The plastic liner market is projected to grow from USD 5.6 billion in 2026 to USD 8.5 billion by 2035, registering a CAGR of 4.75% during the forecast period. The plastic liner market report provides detailed insights into market size, segmentation by material type, application, and end-user industries such as e-commerce, food & beverages, and construction. It includes regional analysis across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The study also covers competitive analysis, key company profiles, value chain and supply chain analysis, trade data, and comprehensive data on manufacturers and suppliers. Increasing infrastructure development and rising demand for sustainable liner solutions are key growth drivers.

The plastic liner market refers to protective plastic-based materials used as liners in containers, tanks, bins, packaging, landfills, and industrial equipment to prevent leakage, contamination, and corrosion. These liners are typically made from polyethylene (LDPE, HDPE, LLDPE), polypropylene, PVC, and specialty engineered plastics, providing chemical resistance, moisture barrier properties, durability, and flexibility.

Plastic liners are widely used in waste management, agriculture, food & beverages, construction, mining, chemicals, and logistics. Market growth is driven by increasing demand for safe packaging, rising construction and infrastructure projects, growth in waste management practices, and regulatory compliance for environmental protection.

The incorporation of AI technology in the plastic liner market plays an important role in regulating supply chain distribution process. It is widely used for material development process to generate high-quality plastic liners in the market. AI help in manufacturing sustainable and advanced formulation for plastic which are recyclable and emit low carbon. It ensures timely production with automation tool support which enhance the reliability in this sector.

Rising Focus towards Sustainable Packaging

Increasing emphasis towards development of sustainable packaging has influenced the development of the plastic liner market. With ecological apprehensions gaining importance, industries across businesses are looking for environment-friendly substitutes to traditional packing. Plastic liners provide a durable and lightweight option, decreasing the requirement for extreme packaging resources. Producers are developing to meet the demand for sustainable packaging by inventing with recyclable and recycled materials. As industries manage ecologically responsible choices, the acceptance of plastic liners bring into line with broader company sustainability aim, pushing the market to grow.

Rising Ecological Concern and Packaging Guidelines

The rising concern towards ecological pollution due to plastics and strict guidelines in the packaging sector has hindered the expansion of the market. Governments and supervisory bodies are executing strict guidelines aimed at decreasing single-use plastic liners and reassuring more sustainable substitutes. Plastic liners are a part of the huge plastic ecology, face inspection and calls for substitutes that have lesser ecological influences.

Advancement in Recyclable Resources

The continuous advancement in the recyclable resources has raised the opportunities for the market. With the rising emphasis on sustainability raised the demand for plastic liners which are functional as well as ecologically friendly. Investment in study and development to generate recyclable plastic liners materials with improved performance and durability can open new return streams. Producers that effectively present such environment-friendly resolutions can plea to ecologically conscious customers and increase a competitive advantage in an industry progressively shaped by sustainability apprehensions.

")

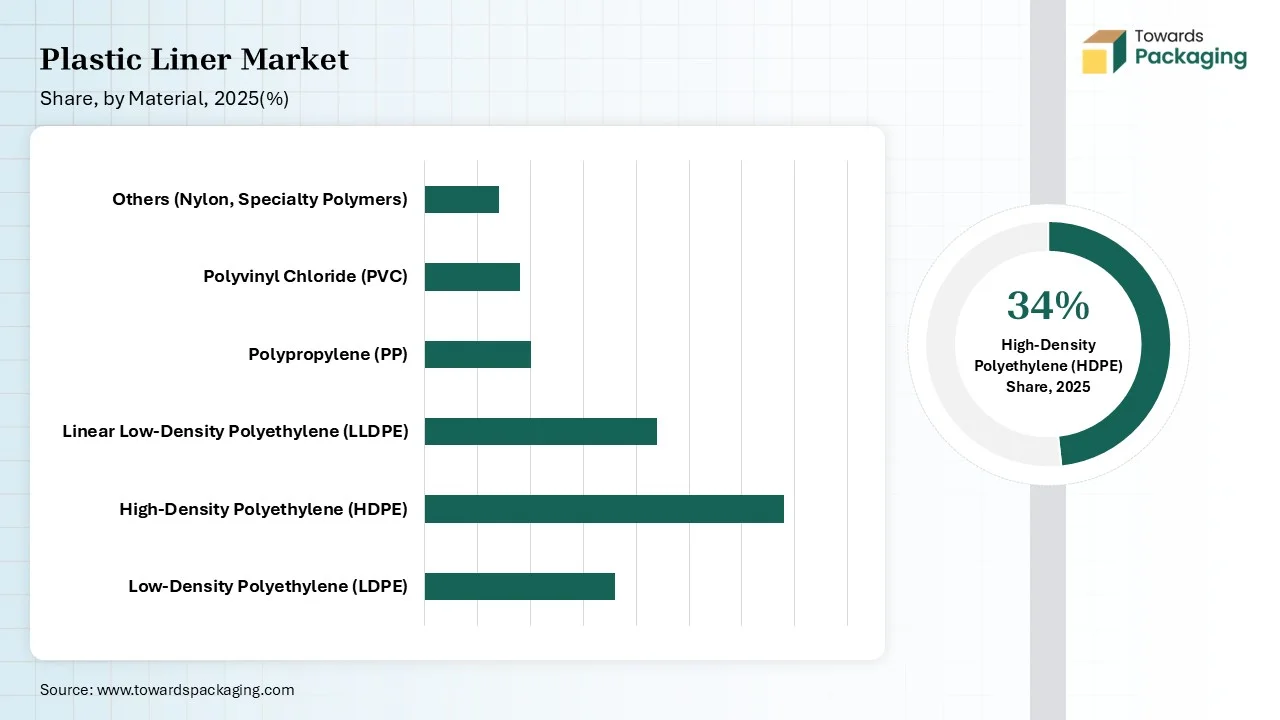

The HDPE segment dominated the market in 2025 due to its chemical resistance, cost-effectiveness, and durable quality. These capabilities make it ideal for storage and containment in industries such as agriculture and waste management sector. This segment is continuously undergoing innovation process which has developed high-performance and eco-friendly liners. It is well-known for its high strength, strong physical security, and striking tensile strength.

The LLDPE segment is expected to grow at the fastest rate in the market during the forecast period of 2026 and 2035. This segment is growing due to its puncture resistance, excellent strength, and flexibility. The toughness of this material provides safety assurance to fragile substances. These can stretch under pressure without breakage and provide a smooth surface for products.

")

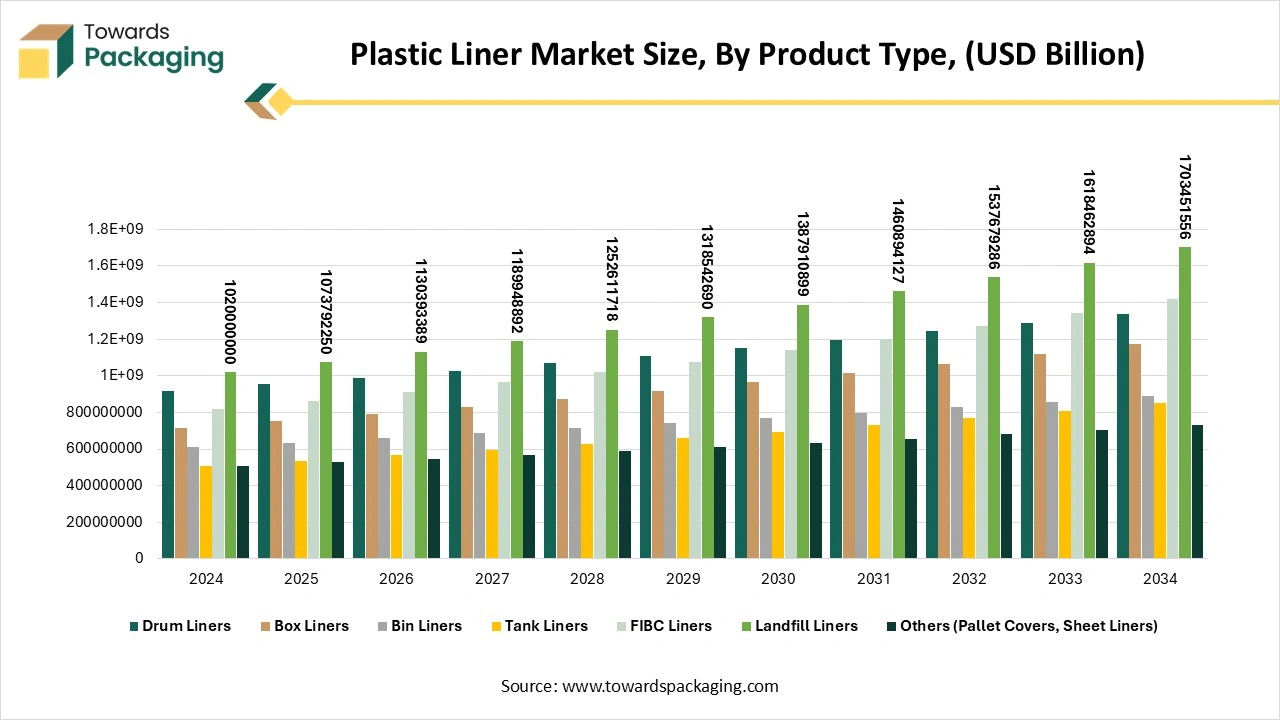

The drum & bin liners segment held the largest share of the plastic liner market in 2025 due to rising industrial and household demand for effectual containment solution, safety, and hygiene. These protect from contamination and corrosion of premium drums and allow to reuse it multiple times. These are versatile and used in various sectors which enhance its production process as well as quality of the liners. It helps in keeping waste products segregated in drums and bins which reduce contamination or spoilage of products.

The FIBC & landfill liners segment is expected to grow at the fastest rate in the market during the forecast period of 2026 and 2035. This segment is growing rapidly due to its cost-efficacy, strict ecological guidelines, and rising industrialization. It provides safety against contamination, moisture, and static discharge which is ideal for various sectors such as pharmaceuticals, food, and chemicals. Increasing infrastructures enhance the usage of these liners for projects such as water management, and various other.

")

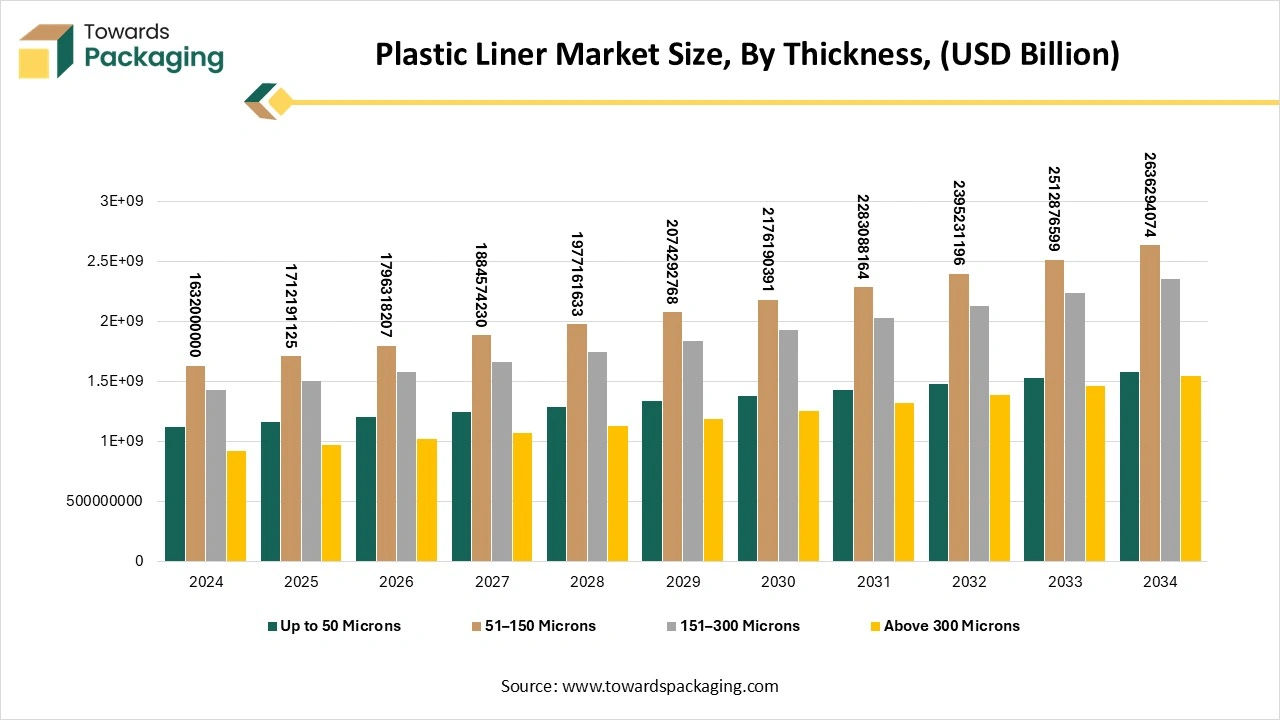

The 51–150 microns segment dominated the plastic liner market in 2025 as it offers flexibility, cost-efficiency, and strength. This thickness is majorly maintained in liners made up of HDPE and LDPE which are utilized for the medium duty requirements in several industries. This thickness is suitable in wide range such as from basic moisture protection to harsh chemicals leakage which enhance its demand in several sectors. These are cost-effective which allow industries to demand high quality liners.

The above 300 microns segment is expected to grow at the fastest rate in the market during the forecast period of 2026 and 2035. This segment is growing due to rising focus on developing durable and high-performance liners. The major driver of this segment is the rapid growth of industrialization, expansion of agricultural sector, and large infrastructures. The expansion of aquaculture industry has also raised the usage of liner with this thickness.

")

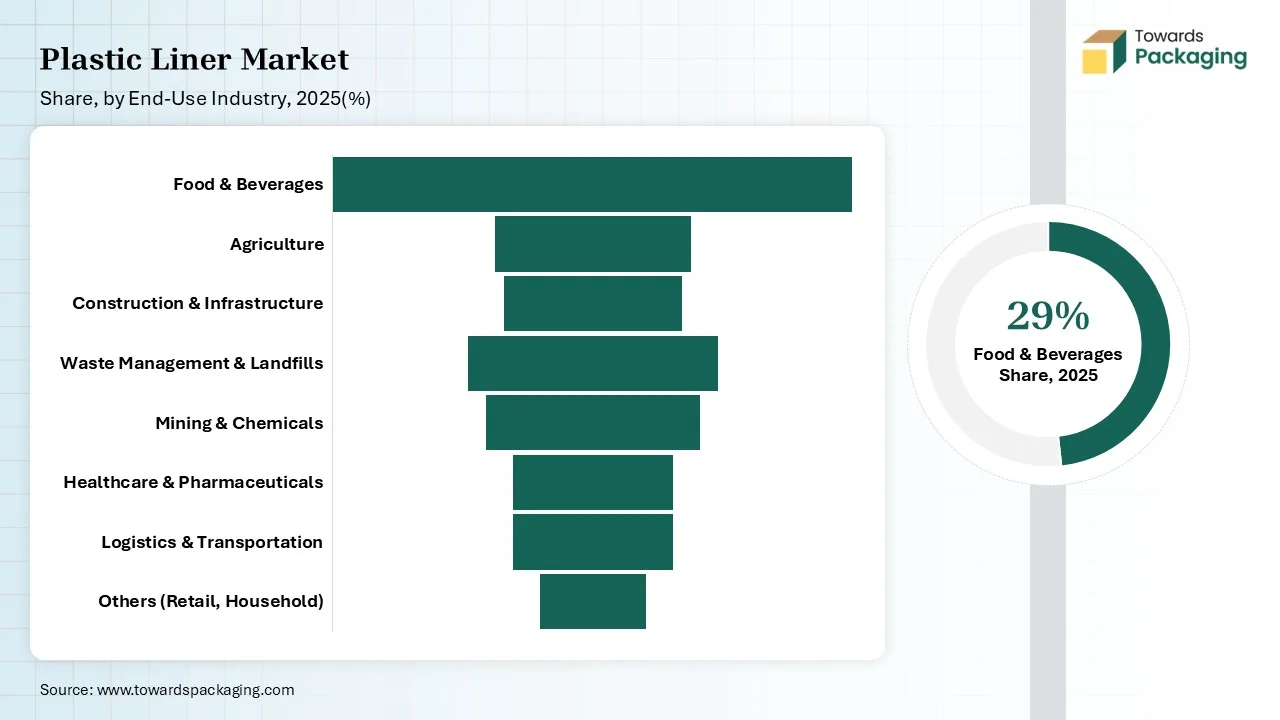

The food & beverages ingredients segment dominated the plastic liner market in 2025 due to rising demand for packaging products. This rising safety standard in this industry has influenced the demand for high-quality liners. Plastic liners protect food products from moisture, oxygen, and light which result in extended shelf life of the products. The increasing versatility and product protection concern has raised the demand for this sector. Advancement in the production process of the plastic liners has enhanced its adoption in this sector.

The waste management & healthcare segment is expected to grow at the fastest rate in the market during the forecast period of 2026 and 2035. This segment is growing due to rising concern for plastic waste generation, ecological issues, and specific healthcare requirements. Healthcare sector utilizes plastic liners for disposal of waste generated and waste management is also essential in this industry to reduce the widespread of infectious diseases. These liners are also utilized in labs, clinics, hospitals, and research centres require management of waste.

")

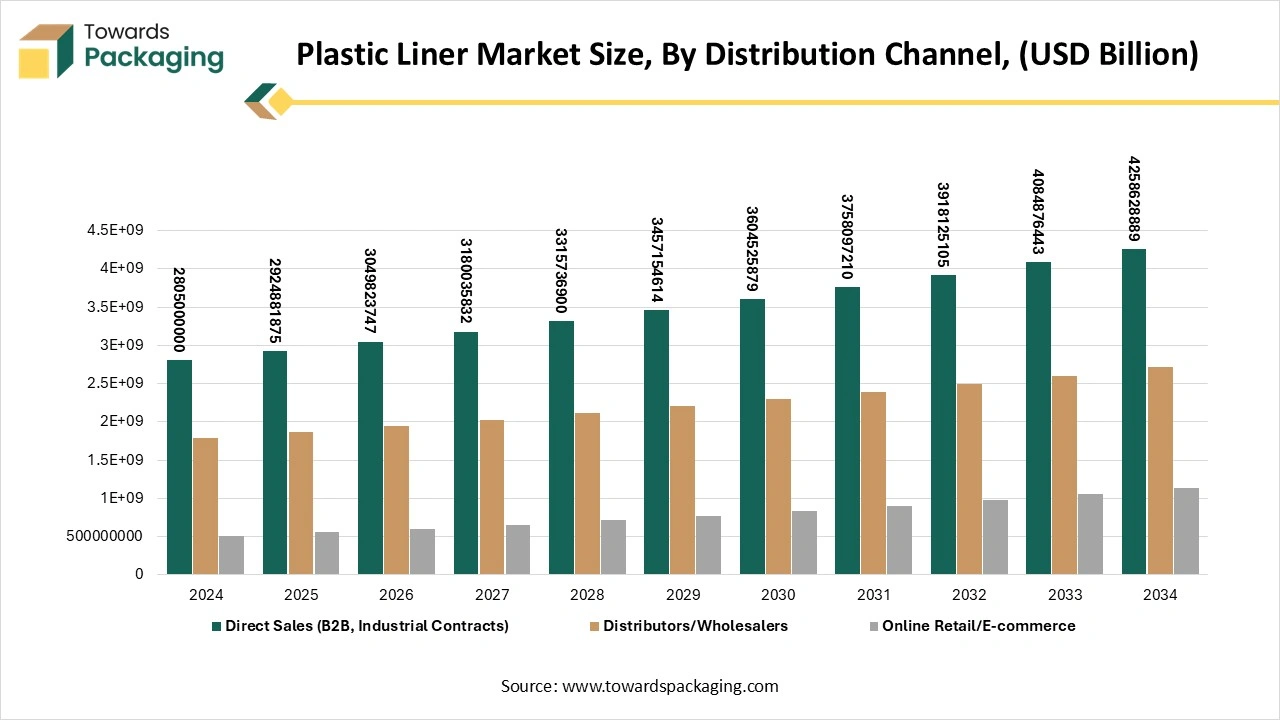

The direct sales (B2B) segment held the largest share of the market in 2025 due to huge requirement for customization and customer relationships. This segment is widely utilized by manufacturers, wholesalers, and distributors to generate high profit margin. It offers huge customization option to meet the demand of the consumers from several industries. It provides excellent technical support and consultation to the customers majorly for high-performance or complex polymers.

The online retail/e-commerce segment is expected to grow at the fastest rate in the market during the forecast period of 2026 and 2035. This segment is growing rapidly due to its low-cost transportation, lightweight, and durable properties. The rapid expansion of e-commerce sector and increasing reliance of consumers for home delivery of products has raised the demand for plastic liners in this sector.

")

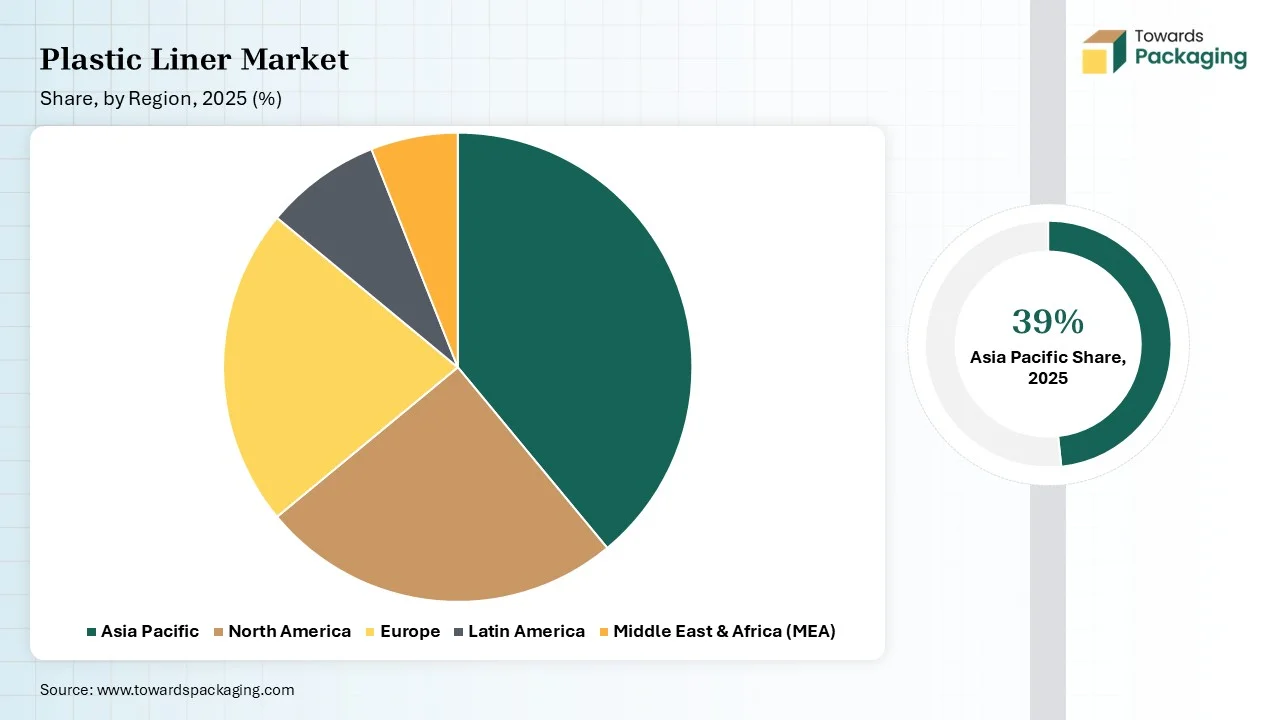

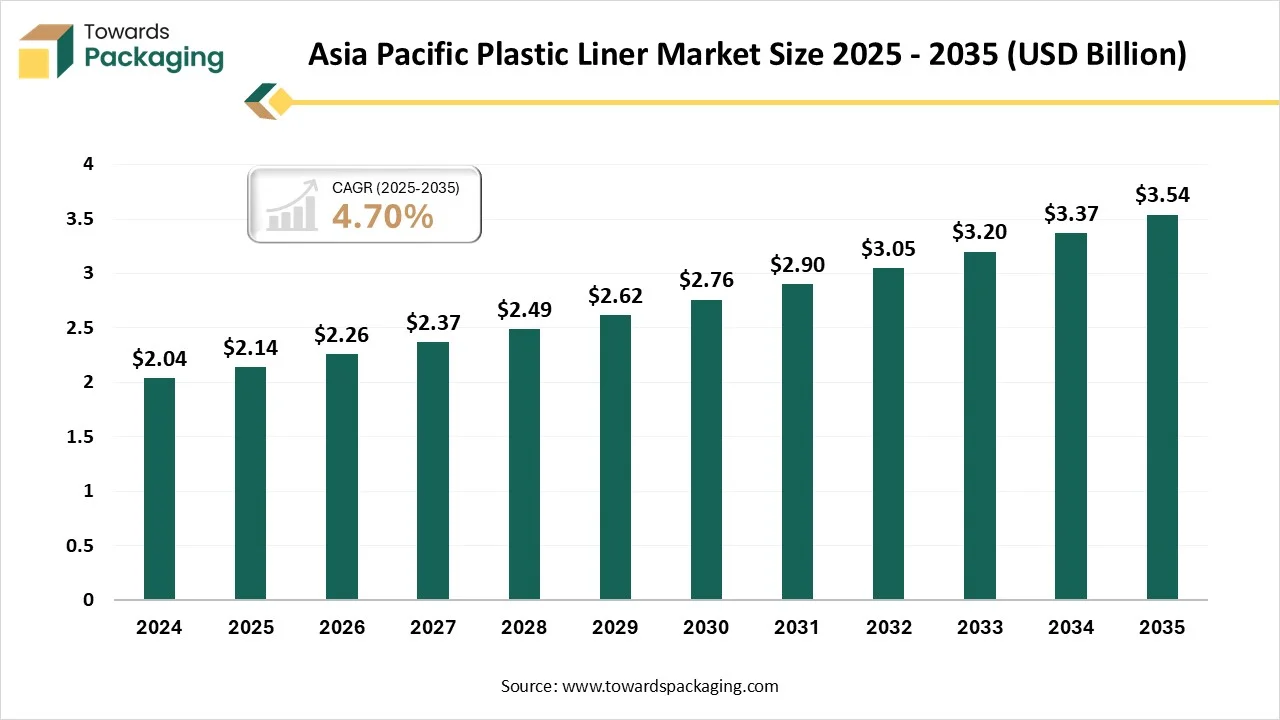

Asia Pacific held the largest share of the plastic liner market in 2025, due to the presence of strong industrial output and rapid urbanization. The rising demand for plastic liners in industries such as packaging, agriculture, food & beverages, and construction. Huge investment in the infrastructure development raised the construction work in countries like China and India boost the demand for plastic liner with enhanced quality. Government strategies encourage the waste management policies which push the market to develop rapidly.

Presence of huge manufacturing capacity has raised the expansion of the market in China. The advancement in the technology, manufacturing capacity, and cost-effective production process has pushed the market to develop significantly. China has a large consumer for plastic packaging which drive the production process.

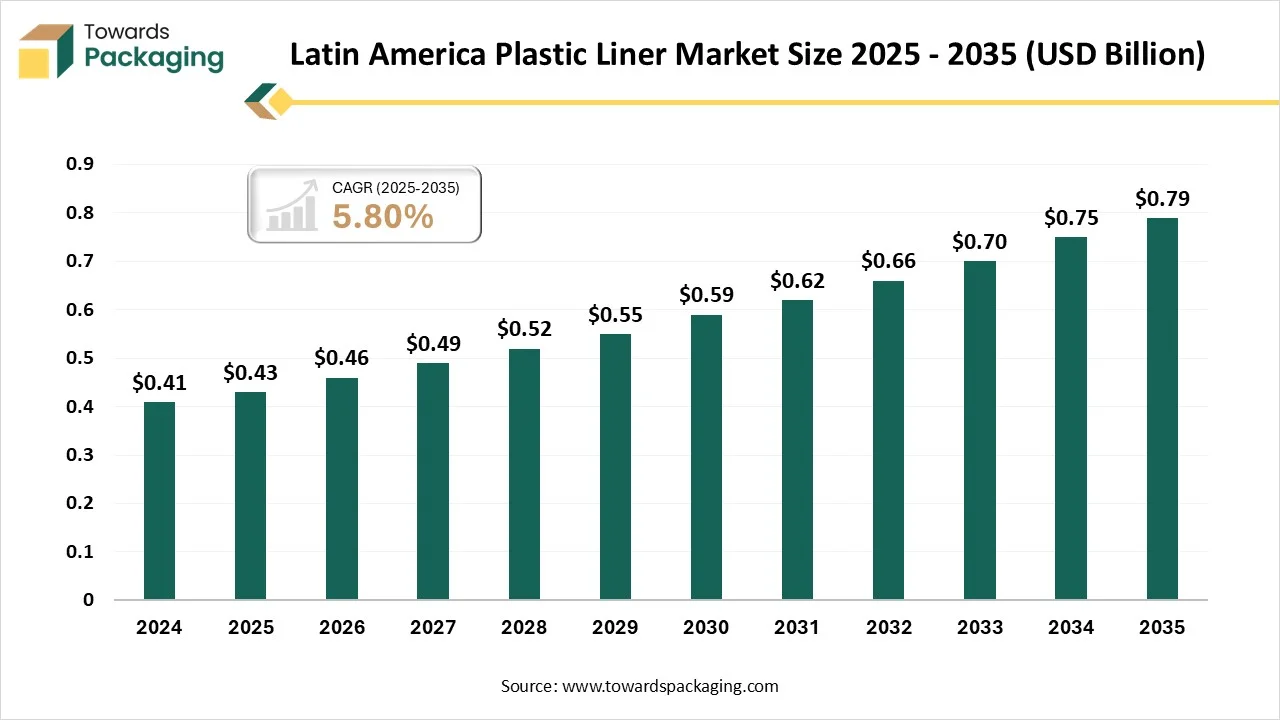

Latin America expects the significant growth in the market during the forecast period. The rising export business of various sectors has enhanced the demand for plastic liners such demand raise the growth of this market. Supervisory changes in the direction of circular economy practices have created opportunities for invention and environment-friendly packaging solution. The rapid expansion of packaged food products demand has enhanced the demand for such liners to preserve food from contamination.

The raw materials used in this market are majorly Low-Density Polyethylene (LDPE) , High-Density Polyethylene (HDPE), Linear Low-Density Polyethylene (LLDPE), Polypropylene (PP) and Polyvinyl Chloride (PVC).

It comprises a wide range of processes and products starting from industrial transportation bags to special containment process.

It manages the supply chain process that comprises of raw materials procurement, manufacturing and in-plant logistics, and finished goods distribution.

By Material

By Product Type

By Thickness

By End-Use Industry

By Distribution Channel

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarPlastic Liner Market