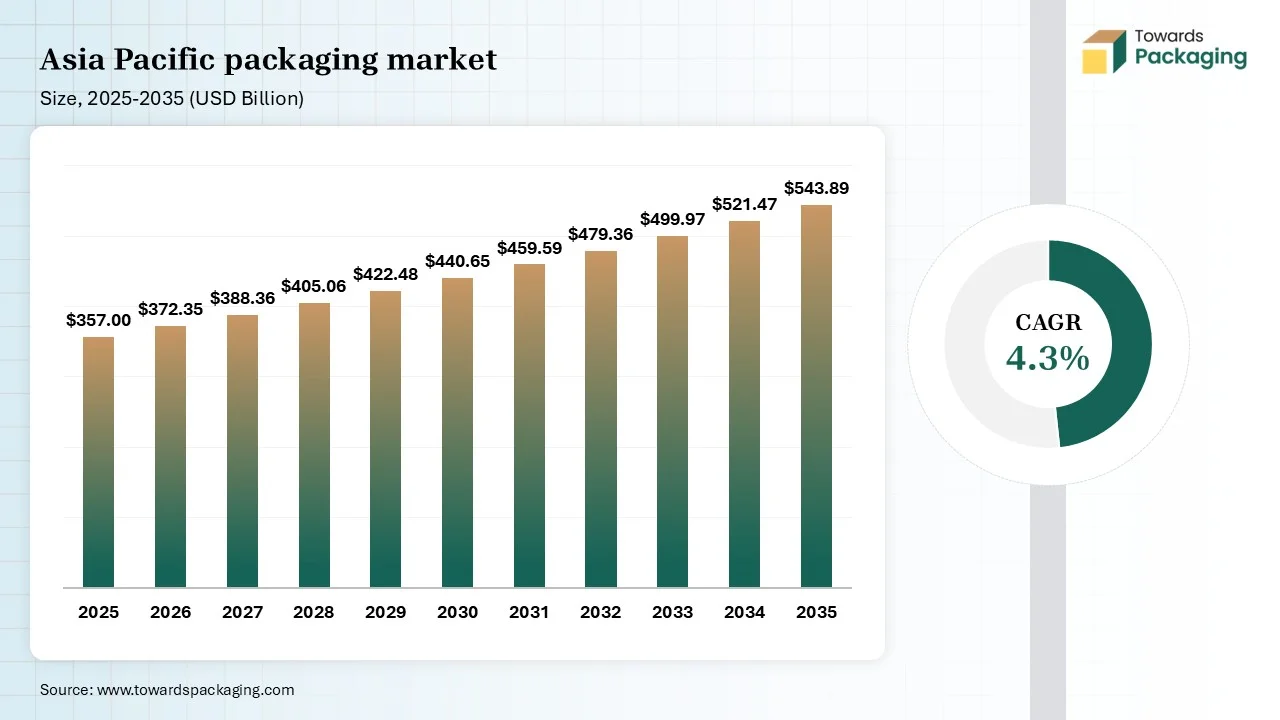

The Asia Pacific packaging market is forecasted to expand from USD 372.35 billion in 2026 to USD 543.89 billion by 2035, growing at a CAGR of 4.3% from 2026 to 2035. It covers extensive regional insights across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, supported by statistical data, market share analysis, and investment trends. The study includes a full competitive landscape of top packaging manufacturers, trade flow data, supply–demand patterns, and in-depth value chain analysis covering raw materials, converters, distributors, and brand owners.

The Asia Pacific packaging market encompasses the ecosystem of materials, technologies, and solutions used to enclose and protect products for distribution, storage, sale, and use across countries in Asia and Oceania. It includes rigid, flexible, and semi-rigid packaging used in industries such as food & beverage, personal care, pharmaceuticals, electronics, and retail.

In today's rapidly evolving technological landscape, AI integration holds great potential to reshape the landscape of the packaging industry by improving manufacturing efficiency, reducing material wastage, enhancing sustainability, and offering predictive analytics. AI plays a role in modernising packaging practices and enables companies to create innovative and efficient packaging solutions. AI technology in the packaging industry makes the process cost-effective, efficient, and faster. AI can effectively analyse large amounts of data to predict demand patterns, assisting packaging organizations to optimize production schedules and reduce excess inventory. AI-powered discovery assists businesses in adopting eco-friendly and sustainable packaging solutions without compromising performance.

Increasing Demand for Packaged Goods

The rising demand for packaged goods is expected to boost the growth of the Asia Pacific packaging market during the forecast period. Consumers are increasingly looking for ready-to-eat or easy-to-prepare food items, driven by rapid urbanization, changing lifestyles, and rising consumer preference for convenience. Packaging plays an integral role in protecting products from contamination, spoilage, and damage during handling, storage, and transportation, ensuring better product quality and safety. In addition, rising improvements in packaging technology to meet the evolving consumer preferences are likely to positively impact the market’s growth during the forecast period.

Rising Environmental Concerns

The growing environmental concerns, particularly single-use plastics, are anticipated to projected to hamper the market's growth. Several Governments in the Asia Pacific region are implementing stringent regulations to reduce environmental waste in response to public concerns about plastic packaging waste. The widespread use of non-recyclable and non-biodegradable packaging often contributes to pollution in landfills, oceans, and other ecosystems.

How is the Rising Awareness of Sustainability and Supportive Government Guidelines Offering Growth Opportunities to the Market?

The rising awareness of sustainability, along with the supportive government guidelines for eco-friendly packaging solutions, is projected to offer lucrative growth opportunities to the Asia Pacific packaging market in the coming years. The market is experiencing a growing preference for materials that are biodegradable, recyclable, and compostable. Several packaging companies operating in the Asia Pacific region are increasingly adopting sustainable practices in their packaging to meet the evolving consumer expectations and regulatory mandates. Moreover, favourable government regulations and policies, such as subsidies and tax breaks, encourage businesses to adopt eco-friendly packaging solutions to align with circular economy principles.

The blow moulding segment is expected to dominate the packaging market. Blow moulding is one of the integral manufacturing processes in the packaging industry. It finds applications in bottles, containers, drums, and other industrial parts. Blow moulding is most extensively used to create hollow plastic bottles and containers. Blow moulding mostly uses typical materials such as PP, HDPE, and LDPE. Blow moulding is widely adopted in the personal care industry for shampoo and conditioner bottles, jerry cans for the automotive industry, and others.

On the other hand, the digital printing & smart labelling segment is growing at the fastest CAGR, owing to the rising popularity of digital printing and smart labelling technologies in the packaging industry. Digital printing offers on-demand printing, increased efficiency, and customized packaging, catering to unique customer demand. In comparison with traditional printing methods, digital printing significantly reduces the production process and enables faster turnaround times. Smart labelling technologies such as RFID systems, QR or bar codes, and NFC tags, which enable real-time tracking of products throughout the supply chain, enhance product safety, consumer engagement, and prevent counterfeiting by incorporating unique identifiers.

The plastic packaging segment accounted for the highest revenue share in 2024, owing to its lightweight, durability, strength, and versatility. Plastic is cost-effective and can be easily molded into various sizes and shapes, making it an attractive option for various industries such as food, beverage, home care, pharmaceuticals, and personal care products, and others, to meet diverse product needs. Additionally, the increasing investment by prominent packaging companies to deliver innovative solutions for better plastic packaging is anticipated to propel the expansion of the segment during the forecast period.

On the other hand, the sustainable/biodegradable packaging segment is expected to grow at a significant rate, owing to the rising environmental concerns in Asia Pacific. Sustainable/biodegradable packaging focuses on the use of packaging solutions that are generally made from materials such as recyclable HDPE or PET plastics, cardboard, paper, and other renewable packaging materials. Sustainable packaging solutions have a minimal environmental impact through the use of recycled, bioplastics, or renewable resources. Bioplastic, particularly polylactic acid (PLA), offers a promising pathway as a sustainable alternative to conventional plastics owing to its biodegradability properties. In the packaging industry, sustainability efforts allow businesses to address several ongoing environmental challenges, which often include climate change, plastic pollution, and exhaustion of resources. Consumers are increasingly preferring biodegradable and sustainable packaging solutions and are even willing to more by replacing traditional fossil-based plastic packaging, which contributes to accumulating pollution levels, posing threats to both human health and ecosystems.

The flexible packaging dominated the packaging market in 2024, owing to the increasing demand for flexible packaging products across various industries such as the medical and pharmaceutical sectors, food and beverage, personal care, and others. Flexible packaging is generally made from easily yielding materials such as film, plastic, paper, and aluminum foil, which can be easily folded, shaped, and sealed to preserve and protect the integrity of the products. Flexible packaging is widely available in bags, pouches, sachets, and wraps, offering various benefits such as lightweight, versatility, cost-effectiveness, barrier properties, adaptability, durability, ease of use, and the ability to extend product shelf life.

On the other hand, the semi-rigid packaging segment is expected to grow at a notable rate during the forecast period. Semi-rigid packaging offers a perfect balance between flexibility and structure. Semi-rigid packaging solutions maintain their shape but can be bent or compressed under pressure. These packaging solutions are usually lightweight, affordable, and offer an aesthetic appeal, which provides a more refined look than flexible packaging. Semi-rigid packaging is ideal for various applications in pharmaceutical & medical, food, and consumer goods, which include clamshell containers, food trays, yogurt cups, and others. Additionally, the rising disposable incomes, changing lifestyles, and rapid rise of online shopping in countries like China, India, Japan, and other emerging nations in the Asia Pacific region result in spurring the demand for semi-rigid packaging that can withstand handling and shipping.

The food & beverage segment held a dominant presence in the packaging market in 2024, mainly driven by the rapid urbanization, changing lifestyle, increasing disposable incomes, and evolving consumer preferences, which further boost the segment’s growth during the forecast period. Consumers are increasingly preferring convenient packaging options for frozen and ready-to-eat foods and beverages. In addition, the increasing awareness of environmental sustainability and rising regulatory pressure is compelling the food & beverage industry to embrace eco-friendly packaging materials such as plant-based plastics, paper, paperboard, and recyclable materials.

On the other hand, the e-commerce & retail segment is expected to grow at a notable rate. The growth of the segment is driven by the rapid expansion of e-commerce & retail in countries like Japan, India, China, South Korea, and other Southeast Asia countries. Packaging plays a crucial role in offering secure and efficient product delivery, which ultimately enhances the consumer experience. Moreover, e-commerce platforms are increasingly focusing on improving the unboxing experience through customized packaging, which significantly fuels the segment’s growth. In the e-commerce & retail industry, the market has witnessed the increasing adoption of sustainable packaging solutions as an eco-friendly alternative to conventional fossil-based plastics for reducing the environmental carbon footprint.

China held the largest share of the Asia Pacific packaging market in 2024. China has a well-established packaging sector supporting food & beverage, pharmaceuticals & medical, electronics, cosmetics, and consumer goods industries, all are major users of packaging. China's high per capita income and evolving consumer preference for convenience drive the demand for packaged products, especially in retail, e-commerce, and food & beverage. The growth of the country is mainly attributed to the presence of prominent key players, the wide availability of packaging raw materials, rising consumer need for product protection and convenience, rapid advancements in recycling technologies, rapid urbanization, and increasing focus on sustainability.

The packaging industry in China is rapid shift toward biodegradable, recycled, and compostable materials, owing to the rise in regulatory pressures to combat greenhouse gas emissions and meet the consumer preference for sustainable packaging solutions, which is significantly bolstering the country’s market growth in the coming years. Additionally, the continuous research and development efforts by prominent packaging companies to improve packaging properties and expand their applications, making them more efficient, sustainable. And user-friendly packaging solutions.

On the other hand, India is anticipated to grow at the fastest rate in the market during the forecast period. The growth of the country is driven by the rising research and development efforts by key players to improve the properties of packaging, increasing consumer demand for robust protective and convenient packaging solutions, rapid advancements in packaging materials, rising population, increasing sustainability trends, and rising innovations with innovations in materials like air pillows and bubble wrap. The rise in disposable income, changing lifestyle, and rapid urbanization have significantly boosted the demand for packaged foods in the country.

The market is also experiencing an increasing need for robust protective packaging in various end-use industries, including food & beverage, pharmaceuticals, e-commerce, electronics, industrial goods, agriculture, automotive, and others, which is expected to fuel the packaging market’s growth in the country. The rising consumer preference for materials that are recycled, compostable, and biodegradable, fueled by the rising awareness of environmental sustainability. In response, packaging companies in India are increasingly adopting eco-friendly and sustainable packaging practices to meet consumer expectations and government sustainability initiatives, as well as align with circular economy principles.

According to the India Brand Equity Foundation, packaging is currently the fifth-largest sector of the Indian economy. Packaging is among the high-growth industries in India and is developing at the rate of 22 to 25% per annum, and is becoming a preferred hub for the packaging industry. According to current industry data, India has nearly 861 paper mills, 526 of which are operating, with a total installed capacity of 27.15 million tonnes. Almost 4,990 thousand tons of installed capacity are contained in the more than 900 paper units that make up the industry structure. India continues to lead the global paper market, with domestic consumption of packaging paper and paperboard growing at 8.2% in 2023-24. (Source:IBEF)

By Material Type

By Packaging Type

By Technology

By Application

By Country/Subregion

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarAsia Pacific Packaging Market