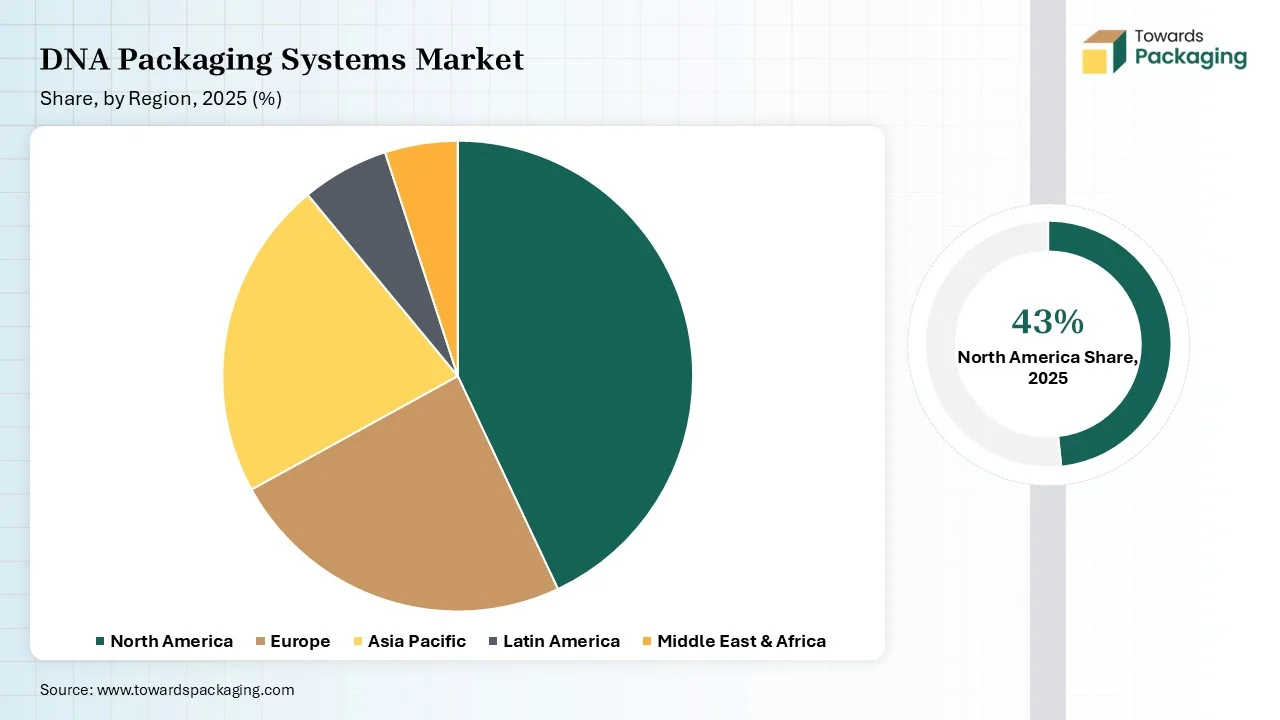

The DNA Packaging Systems market provides an in-depth evaluation of global market size, historical data, and 2025-2034 forecasts, covering all key segments such as viral vectors, non-viral delivery systems, DNA vaccines, gene therapy, and end-use industries. The study includes detailed regional analysis across North America (44% share in 2025), Europe, Asia Pacific (fastest CAGR -10%), Latin America, and MEA, examining demand shifts and growth patterns. It further delivers competitive profiling of Tier-1, Tier-2, and Tier-3 companies, trade flow assessments, manufacturing footprints, supplier mapping, and complete value chain analysis from raw material processing to distribution.

Growth is driven by expanding gene therapy pipelines, increasing adoption of DNA vaccines, advancements in synthetic biology, and demand for safe and scalable DNA delivery solutions.

The DNA packaging systems market refers to technologies and platforms designed for the efficient encapsulation, protection, and delivery of DNA molecules for research, therapeutic, or industrial applications. These systems are essential for gene therapy, vaccine development, molecular biology research, and synthetic biology, ensuring DNA stability, controlled release, and high transfection efficiency. The market includes viral and non-viral packaging technologies, lipid nanoparticles, polymeric systems, electroporation-based platforms, microfluidics, and other encapsulation technologies.

| Metric | Details |

| Market Drivers | Expanding gene therapy pipelines, DNA vaccine adoption, synthetic biology advancements, demand for safe & scalable DNA delivery solutions |

| Leading Region | North America |

| Market Segmentation | By Technology / Packaging Method, By Application, By End User and By Region |

| Top Key Players | Thermo Fisher Scientific, Lonza Group, Merck KGaA / MilliporeSigma, Sartorius AG, GE Healthcare Life Sciences, Catalent / Paragon Bioservices, WuXi AppTec, Charles River Labs, AGC Biologics, Fujifilm Diosynth, BioNTech, ElevateBio, Kite Pharma, Novartis, AstraZeneca |

The therapeutic methods accepted by current medicine concentrate on the early tracking and focused manipulation of disease-linked genes. Specifically for complicated diseases such as neurodegenerative diseases and cancer diseases like Alzheimer’s and chronic inflammations linked with aging, the issue is not just to track individual genes, but also to identify their regulatory networks. It is becoming increasingly clear that the three-dimensional company of DNA in the cell nucleus -known as chromatin -plays an important role. Also, the researchers can then accept an algorithm- a complex neural network, a design of an artificial intelligence expert in image processing -to track these designs. The AI developed an “eye” for the specific traces that are left by activity in the chromatin image.

Apart from this, the potential and capability of AI is to classify patterns, predict the results, and also speed up the research timelines, which are indeed proving to be a disruptor when it comes to particularly the areas of genomic research, drug discovery, and disease diagnosis.

Positive Developments Drive The DNA Packaging Systems Market

Histones are high in basic amino acids, particularly in arginine and lysine, both of which are positively charged. The purpose of this is that DNA is negatively charged because of phosphate groups in its backbone. The positive updates on the basic amino acids in histones enable them to bind tightly to the negatively charged DNA. This communication between the DNA and histones is important for several reasons. The heavy content of basic amino acids enables histones to securely bind to DNA, assisting it in coiling and bending into a more compact pattern. This method is important because it enables the long DNA molecules to fit into a small area of the cell nucleus. Without histones, DNA would be too heavy to be smoothly organized and stored.

Complex Nature Is The Drawback

Combining large gene fragments is fraught with complexities, which mainly develop the technical urges as compared to oligonucleotide synthesis. As the range of the DNA sequence grows, the error rate during the synthesis tends to rise. These faults can be imagined as insertions, substitutions, or deletions within the series that adjust the functionality of the outcome gene. Tracking the high fidelity across the grown DNA series is thus an important challenge. Also, the cost of synthesizing heavy genes can be excessively high due to the initial procedure and heavy purification steps needed.

Strong Protein Genes Are The Future Of The DNA Packaging Systems Market

Recombinant DNA stages generate an accurate genetic match to the proteins of a virus. The protein’s DNA will be integrated with DNA from a virus, which is harmless to human beings, and once it is injected, it will rapidly generate large quantities of antigen that boost the immune system to protect against the virus. Important vectors are machines that are prevalently used to introduce genetic materials into cells. A viral vector vaccine gives a statement of pathogen proteins without host cells, similar to other attenuated vaccines. Hence, since popular viral vector vaccines have only a small fraction of pathogen genes, which are much less likely to be infected and safer, it is impossible for the pathogen to be transmitted.

")

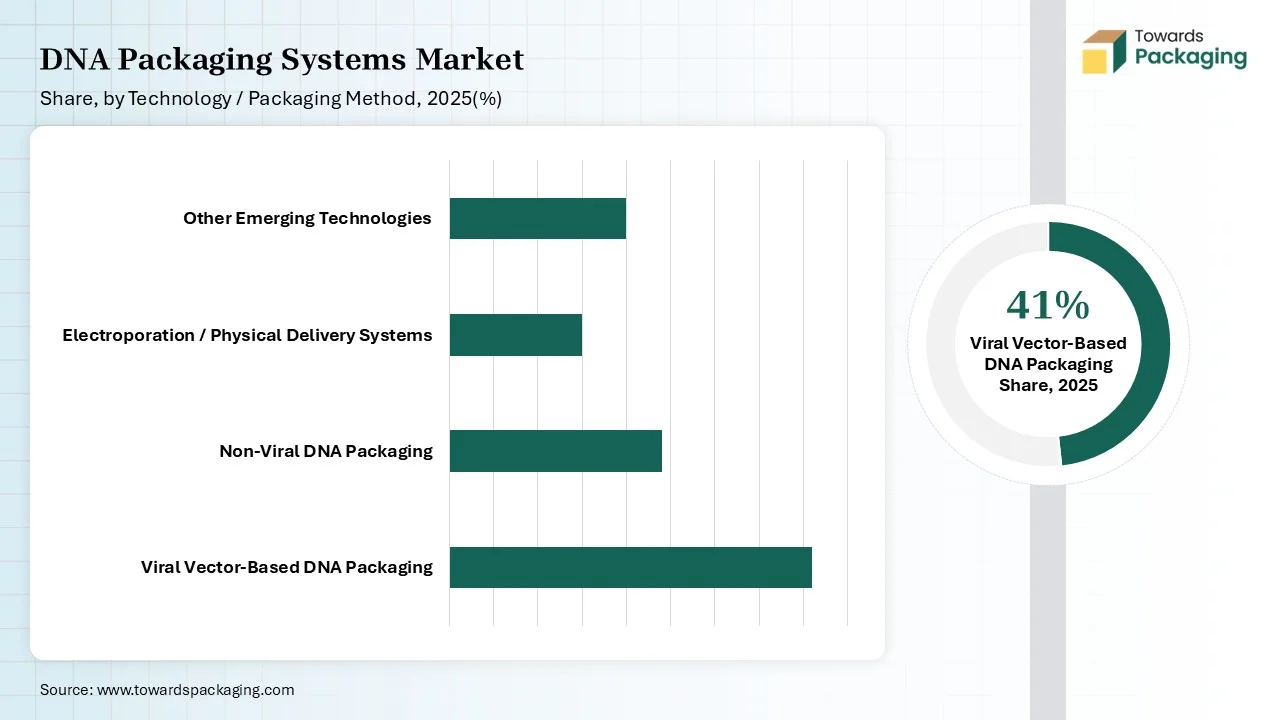

The viral vector-based DNA packaging segment dominated the market with approximately 42% share in 2025, as viral vectors are a well-known research tool in terms of biological sciences and other fields. They are personalized, enabling research with various genes of interest in a variety of in vitro and in vivo uses. Adeno-associated virus was primarily explored as a pollutant in adenovirus cultures, classified by a non-enveloped pattern and single-stranded DNA cargo, which is distinct from adenovirus, having double-stranded DNA. Also, Lentiviral vectors that come from lentiviruses, a subclass of retroviruses, are derived from the human immunodeficiency virus (HIV), which is most well-known.

Apart from this, adenoviruses cause infections in several organs, including the intestines and lungs. And retroviral vectors are made by removing famous genes from retroviruses and inserting a therapeutic gene.

The non-viral DNA Packaging segment is expected to grow at the fastest CAGR of approximately 30% during the forecast period. Non-viral vectors are artificially created to serve the main gene expression without inducing unnecessary inflammatory and immune reactions. These types of vectors are initially developed via physical and chemical procedures. Physical procedures count electroporation, microinjection, needle injection, and gene gun, while the chemical methods include inorganic materials, lipid-dependent systems, and polymers too. Scientists utilise the jet injection procedure in several gene therapy uses, including the growth of genetic vaccines and focusing on suicide genes to market antitumour therapy. This procedure has been utilised for the treatment of several sinus diseases.

The gene therapy segments dominated the market with approximately 45% share in 2025, as gene therapy is a kind of treatment for genetic disorders. It is occupied by either changing a disease-generating gene or providing you with a working copy of that gene. Genes are directions for creating proteins, which assist our body's work. The normal gene is utilised to substitute the pathogenic gene in situ, so that the DNA in the cell is overall stored again to normal. Gene augmentation therapy is utilised to diagnose diseases caused by loss-of-function mutations, which prevent the gene from generating a functional product.

This type of gene therapy procedure introduces DNA containing a regular version of the lost gene into the cell, and the goal is to generate a functioning product at smooth levels to substitute the protein that was originally missing.

The DNA Vaccines segment is expected to grow at the fastest CAGR of approximately 25% during the forecast period. Relying on the nature of the vaccines, the following production steps are relevant, such as Immunization that has the complete microbe in an attenuated way. An “ATTENUATED” design is when the microbe is being managed to make it less aggressive, such as by lowering its potential to multiply. It is the most proficient method, but also the one that needs the most care. Attenuated live vaccines copy natural immunity and are a catalyst for long-term immune feedback. After one or two doses, there is no demand for a booster vaccination.

")

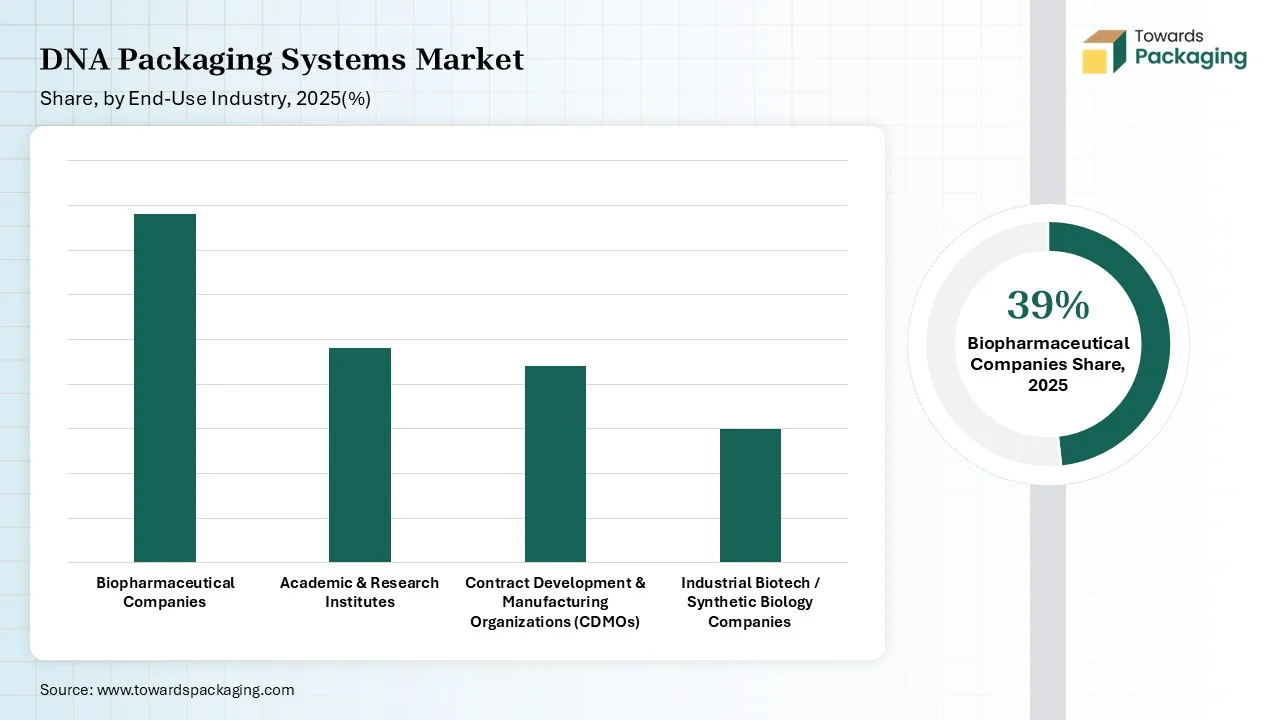

The biopharmaceutical companies' segments dominated the market with approximately 40% share in 2025. As the biopharmaceutical industry is loyal to developing and saving lives, the complete effect of pharmaceutical production practices on the health of our people and planet has only received reliable attention in recent years. The manufacturing of both large and small molecule drugs is highly energy-oriented, specifically involving substantial water use, generating considerable waste and toxic chemicals. Also, environmental issues arise from packaging, the disposal of medical waste, distribution practices, and unused medications.

There are many capable alteration procedures for generating DNA, which are perfect for use as a complicated material in high-level therapy manufacturing.

The academic and research institutes segment is expected to grow at the fastest rate during the forecast period at a CAGR of 25%. Researchers and academic institutes need DNA packaging solutions in order to fit huge amounts of DNA into small cell nuclei, protect the physical damage and degradation, and manage gene expressions by managing access to DNA. Packaging is also important for precisely classifying DNA during cell division, making sure that the genetic material is correctly distributed by cell division and daughter cells. The program of DNA packaging classifies which genes are useful for the purpose of transcription. Firmly packed regions are usually silent, while more accessible areas are potential, enabling fine-tuning of gene expression.

")

North America dominated the market with 44% share in 2025, as the procedure begins with classifying the gene that codes for the wanted protein, the gene of interest. This can be completed through different techniques such as DNA, PCR Sequencing, or gene synthesis, for which demand is very high in the North American region. The expression vector is established into the host organism ( insect, yeast, bacterial, algal, cell-free, or mammalian cells ) with the assistance of transformation for yeast and bacteria or transfection for mammalian cells. Vector building includes designing and putting a DNA Molecule that carries the gene encoding the protein of commercial interest, along with regulatory elements, which is compulsory for protein expression. The host cells are well polished under updated conditions, such as pH, temperature, inducer formulation, and developed media, enabling them to develop and express the target protein.

Asia Pacific is expected to grow at the fastest CAGR of 10% during the forecast period. The Asia Pacific region is being classified by rising healthcare infrastructure, research and development activities, and growing investments in biotechnology. Countries like Japan, China, India, Australia, and South Korea are making the main investments in regional market development. The region shows rigid capabilities for market expansion, which is driven by growing acceptance of molecular diagnostics, which fully concentrates on tailored medicines, and developing healthcare expenditure.

The urge for “ DNA Packaging” in India initially points to the industry for biological and industrial packaging materials, as well as the rising demand for the DNA production and DNA sequencing industry. While the DNA production is witnessing rigid development, driven by clinical trials and research, the urge for physical packaging is huge, wrapping sectors like electronics, food, pharmaceutical, and aviation with packaging organisations serving solutions for different industrial demands, including moving specialized and supplies boxes.

There are some government-initiated programs under various departments for various aims. These programs not only achieve their own aim but also quietly develop India’s DNA Health and Overall wellness.

Tier 1

Tier 2

Tier 3

By Technology / Packaging Method

By Application

By End User

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarDNA Packaging Systems Market