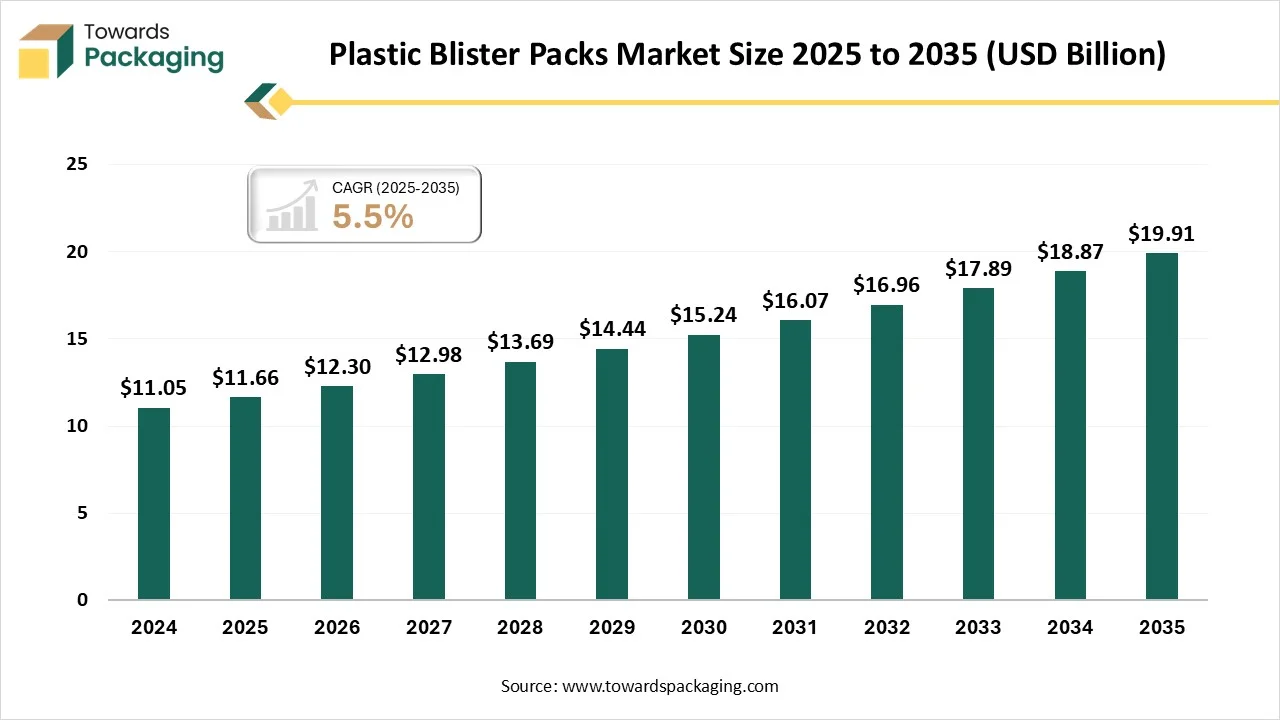

The plastic blister packs market is projected to grow from USD 12.30 billion in 2026 to USD 19.91 billion by 2035, expanding at a CAGR of 5.5% during the forecast period from 2026 to 2035. The report provides detailed insights including market size, segment data, regional analysis, company profiles, competitive landscape, value chain analysis, trade data, and manufacturers and suppliers data. The market growth is mainly supported by increasing demand for cost-effective, tamper-evident packaging solutions, particularly in the healthcare and pharmaceutical sectors where protection from contamination, moisture, and gases is essential.

Plastic blister packs are a type of pre-formed packaging that consists of a plastic cavity, or "blister," sealed to a helpful resource such as aluminum foil or cardboard. It is widely used to protect and package small goods, such as pharmaceuticals (capsules and tablets) and consumer products (toys, batteries, and electronics). The plastic hollow is naturally twisted over thermoforming, and the sealed pack shields the goods from tampering, moisture, and contamination.

Technological transformation in plastic blister packs includes smarter, more customer-friendly designs, the integration of smart technology, improved sustainability, and more efficient production processes. Inventions focus on services like peel-off and easy-open patterns for approachability, smart packaging with QR codes or NFC for patient and tracking data, and the growth of recyclable mono-material packs to decrease ecological impact. Advanced equipment utilizes a precise heat switch to avoid inferior-quality and ensure superior-quality packing.

Across HS-proxy data and trade dashboards, the most visible exporter origins for plastic blister items and related converted packaging are:

The major raw materials utilized in this market are polyvinylidene chloride (PVDC), cyclic olefin polymers (COP), and polyester (PET).

The component manufacturing in this market comprises forming film, lidding, printing, and heat-seal coating.

This segment is growing focus on direct sales to end-user industries and specialized transport.

The carded blister packs (blister + card) segment dominated the market with the highest share in 2025, driven by its branding opportunities, suitability, and cost-effectiveness. This type of packaging is favoured for its ability to shield goods, clearly display branding, and improve shelf management, which has led to its robust market presence in sectors such as pharmaceuticals and consumer goods. This packaging arrangement is an inexpensive option for producers, with broad applicability across many product types. The cardboard back offers ample space for printing branding, supervisory information, and marketing messages, making it effective for customer engagement. Carded blister packs (blister + card) can be arranged in several sizes and shapes to accommodate various goods, from small pharmaceutical to electronics products.

The strip/cavity blister pack segment is expected to grow at the fastest CAGR during the forecast period of 2025 to 2034. This segment is growing due to better protection and ecological factors. These are mainly for smaller products; cavity packs are highly popular for their ability to provide better protection against environmental factors such as light and moisture, which is important for enhancing shelf life and ensuring patient safety. These are used for single-dose capsules, tablets, and suppositories, offering a protective, tamper-resistant, and often child-resistant container.

The wallet blister packs are the fastest-growing in the plastic blister packs market, as they offer convenience and portability. An increasing demand for patient-safety packaging, which wallet blister packs offer by being tamper-resistant and protecting against contamination. The design emphasizes the portability and convenience of use for over-the-counter supplements and drugs. This segment is observing progress in technology, with new biodegradable resources and incorporated processes being developed. The increase in specialty drugs and biologics, which require high-perceptibility and tamper-proof packaging, is influencing development.

| End-Use Industry Segments | Market Share 2025 (%) |

| Pharmaceuticals & Healthcare | 50% |

| Food & Beverages (Portion Packs, Snacks, etc.) | 15% |

| Consumer Electronics & Household Goods | 15% |

| Industrial / Automotive / Other Specialty Uses | 10% |

| Personal Care / Cosmetics | 10% |

The pharmaceuticals & healthcare segment dominated the market in 2025, with the highest share, driven by tamper-evident, safe, and hygienic packaging. These packs protect medications from environmental factors such as oxygen and moisture, helping maintain their efficiency and shelf life. The pre-portioned properties of blister packs help ensure precise dosing and can enhance patient adherence to handling plans. These packages are a cost-effective option for huge-volume goods, making them a prevalent choice for several pharmaceutical industries. The pharmaceutical sector needs packaging that meets stringent regulatory requirements. These packs are designed to be chemically compliant and inert with these requirements.

The consumer electronics & household goods segment is expected to grow at the fastest CAGR during the forecast period of 2025 to 2034. This segment is growing due to tamper-evident, visibility, and product protection. These packs and clamshells are widely used for a range of electronic products, including smaller gadgets, headphones, and cables. The segment is influenced by the need for durable, tamper-proof packaging to protect fragile or high-value products during transportation and storage, particularly with the growth of the e-commerce sector. These packages also provide excellent product visibility, which improves customer appeal in the retail sector.

The food & beverages (portion packs, snacks, etc) are the fastest-growing in the plastic blister packs market, as they comprise hygienic, convenient, and portion-controlled products. Busy customer lifestyles enhance the demand for one-time serve, easy-to-manage snacks & portion-controlled food products, which plastic blister packs enable. These packs provide superior barrier protection against oxygen, moisture, and pollution, enhancing shelf life and confirming food security. Plastic blister packs are a cost-effective alternative to other arrangements, requiring fewer materials and freeing up shelf space.

")

Asia-Pacific held the largest share of the plastic blister packs market in 2025, driven by strong manufacturing capacity. Major factors include rising healthcare needs, the expansion of e-commerce, and demand for cost-effective, robust, and versatile packaging options, particularly from countries such as Japan, China, South Korea, and India. The noteworthy growth of the e-commerce sector in the region underscores the need for safe, effective packaging that withstands transit. These packs are cost-effective, versatile, and lightweight compared to other packing types, making them an ideal option across several industries.

The huge manufacturing base and the growing e-commerce sector have driven demand for plastic blister packs in China. The growing e-commerce industry and strong regulatory support for product security, particularly in the pharmaceutical sector, also drive demand for plastic blister packs, which offer a user-friendly, tamper-evident solution. The focus on product safety and integrity in China's packaging laws, particularly in the food and pharmaceutical sectors, makes plastic blister packs a favored option, given their tamper-evident features that help confirm compliance.

The expansion of the pharmaceutical sector has raised the demand for plastic blister packs. The robust development is also influenced by the region's progressive healthcare organizations, which drive demand for tamper-evident packaging that confirms patient safety and dose accuracy. Severe guidelines in the region require safe, tamper-evident packaging to verify drug authenticity and patient safety, further driving demand for plastic blister packs. Industries are capitalizing in advanced and sustainable packing solutions, comprising environment-friendly resources and high-tech structures like series for anti-fabricating. Advances in resource science and robotic engineering procedures are also contributing to market development.

Continuous changes in consumer habits have accelerated development in the U.S. plastic blister packs market. There is a growing shift from blister packs to bottles for solid oral medications, driven by suitability and enhanced patient adherence. The extension of the customer products and electronics industry in the U.S. is driving the demand for plastic blister packs to protect goods and display them efficiently on retail shelves. Strict guidelines in the pharmaceutical sector drive the use of plastic blister packs that offer features such as extended shelf life and single-dose safety.

The major factors influencing the growth of plastic blister packs market are improved product protection, security and tamper-evidence, single-dose format, versatility, and cost-effectiveness. Plastic blister packs offer excellent protection against exterior factors such as contamination, moisture, oxygen, and light, which is important for preserving the efficiency and shelf life of sensitive medicines. Plastic blister packs are a cost-effective option compared to some substitute formats, providing versatility in pattern and attractive goods visibility for retail presentation. The integration of automation, digital technologies, and advanced thermoforming capabilities into engineering processes is improving efficiency, quality control, and the overall appeal of plastic blister packs.

The rising demand for durable, shelf-appealing, and cost-effective packs has fuelled growth in the plastic blister pack market. These packs are increasingly used in e-commerce due to their durability and resistance to spills and breakage, which are important for transportation. They are frequently less costly than substitutes such as hard bottles and the use of some resources, which makes them inexpensive. These packaging options offer an excellent demonstration for retail, with choices for hang-hook displays and modified branding to stand out on shelves.

By Product / Format

By End-Use / Industry

By Geography / Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarPlastic Blister Packs Market