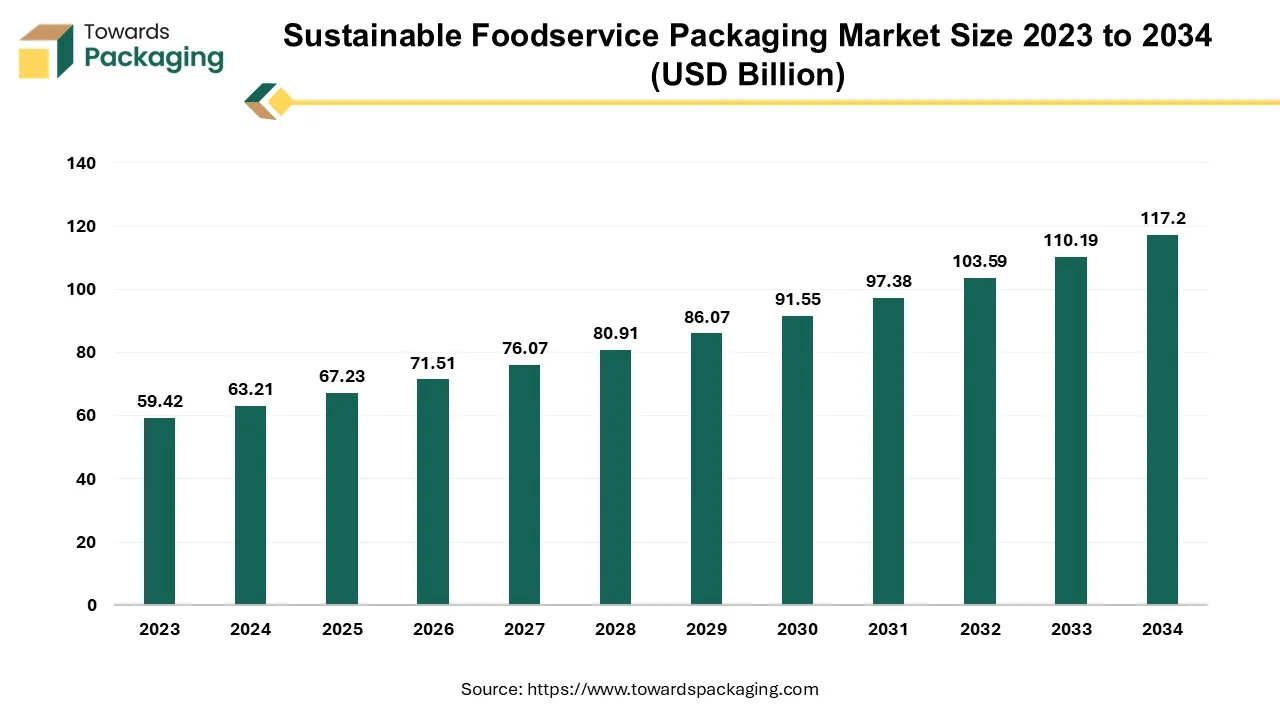

The sustainable foodservice packaging market is forecasted to expand from USD 71.52 billion in 2026 to USD 124.68 billion by 2035, growing at a CAGR of 6.37% from 2026 to 2035. This report includes an in-depth analysis of the market's key segments such as Quick Service Restaurants (QSR) (44.23% market share in 2025) and materials like paper & paperboard (41.21% market share). With Asia Pacific expected to grow at a CAGR of 8.60%, the report covers regional insights, company strategies, and emerging trends in biodegradable and compostable packaging.

To significantly reduce the foodservice industry's environmental effect, sustainable foodservice packaging is necessary. Companies can reduce the waste, preserve the natural resources and decrease the carbon emissions by switching to the sustainable materials. Companies in the foodservice industry can gain a lot from using the sustainable packaging. The sustainable packaging industry is growing at a significant rate. The foodservice sector, which holds a majority share of the market for sustainable packaging, is primarily responsible for this enormous growth. Sustainable foodservice packaging has multiple benefits that extend beyond environmental protection to include improved product quality, brand recognition, economic effectiveness through product repurposing and consumer preference.

The increasing environmental awareness among consumers coupled with the stringent government regulations and bans on single-use plastics is anticipated to augment the growth of the sustainable foodservice packaging market within the estimated timeframe. The development of innovative, cost-effective biodegradable, compostable, and recyclable materials along with the rise of the circular economy concept are also expected to support the market growth. Furthermore, the increasing investment in recycling and composting infrastructure as well as the growing demand for sustainability is also likely to contribute to the growth of the market in the years to come. The global packaging market is estimated to grow at a 3.16% CAGR between 2026 and 2035.

With more ecologically conscious consumers than ever, the use of sustainable packaging is growing. According to the 2023 Buying Green Report by Trivium Packaging, global inflation has caused consumer prices to increase significantly, yet customers are willing to pay extra for the products that are packaged sustainably. In general, 82% of the people surveyed said they would be willing to pay extra for the sustainable packaging that is an increase of 4 points from 2022 and 8 points from 2021. This suggests that despite the economy being worse, consumers still prioritize protecting the environment. Consumers that are between the ages of 18 and 24 are even more inclined towards sustainability, they lead at 90%. Today, sustainable packaging is essential for the company growth since environmentally concerned consumers are searching out the firms that adopt eco-friendly practices.

Foodservice brands are gradually shifting to using more environment friendly packaging for their goods due to the growing local restrictions, consumer demand along with the increasing need for the companies to be recognized as an ecologically conscious brand. Just by looking at or feeling the packaging, consumers are likely to be able to distinguish between the unsustainable and sustainable packaging. Sustainable packaging, which is typically used in place of most plastics, is more aesthetically acceptable to the consumers and is comprised of natural materials like bagasse, wood pulp, cornstarch and even seaweed. Since2022, especially the younger ones and those with higher incomes, have expressed an interest in buying the products that are packed sustainably. Thus, with the customers demand for more sustainable solutions and governments regulations, companies of the packaging goods and brands are progressively embracing the trend.

The higher cost of sustainable packaging materials is likely to hinder the growth of the sustainable foodservice packaging market within the estimated timeframe. Demand for more ecological packaging options is undoubtedly increasing. However, even though people want their packing materials to be eco-friendly, they additionally desire the same amazing package experience as before, in terms of the safety and quality, which can be difficult for packaging makers to achieve. However, preserving quality isn't the only challenge that producers face. Almost 40% of the brands have identified cost as one of the most significant hurdles in transitioning to sustainable packaging.

Furthermore, despite the use of the recycled materials is growing in popularity, especially since the passing of the Plastic Tax bill, using the recycled materials is still generally more expensive than utilizing virgin materials. This is due to the fact that the majority of the environmentally friendly packaging materials are quiet new and has a smaller production scale. Therefore, in order to alter the machinery line, more expenditure for research and development is required, which accounts for the increased costs. Furthermore, the majority of sustainable products are now produced at a higher cost due to the use of renewable energy in their manufacturing process. The eco certification is an additional factor that might frequently increase the pricing. These certifications are vital as they demonstrate to the customers that a business or product is truly eco-friendly and that false green marketing is not being used. However, quality checks and inspections, administrative charges, certification fees as well as the marketing expenses must all be covered in order to obtain an eco-certification.

The increasing investments in the sustainable packaging and composting infrastructure are likely to create opportunities for the growth of the sustainable foodservice packaging market in the years to come. In a circular economy, efficient sustainable packaging is intended for the recovery either by recycling or composting rather than for disposal in landfills or for burning. Companies have a significant chance to invest in their supply chains and the future of the world by adopting the circular economy. Organizations that focus on the environmentally friendly packaging should also make sure that the infrastructure for product-package sorting and reprocessing such as composting and recycling centers, is supported by the expansion of these facilities.

Some of the recent investments and funding made include:

These strategic investments in sustainable packaging and related infrastructure are important for the sustained growth and development of the sustainable foodservice packaging market.

| Rank | Company | Headquarters | Country | Why Relevant to This Market | Key Packaging Products/Services |

| 1 | Huhtamaki | Espoo | Finland | Global leader in sustainable foodservice packaging with extensive fiber-based and molded fiber portfolio | Cups, containers, trays, molded fiber packaging |

| 2 | Pactiv Evergreen | Lake Forest, Illinois | USA | Major supplier of paper, molded fiber, and recyclable foodservice packaging | Food containers, cups, trays, takeout packaging |

| 3 | Dart Container | Mason, Michigan | USA | Global foodservice packaging producer expanding recyclable and fiber-based product offerings | Cups, containers, lids, foodservice packaging |

| 4 | Sabert | Sayreville, New Jersey | USA | Leading supplier of sustainable food packaging for retail and foodservice markets | Fiber containers, compostable packaging, trays |

| 5 | Genpak | Charlotte, North Carolina | USA | Major provider of recyclable, compostable, and molded fiber foodservice packaging | Food containers, trays, hinged containers |

| Rank | Company | Headquarters | Country | Why Relevant to This Market | Key Packaging Products/Services |

| 1 | Graphic Packaging International | Atlanta, Georgia | USA | Strong portfolio of fiber-based foodservice packaging solutions | Paper cups, cartons, food containers |

| 2 | Stora Enso | Helsinki | Finland | Leading supplier of renewable fiber materials and formed fiber foodservice packaging | Fiber foodservice products |

| 3 | Berry Global | Evansville, Indiana | USA | Expanding portfolio of recyclable and reusable foodservice packaging | Recyclable containers and cups |

| 4 | Mondi | Weybridge, England | United Kingdom | Develops paper-based and barrier food packaging solutions | Paper food packaging and wraps |

| 5 | Amcor | Zürich | Switzerland | Invests in recyclable and bio-based flexible packaging for foodservice applications | Flexible food packaging solutions |

| Rank | Company | Headquarters | Country | Why Relevant to This Market | Key Packaging Products/Services |

| 1 | Notpla | London, England | United Kingdom | Pioneer in seaweed-based packaging for takeaway food and beverages | Seaweed-coated food containers and sachets |

| 2 | Footprint | Gilbert, Arizona | USA | Developer of plant-based molded fiber foodservice packaging | Molded fiber containers and trays |

| 3 | BioPak | Sydney, New South Wales | Australia | Specialist in compostable foodservice packaging | Compostable cups, containers and cutlery |

| 4 | Vegware | Edinburgh, Scotland | United Kingdom | Global supplier of commercially compostable foodservice packaging | Compostable foodservice packaging |

| 5 | Duni Group | Malmö | Sweden | European provider of sustainable tabletop and takeaway packaging solutions | Fiber containers, cups, takeaway packaging |

The paper & paperboard segment captured largest market share of 41.21% in 2025. Since long ago, paper and paperboard have been valuable materials for a variety of applications including printing, packaging, and arts. Cellulose fibers are woven into a network to form sheets of paper and paperboard. Both flexible and rigid packaging can be made using these materials. From freezing food storage to boiling water and heating in microwaves and traditional radiant heat ovens, paper and paperboard packaging can withstand a broad range of temperatures. The fact that paper and paperboard are made from renewable resource that is trees, is one of their main advantages. Also, to minimize their negative effects on the natural ecosystems and to assist the local communities that rely on the forestry for their livelihoods, many suppliers of paper and paperboard are dedicated to procuring their products from the certified sustainable forests. Paper and paperboard are a wise choice for customers and organizations trying to minimize their environmental effect as they provide a number of ecological benefits.

The quick service restaurants (QSR) segment held largest market share of 44.23% in 2025. Offering eco-friendly packaging and disposal bins that separate the recyclable, compostable, and biodegradable materials helps QSRs gain more popularity with environmentally conscious clients and draw in additional revenue. The fast food and quick-service restaurant (QSR) meal consumption of the millennials is fueled by their busy lifestyles. Growth in this segment is also being driven by operators' desire to be responsive to the customers' dining tastes and experience expectations. Unique QSR packaging trends are also being driven by independent QSRs, or the ones with no more than four locations with the same name. These eateries are anticipated to expand at the fastest rate per year, which will enable them to provide distinctive in-restaurant as well as delivery experiences. One characteristic that sets them apart is their tendency to provide quick cuisine that can be customized to the tastes of the local population.

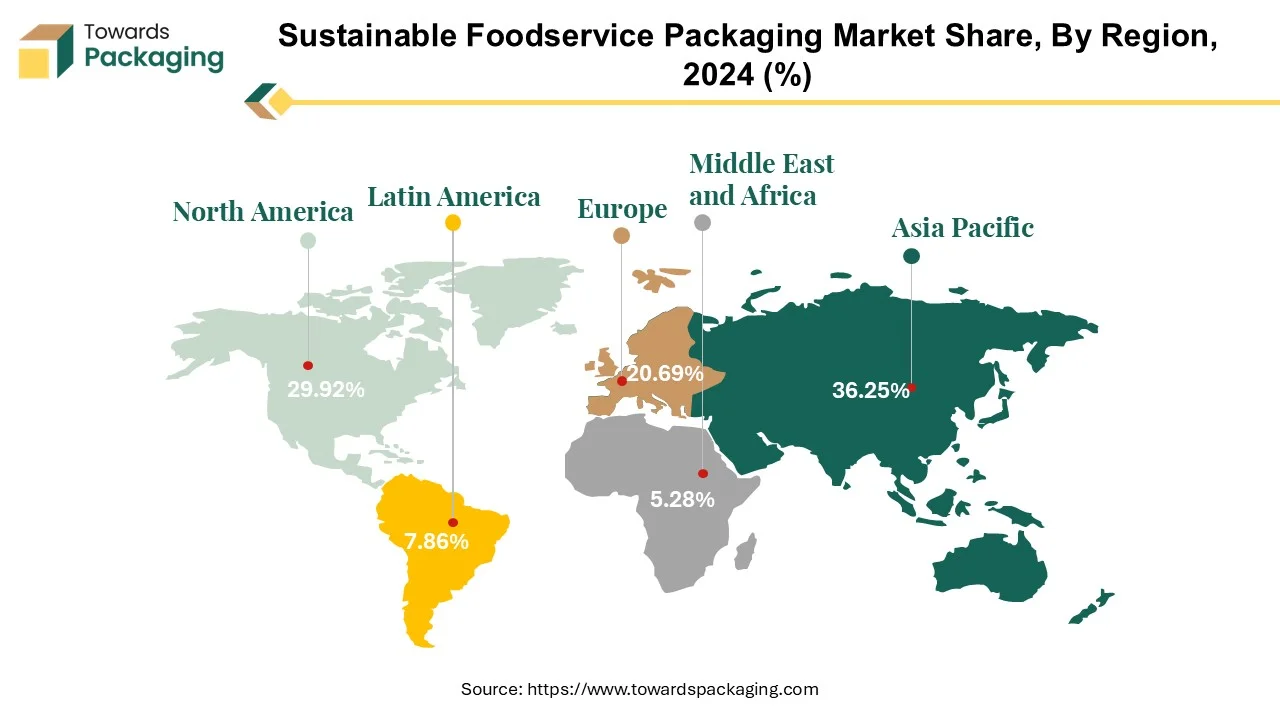

Asia Pacific held largest market share of 36.25% in 2025 and is expected to grow at a fastest CAGR of 8.60% during the forecast period. This is owing to the rapid urbanization which is leading to an increased demand for foodservice outlets, including quick service restaurants, cafes, and kiosks. Furthermore, the growing population in economies like China, India, and Indonesia with higher consumption rates is also likely to support the regional growth of the market. Additionally, the rapid economic growth as well as the increasing disposable incomes and higher consumer spending on foodservice are also anticipated to contribute to the regional growth of the market within the forecast period.

China Market Trends

China's sustainable foodservice packaging market is driven by the manufacturing infrastructure and economies of scale. China has implemented strict regulations on single-use plastics, pushing businesses to adopt sustainable alternatives. Sustainability is a key part of China’s national development goals, with support for green packaging technologies and materials. The government promotes recycling and biodegradable packaging solutions as part of its broader environmental policy.

China’s established manufacturing base allows it to produce sustainable packaging materials at scale and lower cost. Abundant natural resources like bamboo and agricultural by-products give China a local advantage in eco-friendly material production. Many Chinese companies control the entire supply chain from raw materials to finished packaging making them more efficient and competitive. The region exports a significant portion of sustainable packaging products to North America, Europe, and Southeast Asia. Many international food brands rely on Chinese suppliers for private label or custom sustainable packaging solutions. Apps like Meituan and Ele.me fuel massive demand for takeaway packaging, driving innovation in sustainability.

North America is expected to grow at a substantial CAGR of 4.96% in 2025. This is due stringent regulations aimed at reducing plastic waste and promoting sustainability across the region. Also, the consumer preferences towards products that are perceived to be healthier and more environmentally friendly along with the rise in food delivery services is further expected to support regional growth of the market in the years to come. Furthermore, the growing investment in the sustainability-focused startups and technologies as well as in the recycling and composting infrastructure is also expected to support the regional growth of the market in the near future.

U.S. Market Trends

The U.S. sustainable foodservice packaging market is driven by the boom in takeout and delivery services in the country. The post-COVID shift toward takeout, curbside pickup, and third-party food delivery (e.g., DoorDash, Uber Eats) has driven up packaging use. This surge is matched by pressure to adopt eco-friendly, tamper-evident, and durable packaging. U.S. consumers are increasingly prioritizing sustainability, recyclability, and biodegradability in their purchases. There’s a shift away from Styrofoam and single-use plastics toward compostable and recyclable alternatives, especially among Gen Z and Millennials.

Many states and cities have banned plastic straws, foam containers, and plastic bags. These regulations force foodservice businesses to adopt sustainable packaging solutions, such as PLA-based containers, paper straws, and fiber-based trays. Major foodservice brands (e.g., McDonald’s, Starbucks, Chipotle, Yum! Brands) are pledging to eliminate plastic and adopt 100% recyclable or compostable packaging by 2025–2030. These commitments create widespread adoption of sustainable materials across supply chains.

U.S. companies are investing in compostable bioplastics, molded fiber, bamboo, bagasse, and algae-based packaging. Startups and material science firms are bringing disruptive plant-based and recyclable packaging technologies to market. Large retailers like Walmart, Whole Foods, and Costco require suppliers and food vendors to use sustainable packaging. Universities, hospitals, and airports are also adopting green procurement policies, driving demand for compliant packaging. The U.S. government and private foundations are investing in recycling infrastructure, composting facilities, and packaging R&D.

Government initiatives and polices are the major drivers of the European market. The European Union’s Single-Use Plastics Directive (SUPD) bans or restricts many non-sustainable packaging items like plastic cutlery, straws, and Styrofoam containers. The EU Green Deal and Circular Economy Action Plan mandate businesses to reduce packaging waste and improve recyclability. Municipal composting is widespread in countries like France, Austria, and the Netherlands, supporting the use of compostable bioplastics and fiber-based packaging. EU funding programs and national grants support innovation in sustainable packaging materials and waste reduction technologies. Governments reward eco-certification, eco-design, and green labeling initiatives.

European consumers are among the most environmentally aware globally. There's a strong preference for minimalist, plastic-free, and biodegradable packaging in foodservice, especially in Scandinavia, Germany, and the UK. “Green” packaging can significantly influence brand loyalty and buying behavior in Europe. Many European countries have well-developed waste sorting, composting, and recycling systems, making it easier to integrate compostable and recyclable foodservice packaging.

Europe is home to industry leaders like Huhtamaki (Finland), DS Smith (UK), Mondi (Austria/UK), and Vegware (Scotland), all of which specialize in sustainable food packaging. These companies offer a wide portfolio of plant-based, compostable, and recyclable products, positioning Europe at the forefront of global supply. Major European foodservice and retail chains (e.g., Pret a Manger, Carrefour, Tesco) have adopted zero-waste and plastic-free goals. Hotels, airports, and quick-service restaurants across Europe are phasing out plastic in favor of paper, bamboo, and biopolymer-based foodservice packaging. European R&D is leading in molded fiber, seaweed-based films, biodegradable coatings, and compostable bioplastics.

New materials meet both functional requirements and eco-standards. Multi-stakeholder platforms unite businesses, governments, and NGOs to set goals for plastic reduction and sustainable alternatives. These partnerships accelerate market-wide shifts in the foodservice packaging industry. EU regulators are targeting false sustainability claims, increasing the demand for certified, verified eco-labels like OK Compost, TÜV Austria, and EU Ecolabel. European foodservice culture increasingly values local sourcing, low-impact operations, and eco-design all of which favour sustainable packaging practices. Cities like Paris, Copenhagen, and Amsterdam have introduced citywide sustainable foodservice initiatives, further driving adoption.

By Material

By Product

By End User

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarSustainable Foodservice Packaging Market