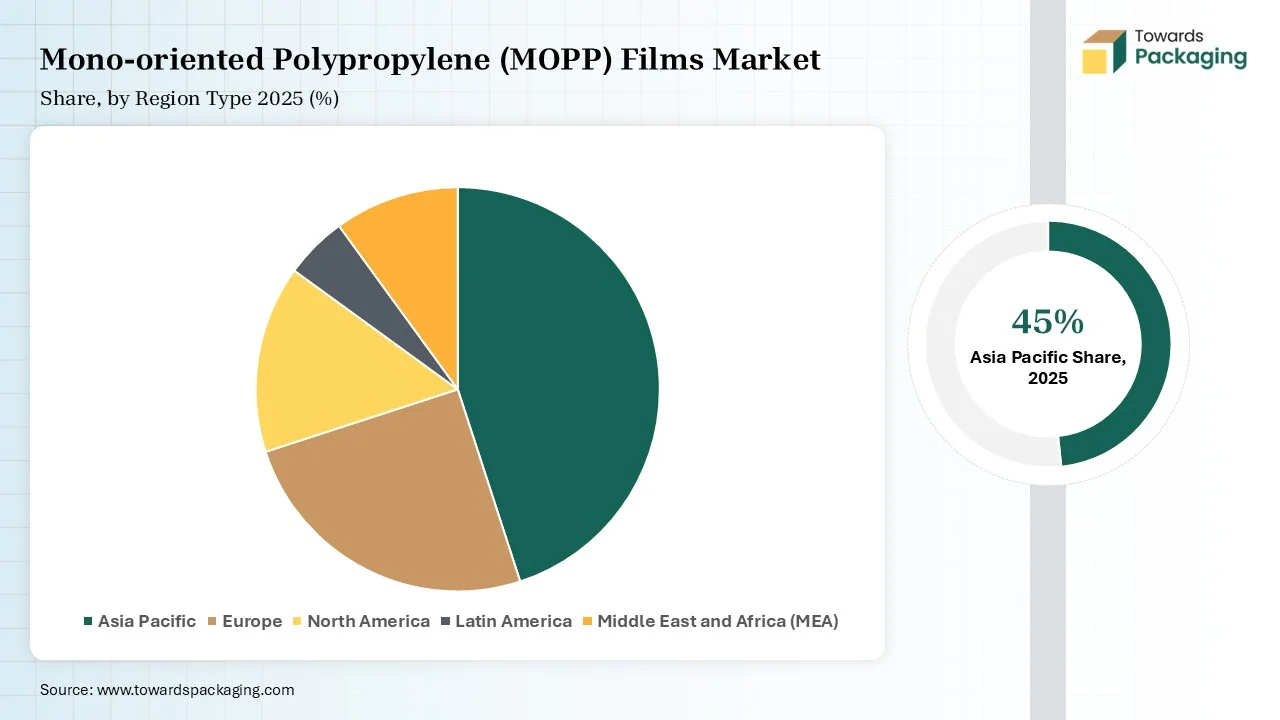

Asia Pacific held the largest share of the market in 2024, due to its large-scale production demand of these films. These films are widely used in pharmaceuticals and cosmetics, food & beverages, and e-commerce and retail packaging industries. The increasing demand for protection from factors like sunlight and heat, enhance shelf-life, and product preservation has raised the production and advancement of these films. The rising focus towards adoption of more sustainable packaging has boosted the growth of this industry.

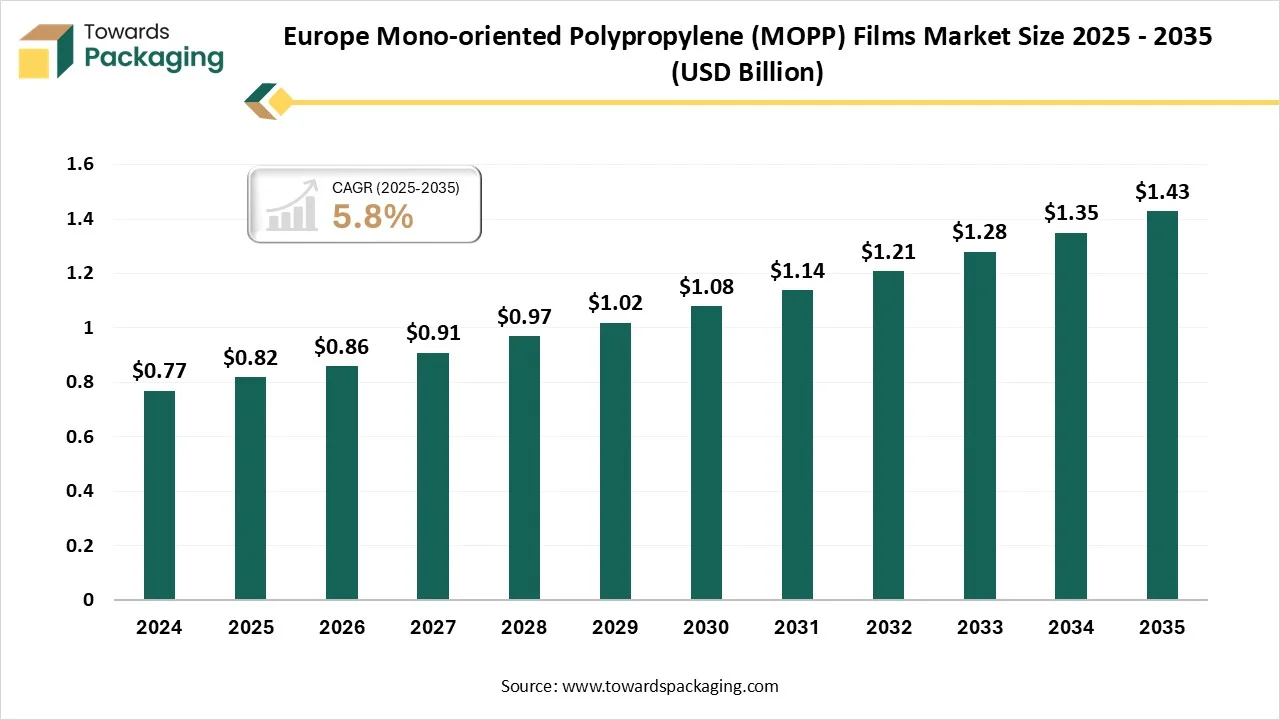

Films Market Size 2025 - 2035")

Europe held the largest share of the mono-oriented polypropylene (MOPP) films market in 2024, due to enhanced focus towards mono material packaging films. Strict supervisory guidelines in Europe have promoted the usage of the utilization of eco-friendly packaging. The major market players are widely investing for the development of packaging that can be recycled multiple times.

| Regions/ Countries | Regulatory Bodies | Key Regulations |

| UK | Food Standards Agency | National FCM guidance and authorisation routes for GB |

| Japan | Ministry of Health, Labour & Welfare (MHLW) | Permitted polymers, additives, and monomers. |

| Germany | BfR (Federal Institute for Risk Assessment) | It issues scientific recommendations on substances |

| India | FSSAI | BIS standards plastic cover packaging types. |

| China | National Health Commission | GB standards for food contact plastics |

By Thickness

By Application

By End-Use Industry

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarMono-oriented Polypropylene (MOPP) Films Market