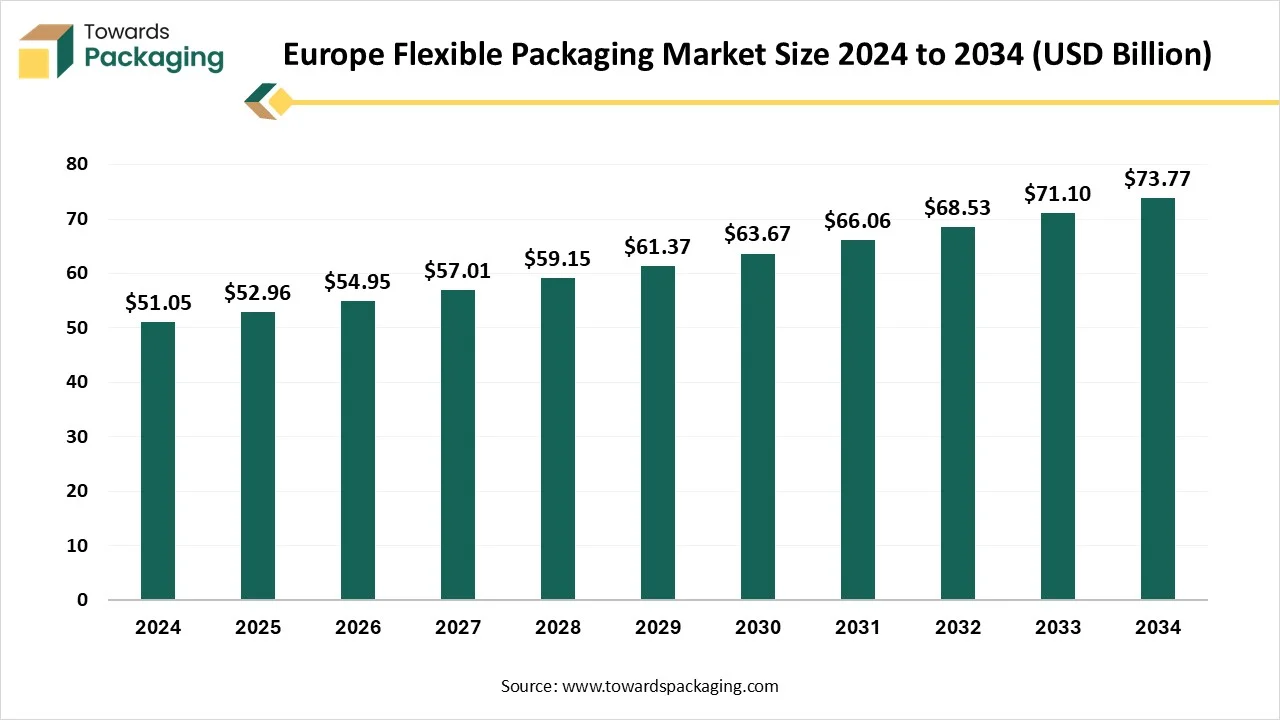

The Europe flexible packaging market is projected to reach USD 76.54 billion by 2035, growing from USD 54.95 billion in 2026, at a CAGR of 3.75% during the forecast period from 2026 to 2035. Key segments include plastics (50% market share in 2025), pouches & bags (40% share), and food & beverages (55% share). Leading companies such as Amcor plc, Mondi Group, and Huhtamaki Oyj dominate the market, with Germany, the UK, and France being the primary consumers. The market is characterized by innovations in biodegradable materials and smart packaging technologies.

Europe flexible packaging market is experiencing steady growth, motivated by the growing need for lightweight and environmentally friendly packaging options. Flexible packaging is becoming increasingly popular due to rising consumption in the food, beverage, and pharmaceutical industries. Innovations in eco-friendly substitutes and materials are also facilitating market growth throughout the region.

Europe’s flexible packaging market is being shaped by stringent sustainability regulations that force businesses to use materials that are recyclable, reusable, or compostable. Traditional multilayer formats are becoming less viable due to regulations like mandatory recycled content, EPR fees, and prohibitions on plastics that are hard to recycle. Brands are consequently moving toward low-carbon designs mono mono-material structures, and packaging that can amply demonstrate recyclability and environmental performance.

At the same time, there is a growing data approach to compliance requirements. Businesses are required to offer carbon reporting, traceability, and verified sustainability claims, which promotes the use of eco certifications, digital labeling, and open supply chain procedures. In general, packaging manufacturers are being forced to innovate swiftly while controlling costs as sustainability in Europe shifts from voluntary pledges to mandated standards.

| Metric | Details |

| Market Size in 2025 | USD 52.96 Billion |

| Projected Market Size in 2035 | USD 76.54 Billion |

| CAGR (2026 - 2035) | 3.75% |

| Market Segmentation | By Material Type, By Packaging Type, By Application, By End-User Industry, By Distribution Channel and By Region |

| Top Key Players | Amcor plc, Mondi Group, Constantia Flexibles, Huhtamaki Oyj, DS Smith Plc |

Rising Focus on Sustainability and Recyclability

To reduce packaging waste and increase recycling rates Europe governments are enforcing stricter regulations, which are forcing companies to rethink their packaging designs. Additionally, consumers are actively selecting products with eco-friendly packaging, hastening the transition to adaptable recyclable solutions.

Shift toward convenient and lightweight packaging formats

Easy-to-handle single-serve and resealable packaging is becoming increasingly popular due to urban lifestyles and smaller households. Additionally, flexible packs help brands draw customers in cutthroat retail settings by improving shelf visibility and product differentiation.

Rapid growth of e-commerce and organized retail

By decreasing shipping weight and material consumption, flexible packaging promotes effective logistics because of its adaptability and durability. It can be used to protect goods during last-mile delivery and long-distance shipping.

Cost efficiency compared to rigid packaging

Manufacturers can keep operating costs under control by using fewer materials and having less storage space. In addition to lowering fuel consumption and carbon emissions, reducing transportation weight also enhances supply chain efficiency.

Advancements in packaging materials and printing technologies

The creation of high-performance films and nonmaterial structures increases recyclability without sacrificing protection. More customization, shorter production runs, and improved branding are all made possible by advanced printing techniques.

Government Initiatives

| Company | Ticker / Exchange | Country | Market Cap | P/E Ratio | Price-to-Sales (P/S) | EV / EBITDA | Dividend Yield | Revenue (Last FY) | EBITDA (Last FY) | Employees |

| Huhtamäki Oyj | OMXHEX: HUH1V | Finland | €3.0 B | 14.2× | 0.76× | 8.18× | 3.65% | €4.8 B | €587 M | 17,790 |

| Mondi plc | LSE: MNDI | United Kingdom | £3.6 B | 12.8× | 0.80× | 7.80× | 5.00 % (2024) | £6.14 B | £880.94 M | 22,000 |

| Amcor plc | NYSE: AMCR / ASX: AMC | Switzerland / Australia | USD 19 B | 21.3× | 1.07× | 10.5× | 4.60% | USD 14.7 B | USD 1.40 B | 44,000 |

| Ergis S.A. | GPW: ERG | Poland | PLN 160 M (≈ €33 M) | 11.5× | 0.41× | 13.20× | 1.20% | PLN 320 M | PLN 24 M | 128 |

| UPM-Kymmene Oyj | OMXHEX: UPM | Finland | €11.5 B | 16.7× | 0.73× | 8.40× | 4.30% | €10.48 B | €1.25 B | 16,500 |

| Smurfit Kappa Group plc | Euronext Dublin: SKG / LSE: SKG | Ireland | €11.8 B | 14.9× | 0.85× | 6.9× | 3.10% | €12.85 B | €1.86 B | 47,000 |

| DS Smith plc | LSE: SMDS | United Kingdom | £7.2 B | 13.1× | 0.70× | 7.25× | 4.90% | £8.22 B | £1.08 B | 30,000 |

The PPWR is officially applicable to all packaging that is kept in the EU industry; instead, they are supplied, produced, and sold from outside the EU, and the packaging waste is generated in the EU. The regime, which has imposed restrictions on producers, importers, suppliers, and distributors, has checked representatives and completeness service providers.

Every packaging, regardless of the number of exemptions, has to be crafted for recyclability and align with defined recyclability performance criteria. We can implement acts that are needed to be accepted by 1 January 2028.

Businesses are adopting eco-friendly packaging because of stricter EU regulations on single-use plastics and growing consumer preference for sustainable products. Manufacturers now have the chance to experiment with plant-based substitutes, recycled materials, and compostable films.

Although there is a growing need for environmentally friendly packaging, multi-layer flexible packaging is still challenging to recycle effectively. Eco-friendly packaging solutions are not widely adopted due to a lack of infrastructure and high sorting costs. Furthermore, regional variations in consumer awareness and recycling program participation continue to undermine overall efficacy.

")

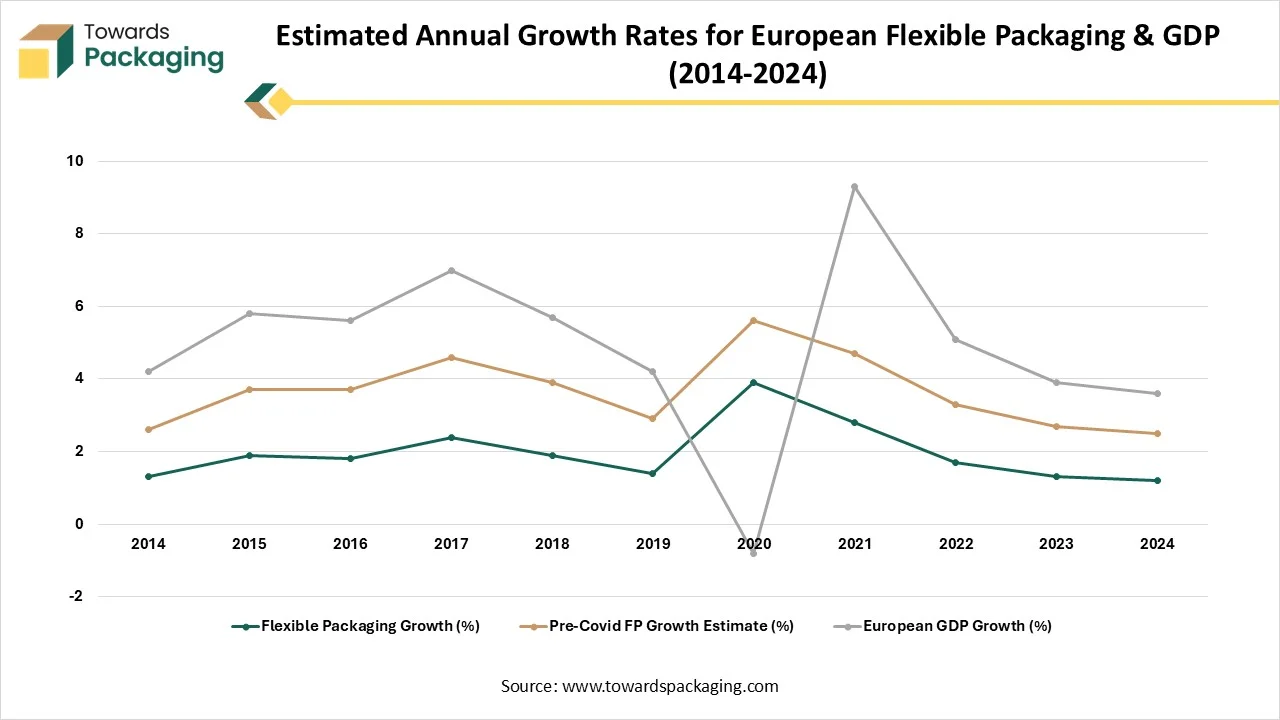

| Year | Flexible Packaging Growth (%) | Pre-Covid FP Growth Estimate (%) | European GDP Growth (%) |

| 2014 | 1.3 | 1.3 | 1.6 |

| 2015 | 1.9 | 1.8 | 2.1 |

| 2016 | 1.8 | 1.9 | 1.9 |

| 2017 | 2.4 | 2.2 | 2.4 |

| 2018 | 1.9 | 2 | 1.8 |

| 2019 | 1.4 | 1.5 | 1.3 |

| 2020 | 3.9 | 1.7 | -6.4 |

| 2021 | 2.8 | 1.9 | 4.6 |

| 2022 | 1.7 | 1.6 | 1.8 |

| 2023 | 1.3 | 1.4 | 1.2 |

| 2024 | 1.2 | 1.3 | 1.1 |

The data compares the annual growth of Europe’s flexible packaging sector with overall GDP performance from 2014 to 2025. Flexible packaging growth remained stable between 1-2.5% before Covid-19, while GDP followed a similar but slightly more volatile trend. In 2020, the pandemic caused a steep drop in GDP, contrasted by a sharp rise in flexible packaging demand driven by increased food, medical, and e-commerce consumption. Growth levels normalize after 2021, returning to steady, moderate rates through 2025.

The plastics segment dominated the Europe flexible packaging market with a 50% share in 2025 because it is affordable, long-lasting, and adaptable. Plastics are the most popular material for packaging in the food, beverage, and pharmaceutical industries because of their strong barrier qualities, lightweight nature, and compatibility with a variety of products.

The biodegradable/compostable materials are expected to be the fastest-growing in the market during the forecast period, driven by tighter EU sustainability regulations and growing consumer awareness. The region's drive for eco-friendly substitutes and circular economy objectives is reflected in the growing use of bio-based polymers and compostable films.

The pouches & bags segment dominated the Europe flexible packaging market with approximately 40% share in 2025, because they are widely used in food and household products and are convenient and affordable. They appeal greatly to both manufacturers and consumers due to their resealable, lightweight, and portable qualities.

The stand-up pouches segment is predicted to be the fastest growing in the market during the forecast period. They blend robust functionality with shelf appeal because they use less material than rigid packaging alternatives. These pouches promote longer shelf life, take up less room, and support sustainability goals.

")

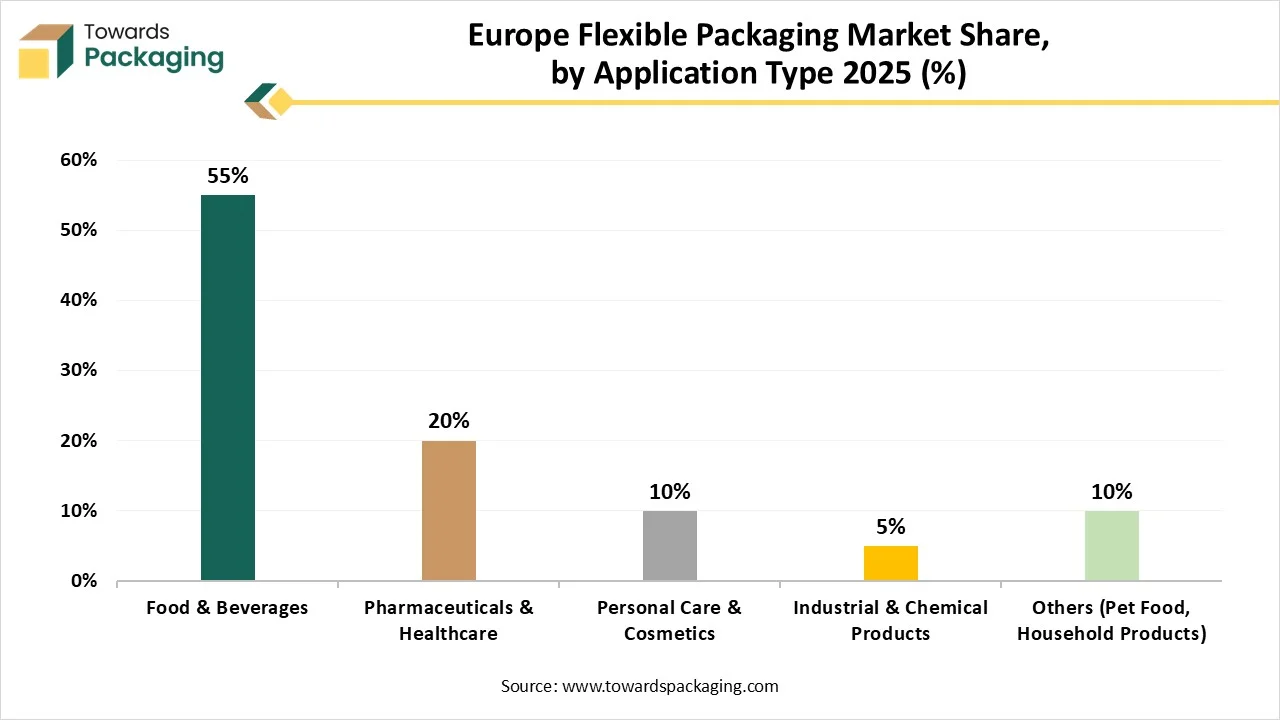

The food & beverages segment has dominated the market with approximately 55% share in 2025, for perishable goods, since flexible packaging guarantees longer freshness, portability, and cost effectiveness. Its widespread adoption has been further fueled by the growing demand for packages and ready-to-eat foods.

The pharmaceuticals & healthcare is predicted to be the fastest growing in the market during the forecast period because of an increasing demand for packaging that is safe tamper tamper-evident, and protective encourages adoption. The region's safe distribution and storage are supported by the growing use of medical pouches, sachets, and blister packs.

The food processing & beverages segment has dominated the market with approximately 60% share in 2025, bolstered by the strong demand for flexible packaging in the dairy, pastry snack, and beverage industries because of its low cost, long shelf life, and ability to accommodate a range of product-sized manufacturers favor flexible packaging.

The cosmetics & personal care segment is predicted to be the fastest growing segment in the market during the forecast period because, to meet sustainability goals, brands are using flexible packaging formats such as refill packs, sachets, and pouches. This trend is being driven by the consumer's growing desire for packaging that is convenient, environmentally friendly, and portable.

The distributors & dealers segment dominated the market with approximately 50% in 2025 because they serve as the main conduit between producers and consumers, guaranteeing supply across the retail and industrial sectors. Their well-established networks facilitate quicker distribution throughout several areas.

The online platforms segment is predicted to be the fastest in the market during the forecast period because of the growth of direct-to-consumer and e-commerce brands. Flexible packaging is perfect for online delivery due to its durability and light weight, which is further reinforced by consumers increasing desire for easy doorstep shopping.

")

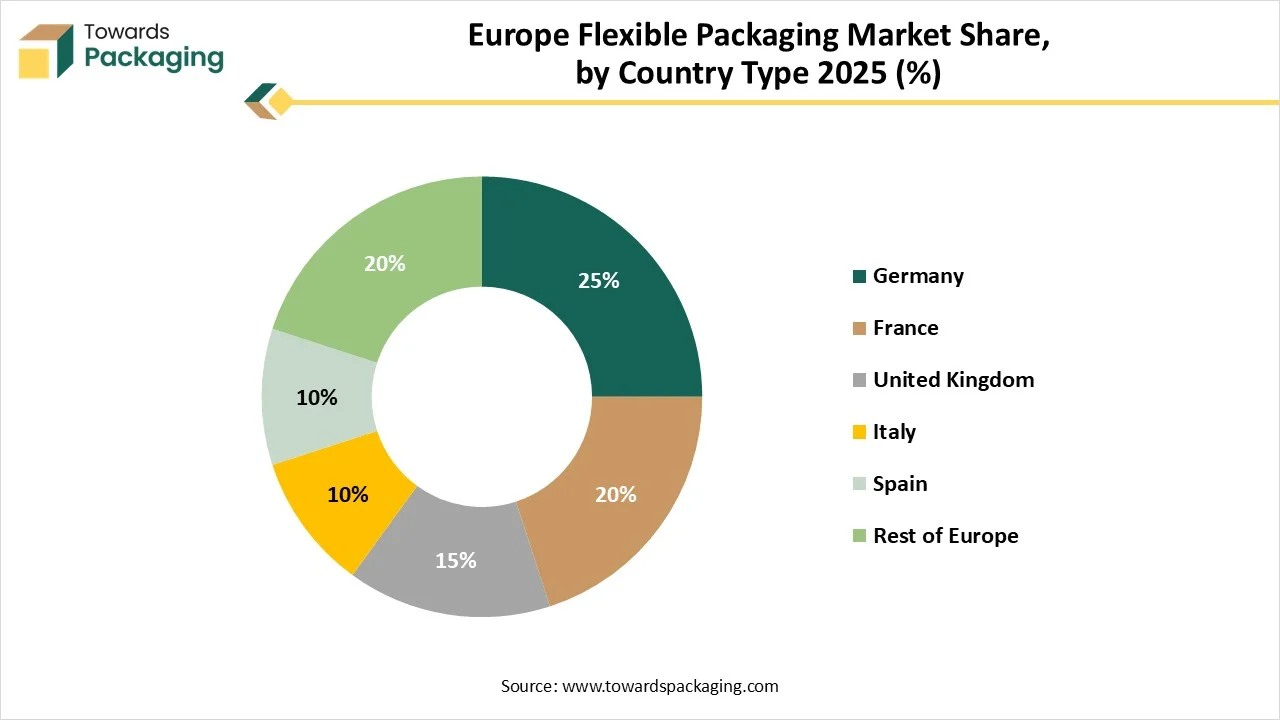

The French flexible packaging sector is witnessing constant growth in 2050, which is being assisted by strong government policies, growing consumer demand, and the development of technology acceptance. Regional trends have featured in developed funding across main urban hubs such as Lyon, Paris, and Marsvield during the period of market expansion and innovation. With a developing center on sustainability, compliance with EU regulatory requirements, the sector is maintained for long-term relevance. Industry size continues to stretch, which is being driven by both domestic usage and export capability. Foretell suggests constant growth possibilities, which makes France a strategic center for organisations finding invention, sustainable development, and competitiveness in the Flexible Packaging industry.

Trend of Italy Flexible Packaging: Italy’s packaging industry is witnessing a major move towards sustainability that is being driven by both regulatory pressure and consumer expectations. Environmental issues are at the top of mind for 79% of the Italian users while buying food products, which predicts 73% sustainable packaging for the healthy foods. The Italian government and the EU have used rigid controls on the packaging materials that encourage greater recyclability and lower plastic usage.

The Europe flexible packaging market is witnessing robust growth, encouraged by growing industry demand for lightweight, sustainable solutions. Businesses are being pushed to use recyclable, biodegradable, and compostable materials by the region's stringent environmental laws and strong emphasis on circular economy principles. The demand for creative and long-lasting flexible formats is rising due to the expansion of e-commerce.

Germany dominates the European flexible packaging market, enjoying the benefits of a robust industrial base and high packaged food and beverage consumption. Due to strict national recycling regulations and consumer demand for sustainable goods, the nation has taken the initiative to implement eco-friendly packaging solutions. A major exporter of flexible packaging materials to other European countries.

The UK flexible packaging market continues to expand, largely bolstered by expansion in the food processing sector, retail, and internet shopping. The market is changing due to growing consumer demand for easy-to-use and recyclable packaging options, and businesses are being pushed by regulations to reduce plastic waste to use recyclable and biodegradable alternatives.

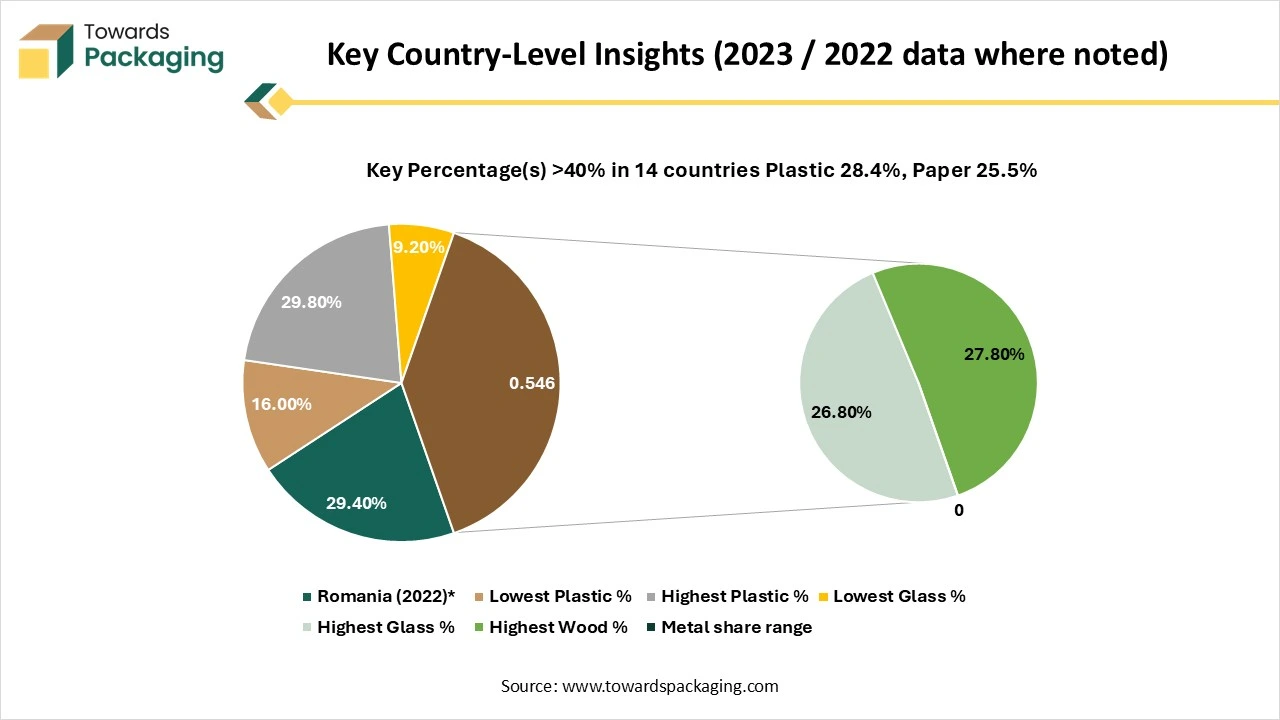

In 2023, the European Union generated 79.7 million tonnes of packaging waste. The majority came from paper and cardboard, which accounted for over 40% of the total. Plastics and glass also contributed significantly, making up 19.8% and 18.8%, respectively. Wood represented about 15.8%, while metals and other materials formed only a small portion.

")

Across most EU countries, the distribution by material was similar to the EU average. Paper and cardboard were the largest source of packaging waste in 26 out of 27 countries, with Bulgaria being an exception, where plastic waste was slightly higher. Plastic waste contributed as little as 16% in Luxembourg and nearly 30% in Ireland. Glass packaging waste varied widely—from 9.2% in Finland to 26.8% in Croatia. Metal waste was generally low everywhere, remaining below 10% in all nations.

| Product/Application Segment | Share of PE Flexible Films (%) | Approx. Volume (Mt) |

| Non-Food Packaging Films | 41% | 3.48 – 3.69 |

| Food Packaging | 23% | 1.96 – 2.07 |

| Bags & Sacks | 22% | 1.87 – 1.98 |

| Agricultural Films | 7% | 0.60 – 0.63 |

| Building & Construction Films | 2% | 0.17 – 0.18 |

| Other | 5% | 0.42 – 0.45 |

| Total | 100% | 8.50 – 9.00 Mt |

| Sub-Category | Share % | Approx. Volume (Mt) |

| Stretch Film | 18% | 1.53 – 1.62 |

| Shrink Film | 14% | 1.19 – 1.26 |

| Film on Reel | 9% | 0.77 – 0.81 |

| Product Category | EU28 Trade Status | Quantity | Value Impact |

| LLDPE (Primary form) | Net Importer | +720 Kt imports | Negative trade balance |

| LDPE (Primary form) | Net Exporter | +330 Kt exports | Positive impact |

| Combined LDPE/LLDPE | Net Importer | - | –€200M |

| Film & Sheet | Net Exporter | - | +€950M |

| Sacks & Bags | Net Importer | - | –€700M |

| Major sources/destinations | Imports: Saudi Arabia | Exports: China, Turkey | - |

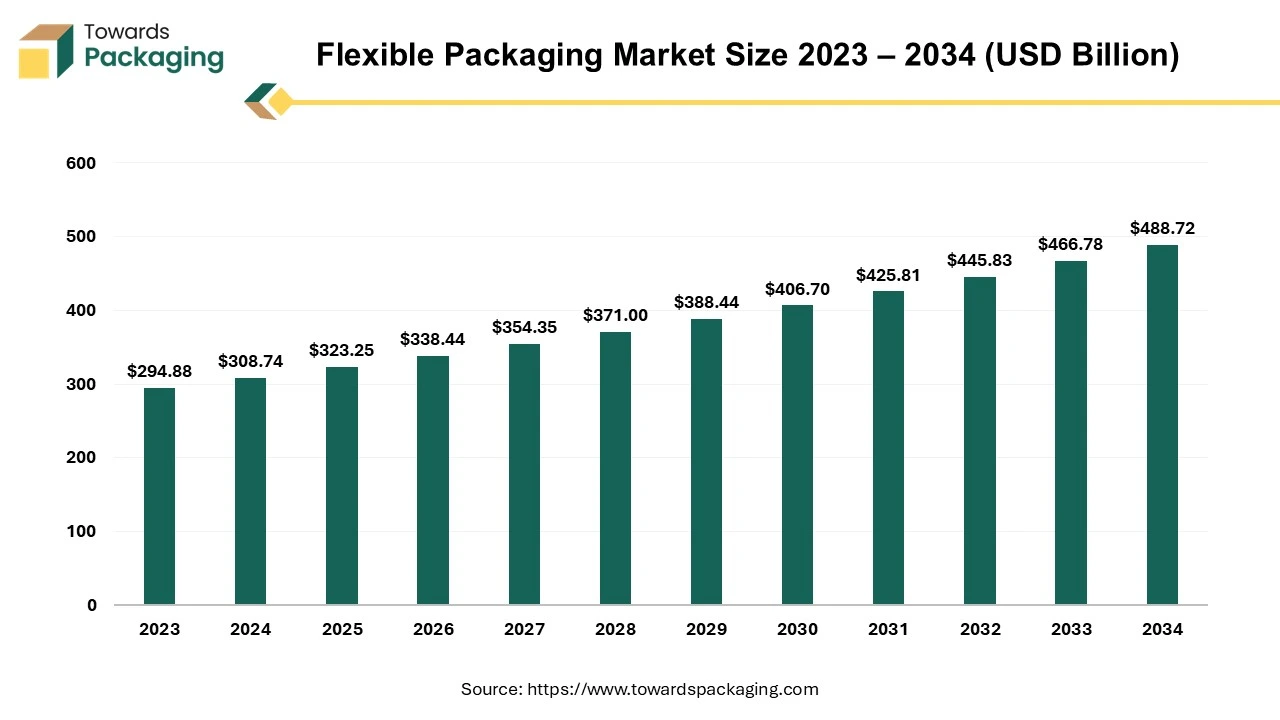

The flexible packaging market is set to grow from USD 323.25 billion in 2025 to USD 488.72 billion by 2034, driven by convenience-seeking consumers and regulatory demands for eco-friendly solutions. This report explores key market drivers, including innovations in technology, AI integration, and the growing adoption of sustainable materials across industries like food & beverages, pharmaceuticals, and personal care. The shift in consumer behavior toward convenience, coupled with regulatory pressure for eco-friendly solutions, has accelerated market adoption across industries.

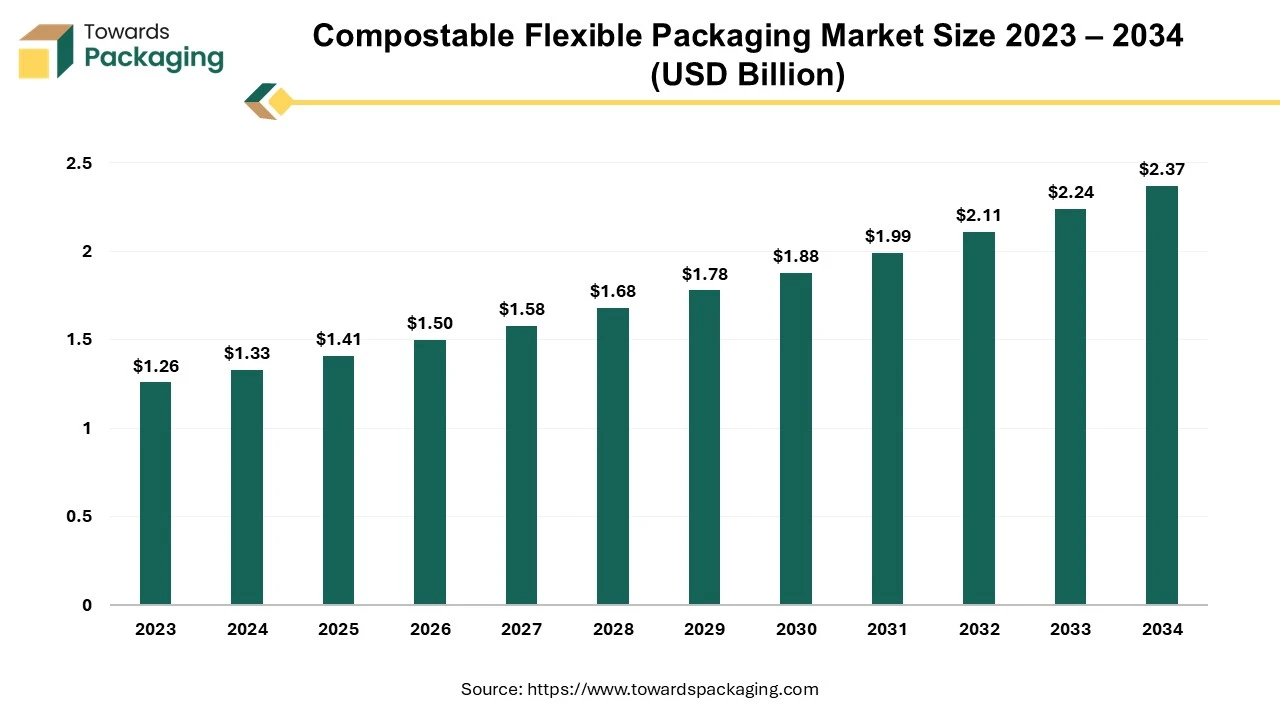

The compostable flexible packaging market is projected to grow from USD 1.41 billion in 2025 to USD 2.37 billion by 2035, at a CAGR of 5.9%. This market includes various biodegradable materials such as PLA, PBAT, and PHA, with North America, Europe, and Asia Pacific leading the charge. The report provides detailed data on market segments, including bioplastics, end-use sectors like food & beverage, pharmaceuticals, and industrial applications. In-depth regional performance analysis is also covered, along with key trends driving the market forward.

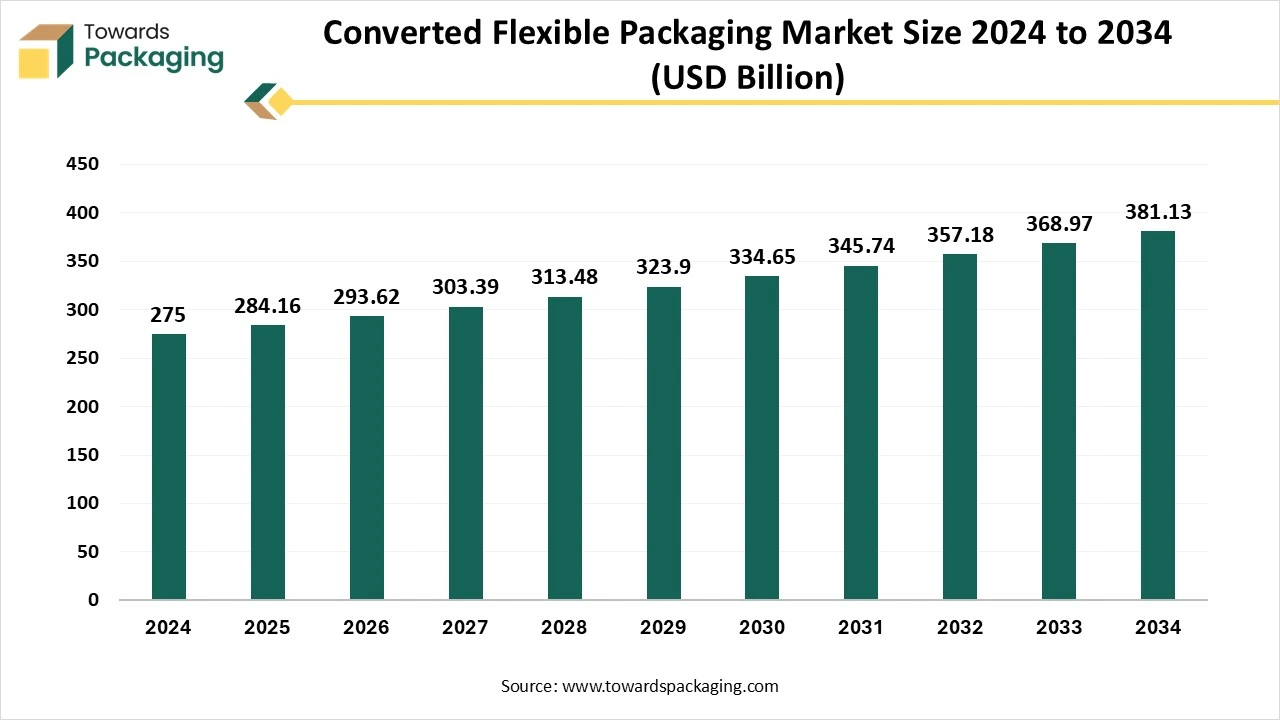

The global converted flexible packaging market is expected to increase from USD 284.16 billion in 2025 to USD 381.13 billion by 2034, growing at a CAGR of 3.33% throughout the forecast period from 2025 to 2034. The increasing focus on sustainability and the rising consumer preference for convenient and portable packaging options.

Tier 1

Tier 2

By Material Type

By Packaging Type

By Application

By End-User Industry

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarEurope Flexible Packaging Market