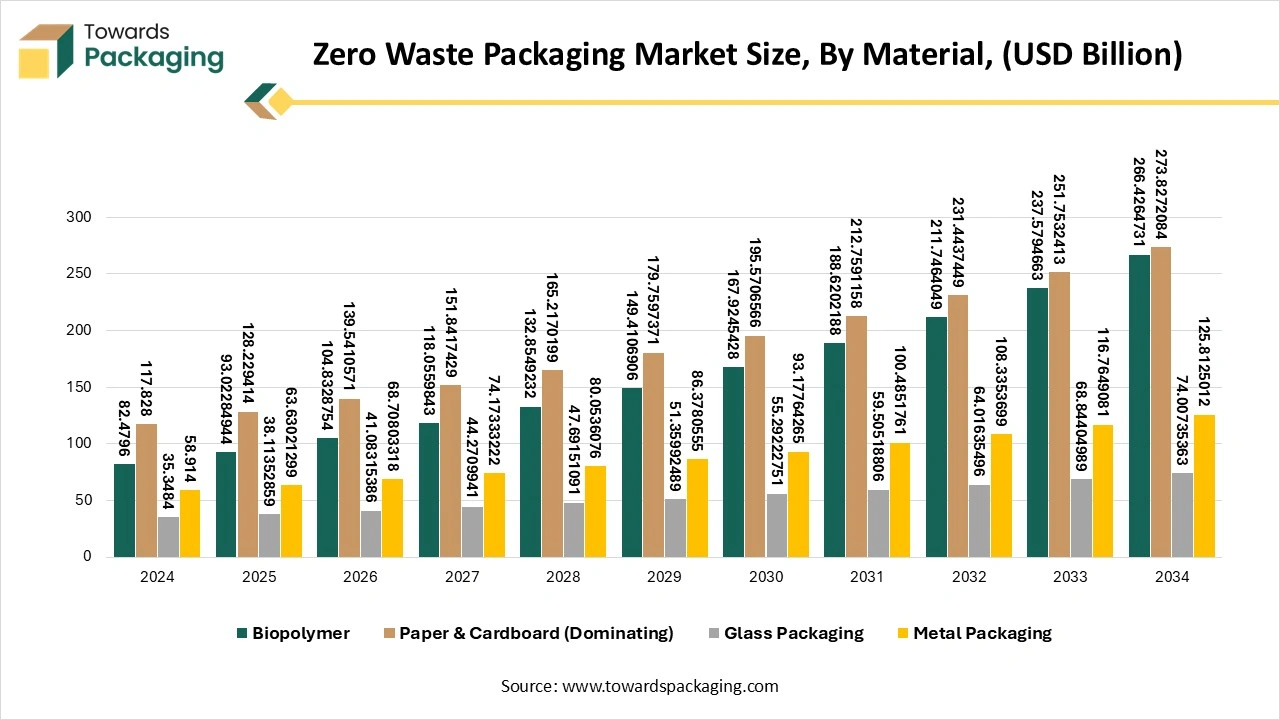

The zero waste packaging market is forecasted to expand from USD 354.17 billion in 2026 to USD 811.49X billion by 2035, growing at a CAGR of 9.65% from 2026 to 2035. This report covers market size, trends, segment analysis (materials, outlook, distribution channels, applications), regional performance across NA, Europe, APAC, Latin America, and MEA, and competitive insights on companies such as Notpla, Loliware, Better Packaging Co., Patagonia, Lifepack, and Noissue. It also includes a full value chain assessment, trade data, manufacturer profiles, supplier mapping, and pricing structures, along with market drivers like circular economy adoption and technology advancements.

This market is proliferating due to the rising concern for sustainable packaging and economical solutions for packaging several products in almost every sector such as food & beverages, pharmaceuticals, e-commerce, and many others. The zero-waste packaging market is also rising due to the continuous effort of market players to reduce carbon emissions and produce environment-friendly packaging products.

Zero waste packaging means recycling and reusing materials for packaging purposes such as using glass milk bottles or any other glass bottles several times repeatedly resulting in reduced wastage of raw materials. The growing concern among consumers regarding eco-friendly packaging of products raises the demand for zero waste packaging. The major motive is to reduce the quantity of waste materials going to landfills and decrease environmental pollution. Government strict rules for packaging industries also influence market players to develop such products that can be recycled multiple times.

The growing awareness among people for the disposal of packaging waste with proper segregation is contributing towards the rise of the growth of the zero waste packaging market. The major market players are focusing on developing products that can be recycled, reused, biodegradable, and should be environmentally friendly in several ways. The continuous contribution of market players to developing edible packaging, biodegradable wrappers, and plant-based plastics. The market is anticipated to grow rapidly during this predicted period as the packaging sector is introducing innovative solutions regularly.

There is a huge upsurge in the demand for recyclable and reusable packaging products in all sectors which influences the growth of zero waste packaging industry. These are cost-effective along eco-friendly which makes them preferable for a wide range of market players. The production of recyclable materials is a cost-effective packaging solution for companies as these require less energy consumption and labour charges for manufacturing these products which ultimately reduces the costs. Usage of organic products such as corn and mushrooms for the production of packaging materials. The market is observing continuous progress and improvements in plans and materials that can lessen the possible threat of eliminating secondary packing. Numerous producers are shifting in the direction of nominal packaging and substituting plastic packaging with glass, paper, wood, and many other sustainable and biodegradable materials.

| Metric | Details |

| Market Size in 2025 | USD 323.00 Billion |

| Projected Market Size in 2035 | USD 811.49 Billion |

| CAGR (2025 - 2035) | 9.65% |

| Leading Region | Asia Pacific |

| Market Segmentation | By Material Type, By Outlook Type, By Distribution Channel Outlook, By Application and By Region Covered |

| Top Key Players | Notpla, Boxed Water Is Better, Lifepack, Loliware, Noissue. |

Rising demand for eco-friendly packaging products due to growing awareness among people towards environmental issues. As the adverse effect of plastic is rising significantly governments as well as customers are trying to adopt methods that can help to lessen such adverse impacts. The rising popularity of the circular economy enhanced the market potential by introducing materials and products that can be recycled reused, and biodegradable which help to reduce waste quantity in landfills. Governments worldwide apply strict regulations and supervision to decrease single-use plastics practices, this has compelled market players to use products that can be recycled and adopted by almost all sectors.

Asia Pacific witnessed the highest revenue share for the year 2025 this growth is due to the presence of several small to medium levels of industries and the increasing demand of customers for eco-friendly packaging of products. As such companies are highly focused on producing packaging products made up of cardboard or paperboard that can be discarded or recycled easily. This promotes the industry to grow rapidly by fulfilling both the demand of the customers as well the government policies associated with the packaging industry. In several countries such as India, Japan, China, South Korea, and Thailand this zero waste packaging sector is expanding rapidly. The innovative packaging solutions incorporated by the e-commerce industry have supported the market to develop exponentially.

Strong Manufacturing Base: Booster of China’s Market

China has a well-established and large base of small and medium-sized manufacturers of paper and cardboard packaging and recycling. The rise of e-commerce has increased demand for packaging solutions. However, the increased awareness of environmental impact and the importance of waste management is driving the trend of zero waste packaging demands in the country.

Europe is estimated to grow at the fastest rate over the forecast period. The growing awareness among people regarding increasing environmental issues and knowledge of preventive measures has influenced this market. Funding from the government and other private firms to develop an eco-friendly packaging solution has supported the market players present in this region to develop the market by fulfilling customers' demands. Several companies collaborating to develop such solutions and reduce single use of plastic. Due to the rising demand major companies are choosing such materials for packaging are using recyclable and biodegradable materials to enhance their brand value.

Robust Regulatory Polices: Leading the UK’s Market

The UK is the major player in the European zero waste packaging market, growth driven by the presence of strong government policies for waste management. The UK has a large sensitivity toward sustainability, which drives demand for eco-friendly packaging solutions. Additionally, the UK’s circular economy to reduce waste and promote sustainable choices are fostering the market.

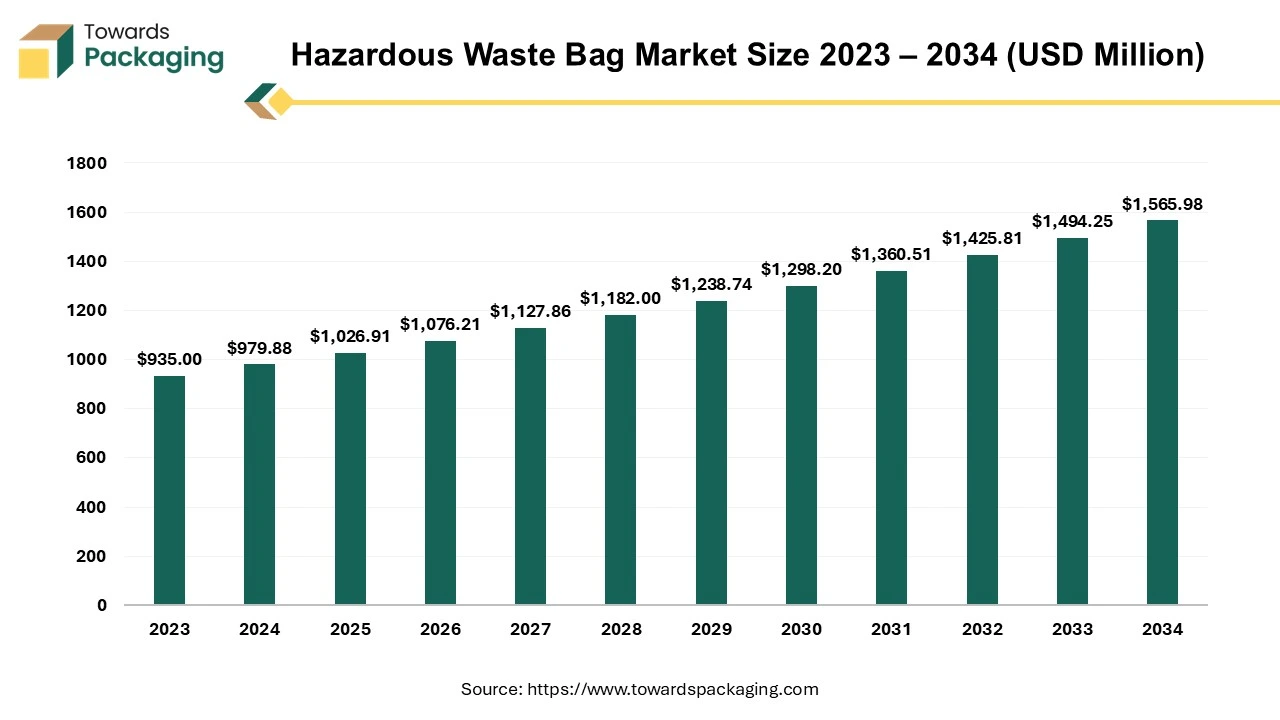

The hazardous waste bag market is projected to reach USD 1565.98 million by 2034, growing from USD 1026.91 million in 2025, at a CAGR of 4.8% during the forecast period from 2026 to 2035.

The key players operating in the market are focused on adopting inorganic growth strategies like acquisition and merger to develop advance technology for manufacturing hazardous waste bags which is estimated to drive the global hazardous waste bag market over the forecast period.

A hazardous waste is any trash that has characteristics that make it potentially damaging to the environment or human health. Hazardous waste can be liquids, solids, gasses, or sludges and is produced by a variety of processes, from batteries to industrial manufacturing waste. Hazardous waste refers to any waste material that is dangerous or harmful to human health or the environment. These wastes can be in solid, liquid, or gas form and are typically generated by chemical, industrial, pharmaceutical, and agricultural activities. Hazardous waste can include substances that are corrosive, toxic, reactive, flammable, or infectious. Due to their potential to cause environmental damage or harm to human health, hazardous wastes must be carefully managed, treated, and disposed of according to strict regulatory guidelines. Examples include used certain industrial byproducts, chemicals, contaminated equipments, and batteries.

The global packaging waste management market is expected to increase from USD 39.78 billion in 2025 to USD 54.21 billion by 2034, growing at a CAGR of 3.5% throughout the forecast period from 2026 to 2035. The global packaging waste management market is growing, driven by rising concerns about addressing rising pollution, rising consumer demand for sustainability, stringent governmental regulations, growing emphasis on circular economy principles, and increasing technological innovation in recycling technologies. Sustainability is increasingly becoming the key focus, encouraging the adoption of packaging waste management practices.

Several key players operating in the packaging waste management market are focused on adopting growth strategies like acquisitions and mergers to develop advanced technology for packaging waste management, bolstering the market’s expansion in the coming years. In addition, the market is expanding exponentially in various developing and developed regions, particularly Asia Pacific, fuelled by the rising focus on sustainability and rising investment in recycling infrastructure.

The global packaging waste management market focuses on the collection, sorting, processing, and disposal or recovery of packaging materials after their intended use. This market is crucial for addressing the growing global issue of packaging waste, driven by the increased consumption of packaged goods and heightened awareness of environmental pollution. It encompasses various strategies, ranging from traditional landfilling and incineration to more sustainable approaches, such as recycling, composting, and waste-to-energy conversion, to minimize environmental impact and promote a circular economy for packaging materials.

The packaging waste recycling market is expected to increase from USD 34.50 billion in 2025 to USD 52.16 billion by 2034, growing at a CAGR of 4.7% throughout the forecast period from 2026 to 2035. The rising awareness towards ecological issues and strict guidelines such as Packaging and Packaging Waste Regulations. With rising ecological cons and strict guidelines, this industry is observing noteworthy development. As industries and government progressively arrange sustainable choices the market is growing significantly. With an increasing focus on circular economy ethics, producers are looking for advanced solutions to decrease carbon footprints of the packaging. This market is dominating in Europe due to presence of market players with goal of waste reduction.

The packaging waste recycling market refers to the industry focused on the collection, sorting, processing, and repurposing of discarded packaging materials into reusable raw materials or new products. It encompasses the recycling of various packaging formats such as plastics, paper & cardboard, metals, glass, and wood, generated from sectors like food & beverages, e-commerce, retail, healthcare, and consumer goods. The market is driven by increasing environmental concerns, stringent government regulations on waste management, rising consumer awareness of sustainability, and the growing demand for recycled materials in manufacturing.

By Material Type

By Outlook Type

By Distribution Channel Outlook

By Application

By Region Covered

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarZero Waste Packaging Market