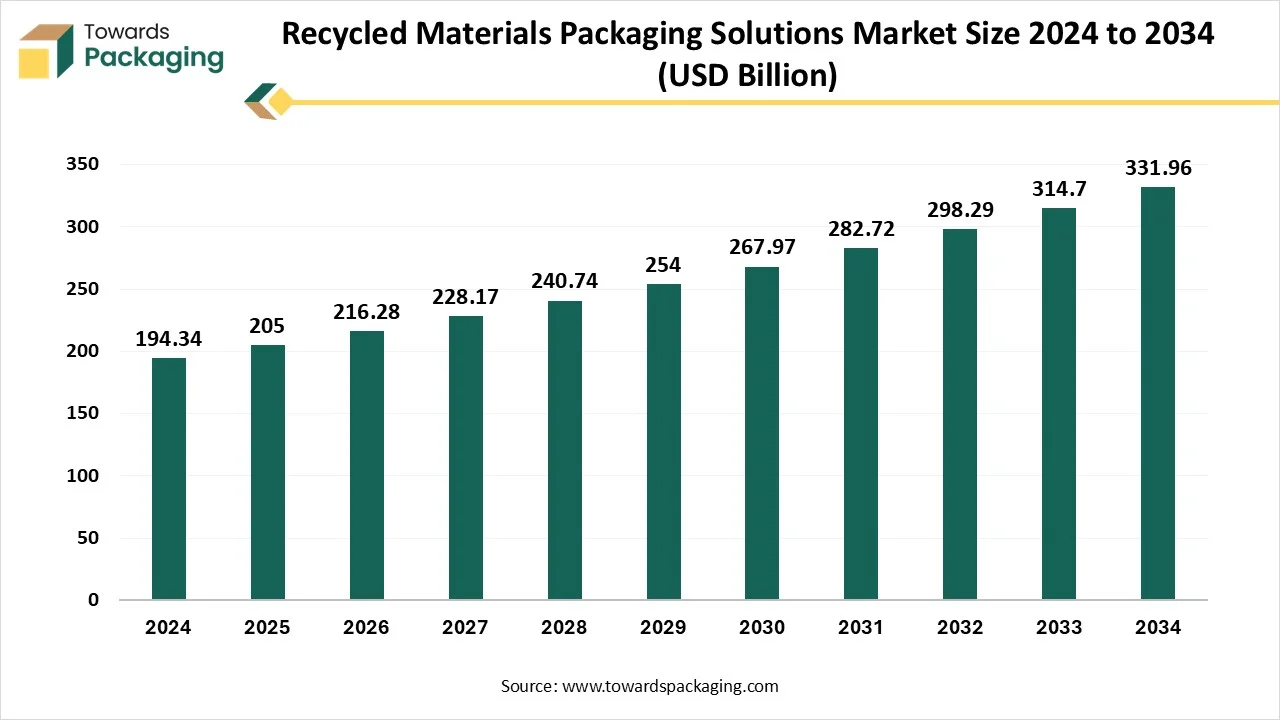

The recycled materials packaging solutions market is forecasted to expand from USD 216.31 billion in 2026 to USD 350.22 billion by 2035, growing at a CAGR of 5.5% from 2026 to 2035. This report covers full market size, growth trends, and segment-level insights across material types (recycled paper & cardboard 38%, plastics 30%, metals 15%, glass 17%), packaging formats (corrugated boxes 34%, rigid packaging 28%, flexible packaging 25%), recycling sources (PCR 60%, PIR 40%), and industries (food & beverage 42%, cosmetics 15%, e-commerce 13%). It provides regional analysis for North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, highlighting Europe’s 30% share, APAC’s high growth, and region-wise CAGR.

The study also includes top companies, competitive structure, value chain mapping, trade data, and manufacturer & supplier profiling across global markets.

The global recycled materials packaging solutions market comprises packaging solutions made from materials that have been previously used and processed through industrial recycling. These materials include paper, plastic, metal, and glass that are collected, sorted, cleaned, and remanufactured into new packaging products. These solutions are increasingly adopted across industries to minimize environmental impact, comply with regulations, and meet sustainability goals.

The incorporation of AI in the global recycled materials packaging solutions market plays a crucial role in optimizing the materials utilized for the packaging of products. It also predicts the demand of the market, which reduces the wastage of materials. AI is widely used for improving printing technology in packaging. With the incorporation of advanced technologies, the labour charges are deducted while manufacturing packaging.

")

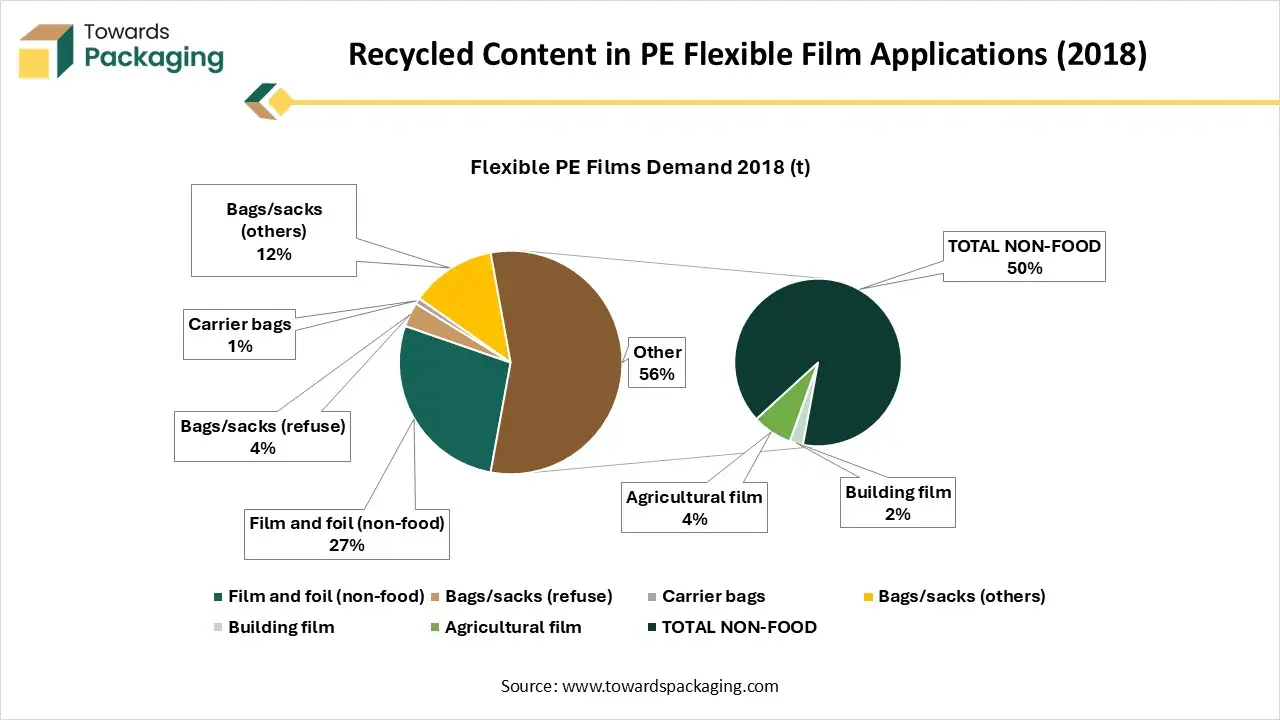

In 2018, the European market produced 1.8 million tonnes of recycled PE films, which represented roughly 20% of total PE flexible film demand. Of this, an estimated 1.2–1.3 million tonnes were high enough quality to be reused in film applications again, about 20% of all non-food film demand.

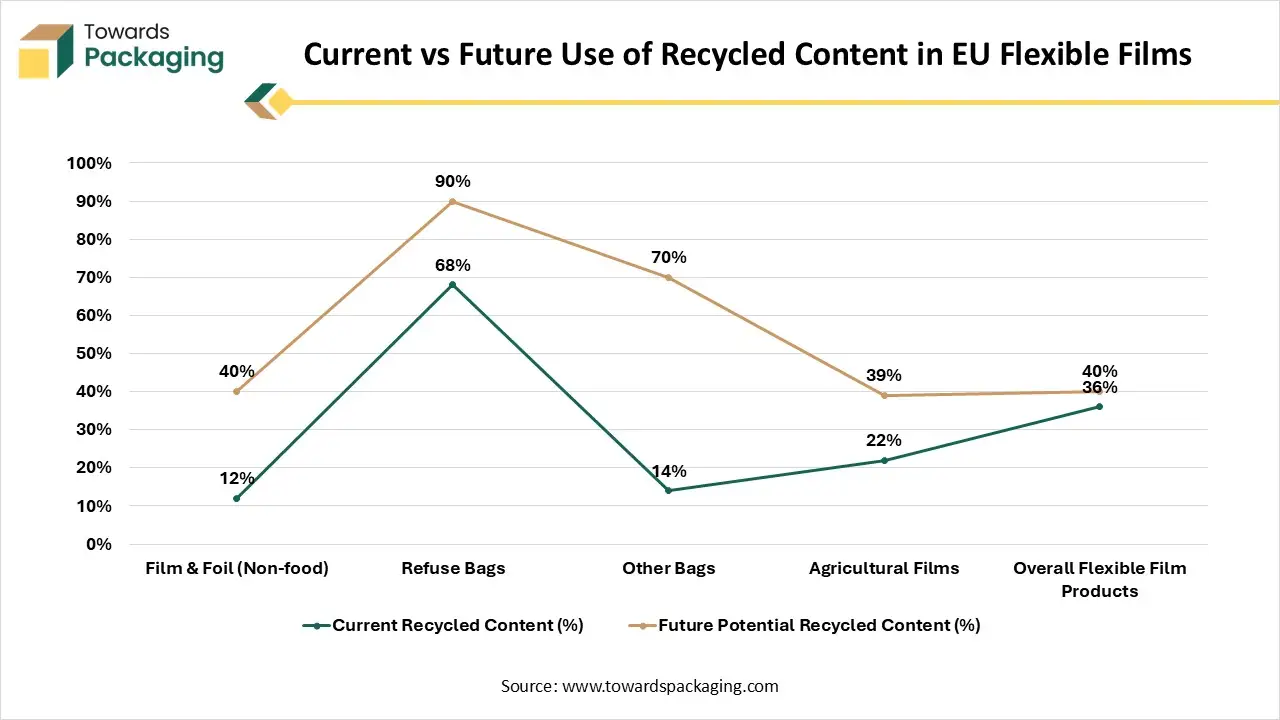

Recycled PE from films cannot currently be used in food-contact packaging, but there is significant untapped potential in almost all other flexible film sectors.

Refuse bags already use large amounts of recycled material (68%) and could reach 90% in the future.

| Growth Scenario (PE Film Production) | Estimated Demand for Recyclate (2030) |

| 1% Annual Growth | 3.6 million tonnes (Mt) |

| 4% Annual Growth | 5.0 million tonnes (Mt) |

| Additional recyclate usable in refuse bags | Up to 200 kt |

Across all flexible films, recyclate uptake could be dramatically expanded if technical and quality barriers are addressed. By 2030, depending on the growth of PE flexible packaging production, Europe could require between 3.6 Mt and 5 Mt of PE recyclate for flexible film applications alone.

Stringent Government Regulations in the Packaging Industry

The implementation of stringent government regulations in the packaging industry has driven the growth of the global recycled materials packaging solutions market. These creativities command the phasing out of single-utilization of plastics, ban injurious materials such as imposing taxes on non-recycled plastic and PFAS in packing convincing businesses to accept sustainable choices. As a consequence, there is a rising demand for packing solutions that use recycled resources and lessen ecological impact. The supervisory countryside not only applies acquiescence but also inspires invention in environment-friendly packaging resolutions. It is driving producers to grow and accept new skills and resources, thus nurturing a sustainable future for the packing business worldwide.

High Charges Linked with Recycling Infrastructure

The high charges connected with recycling organizations and skills pose important barriers to the development of the global recycled materials packaging solutions market. These charges comprise investment in gathering organizations, sorting skills, and processing services needed to recycle packaging resources proficiently. Such expenses discourage extensive acceptance of recycled resources, despite their ecological benefits.

Rising Collaboration among Market Players

The rising collaboration among shareholders for enhanced recycling procedures can result in cost-effective resolutions, additionally influencing the acceptance in several businesses. Developing sectors also show an important possibility, as the-influence for sustainability generates a fertile ground for presenting recycled packaging resolutions in emerging areas. In current times, movements show a change in the direction of circular economy principles, where packing is intended for reuse and recyclability. Companies are progressively transparent about their tracking and manufacturing procedures, further endorsing customer belief.

The growth of e-commerce has also inclined the packaging aspect with demand for resources that can resist shipping while being ecologically friendly. Moreover, customer preferences are developing, with greater stress on minimalistic and practical design in packing that uses recycled content. This tendency imitates a broader societal change in the direction of accountable consumption and waste decrease, inspiring ongoing invention in the packaging segment.

The recycled paper & cardboard segment contributed a considerable share of the global recycled materials packaging solutions market in 2024 due to its high biodegradability and recyclability. Technological advancements in this sector have influenced the growth of the segment by enhancing the reliability of the consumers. The rising ecological concern among consumers due to increasing environmental issues has enhanced the demand for this market. Rapid growth in the e-commerce sector has inclined consumers towards this type of packaging.

The rPET (Recycled Plastic) segment is expected to grow at the fastest rate in the market during the forecast period of 2025 to 2034. The rising demand for sustainable packaging has influenced the development of this segment. The strength, durability, safety, and clarity of products have helped to expand this segment rapidly. The increasing commitment of the food & beverage industry towards sustainable packaging has raised the usage of this market.

The corrugated & paperboard boxes segment held a considerable share of the global recycled materials packaging solutions market in 2024 due to its widespread cost-effectiveness and accessibility. Easily availability of such boxes is the major reason behind the growing demand for this market. These are widely used in e-commerce, food & beverages, cosmetics, electronics, and pharmaceutical industries. Advancements in printing technology have also improved the demand for recycled materials and packaging solutions.

The flexible pouches segment is expected to grow at the fastest rate in the market during the forecast period of 2025 to 2034. The lightweight, consumer-friendly, and cost-effective properties help this segment to grow rapidly. The enhanced recyclability demand in the packaging sector has increased the adoption of this segment in various sectors.

The post-consumer recycled segment was dominant over the low-carbon footprint packaging market in 2024 due to the corporate sustainability goals, technological advancements, and strict regulatory compulsion. Rigid bottles and pouches are high in demand in this segment. Both mechanical and chemical recycling process advancements have influenced the demand for this market. The enhanced materials performance demand has increased the development of this sector.

The post-industrial recycled (PIR) segment is expected to grow at the fastest rate in the market during the forecast period of 2025 to 2034. This is because of the circular economy, scalability, and consistency of the market. The advancement in the recycling industry and stringent ecological guidelines have raised the demand for this market. It safeguards uniform quality, lower infection, and ensures easier obedience.

The food & beverages segment held a considerable share of the global recycled materials packaging solutions market in 2024 due to the regulatory guidelines and customer demand. Recycled jars and bottles provide clarity, safety, and provide high barrier from adverse ecological conditions. It has properties to provide safety to perishable food products have raised the demand for this market. The strict guidelines of the food packaging industry have compelled brands the adoption such packaging materials.

The e-commerce & retail segment is expected to grow at the fastest rate in the market during the forecast period of 2025 to 2034. This segment is growing rapidly due to the increasing regulatory pressure and sustainability demand of the market. E-commerce -platforms such as Flipkart, Amazon, Myntra, and several others have raised major concerns about packaging waste. Such awareness and brand image consciousness have influenced the growth of this market.

The direct (B2B) segment accounted for a considerable share of the global recycled materials packaging solutions market in 2024 due to the supply-chain innovation, sustainability orders, and cost-effectiveness. Direct (B2B) buyers are adopting biodegradable sources such as bamboo, PCR cardboard, seaweed, molded pulp, and mycelium composites. This section is intensifying dealers across the region to make the most in local construction, and encouraging multi-tier sourcing. Compact waste and direct (B2B) brand positioning has predisposed the expansion of this market.

The online platforms segment is expected to grow at the fastest rate in the market during the forecast period of 2025 to 2034. The growing importance of customers in utilizing eco-friendly packaging has improved the demand for this industry. Smart tech amalgamation, like NFC tags and QR codes, has boosted assignment and transparency. Personalization with digital printing has enhanced the expansion of this market.

Europe held the largest share of the global recycled materials packaging solutions market in 2024, due to advancements in recycling technology, strict government regulation, and high consumer demand. In countries such as the U.K., Germany, Italy, Sweden, and many others are encouraging recycled packaging materials, which is altering the packaging industry's worth chain, inducing innovation in material obtaining, production procedures, and supply chain logistics. This change not only influences customer behavior and supervisory outlines but also nurtures a more sustainable and global economy within packing.

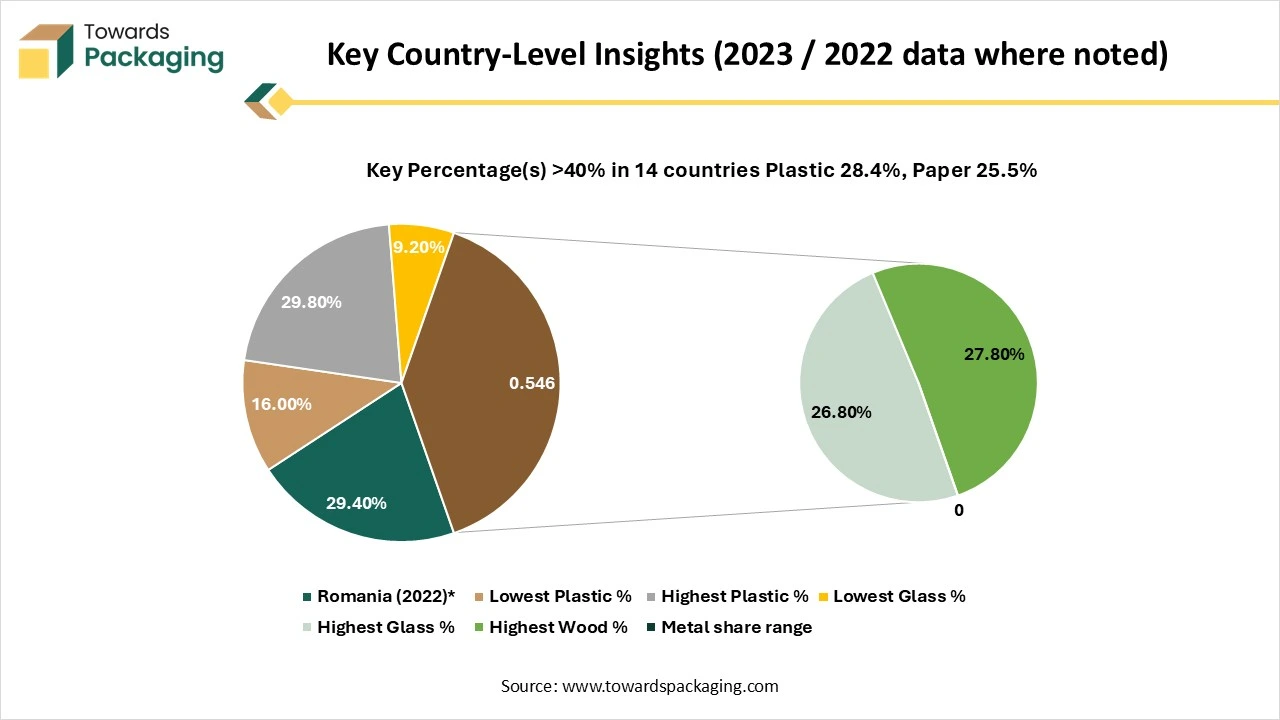

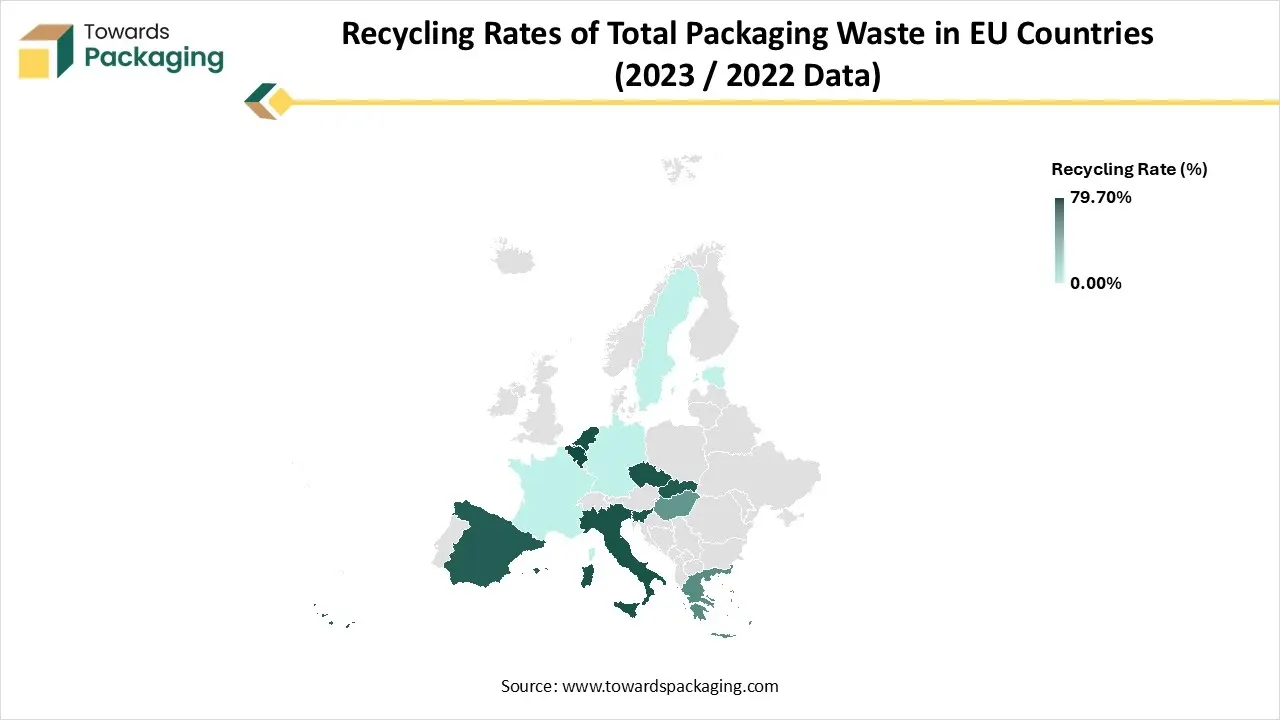

In 2023, the European Union generated 79.7 million tonnes of packaging waste. The majority came from paper and cardboard, which accounted for over 40% of the total. Plastics and glass also contributed significantly, making up 19.8% and 18.8%, respectively. Wood represented about 15.8%, while metals and other materials formed only a small portion.

")

Across most EU countries, the distribution by material was similar to the EU average. Paper and cardboard were the largest source of packaging waste in 26 out of 27 countries, with Bulgaria being an exception, where plastic waste was slightly higher. Plastic waste contributed as little as 16% in Luxembourg and nearly 30% in Ireland. Glass packaging waste varied widely from 9.2% in Finland to 26.8% in Croatia. Metal waste was generally low everywhere, remaining below 10% in all nations.

The EU aims to recycle 70% of all packaging waste by 2030, with even higher targets for specific materials like 85% for paper, 75% for glass, and 55% for plastics. In 2023, the EU was close to reaching this goal, achieving a recycling rate of 67.5%.

")

Seven EU countries have already surpassed the 70% target, including Belgium, Netherlands, Italy, Czechia, Slovenia, Slovakia, and Spain. Many others, such as Germany, France, Estonia, Sweden, and Cyprus, are very close, reporting recycling rates between 68.5% and 69.5%. However, some countries are struggling: Romania, Hungary, Malta, and Greece achieved recycling rates below 50%, far from the EU’s 2030 ambitions.

The Asia Pacific region is estimated to grow at the fastest rate in the global recycled materials packaging solutions market during the forecast period. The rising government initiatives towards ecological issues have raised the concern among people to use packaging which are eco-friendly. In countries such as India, Japan, China, Thailand, and several others, the presence of major market players has introduced innovation in this market.

By Material Type

By Packaging Type

By Recycling Source

By End-Use Industry

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarRecycled Materials Packaging Solutions Market