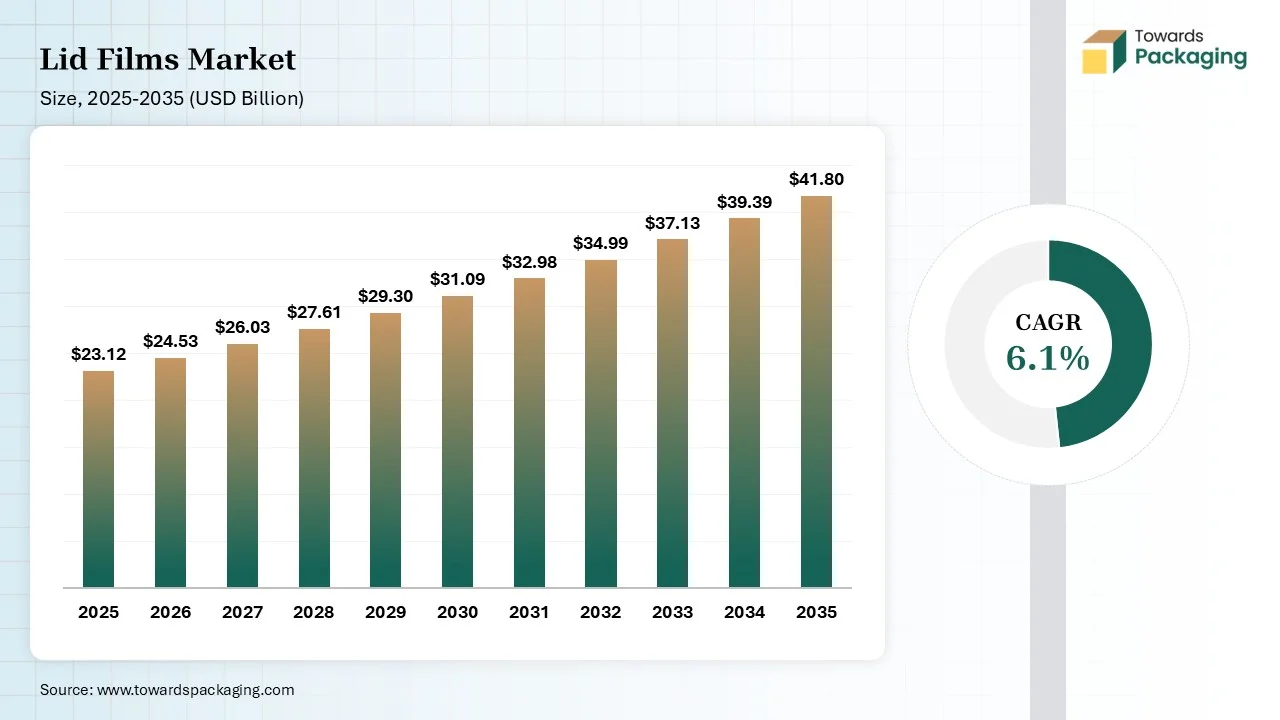

The lid films market is projected to grow from USD 24.53 billion in 2026 to USD 41.8 billion by 2035, registering a CAGR of 6.1% during the forecast period. This report provides detailed insights into market size, segment-level data by material type, product type, and end-use industries, along with regional analysis across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. It also covers key company profiles, competitive landscape, value chain analysis, trade data, and comprehensive information on manufacturers and suppliers driving the industry forward.

Lid films are a thin layer of material utilized to pack containers like trays, cups, and tubs. It serves as a preventive barrier, protects freshness, and frequently suggests highlights like printability or peelability for branding usage. Generally, they are created from aluminum foil or plastic, as lidding films are crafted to align with needs like puncture resistance, heat resistance, and barrier characteristics against oxygen, moisture, and pollutants.

In current thermoformed tray and cup packaging, the lidding film operates as the “leading web”, which matches bottom materials such as PP, APET, or PS and current high-speed sealing lines. Actual designs include PE, PET, BOPP, and CPP, which rely on the needed sealing and barrier results.

Metallized films (MET) such as MET OPP have been chosen as a substitute for foil in terms of flexible packaging uses. As technology develops, MET PET has become a perfect choice for replacing foil in terms of lidding applications. Currently, as food producers choose their lidding design, they are always seeking MET PET more than ever to check the growing cost and restricted availability of foil. Films are easily available, and the broadness of the vacuum-deposited metal is only a few hundred angstroms, so the effect of the amount of film will be totally avoidable as compared with what is calculated for aluminum foil.

High-Barrier lidding films segment dominated the market with 36% share in 2025 as they are tailored multi-layer flexible materials which are designed to seal strong containers, cups, or taurus that serve as a perfect protective layer against external elements like moisture, oxygen, and light. Such films are complicated for expanding the shelf life of fragile products, specifically in the pharmaceutical and food sectors, by tracking internal surroundings and protecting them from pollutants. High-barrier lidding films lower the moisture and oxygen levels to protect against mold and oxidation, which mainly lowers the food waste.

The resealable films segment held 6% market share in 2025 and is expected to have the fastest CAGR of 8% during the forecast period. Flanges reseal PET is ideal for manufacturers and other products, such as pasta, that users utilize over a long period of time. They are crafted with accuracy laser perforation, as such solution make the updated eco-friendly lettuce which demand to stay fresh for longer time. Flange reseal PET film highlights a luxury, easy-to-open closure which can be opened and sealed again up to 10 times and is crafted for application with PET containers.

The dual ovenable films segment held the second largest share of 16% in 2025 as ovenable lidding is made of lower molecular weight polyethylene terephthalate copoly esters and is crafted for food link up to 400 degrees Fahrenheit. It packs well to PET-covered paperboard, but usually do not seal well to OPET film, which is laminated or mostly impactful and modified CPET trays. They enable users to shift products directly from the freezer to either a regular oven or a microwave without piercing or removing the film.

The polyethylene segment dominated the market with 30% share in 2025. because they are plastic films manufactured from polyethylene, a prevalent polymer in the plastic sector. Such films are greatly used in many households uses, ranging from packaging to protective coverings, which possess their durability, flexibility, and cost-effectiveness. Polyethylene is a thermoplastic polymer, which indicates it can be reformed and melted, which makes PE film recyclable.

The bio-based/sustainable materials segment held 4% market share in 2025 and is expected to have the fastest CAGR of 8.5% during the forecast period. Sustainable material invention are a main trend in the lidding packaging sector, that counts recyclable designs, bio-based materials and the compostable selections. Such inventions goal is to lower surrounding effect while tracking packaging result and prevention. Furthermore, user feedback show that 83% of consumers choose sustainable packaging, which is crucial part of the brand responsibility.

The Polyethylene Terephthalate (PET) segment held the second largest share of 25% in 2025 because these films are an applicable polyester material in terms of packaging. Manufacturers generate Thai films with aromatic rings and ester groups. Such space makes PET film water-resistant and rigid. PET films are flexible for packaging purposes as they are utilized in drinks, food, and medicine. These films have the potential to block moisture and can be conveniently recycled.

The polypropylene (PP) segment held the third largest share of 20% in 2025, as they are solid and small particles created from polypropylene, which are highly reliable for thermoplastic polymer. They are well-known for their ideal chemical and physical properties, like granules that serve exceptional reliability, high chemical resistance, and likely a lower melting point. This packaging is a prevalent usage of PP plastic, which is valued for its moisture resistance, durability, and potential to be packed smoothly. They are widely utilized for trays, containers, and flexible films that protect pharmaceutical and food products while tracking freshness and safety.

The PVC segment held fourth largest share of 8% in 2025. They are reliable materials utilized in lid films for their durability, excellent clarity, and barrier elements that are against oxygen and moisture. They are prevalently used in both flexible cling wraps and rigid lidding for the purpose of confectionery, snacks, and pharmaceutical blister packs. PVC is widely used as a lidding or base material in blister packaging for capsules and tablets, which frequently interacts with layers like PVDC for developed moisture prevention.

The food & Beverages segment dominated the market with 65% share in 2025, as for the food packaging industry, particularly for items like ready meals, protecting the flavor and aroma is necessary. Lidding film secures the food from eco-friendly factors that can affect its quality, by making sure that the product stays as fresh as possible when it reaches users. One of the main benefits of lidding films is their potential to protect the flavor and aroma of packaged food. Aroma plays an important role in user satisfaction and product requests.

The industrial & others segment held 10% market share in 2025 and is expected to have the fastest CAGR of 7.5% during the forecast period. In the electronics sector, lidding films are tailored to flexible packaging materials that are used to pack rigid trays or containers that carry fragile components. Like food-grade films, electronics lidding films are crafted to solve technical problems like moisture ingress and static discharge during storage and transport. Getter Combo lids are one of the high-level lids that are used in hermetic packaging, which include getter materials to absorb internal gases to protect device degradation over time.

The pharmaceutical & healthcare segment held the second largest share of 15% in 2025 because in this industry, lidding film plays a main role in protecting the smoothness of medications. They make barrier elements that protect medical products against external factors such as moisture and light, which affect their quality. Lidding films are widely used in unit-dose product packaging, which guarantees the precision of medication dosage. This is necessary and crucial for patients who depend on precise medical regimens. Lidding films are designed with child security in mind, as they are child resistant.

The personal care & cosmetics segment held 10% market share in 2025 due to lidding films are important for tracking the reliability of personal care & cosmetics. They prevent them from contamination and pollutants, which protects the product from evaporation and leakage. They are used in this sector to deliver marketing and branding machines. They deliver as a marketing and branding machine as they help us to develop the complete appearance of the request and identity to users. Additionally, tamper-evident highlights in lidding films are important for user safety in cosmetic and personal care products.

The trays segment dominated the market with 40% share in 2025, as lidding films enable food delivery services to manage the visual look of the dishes they serve. The transparent nature of the films allows users to watch the food inside, which develops its appearance and tempts them to order. Additionally, lidding films can be tailored with branding elements, logos, or nutritional information that forces the brand identity and serves insightful information to users.

Pouches & Top Web segment held second largest share of 22% in 2025 and expects the fastest CAGR of 8% during the forecast period. Lidding films are a type of flexible packaging film that is utilized to pack containers such as plastic tubs, taurus, or blister packs. They are prevalently found in dairy products, ready-to-eat meals, snacks, and pharmaceutical packaging. Such films serve as an airtight pack to protect freshness, which delivers tamper-evidence and serves user-friendly characteristics such as reclosability and peelability.

Cups & containers segment held the third largest share of 20% in 2025, from a single-serve fruit jellies for purpose of kids to a luxury gelatin-based desserts for adults, and packaging plays a complicated role in designing both product integrity and shelf appeal. Among the several inventions in food packaging, metallized PET lidding films have quickly become a game changer. Metallized lidding films, which have a sleek and mirror-like finish, have instantly developed product requests. The film’s layer not only creates the brand logo that differentiates itself but also makes a judgment of quality.

The bottles & jars segment held the fourth largest share of 10% in 2025. A high-barrier film in any sauce container with a lid is a perfect partnership for freshness. It effectively lowers the oxygen by entering as oxygen can cause pollutants. An ideal film in a plastic sauce container with a lid tracks freshness for an extra 3 to 6 months. Brands demand an airtight pack for any quality sauce container with a lid. A packed disposable sauce container that has a lid also stays uncontaminated.

Asia Pacific dominated market with 35% share in 2025, as there is a huge urge for packaged easy foods, snacks that come in single-serve portable formats, and dairy products such as flavored milk and yogurt. The fast development of online grocery platforms and food delivery services is developing in India, China, and Southeast Asia. Additionally, cost-effective production facilities and discovered food processing centres make the region a main centre for packaging purposes. Also, they are witnessing fast growth, which is driven by growing urbanization, growing disposable incomes, and a developing choice for ready-to-eat and packaged foods.

India Lid Films Market Trends

This country’s inventions in thermoforming films are currently focused on many main areas. High-barrier films show one of the fastest-developing segments, as food manufacturers and retailers find packaging that can expand product shelf life by lowering dependency on preservatives. Multilayer films that contain polyvinylidene chloride (PVDC) or ethylene vinyl alcohol (EVOH) barrier layers have received selective shifting for cheese, meat, and ready-meal packaging.

Middle East & Africa are expected to experience the fastest growth in the market with 7.5% CAGR during the forecast period. The food sector accounts for the biggest urge for cheese tubs, yoghurt cups, and ready-to-eat meals, specifically in the UAE and Saudi Arabia. Latest regulations, such as Saudi Arabia’s “Regulation of Plastic Products, “ have made it compulsory that packaging should be biodegradable or recyclable, which is a move towards mono-materials and eco-friendly films. Furthermore, the growth of food delivery services has also developed the demand for resealable and puncture-resistant packaging to track freshness during transportation.

UAE Lid Films Market Trends

The demand for this industry in the UAE is due to the country’s strong food and beverage industry and its position as a main regional logistics centre. The growing urbanization and quick-paced lifestyle are driving demand for single-serve dairy products, ready-to-eat meals, and lastly, on-the-go packaging. There are growing e-commerce and food delivery industries that ensure product safety during logistics and transportation. The heavy funds in healthcare infrastructure are developing the demand for peelable and sterile seals for the purpose of blister packs and diagnostics.

By Product Type

By Material Type

By Application

By Packaging Format

By Regions

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarLid Films Market