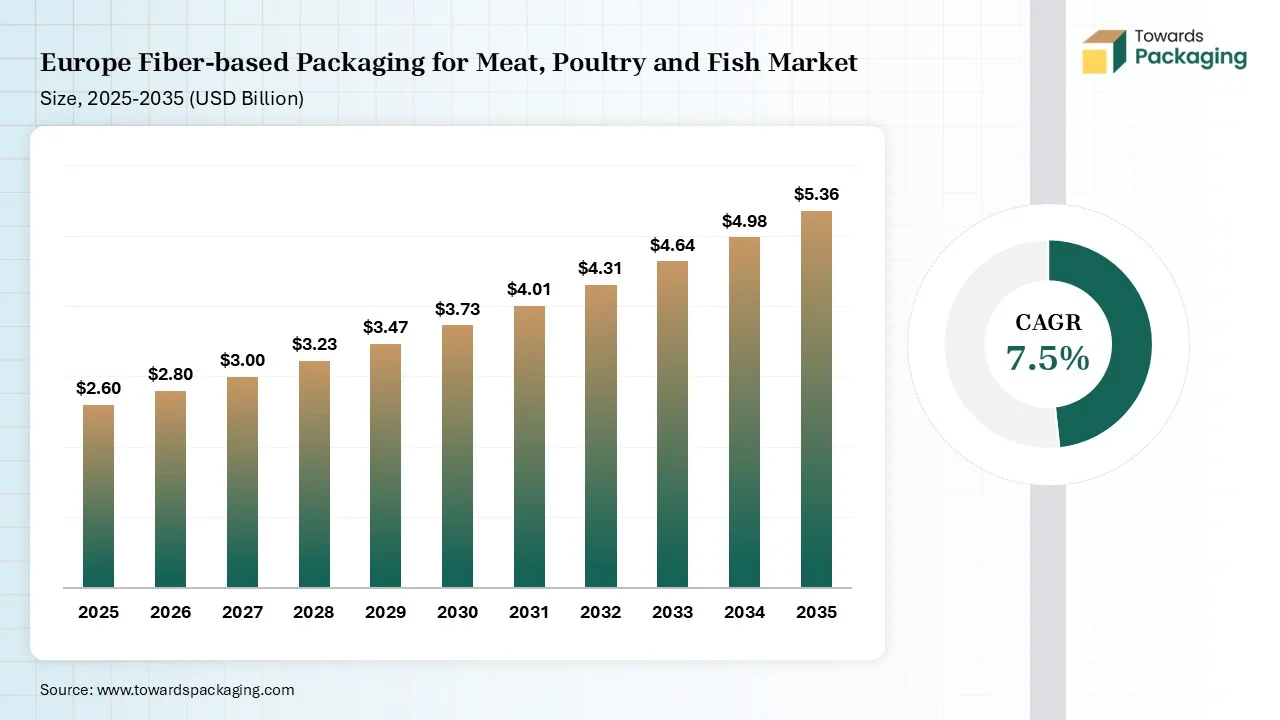

The Europe fiber-based packaging for meat, poultry, and fish market is projected to grow from USD 2.8 billion in 2026 to USD 5.36 billion by 2035, registering a CAGR of 7.5% during the forecast period. The market study provides detailed insights into market size, revenue forecasts, segment-wise analysis by material type, packaging format, and application. It further covers regional trends across Western Europe, Eastern Europe, Nordic countries, and Southern Europe, along with comprehensive company profiles, competitive benchmarking, value chain analysis, trade flow statistics, and extensive manufacturers and suppliers data. The report also evaluates sustainability regulations, consumer demand for eco-friendly packaging, and advancements in recyclable fiber-based solutions shaping the European market.

Market Size (2025): USD 2.6 Billion

CAGR (2025–2035): 7.5%

Market Volume (2025): 1.8 million Metric Tons

Market Volume CAGR (2025–2035): 6.8%

Fiber-based packaging has plant-based raw materials. They generally consist of wood, but can also be hemp, grass, bagasse, or bamboo, as a by-product of sugar cane processing. Such fibers are being processed into cardboard, paper, or molded pulp. Applications range from functional secured packaging to simple bags, as they are used for food or electronics. Current technologies also make it feasible to mix regular barriers against moisture, grease, or oxygen into the material. These points to demands that can be matched were lastly acceptable with plastic.

IoT (Internet of Things) packaging assists senders to transform into more environmentally friendly because it allows them to manage metrics such as humidity, surfaces, and temperature updates, as it protects against spoilage and waste of shipments that have sensitive goods, which include pharmaceuticals and food products.

Factors such as QR codes can manage return cycles and directions, which ensure users come back with containers for reuse and cleaning. Artificial Intelligence machines can help track the most effective combination of pinpoint and materials that have the least eco-friendly effect. Such technology uses such information to assist companies in lowering the materials that are used to make packaging with the least possible environmental impact.

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

|---|---|---|---|---|---|

| 1 | Huhtamaki | Espoo, Uusimaa | Finland | Global leader in molded fiber food packaging and fiber trays for protein products | Fiber food trays and sustainable packaging |

| 2 | Stora Enso | Helsinki | Finland | Leading innovator in fiber-based trays for fresh protein packaging | Formed fiber food trays |

| 3 | DS Smith | London, England | United Kingdom | Strong European paper-based food packaging capabilities | Fiber food packaging solutions |

| 4 | Smurfit Westrock | Dublin | Ireland | Large-scale paper-based food packaging manufacturer | Fiber tray and carton solutions |

| 5 | Graphic Packaging International | Atlanta, Georgia | USA | Significant investment in paperboard meat packaging technologies | Fiber trays and paperboard packaging |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | Metsä Board | Espoo, Uusimaa | Finland | Premium fresh-fiber paperboards used in protein packaging | Food-grade paperboard solutions |

| 2 | Billerud | Solna | Sweden | Strong sustainable packaging materials portfolio | Barrier paper and paperboard |

| 3 | Coveris | Vienna | Austria | Developing fiber-based packaging alternatives for food markets | Sustainable food packaging |

| 4 | Sonoco | Hartsville, South Carolina | USA | Producer of molded fiber food packaging solutions | Fiber food trays |

| 5 | Hartmann | Gentofte | Denmark | Leading molded fiber packaging specialist expanding food applications | Molded fiber trays |

| Rank | Company Name | Headquarters | Country | Why Relevant to This Packaging Market | Key Packaging Products/Services |

| 1 | PulPac | Gothenburg | Sweden | Pioneer of dry molded fiber manufacturing technology | Fiber tray production technology |

| 2 | Metsä Spring | Espoo, Uusimaa | Finland | Developer of next-generation fiber packaging innovations | Fiber packaging technologies |

| 3 | Paptic | Espoo, Uusimaa | Finland | Fiber-based packaging material innovator | Renewable fiber packaging materials |

| 4 | CKF Inc. | Hantsport, Nova Scotia | Canada | Producer of molded fiber food packaging products | Fiber trays and containers |

| 5 | EnviroPAK | Worcestershire, England | United Kingdom | Specialized molded fiber packaging producer | Food-grade molded fiber trays |

The molded fiber segment dominated the market with a 34% share in 2025. These are packaging products produced from recycled agricultural waste, recycled paper pulp, or natural fibers. The pulp is designed using molds and dried to make strong and secure packaging solutions.

Such products are compostable, biodegradable, and recyclable, which makes them an ideal choice for foam-dependent and plastic packaging. Currently, several molded fiber packaging brands are funding high-level molding technologies to generate packaging that is not sustainable but is also visually appealing and excessively functional.

The kraft paper & paperboard segment held 26% market share in 2025 because these papers are initially wood-based and well-known for their reliability and tear resistance, which makes them ideal for wraps and containers that demand strength. It depends on wood pulp that comes from trees, while bagasse uses agricultural byproducts, which streamlines the complete resource wastage. They are specifically convenient to print, fold, and create into a designed packaging, like bags and boxes.

The corrugated fiberboard segment held 22% market share in 2025 because they are strong and lightweight packaging material manufactured by sticking a fluted sheet, which is frequently referred to as the medium, between one or two flat liner boards. Corrugated fiberboards are used for food packaging that protects against bacteria, moisture, and other conditions. Additionally, these boxes are a famous option for e-commerce brands that deliver tailored and rigid packaging for online transactions.

The trays segment dominated the market with 30% share in 2025, as bagasse trays deliver an ideal option to foam or plastic trays, as they are created from compostable material, renewable or sugarcane fiber. Such disposable trays are breathable, reliable, and serve a precise display of fresh meat, fruits, and vegetables. They consist of a smooth layer that assists with tailored branding and barcode labelling, as the stackable design ensures convenient transportation and storage.

The boxes and cartons segment held the 24% market share in 2025 because bagasse fibers are naturally strong. They can firmly stand with a huge temperature range that ranges between -20 degrees Celsius and 120 degrees Celsius, which makes them more reliable than regular Styrofoam, which can conveniently leach or melt chemicals when heated. Sugarcane is quickly developing renewable resources by transforming into bagasse; every brand can lower its carbon footprint to up to 50% as compared to petroleum-based plastics.

The clamshell containers segment held 18% market share in 2025 because fiber-based clamshell packaging is a hinged, two-part device or container that opens and closes like a clamshell, like a natural clam, which has two hard shells. Such two shells are strongly and flexibly linked collectively at their edges through hinges that receive a shell closing and opening. Compostable food containers are utilized for ready-to-eat food, fruits and vegetables, and other spaces that need visual display and security.

The primary packaging segment dominated the market with 46% share in 2025 because this kind of packaging is directly linked to the products. It's crucial aim is to secure and manage their perfect elements. The primary packaging of a product is the initial layer or material that surrounds it and generally defines its minute unit of sale. The working of primary packaging is to classify, secure, communicate highlights and expiry dates, while in some cases it attracts attention and constructs commitment.

The secondary packaging segment held the 24% market share in 2025 because it is the layer of packaging that covers primary packaged products. Instances count cardboard boxes, shrink-wrapped bottles, cases, and taurus. On the other hand, primary packaging secures the product directly, but secondary packaging streamlines storage, handling, and transportation. For brands in sectors like pharmaceuticals, food and beverage, and consumer goods, secondary packaging ensures product safety and develops supply chain effectiveness.

The protective packaging segment held 18% market share in 2025, This segment has gained significant importance with the rapid expansion of e-commerce, where products must travel through complex logistics networks and require durable yet lightweight protection. The protective packaging is engineered to absorb shocks, prevent movement, reduce vibration, and minimize damage caused by compression or impact.

The meat (beef, pork, and lamb) segment dominated the market with 40% share in 2025 because color has stayed the main sales driver for red meats, and modified atmosphere packaging (MAP) has continued to receive attention. By precisely balancing carbon dioxide, oxygen, and nitrogen, MAP can ensure that the product has a fresh and bright look while lowering microbial development. On the other hand, fiber trays that are created from agricultural byproducts like wheat straw or sugarcane bagasse send a rigid sustainability signal in this case.

The poultry segment held the 35% market share in 2025 as a compostable and plant-based cling film for poultry developing, particularly for organic, natural, or luxury chicken initiatives. Such types of films are generally manufactured from bio-based polymers like PLA mixtures or other compostable materials and are designed to break down under industrial composting conditions. They are ideal for brand storytelling and environmentally friendly poultry packaging. They demand precise checking on freezer-safe poultry wrap uses and bone-in items.

The fish & seafood segment held the 25% market share in 2025. The fiber-based packaging made from cornstarch or sugarcane offers an eco-friendly alternative to regular plastics. Such materials are compostable and biodegradable, which lessens the ecologically unfriendly effect after disposal. Biodegradable trays created from starch composites, polylactic acid (PLA), and cellulose-based materials are being created as choices to regular PET trays and polystyrene.

Germany has dominated the market because the development is initially being driven by growing usage and official acceptance across main sectors like logistics, healthcare, food and beverages, and retail. As users urge for fiber-based packaging solution implementation, German brands are quickly moving towards fiber-based choices that deliver eco-friendly advantages, cost-effectiveness, and lightweight elements. The industry’s upward growth is step-by-step towards environmentally friendly materials, assisted by user choice and regulatory pressures for greener items.

United Kingdom is expected to experience the fastest growth in the market during the forecast period. The fiber-based packaging in this country is experiencing technological developments whose aim is to develop functionality, sustainability, and production effectiveness. Inventions are concentrated on growing high-level barrier coverings that develop shelf life for fragile items, along with the mixing of intelligent packaging solutions for user engagement and traceability. Additionally, developments in molding and pulping technologies are enabling the making of stronger, lighter, and deeper fiber-based designs.

By Material Type

By Product Type

By Packaging Type

By End-Use

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarEurope Fiber-based Packaging for Meat, Poultry and Fish Market