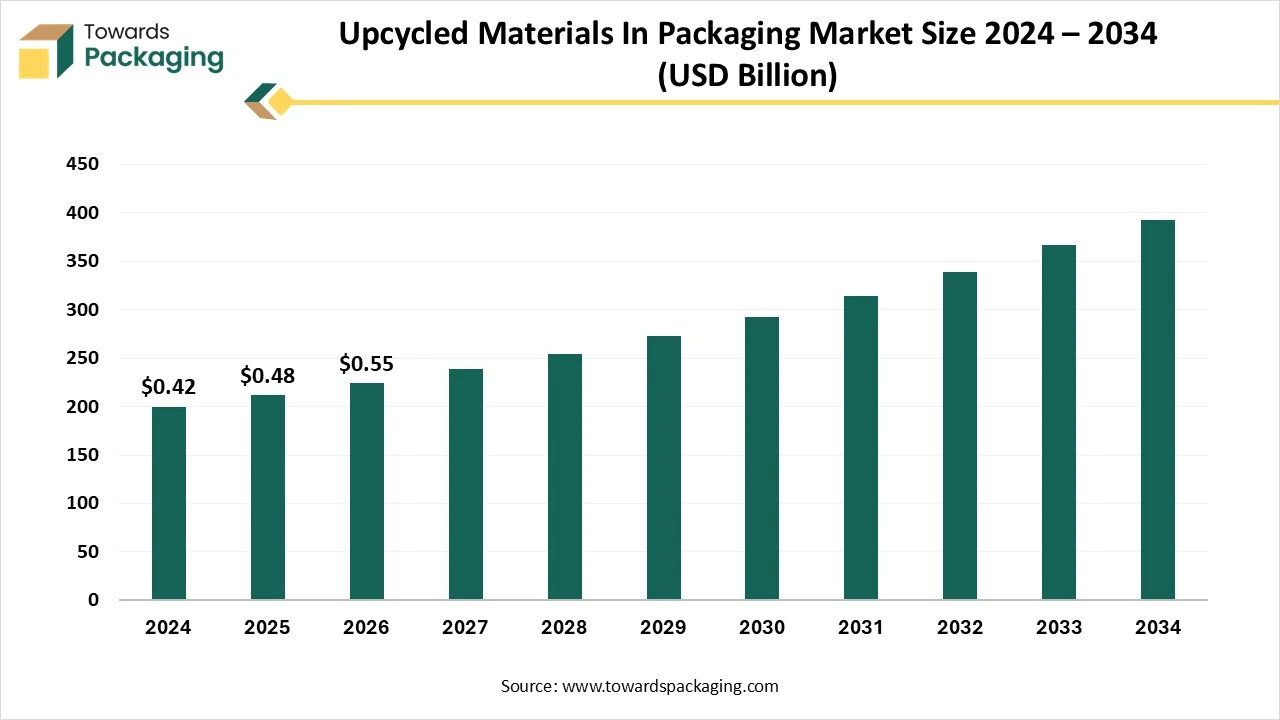

The upcycled materials in packaging market provides a full analytical overview covering market size, growth forecasts, trends, and all statistical insights across material types, packaging forms, and end-use sectors. This report includes detailed regional coverage for North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, along with company profiles, competitive analysis, value chain assessment, and global trade data. It also maps key manufacturers, suppliers, and industry stakeholders to give readers a complete data-backed understanding of the market.

Upcycled materials in packaging refer to packaging solutions created from waste materials that have been repurposed or transformed into higher-value products, rather than being discarded. Unlike traditional recycling, which often results in a degradation of material quality, upcycling retains or enhances the original material’s value. Common sources include post-consumer products, scrap textiles, and agricultural byproducts. The primary attributes of upcycled packaging are waste reduction, environmental sustainability, and innovation. This approach not only diverts waste from landfills but also lowers the environmental footprint of packaging production by substituting virgin materials with renewable or repurposed inputs. According to the Sustainable Packaging Coalition, upcycling contributes significantly to circular economy goals by converting discarded materials into functional, high-quality packaging solutions.

| Metric | Details |

| Market Drivers | E-commerce growth Environmental awareness Regulatory support |

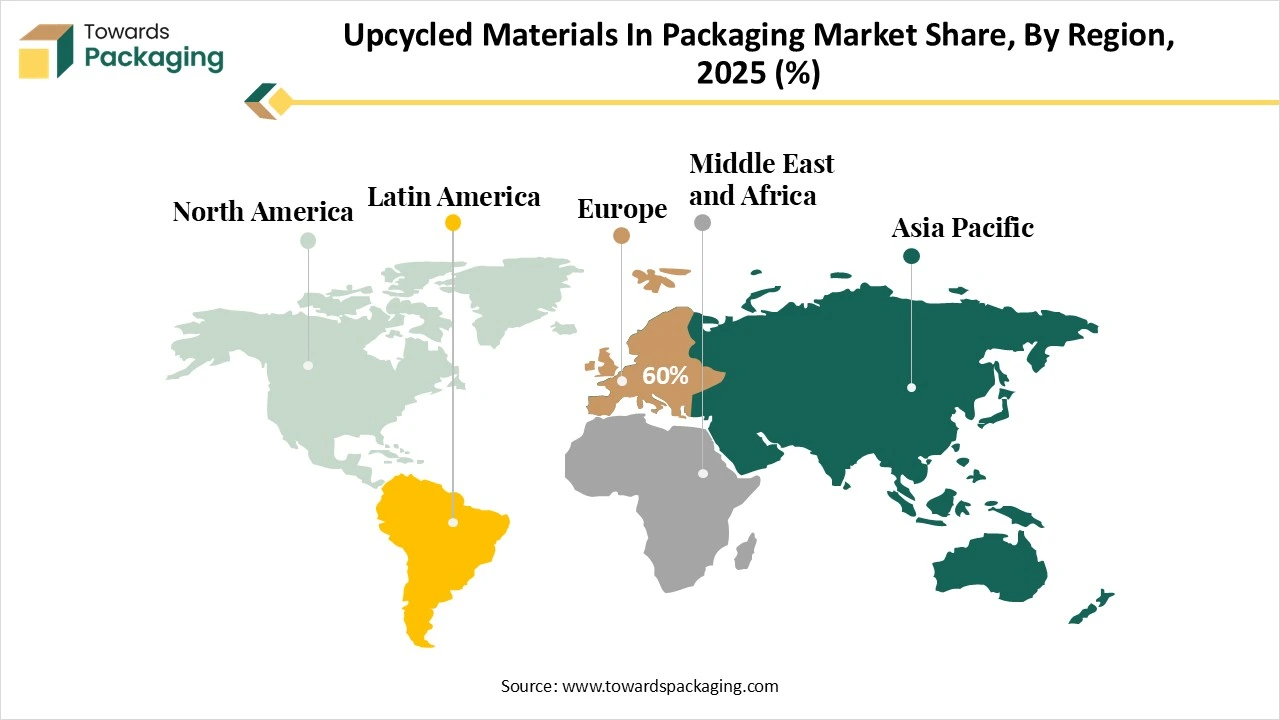

| Leading Region | Europe |

| Market Segmentation | By Material Type, By Packaging Form, By End-Use Industry and By Region |

| Top Key Players | Amcor Plc, Mondi Group, Berry Global Inc., Smurfit Kappa, Ball Corporation, Mauser Packaging Solutions. |

(Source: Sustainable Packaging Coalition, 2024)

Artificial Intelligence (AI) is playing a transformative role in advancing the upcycled materials in packaging industry by enhancing material discovery, design optimization, and environmental assessment. AI algorithms can analyze vast datasets of chemical compositions, molecular structures, and functional properties to identify upcycled material candidates with ideal attributes such as biodegradability, tensile strength, and barrier performance. This accelerates the development of innovative, eco-friendly packaging solutions.

AI-driven design tools further optimize the formulation, structure, and processing parameters of upcycled packaging materials, enabling manufacturers to reduce material usage while enhancing functionality and sustainability across the product lifecycle. Additionally, AI-powered life cycle assessment (LCA) platforms evaluate environmental impacts from raw material extraction to end-of-life, helping stakeholders make data-driven decisions for greener packaging.

Moreover, AI enhances packaging circularity by optimizing designs for reusability, recyclability, and compostability, thus aligning with the principles of the circular economy. According to the Ellen MacArthur Foundation, leveraging AI technologies in sustainable design and material innovation is essential for driving circular solutions in the packaging sector.

One of the key drivers of the upcycled materials in packaging industry is the convergence of rising environmental concerns and the rapid expansion of e-commerce. Increasing awareness about climate change, plastic pollution, and resource depletion has led consumers and businesses to demand more sustainable packaging solutions. Upcycled materials provide a low-impact alternative by diverting waste from landfills and minimizing dependence on virgin raw materials.

The growth of e-commerce platforms such as Amazon, Shopify, and Flipkart has significantly increased the demand for shipping and secondary packaging—boxes, fillers, pouches, and labels—creating a substantial opportunity for the integration of upcycled materials like post-consumer cardboard, agricultural waste-based paper, and biodegradable fillers. According to the Ellen MacArthur Foundation, aligning packaging strategies with circular economy principles—such as reuse, recycling, and upcycling—is essential for reducing environmental harm and promoting sustainability.

E-commerce platforms can play a pivotal role by mandating or incentivizing the use of upcycled packaging among sellers, offering sustainability certifications or badges, and incorporating eco-friendly filters in product search tools. These initiatives not only encourage vendors to adopt upcycled materials but also cater to the growing segment of environmentally conscious consumers. Additionally, reverse logistics models that support take-back or reuse of packaging further strengthen the circular value chain, turning delivery waste into raw material for future packaging.

A significant restraint in the upcycled materials in packaging market is the limited and inconsistent supply of raw materials, coupled with complex regulatory challenges. Upcycled packaging relies heavily on post-consumer and industrial waste streams such as agricultural byproducts, food scraps, and textile remnants. These inputs can be seasonal, variable in quality, and prone to contamination, resulting in supply chain disruptions and difficulties in maintaining consistent material standards.

Moreover, regulatory compliance poses additional barriers. Ensuring food safety and meeting packaging standards with upcycled materials can be difficult due to inconsistent composition and potential contamination risks. Many regions also lack clear regulatory frameworks or certifications specific to upcycled materials, which creates uncertainty for manufacturers and limits market scalability. According to the U.S. Environmental Protection Agency (EPA), the absence of standardized guidelines and reliable supply chains is a key challenge in integrating upcycled content into mainstream packaging solutions.

A major opportunity in the upcycled materials in packaging market lies in the rapid advancements in material science. Ongoing research and development have enabled the transformation of agricultural residues, food by-products, and textile waste into high-performance packaging materials. Innovations in areas such as bio-binders, biopolymers, and fiber reinforcements have significantly enhanced the structural integrity, safety, and visual appeal of upcycled packaging, making it more commercially viable and competitive with conventional materials.

The continuous introduction of novel materials is unlocking new market segments and applications. For example, according to data published in October 2024, RM Tohcello Co., Ltd., TOPPAN Inc., and Mitsui Chemicals, Inc. launched a collaborative pilot project for the horizontal recycling of printed BOPP (biaxially oriented polypropylene) flexible packaging films. This initiative successfully developed a recycled BOPP film capable of being produced at scale, demonstrating how technical innovation can drive the practical implementation of upcycled solutions in mainstream packaging.

(Source: TOPPAN Holdings Inc., October 2024)

The plastic segment accounted for the largest share of the upcycled materials in packaging market in 2024. This dominance is primarily due to the vast and consistent availability of plastic waste, which serves as a reliable feedstock for upcycled packaging. Plastics such as PET (polyethylene terephthalate), HDPE (high-density polyethylene), and LDPE are commonly collected, cleaned, and reprocessed into new packaging materials.

The paper segment is projected to exhibit the highest growth rate during the forecast period. Recycled paper is favored for its ease of reuse (up to 5–7 cycles), biodegradability, and lower carbon footprint compared to plastic or metal.

In 2024, the boxes & cartons segment accounted for a major share of the upcycled materials in packaging market. These formats are essential across industries such as e-commerce, food & beverages, electronics, retail, and consumer goods, making them an ideal application for upcycled materials.

The paper bags & sacks segment is expected to grow at the fastest rate during the forecast period. This growth is driven by rising consumer preference for biodegradable, recyclable, and upcycled alternatives to single-use plastic bags.

The food & beverage segment led the global upcycled materials in packaging market in 2024, driven by increasing environmental pressures and evolving consumer preferences. This industry is actively seeking sustainable packaging solutions to minimize its environmental impact, and upcycled materials provide a low-waste, resource-efficient alternative.

")

Europe held the largest share of the upcycled materials in packaging market in 2024, primarily driven by stringent environmental regulations and proactive sustainability initiatives. The European Union’s Green Deal and Circular Economy Action Plan mandate sustainable production and consumption practices, while comprehensive waste management laws and bans on single-use plastics push companies toward adopting upcycled packaging materials. Extended Producer Responsibility (EPR) regulations further enforce accountability, requiring manufacturers to manage the full lifecycle of their packaging products.

European consumers are among the most eco-conscious globally, significantly influencing market demand. This has prompted businesses to adopt innovative upcycled packaging solutions to meet consumer expectations for transparency, sustainability, and ethical production.

Europe’s advanced recycling infrastructure ensures efficient collection and processing of recyclable materials, providing a consistent supply of high-quality feedstock for upcycled packaging. Additionally, the region is home to numerous sustainability-focused startups and packaging firms, along with reputable certification bodies such as Cradle to Cradle, FSC, and the EU Ecolabel, which enhance market credibility and consumer trust.

According to the European Commission, these combined factors make Europe a global leader in circular economy practices, accelerating its dominance in the upcycled packaging market.

The Asia Pacific region is projected to experience the fastest growth in the upcycled materials in packaging market during the forecast period (2025–2034), driven by regulatory reforms, booming e-commerce, and rising consumer demand for sustainable products. Governments across the region are enacting stringent policies to curb plastic waste and promote eco-friendly alternatives. For instance, China’s “Plastic Ban 2021” restricts the use of non-biodegradable plastics in major cities, while India’s amended Plastic Waste Management Rules (2021) are accelerating the shift to sustainable packaging. Thailand has also announced a complete ban on plastic waste imports by 2025.

The rapid expansion of e-commerce—expected to grow at over 20% annually in the region—is increasing demand for durable yet sustainable packaging solutions. Fast-growing sectors such as food delivery and pharmaceuticals are adopting upcycled materials like molded pulp and recycled paperboard to comply with evolving regulations and sustainability targets.

Consumer preferences are also shifting. A Nielsen report revealed that more than 70% of consumers in Australia and Japan are willing to pay a premium for products in sustainable packaging, incentivizing companies to invest in upcycled solutions. Furthermore, economic growth in countries like India and China has led to increased consumption of packaged goods, amplifying the demand for low-impact, recyclable, and upcycled packaging options.

(Source: Nielsen Global Survey on Corporate Social Responsibility and Sustainability, 2024)

India’s upcycled materials in packaging market is gaining momentum, driven by rising demand for sustainable packaging solutions and increasing regulatory and corporate initiatives. Major brands like PepsiCo India and Amul have committed to 100% sustainable or upcycled packaging as part of their environmental goals, aligning with India’s broader national targets for reducing plastic waste and promoting circular economy practices.

Government policies under the Plastic Waste Management Rules (amended 2021) mandate the use of recycled or biodegradable materials, further encouraging the adoption of upcycled packaging across industries. In addition to top-down corporate commitments, grassroots innovation is playing a vital role. In Dharavi, Mumbai, local artisans are transforming discarded plastic waste into reusable items such as woven bags and mats. These initiatives support both environmental sustainability and local economic empowerment, showcasing the potential for scalable, community-led circular solutions.

According to the Central Pollution Control Board (CPCB), India generates over 3.5 million metric tons of plastic waste annually, highlighting the urgency and market potential for upcycled packaging alternatives in both urban and rural sectors.

North America is expected to witness notable growth in the upcycled materials in packaging market, driven by robust corporate sustainability commitments, expanding recycling infrastructure, and increasing consumer demand for eco-friendly products. Major corporations such as Unilever, Nestlé, Walmart, and PepsiCo have pledged to transition to 100% reusable, recyclable, or compostable packaging by 2025–2030, catalyzing the adoption of upcycled materials across the supply chain.

The region’s well-established recycling infrastructure—with over 2,800 facilities—supports the processing of recyclable and upcyclable materials, helping divert 2.1 million tons of packaging waste from landfills annually. Companies like International Paper are leading investments in sustainable packaging innovations, including fiber-based and biodegradable solutions derived from agricultural or industrial waste.

Consumer behavior further supports this trend, with 82% of North American consumers, and 90% of Gen Z, willing to pay more for products packaged sustainably. Additionally, the region is expanding its use of plant-based and biodegradable packaging, with 1.5 million tons of such materials traded annually, and growing interest in edible packaging—over 500,000 units sold to date.

According to the Sustainable Packaging Coalition (2024), the eco-friendly packaging industry in North America has also become a key employment driver, contributing to over 85,000 jobs, underlining its economic and environmental impact.

Both the United States and Canada play critical roles in supporting the steady growth of the upcycled materials in packaging market in North America, through progressive legislation and sustainability mandates.

In the United States, states like California are leading the charge with some of the strictest packaging regulations in the country. California’s SB 54 law, enacted in 2022, mandates a 25% reduction in single-use plastic packaging by 2032 and requires that at least 30% of plastic packaging be recyclable or compostable by 2028. These regulatory actions are directly encouraging the shift toward upcycled and sustainable packaging alternatives.

Canada has also implemented national-level strategies to tackle plastic pollution. The Canadian government’s Zero Plastic Waste Agenda includes bans on several single-use plastic items and mandates the use of minimum recycled content in plastic packaging. These efforts aim to foster a circular economy and accelerate the adoption of upcycled materials across various industries.

According to Environment and Climate Change Canada (ECCC), these measures are essential to achieving national climate targets and have positioned both countries as leaders in North America’s transition to sustainable packaging.

By Material Type

By Packaging Form

By End-Use Industry

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarUpcycled Materials in Packaging Market