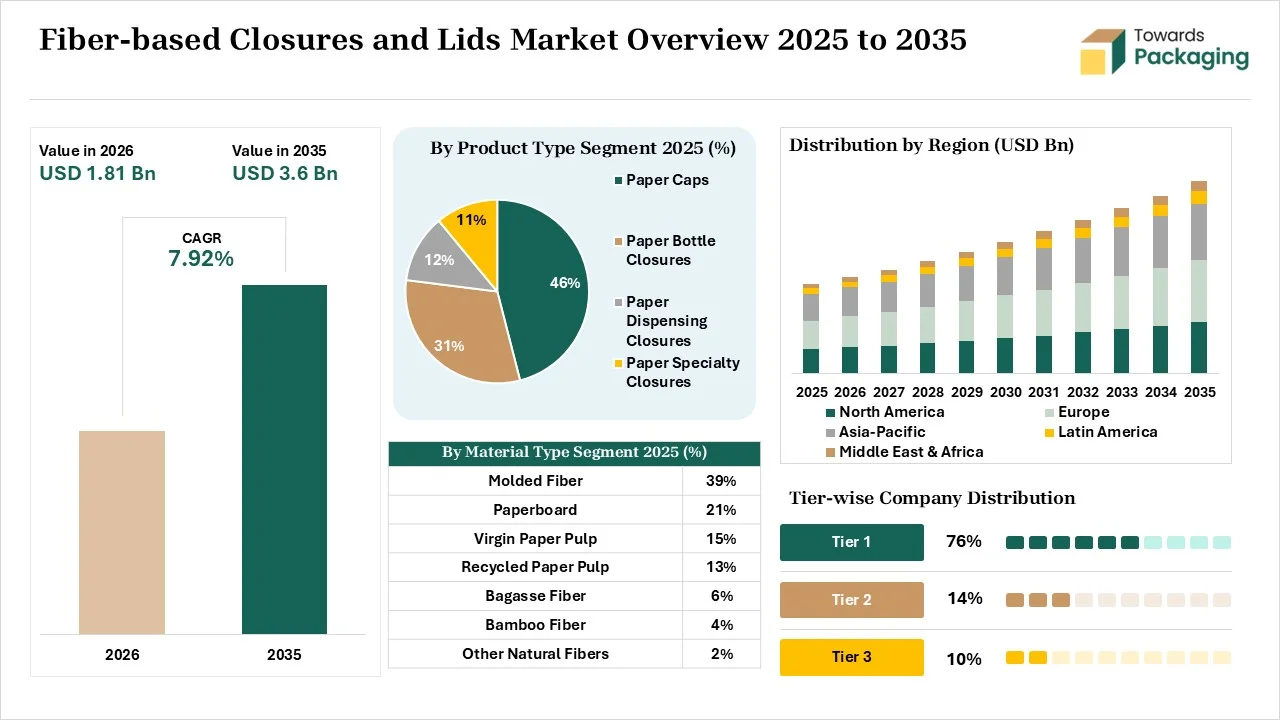

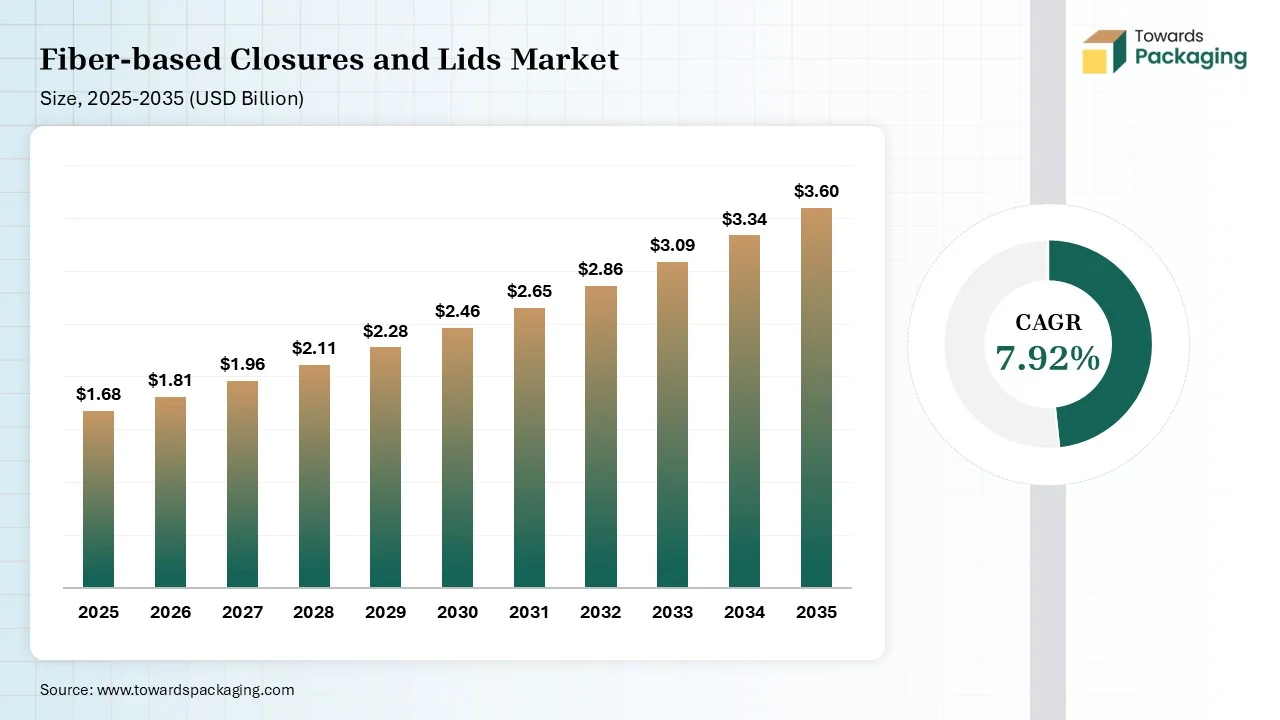

The fiber based closures and lids market is projected to grow from USD 1.81 billion in 2026 to USD 3.6 billion by 2035, registering a CAGR of 7.92% during the forecast period. The report covers market size, segment analysis, regional trends, company profiles, competitive analysis, value chain, trade statistics, manufacturers, suppliers, pricing trends, and growth opportunities shaping the industry.

Fiber-based closures and lids are an eco-friendly packaging solution made from renewable resources. Technologies like thermocompression, surface modification, DMF, and deep forming are used in the creation of fiber-based closures and lids. It offers benefits like biodegradability, superior tactile experience, true circularity, reduced carbon footprints, excellent functional performance, and cost competitiveness. It is widely used in products like vitamin bottles, specialty coffee, organic lotions, takeout containers, supplement bottles, cleaning products, and deli tubes.

For instance, in September 2025, the Great Earth of Scandinavia is shifting towards fiber-based closures for its entire supplement product range. The company uses lids manufactured by Blue Ocean Closures. The shift drives sustainability and increases the recyclability of the brand.

For instance, in February 2026, Live Puri adopted renewable fiber bottle caps. The company uses fiber caps for its vitamin product range. The NutraCap is widely used across glass bottles of vitamin products. The caps feature a natural brown appearance and are manufactured using Deep Forming technology.

The fiber-based closures and lids market growth is driven by the phase outs of plastics, food delivery surge, growing EPR fees, volatile petrochemical prices, barrier coatings innovations, rise of brand differentiations, corporate sustainability pledges, the takeout boom, changing consumer preferences, manufacturing advancements, and the rise in renewable sourcing.

In March 2025, Elopak invested in Blue Ocean Closures to advance the development of fiber-based caps. The collaboration gives the Elopak company rights to distribute, market, and sell fiber-based caps. The collaboration increases the paper content and lowers plastic use in cartons.

In September 2025, Yangi secured investment of US$11.8 million to speed up the fiber packaging solution. The investment supports transitioning towards renewable fiber, and the investment was gathered through a Series A funding round. The investors participating in the investment round includes Almi Invest GreenTech, FutureLab & Partners, Voith, Industrifonden, Turret Oy, and Chanel.

The fiber-based closures and lids market is experiencing technological developments due to the growing demand for replacing single-use plastics. Technological developments like 3D design software, production automation, smart materials, integrated plug solutions, digital tooling, and machine learning are driven by demand for lowering energy consumption and ensuring uniform thickness. The key breakthrough is the AI integration, which helps in scaling production.

AI understands accurate fiber combinations and helps in material selection. AI monitors the factory environments and spots structural inconsistencies in fiber-based closures & lids. AI supports anti-counterfeiting tracking and increases sorting efficiency. AI optimizes the closure performance and supports advanced material engineering. Overall, AI helps in predictive maintenance, precision manufacturing, and defect reduction.

The key raw materials, such as wheat straw, bamboo, virgin wood pulp, bagasse, recycled paper pulp, and hemp, are required.

Material processing steps are pulp preparation, additive integration, forming, drying, finishing, and sealing. Material conversion of wet molded fiber includes slurry preparation, vacuum forming, & hot pressing, and dry molded fiber includes air-laid processing, precision, & barrier application.

Design includes structural integrity, barrier performance, and functionality. Prototyping involves rapid prototyping, validation, and recycling compliance.

The caps segment dominated the market with 34.8% share in 2025. The growing plastic prices and the stringent environmental targets increase the adoption of fiber-based caps. The focus on lowering energy consumption and the preference for tactile feel increase the use of fiber-based caps. The brand's adoption of easily recyclable materials helps with expansion. The drop-in integration, cost competitiveness, and excellent functionality of fiber-based caps drive the segment growth.

The lids segment held the 28.60% market share in 2025 and is expected to grow at the fastest CAGR of 8.8% during the forecast period. The focus on avoiding hefty penalties on plastic packaging and the shift away from fossil-based plastic increase the use of fiber-based lids. The rise in daily supplements and the exploding delivery markets increases the use of fiber-based lids. The continued growth in RTE meals and the manufacturing technology innovations support the segment growth.

The molded fiber segment dominated the market with 43.2% share in 2025. The paper recycling streams and the growing global prohibitions increase the use of molded fiber. The rising fiber-based replacements and the QSRs' preference for natural packaging increase the use of molded fiber. The high functionality, robust temperature tolerance, leak reduction, and thermal insulation of molded fiber help with expansion. The favorable manufacturing policies drive the segment growth.

The bagasse fiber segment held the 14.40% market share in 2025 and is expected to grow at the fastest CAGR of 9.2% during the forecast period. The growing demand for grease-resistant closures and the aggressive legislative mandates increase the use of bagasse fiber. The expanding modern diners and the innovative molding technologies increase the adoption of bagasse fiber. The municipal plastic bans and the sugar-rich economies increase the use of bagasse fiber. The higher adoption of bagasse fibers in brands like Starbucks supports the segment growth.

The uncoated segment dominated the market with 31.6% share in 2025. The growing household paper recycling and the increasing use of dry forming technologies increase the adoption of the uncoated option. The restriction on multi-layer packaging and the growing FMCG branding increase the use of the uncoated option. The supply chain volatility and the presence of commercial composting streams increase the use of the uncoated option. The price stability and ease of recycling of the uncoated coating type drive the segment growth.

The bio-based coating segment held the 16.40% market share in 2025 and is expected to grow at the fastest CAGR of 9.8% during the forecast period. The increased phasing out of PFAS and the focus on avoiding synthetic plastic liners increase the use of bio-based coatings. The shift away from rigid plastic lids and the advancing industrial technology increases the use of bio-based coatings. The interest in plant-based dispersions and corporate social responsibility increases the use of bio-based coatings. The seamless compatibility and high-performance of bio-based coating support the segment growth.

The threaded closures segment dominated the market with 41.5% share in 2025. The growing use of glass packaging and the rise in high-speed bottling operations increase the use of threaded closures. The shortened production cycles and the availability of FSC-certified cellulosic fibers increase the use of threaded closures. The rise in nutraceutical purchasing and growing eco-packaging startups increases the use of threaded closures. The unmatched sealing integrity, reusability, and seamless industrial integration of threaded closures drive the segment growth.

The snap-fit closures segment held the 24.80% market share in 2025 and is expected to grow at the fastest CAGR of 8.7% during the forecast period. The popularity of bagasse food containers and the higher adoption of biodegradable closures increase the use of snap-fit closures. The focus on replacing plastic lids and the need to reduce energy requirements increases the use of snap-fit closures. The expanding hybrid fiber caps and the single-handed operation increase the use of snap-fit closures, supporting the segment growth.

The wet molding segment dominated the market with 47.3% share in 2025. The expansion of cold drink cups and the growing beverage applications increases the use of wet molding technology. The development of food clamshells and the proven manufacturing base increases the use of wet molding. The interest in purchasing daily-use items and focus on preventing leaks increases the use of wet molding. The superior aesthetics, excellent brand appeal, and dimensional precision of wet molding drive the segment growth.

The dry molding segment held the 24.90% market share in 2025 and is expected to grow at the fastest CAGR of 9.1% during the forecast period. The focus on lowering CO2 emissions and the avoidance of fossil-based components in fast-food chains increases the use of dry molding. The production of intricate lids and the production of functional items increases the use of dry molding. The unprecedented production speeds and the high technical performance of dry molding support the segment growth.

The 31-50 mm segment dominated the market with 39.80% share in 2025. The rise in condiment jars and the reduction of material waste increases the adoption of the 31-50 mm size. The growing use of compostable materials in the cosmetic industry and the focus on moisture-absorption capabilities increase the adoption of 31-50mm. The consumer convenience, higher material yield, perfect fit, and seamless scalability of 31-50mm drives the segment growth.

The 51-70 mm segment held the 27.50% market share in 2025 and is expected to grow at the fastest CAGR of 8.6% during the forecast period. The adoption of fiber lids in packaging industries and the booming takeaway services increase the use of 51-70mm size. The rise in wide-mouth jars and the creation of leak-resistant caps increases the use of 51-70mm size. The expansion of standard-size coffee cups and the explosion of standard consumables increase the adoption of 51-70mm, supporting the overall segment growth.

The food & beverage segment dominated the market with 55.2% share in 2025. The hygiene focus in F&B and the avoidance of single-use plastic in food supply chains increase the adoption of fiber-based closures and lids. The priority for fiber packaging in to-go beverages and the need for liquid sealing increases the use of fiber-based closures and lids. The need to enhance operational efficiency in the food production and the consumer's growing interest in food delivery apps drive the segment growth.

The pharmaceuticals segment held the 11.70% market share in 2025 and is expected to grow at the fastest CAGR of 9% during the forecast period. The shift away from conventional metal in the pharmaceutical industry and the growing traditional packaging costs increase the adoption of fiber-based closures and lids. The expanding health supplements and the pharmaceutical focus on following EPR rules increase the use of fiber-based closures and lids. The protection of drugs and growing healthcare applications support the segment growth.

The direct sales segment dominated the market with 61.4% share in 2025. The growing specialized needs in brands increase direct sales adoption. The focus on avoiding retail markups and the growing direct purchasing in brands increases the use of direct sales. The integration of branding strategies and the company's demand for just-in-time supply increases the use of direct sales. The focus on navigating sustainability mandates and the demonstration of long-term ROI increases the use of direct sales, driving the segment growth.

The online/B2B platforms segment held the 11.70% market share in 2025 and is expected to grow at the fastest CAGR of 10.3% during the forecast period. The rise searching of compliant packaging options and the high-volume procurement needs increase the use of online/B2B platforms. The focus on alignment with the circular economy and the presence of diverse global suppliers increase the adoption of online/B2B platforms. The need for pricing comparison and the expanding ghost kitchens increases the use of online/B2B platforms, supporting the segment growth.

Europe dominated the market with 31.8% share in 2025. The stricter legislative mandates and the growing European prices increase the adoption of fiber-based closures and lids. The consumer goods brands focus on fulfilling ESG goals, and the strong packaging machinery presence increases production of fiber-based closures and lids. The transition to molded fiber packaging and the focus on avoiding harmful PFAS chemicals increase the use of fiber-based closures and lids, driving the market growth.

North America held the 28.10% market share in 2025. The recycled-content mandates and the fluctuating petrochemical costs increase the adoption of fiber-based closures and lids. The cellulosic materials advancements and the shift to sustainable packaging designs increase the use of fiber-based closures and lids. The food service is shifting away from plastic lids, and the burgeoning e-commerce logistics increases the adoption of fiber-based closures and lids, supporting the market growth.

Asia Pacific held the 27.60% market share in 2025 and is expected to grow at the fastest CAGR of 9.2% during the forecast period. The strong F&B manufacturing hubs and the advancing dry-molded fiber technology increase the adoption of fiber-based closures and lids. The rise in food delivery apps and the transition away from petrochemical-based packaging increase the adoption of fiber-based closures and lids. The thriving bottled water industry and the burgeoning QSR deliveries increase the use of fiber-based closures and lids, boosting the market growth.

Latin America held the 6.80% market share in 2025. The plastic bans in cities like Chile & others, and the growing demand for eco-friendly packaging substitutes, increase the adoption of fiber-based closures and lids. The rising takeout culture and the preference for health-friendly products increase the use of fiber-based closures and lids. The abundance of forest products and the agile local manufacturing support the market growth.

The Middle East & Africa held the 5.70% market share in 2025. The growing regulations on non-biodegradable plastics and the expansion of city hubs increase the adoption of fiber-based closures and lids. The growing agricultural waste recycling and the explosion of online delivery apps increase the use of fiber-based closures and lids. The sustainability commitments of foodservice operators boost the overall market growth.

| Rank | Company | Headquarters | Country | Major Contribution to Fiber-based Closures and Lids Market | Key Packaging Products and Services |

| 1. | PulPac | Gothenburg, Sweden | Sweden | The company collaborated with Optima and PA Consulting to manufacture fiber-based caps. The company produces aseptic carton closures and paper-based lids. | Paper-Based Cartons Closures, Standardized Food-Grade Lids, Plastic-like Bottle Closures |

| 2. | Huhtamaki | Espoo, Finland | Finland | The company’s product, Future Smart Duo, is developed from plant pulp and wood fibers. The company uses SMF technology to manufacture stackable lids. | SMF Solutions, Future Smart Lids, Envirable Molded Fiber Lids |

| 3. | Smurfit WestRock | Dublin, Ireland | Ireland | The company manufactured products like retail-ready lids, TopClip Beverage solutions, and fiber-based fitments. | Bag-in-Box Fiber Caps & Closures, Molded Fiber Punnets & Lids, CanCollar, PETCollar, TopClip |

| 4. | Stora Enso Oyj | Helsinki, Finland | Finland | The company uses dry-molded fiber technology. The company collaborated with AISA and Blue Ocean Closures for manufacturing a fiber-based closure for a paperboard tube. | PureFiber Lids, Cupforma Natura Aqua, Fiber-Based Tube Closures |

| 5. | Blue Ocean Closures | Karlstad, Sweden | Sweden | The company uses dry-forming technology to manufacture fiber-based closures and lids. The company collaborated with the Coca-Cola company to provide fiber closures to their bottles. | NutraCap 53 mm, NutraCap 38-400, NutraCap 45-400, Paper-Plug Range |

By Product Type

By Material

By Coating Type

By Closure Type

By Manufacturing Process

By Diameter / Size

By End-Use Industry

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarFiber-based Closures and Lids Market