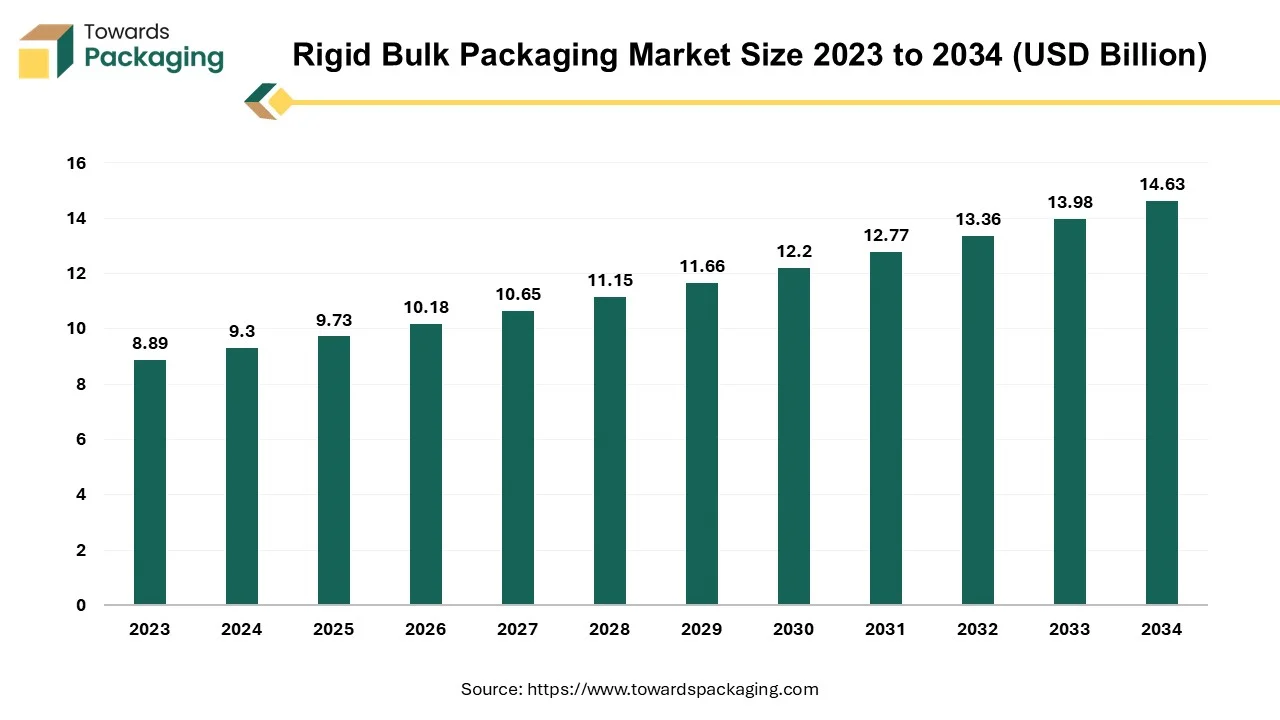

The rigid bulk packaging market is forecasted to expand from USD 10.18 billion in 2026 to USD 15.30 billion by 2035, growing at a CAGR of 4.63% from 2026 to 2035. This market is driven by the increasing demand in the food and beverage and pharmaceutical industries. Key segments include plastic, metal, and wood materials, with Intermediate Bulk Containers (IBCs) dominating product types.

Asia-Pacific holds the largest market share, driven by rapid industrialization and urbanization, while North America and Europe exhibit steady growth due to their mature industries. Major players include Greif Inc., Berry Global Inc., and Mondi Group PLC.

Rigid bulk packaging refers to high-strength packaging containers that are mainly used to transport perishable, delicate, and volatile products. This type of packaging ensures the safe transportation of sensitive products. Heavy-duty materials such as high-strength plastics, metals, and wood are generally used to manufacture rigid bulk packaging.

Rigid bulk packaging is commonly used in the food and beverage, pharmaceutical, and industrial chemical transportation industries. These industries utilize rigid bulk packaging for the safe and efficient transportation of pharmaceutical drugs, perishables, and volatile chemicals. This type of packaging prevents leaks and contamination of products. The global push towards reusable forms of packaging is driving demand for bulk containers. These also have the added advantage of being highly cost-effective compared to smaller containers.

The industry has seen growth due to the rapid pace of industrialization and urbanization occurring in several countries in the Asia-Pacific region which has caused the demand for various products to rise rapidly. A rise in global import and export volumes coming from the region is driving growth in the market. The global packaging market size to grow at a 3.16% CAGR between 2026 and 2035.

Recent government regulations limiting the use of plastics and other raw materials used in rigid bulk packaging are challenging growth in the sector. The increasing popularity of flexible packaging that takes up less storage space and environmental concerns are also a restraint in the market.

Rapid urbanization has caused the demand for food and beverages, pharmaceutical, and manufacturing sectors to skyrocket, particularly in the emerging economies of Asia-Pacific. High demand in these sectors can be attributed to increasing disposable income and significant government investment in energy, industrial, healthcare, and transport infrastructure across the region. The growing oil and gas imports into the region have also spiked demand for rigid bulk packaging. Surging investment in healthcare infrastructure has also grown demand for durable, hygienic, and lightweight variations of rigid bulk packaging.

All these factors have significantly boosted the rigid bulk packaging market as there is now a high demand for reusable bulk containers to optimize cost-effectiveness in regional supply chains and ensure secure bulk transportation of goods. The region is also poised for sustained growth during the forecast period, making it likely that this demand will be maintained.

Strict environmental regulations are being widely adopted by several countries to reduce the impact of hard-to-recycle materials like certain plastics. Some countries have outright banned single-use plastics while others require mandatory plastic offsetting schemes for businesses. Some materials used in rigid bulk packaging have been declared hazardous in some countries while others impose limits on their recyclability. In some regions, the need for adequate recycling infrastructure and trash management systems poses challenges to the growth of the rigid bulk packaging industry.

The growing cost of renting and owning storage space has given way to the rising popularity of flexible packaging which offers greater versatility compared to their rigid bulk counterparts. Some businesses also choose to switch to flexible packaging options to bring down transportation costs.

Rigid bulk packaging manufacturers introduce tailored solutions to meet industry requirements by offering a variety of designs and capacities. Diversifying into manufacturing recycled plastic products, jars, and clamshells help businesses grow, especially in the fast-growing markets of the Asia-Pacific region. Businesses opt to adopt advanced packaging techniques to cater to the growing demand for produce and healthcare packaging solutions in the region.

| Rank | Company | Headquarters | Country | Why Relevant to This Market | Key Packaging Products/Services |

| 1 | Mauser Packaging Solutions | Oak Brook, Illinois | USA | Global leader in industrial packaging, IBCs, drums, and reconditioning services | IBCs, steel drums, plastic drums, reconditioning |

| 2 | Greif | Delaware, Ohio | USA | One of the world's largest industrial packaging companies with extensive bulk packaging operations | Steel drums, IBCs, bulk containers |

| 3 | SCHUTZ | Selters, Rhineland-Palatinate | Germany | Global pioneer and market leader in IBC manufacturing and return systems | Intermediate bulk containers |

| 4 | Time Technoplast | Mumbai, Maharashtra | India | Major global producer of large plastic industrial containers and composite cylinders | IBCs, drums, industrial containers |

| 5 | Snyder Industries | Lincoln, Nebraska | USA | Leading manufacturer of bulk storage and material handling containers | Bulk containers and tanks |

| Rank | Company | Headquarters | Country | Why Relevant to This Market | Key Packaging Products/Services |

| 1 | Muller Group | Rheinfelden, Baden-Württemberg | Germany | Strong supplier of industrial drums and hazardous goods packaging | Steel and plastic drums |

| 2 | Balmer Lawrie | Kolkata, West Bengal | India | Major supplier of industrial packaging for chemicals and lubricants | Steel drums and industrial containers |

| 3 | CurTec | Rijen, North Brabant | Netherlands | Specialist in high-performance rigid plastic bulk packaging | Plastic drums and pails |

| 4 | Hoover Ferguson | Houston, Texas | USA | Leading provider of reusable industrial packaging and logistics solutions | IBCs and container rental services |

| 5 | THIELMANN | Granada, Andalusia | Spain | Specialist in stainless steel containers and industrial transport packaging | Stainless steel IBCs |

| Rank | Company | Headquarters | Country | Why Relevant to This Market | Key Packaging Products/Services |

| 1 | NCI Packaging | Indianapolis, Indiana | USA | Supplier of industrial drums and rigid packaging solutions | Plastic and steel containers |

| 2 | Rahway Steel Drum Company | Rahway, New Jersey | USA | Specialized producer of steel drums and industrial containers | Steel drums |

| 3 | AST Plastic Containers | Stuttgart, Baden-Württemberg | Germany | Regional supplier of industrial bulk packaging solutions | Plastic industrial containers |

| 4 | Envases Universales | Monterrey, Nuevo León | Mexico | Major Latin American producer of industrial packaging products | Industrial drums and containers |

| 5 | Pensteel | Johannesburg, Gauteng | South Africa | Regional supplier of industrial drum packaging | Steel drums and bulk packaging |

The plastic segment held the largest share of the rigid bulk packaging market in 2025. The plastics segment includes bioplastics, polyethylene, polyethylene terephthalate, polystyrene, and others. The versatility, durability, and lightweight but rigid nature of plastic packaging allow businesses to meet a variety of packaging needs across industries. Manufacturing plastic for packaging is also a lot cheaper compared to other materials leading to its widespread adoption in the industry. Due to an increasing demand for sustainable and eco-friendly rigid packaging solutions, metal, wood, and glass alternatives are gaining popularity in the rigid bulk packaging sector.

The metal segment is the fastest-growing material type in the rigid bulk packaging market due to a global shift towards more eco-friendly packaging alternatives. Metal is also more recyclable than materials like plastic. Rigid metal packaging provides an airtight, temperature-controlled, and light-resistant environment for products, helping extend their shelf life. This is particularly useful for the food, beverages, and cosmetic industries. Wood rigid bulk packaging is gaining traction in the space thanks to a shift in consumer behavior and demand for sustainable packaging solutions, including wooden and plywood packaging. Wood is a natural and renewable resource. When wood is harvested and used for packaging, the carbon remains locked away from the atmosphere, reducing net CO2 emissions.

The intermediate bulk containers (IBC) segment led the rigid bulk packaging market. Intermediate bulk containers are the gold standard in rigid bulk packaging owing to their cost-effectiveness. They are especially useful for transporting liquids in bulk that can then be portioned out into smaller containers for end users. Businesses can save on costs by shipping out larger containers, compared to several smaller ones. IBCs are also durable and reusable, making them ideal for transporting hazardous materials due to features such as double valves. The incorporation of such features makes filling and draining them a lot simpler. The universal design of IBCs makes them stackable and easy to handle.

The bulk boxes is the fastest-growing product type in the rigid packaging space due to their durability and customization which contributes to brand recognition. Rigid bulk boxes offer an added layer of security against moisture and other environmental hazards. Pails are also gaining traction in the rigid bulk packaging space. Pails are widely utilized as shipping and transportation containers due to the expansion of manufacturing sectors in growing economies.

The market is divided into food, beverage, pharmaceutical and chemicals, industrial, and others. The food and beverages dominated the market in 2025. The food and beverage industry has grown dramatically in the past decade, especially in the Asia-Pacific region due to a large consumer base and rising disposable income which has shifted consumer tastes and preferences. The increasing demand for staple foods, carbonated soft drinks, caffeinated drinks, snacks, and baked goods is driving demand for proper transportation and storage solutions in the rigid bulk packaging space.

The pharmaceutical segment of the market is the fastest growing segment in the market. The overall rising demand for pharmaceutical products across the globe, is observed to supplement the market. The increasing investment in healthcare and the prevalence of chronic diseases are driving demand for the transportation of goods.

Asia Pacific had the largest share in the rigid bulk packaging market. The region is home to several of the largest emerging economies in the world with a high demand for manufacturing & construction. A high disposable income and a young demographic’s changing lifestyles have spurred demand for a variety of goods through the rise of e-commerce, leading to growing trade.

The Chinese government has implemented stricter environmental regulations to promote recycling and sustainable packaging solutions. This has led to increased demand for high-quality, durable, and reusable rigid bulk packaging.

The Make in India initiative aims to transform India into a global manufacturing hub. This has led to increased investments in manufacturing infrastructure, which in turn drives the demand for rigid bulk packaging to support various industries.

China Market Trends

China's rigid bulk packaging market is driven by robust manufacturing infrastructure in the country. China’s extensive manufacturing capabilities enable the efficient production of various rigid bulk packaging solutions, including drums, boxes, and intermediate bulk containers (IBCs). The country’s competitive labor costs and well-established supply chains contribute to cost-effective manufacturing, making Chinese products attractive in global markets. China’s rapid industrialization and economic expansion have increased the demand for bulk packaging solutions across sectors such as chemicals, food and beverages, and pharmaceuticals. China’s position as a global manufacturing hub has bolstered its export capabilities, making it a key supplier of rigid bulk packaging worldwide. China’s participation in international trade agreements facilitates access to global markets, enhancing its competitiveness in the rigid bulk packaging industry.

North America is the fastest growing region in the space, during the forecast period. The region is home to robust manufacturing industries and important market players in the chemicals, pharmaceuticals, food and beverages, and automotive sectors. The United States is the world's third-largest exporter and second-largest importer of goods. This is leading to high growth in the rigid bulk packaging space. Companies in the region are increasingly adopting smart packaging solutions that incorporate IoT, sensors, and RFID technology to improve supply chain efficiency and product tracking.

U.S. Market Trends

The U.S. rigid bulk packaging market is driven by several factors. U.S. companies are leaders in automated production and high-precision manufacturing of rigid packaging. Emphasis on durability, reusability, and standardized packaging formats supports efficiency in logistics and warehousing. The U.S. has large, mature industries like chemicals, food & beverages, pharmaceuticals, agriculture, and construction, all major users of rigid bulk packaging (e.g., drums, IBCs, crates, and bins). These sectors require durable, high-quality packaging for storage and long-distance transportation.

Regulatory bodies like the U.S. FDA, EPA, and DOT impose rigorous standards for packaging used in transporting hazardous materials, chemicals, and food products. There’s growing demand in the U.S. for returnable and reusable packaging systems, especially in closed-loop logistics and green supply chains. U.S. companies lead in designing eco-friendly packaging that reduces environmental impact and meets corporate sustainability goals. The U.S. is home to several major packaging companies like Greif, Mauser Packaging Solutions, and Berry Global. These firms have global footprints, leading to influence over global packaging standards and widespread adoption of U.S.-made rigid packaging products.

The Latin American rigid bulk packaging is focused, with fewer players accounting for a huge share. The market is being classified by invention, with companies investing in the latest technologies in order to create sustainable and cost-effective packaging solutions. The market is also being regulated, with organisations implementing regulations in order to lower the environmental impact of plastic packaging. The end-user focus is very big, with a few large companies accounting for a major share of the market. The level of M&A in the market is lower, with fewer notable mergers in recent years.

Apart from this, the food sector is the main force in designing the packaging scenario within Brazil, a trend further grown by the common work-from-home culture. Plastics have completely dominated the food industry in Latin America. They are grown by cost-effectiveness, lightweight, and design adaptability.

Rigid bulk packaging is changing the rigid plastic packaging market in the Middle East and Africa, delivering as a main solution for various sectors that totally depend on the packaging of their products. The recyclable rigid plastic packaging items are created of jars with open tops and independent lids, covers, and closures. Heavy and big rigid containers are widely used in supermarkets and shops in order to transport various products, including food and pharmaceuticals. Hence, rigid plastics’ reliability and durability potential to be recycled are the crucial factors driving the market in the region.

Plastics demonstrate many surrounding risks if they are not controlled accurately at the beginning of the value chain and throughout their long duration presence, particularly in the ocean. Due to the growth of plastic manufacturing and usage in the Arabian Gulf, shipping and waste disposal practices, the correct amount of plastic waste on the ocean's surface and beaches has increased.

By Material

By Product Type

By Application

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarRigid Bulk Packaging Market