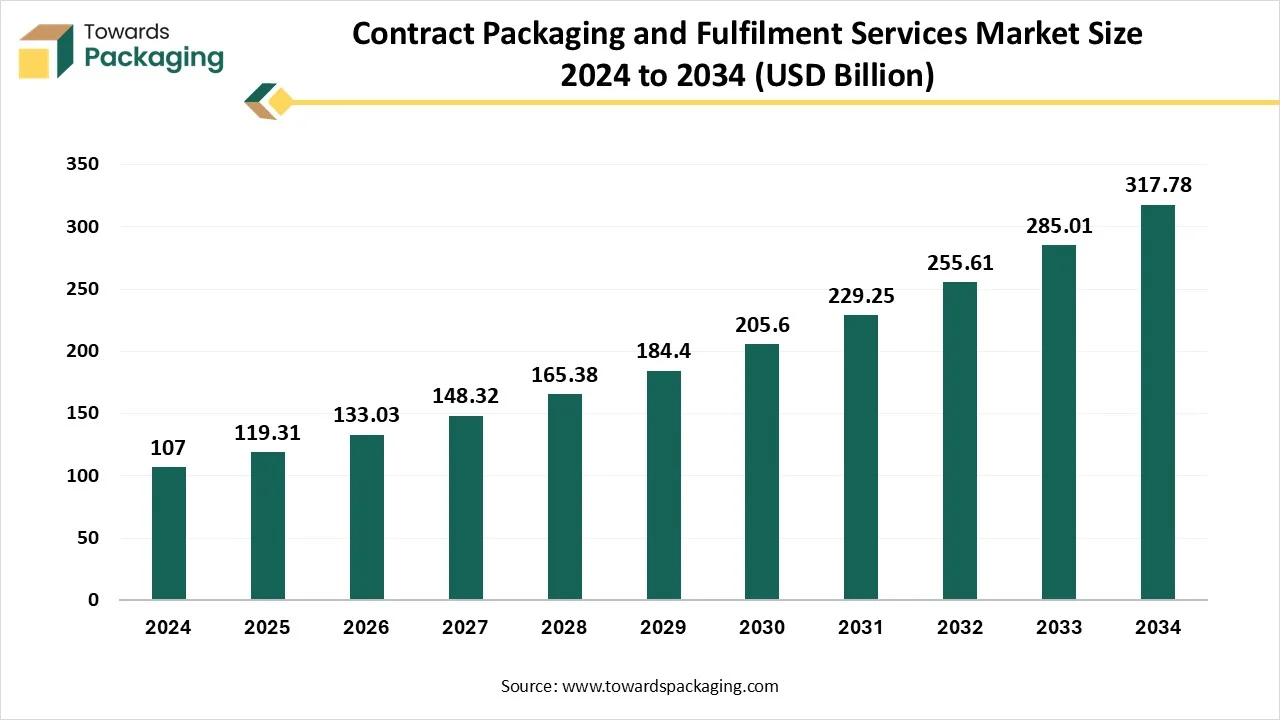

The contract packaging and fulfilment services market is forecasted to expand from USD 133.03 billion in 2026 to USD 354.33 billion by 2035, growing at a CAGR of 11.5% from 2026 to 2035. The report provides detailed insights into service types (contract packaging, fulfilment services), packaging materials (plastic 44%, biodegradable/compostable materials), business models (B2B fulfilment 40%, D2C), channel types (e-commerce, omnichannel), and end-use industries (food & beverage 35%, pharmaceuticals, personal care, electronics).

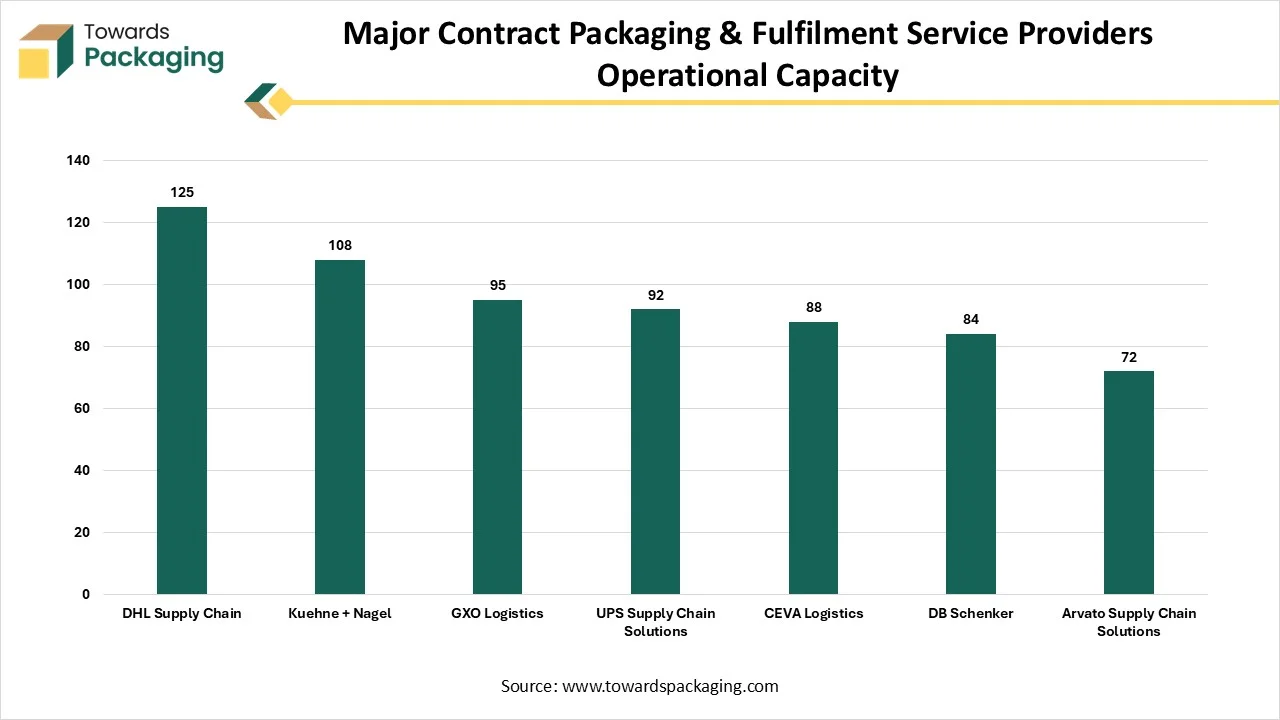

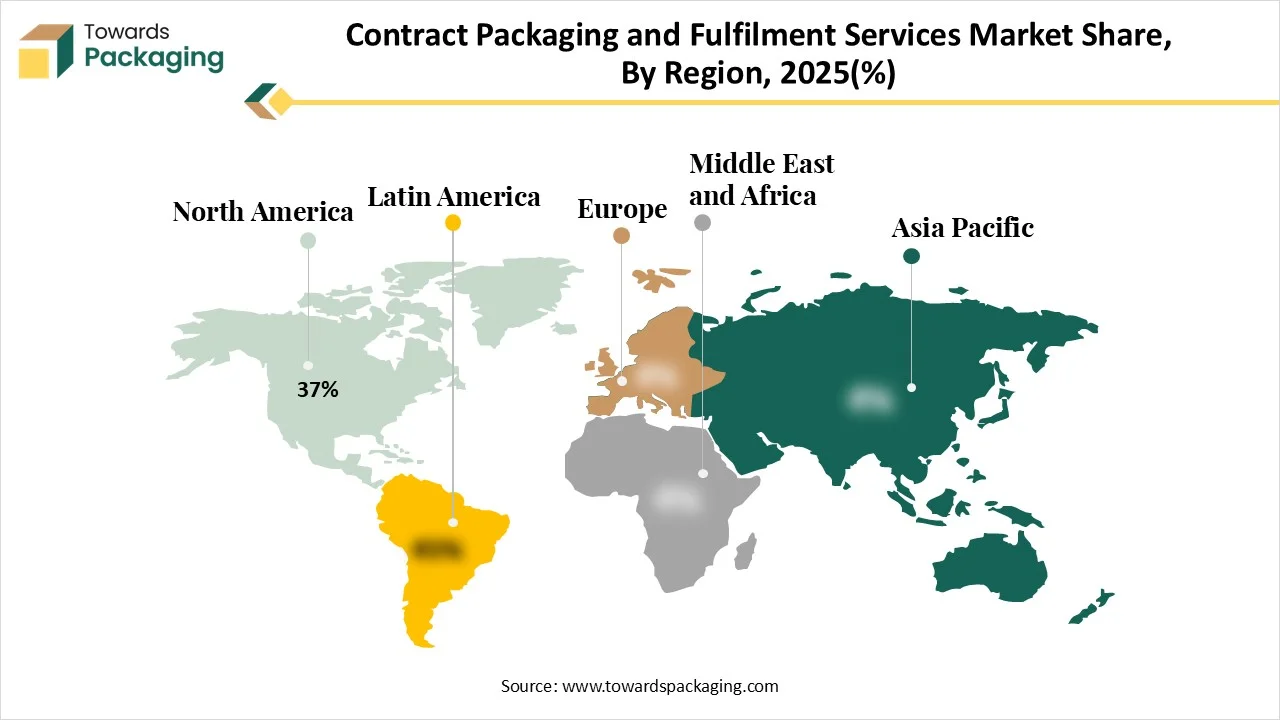

Regional coverage includes North America 37% share, Europe, Asia Pacific fastest-growing, Latin America, and MEA, along with competitive analysis of DHL Supply Chain, Kuehne + Nagel, GXO Logistics, UPS Supply Chain, CEVA Logistics, DB Schenker, Arvato, value chain mapping from primary to tertiary packaging, trade insights, and manufacturer capacities, e.g., DHL 125B units, Kuehne + Nagel 108B units annually.

Contract packaging and fulfilment services refer to third-party services where companies outsource the packaging and/or order fulfillment processes of their products. These services include primary and secondary packaging, kitting, assembly, warehousing, labeling, distribution, and shipping. The industry serves various sectors such as food and beverage, pharmaceuticals, personal care, and electronics, offering scalability, cost-efficiency, and time-to-market advantages.

| Indicator | Statistical Value |

| Global packaged consumer & healthcare units handled annually | 2.35 trillion units |

| Units processed through third-party contract packers | 34 to 37% |

| Contract-packaged units per year | 820 to 870 billion units |

| Orders processed by contract fulfilment providers | 185 to 210 billion shipments |

| Core service types | Packaging, labeling, kitting, warehousing, distribution |

In today's rapidly evolving technological landscape, Artificial intelligence in contract packaging and fulfillment services holds great potential to transform the market by cost savings, optimizing the supply chain, enhancing logistics efficiency, complying with regulatory standards, improving customer satisfaction, and introducing innovative solutions across various operational areas. AI algorithms and Machine learning enable packaging companies and their manufacturing partners to efficiently automate complex and repetitive processes. Harnessing the power of AI in contract packaging and fulfilment services makes the operations faster, smarter, efficient, and adaptable. AI can significantly optimize production schedules to inventory management, minimize wastages, optimize processes, and improve efficiency.

| Region | Annual Units Processed (Billion Units) | Share (%) |

| North America | 305 | 35 |

| Europe | 270 | 31 |

| Asia-Pacific | 225 | 26 |

| Latin America | 45 | 5 |

| Middle East & Africa | 25 | 3 |

Driver

Rising Preference ofBusinesses Toward Contract Packaging and Fulfillment Services

The increasing preference of businesses toward contract packaging and fulfilment services is expected to boost the growth of the market during the forecast period. In recent years, the market has witnessed a rapid shift in the preference of business firms toward contract packaging and fulfilment services, to focus on their core competency, reduce costs, and improve efficiency. Several businesses across various industries are increasingly preferring to outsource their packaging operations to avoid high capital investments in infrastructure and specialized equipment. Contract packaging and fulfilment services providers offer expertise in different packaging types and technologies, enabling organizations to meet diverse needs.

Stringent Regulatory Standards

The strict regulatory requirements are anticipated to hamper the market's growth. Several industries, particularly food and beverage and pharmaceuticals, often face stringent regulations regarding packaging and compliance, which can lead to increased operational costs for contract packagers.-In addition, the rising competition from in-house packaging is likely to limit the expansion of the global contract packaging and fulfilment services market. Businesses often prefer to handle packaging internally to maintain good control and potentially reduce costs.

How is the Rising Expansion of the Food and Beverages and Pharmaceutical Industry Impacting the Market’s Growth?

The rising expansion of the food and beverages and pharmaceutical industry is projected to offer lucrative growth opportunities to the contract packaging and fulfilment services market during the forecast period. Food and beverages and the pharmaceutical industry increasingly prefer contract packaging and fulfilment services to prevent supply chain disruption and reduce the time to market by outsourcing the packaging activities. The food and beverage industry relies on these services to meet fluctuating demands, effectively handle promotional packaging, and manage the consumer demand for seasonal products.

Contract packaging and fulfilment services assist pharmaceutical firms in complying with the stringent regulatory requirements of authorized government bodies, including anti-counterfeiting measures and serialization.-Therefore, the food and beverage and pharmaceutical industry can significantly enhance their operational efficiencies by leveraging third-party contract packaging and fulfilment services.

| End-Use Industry | Annual Units Outsourced (Billion Units) |

| Food & beverage | 285 |

| Pharmaceuticals | 215 |

| Consumer goods & personal care | 175 |

| Medical devices | 85 |

| Nutraceuticals | 65 |

| Industrial & others | 45 |

The contract packaging held a dominant presence in the contract packaging and fulfilment services market in 2024. Contract packaging involves the outsourcing of packaging services to specialized third-party providers, allowing businesses of various sectors, including food and beverage, pharmaceuticals, cosmetics, electronics, and others, to focus on their core competencies while leveraging the specialized expertise, equipment, and resources of these providers. In addition, the rapid innovation and automation in packaging technologies assist contract packagers in handling fluctuating volumes, reducing cost, and improving efficiency.

On the other hand, the fulfilment services segment is expected to grow at a notable rate. The segment fastest growth is mainly driven by the owing to the increasing trend of outsourcing among various businesses. Fulfilment services include order processing, warehousing, packaging, shipping, and other services for businesses, especially e-commerce companies. These services allow businesses to focus on core competencies or aspects of their operations.

The large enterprises-segment registered its dominance in the market. Large enterprises-increasingly prefer contract packaging and fulfilment services as a cost-effective way to access specialized packaging and fulfilment capabilities, meet the sustainability trends, and strongly focus on core competencies like new product development and marketing, which further assists them to compete in the market.

On the other hand, the small and medium enterprises (SMEs)-segment is expected to grow at the fastest CAGR. Contract packaging and fulfilment services provide small and medium enterprises (SMEs)-with access to sophisticated packaging and fulfilment capabilities, which they often lack due to high machinery cost or resource limitations. These services assist them in concentrating on core competencies and meeting diverse packaging requirements, including customized solutions for smaller production volumes.

The e-commerce-segment is expected to dominate the market with the largest share in 2024, owing to the rising expansion of online retail and increasing demand for specialized packaging across various industries. In the direct-to-consumer deliveries, the specialized packaging solutions play a crucial role in ensuring product safety and appeal.-E-commerce businesses are increasingly preferring these services to significantly improve delivery times, manage fluctuating order volumes, and boost customer experience.-These factors are supporting the segment’s growth during the forecast period.

On the other hand, the omnichannel-segment is expected to witness remarkable growth. Omni channel’s business strategy focused on offering a seamless and consistent customer experience in both online and offline channels. The segment’s growth is driven by the rapid expansion of online and organized retail, which significantly increases the need for innovative, sustainable, and customized packaging solutions.

The B2B fulfilment-segment registered its dominance over the global contract packaging and fulfilment services market in 2024. B2B fulfillment increasingly focuses on handling bulk orders between businesses, which often include order processing, packaging, labeling, inventory management, shipping, warehousing, and other services. B2B fulfillment is widely adopted by prominent businesses to ensure the timely delivery of goods to other businesses, to maintain smooth operations.-

On the other hand, the D2C fulfilment-is expected to grow significantly in the coming years, owing to the rapid expansion of the e-commerce platforms in developing and developed nations, along with increasing consumer demand for eco-friendly packaging. Companies are increasingly preferring D2C fulfillment to gain control over their customer experience, optimize their supply chains, and improve profitability margins.

The plastic segment accounted for the dominating share in 2024. The growth of the segment is mainly driven by various benefits offered by the plastic materials, including durability,-versatility, lightweight, and cost-effectiveness. Plastic packaging materials can be easily moulded into various shapes and sizes which making them an attractive option for various diverse industries to meet product needs.

On the other hand, the biodegradable/compostable materials segment is expected to witness a significant share during the forecast period, owing to the rising environmental awareness and regulatory pressure. Consumers are increasingly preferring biodegradable/compostable packaging solutions to reduce their carbon footprint in the environment.

The food and beverages segment held the majority of the market share in 2024. Outsourcing allows food and beverage companies to reduce overhead costs associated with labor, equipment, and infrastructure, and concentrate on their core competencies, like product development and marketing. Contract packagers in the food and beverage industry offer various services such as shrink wrapping, pouch filling, and other specialized packaging solutions for different food categories.

On the other hand, the personal care and cosmetics-segment is projected to grow at a CAGR of between 2025 and 2034, owing to the rapid expansion of e-commerce and increasing emphasis on sustainable packaging practices. The personal care and cosmetics-industry outsources various services such as serialization, sterilization, and adheres to compliance for meeting stringent industry regulations.

| Company | Headquarters | Annual Unit Handling Capacity (Billion Units) |

| DHL Supply Chain | Germany | 125 |

| Kuehne + Nagel | Switzerland | 108 |

| GXO Logistics | United States | 95 |

| UPS Supply Chain Solutions | United States | 92 |

| CEVA Logistics | France | 88 |

| DB Schenker | Germany | 84 |

| Arvato Supply Chain Solutions | Germany | 72 |

North America held the dominant share of the contract packaging and fulfilment services market in 2024. North America, especially the U.S., has a presence of well-established food and beverage, pharmaceuticals, electronics, and cosmetics industries, which spurs the demand for contract packaging and fulfillment services solutions. Companies are increasingly outsourcing packaging and fulfilment services to specialized providers to improve efficiency, reduce costs, and focus on core business activities like product development and marketing. Business can significantly optimize their supply chains and enhance operational efficiencies by leveraging third-party services.

Factors such as the presence of a favourable regulatory environment, increasing demand for sustainable and customized packaging across various industries, the rising entry of key warehousing vendors in the field of contract packaging, growing demand for specialized packaging solutions, and increasing focus of businesses seeking to gain a competitive edge by outsourcing non-core operations. Moreover, the rapid growth of the e-commerce sector and the great focus on sustainability to align with the circular economy principle are expected to accelerate the revenue of the contract packaging and fulfilment services market in the coming years.

Asia Pacific growth is driven by the rapid expansion of the food and beverages industry, a rising shift towards digitization and technological advancement, rapid industrialization, increasing demand for specialized packaging solutions, increasing business need to optimize supply chain management, and growing focus on improving consumer engagement experiences. The strong presence of small and medium enterprises (SMEs), which have increasingly adopted contract packaging and fulfillment services to optimize their operations and compete with larger businesses in the market.

The expansion of the e-commerce sector, particularly in developing economies, and the increasing penetration of smartphones are anticipated to drive the market’s expansion during the forecast period. Several food and beverage, pharmaceuticals, and cosmetics companies operating in the region are employing contract packaging and fulfillment services solutions to focus on core competencies, optimize supply chain, enhance sustainability, reduce cost, combat counterfeiting, and improve speed to market.

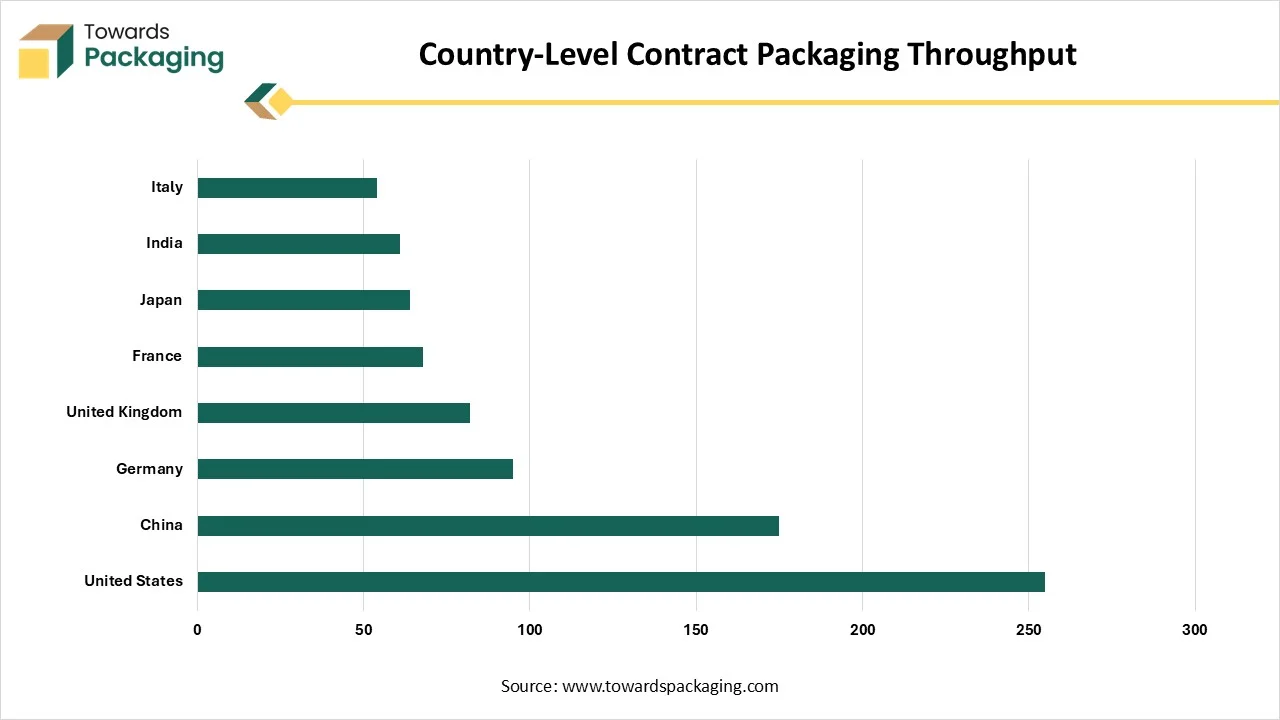

| Country | Annual Units Processed (Billion Units) |

| United States | 255 |

| China | 175 |

| Germany | 95 |

| United Kingdom | 82 |

| France | 68 |

| Japan | 64 |

| India | 61 |

| Italy | 54 |

By Service Type

By Packaging Material

By End-Use Industry

By Business Model

By Company Size

By Channel Type

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarContract Packaging and Fulfilment Services Market