North America Food Packaging Market Size, Share, Trends and Forecast Analysis

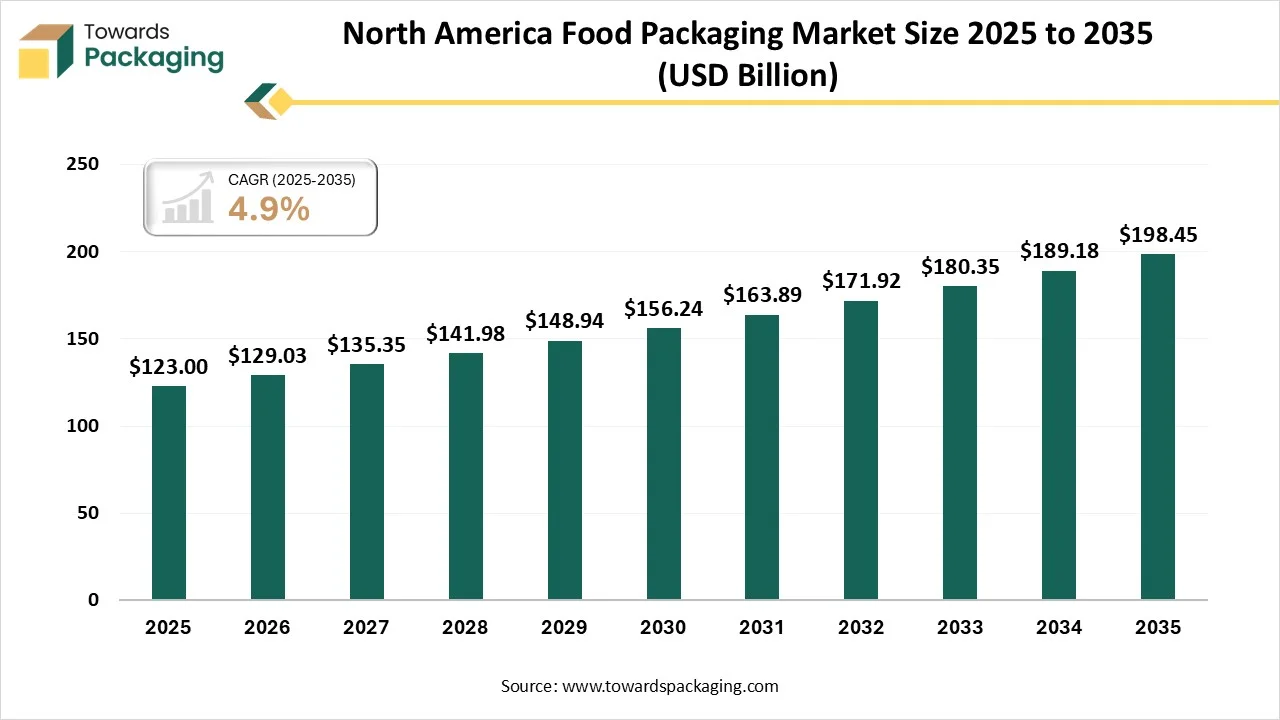

The North America food packaging market is forecasted to expand from USD 129.03 billion in 2026 to USD 198.45 billion by 2035, growing at a CAGR of 4.9% from 2026 to 2035. The urge for food packaging is due to busy and easy -focused lifestyles that drive ready-to-eat (RTE) meal consumption and big demand for food security.

Major Key Insights of the North America Food Packaging Market

- In terms of revenue, the market is valued at USD 123 billion in 2025.

- The market is projected to reach USD 198.45 billion by 2035.

- Rapid growth at a CAGR of 4.9% will be observed in the period between 2026 and 2035.

- By material type, the plastics segment dominated the market with approximately 40.8% share in 2025.

- By material type, the compostable materials segment will be growing at a significant CAGR between 2026 and 2035.

- By packaging type, rigid packaging segment dominated the market with approximately 58.1% share in 2025.

- By packaging type, flexible packaging segment will be developing at a main CAGR between 2026 and 2035.

- By technology, traditional packaging segment dominated the market with 62% share in 2025.

- By technology, smart & active packaging segment will be growing at a significant CAGR between 2026 and 2035.

- By application, the bakery & confectionery segment dominated the market with approximately 38.8% share in 2025.

- By application, the ready-to-eat meals segment will be developing at a significant CAGR between 2026 and 2035.

What is the North America Food Packaging Market?

The North America food packaging market encompasses the production, distribution, and application of packaging materials and solutions designed specifically for food products across the United States, Canada, and Mexico. This market includes a wide range of packaging types such as rigid plastics, flexible films, paper and paperboard, glass, metal, and innovative sustainable solutions used to protect, preserve, transport, and display food items from manufacturers to end consumers.

Trends in the North America Food Packaging Market

- Smart and Connected Food Packaging: Technology plays an important role in designing the current food packaging trends, specifically as brands concentrate on safety, traceability, and transparency. Smart packaging solutions are excessively used to develop how food packaging communicates information.

- Convenience-Focused Food Packaging: Convenience-driven usage is developing due to updated lifestyles, on-the-go eating habits, and smaller households, which are updating food packaging needs. Packaging is now predicted to assist with effective storage, convenient handling, and repeat usage.

- Smart Space Optimisation in Food Packaging: Space smoothness has become a step-by-step focus as brands are giving importance to packaging that lowers space usage without increasing material consumption. Fixed retail locations and growing logistics are updating this move.

- Sustainability- focussed Food Packaging: Sustainability has developed from a value-added to a main need in the food sector. Food brands accept materials and designs that match well with sustainable packaging trends, which update material usage and improve recyclability.

Technological Developments in North America Food Packaging Market

Active packaging counts on materials that communicate with the food or its surroundings to maintain freshness. Moisture absorbers, oxygen scavengers, and antimicrobial films assist in preventing bacterial development and daily spoilage. Such antimicrobial packaging solutions lower food waste and lower the demand for artificial preservatives. Nanotechnology is coming as an updated strategy for food protection. Nano-coatings on packaging materials make antimicrobial barriers that protect against bacterial growth and oxidation. Additionally, nano-encapsulation procedures also enable the controlled release of antimicrobials and antioxidants to store food for a longer time.

Major North American Private Industry Investments for Food Packaging

- Sealed Air acquisition by CD&R – Private equity firm Clayton, Dubilier & Rice acquired Sealed Air Corporation in a roughly $10.3 billion buyout to accelerate innovation and strategic growth in food and protective packaging.

- Platinum Equity investment in Norton Packaging – Platinum Equity made a growth investment in Norton Packaging to support product innovation, footprint expansion, and potential add-on acquisitions in rigid plastic and food-related packaging.

- PPC Flex acquires SÜDPACK’s U.S. operations – The GTCR-backed PPC Flex platform expanded its North American flexible packaging capabilities by acquiring SÜDPACK’s U.S. facility, boosting printing and conversion capacity for food packaging.

- Amcor expands PCR production capacity – Amcor plc invested in increasing post-consumer recycled (PCR) materials production in Kentucky to meet rising sustainable food packaging demand.

- Sonoco expands U.S. manufacturing operations – Sonoco Products Company committed a $30 million investment to expand adhesives and sealants production across multiple U.S. facilities to support food packaging growth.

- Pactiv Evergreen’s integration with Novolex – Novolex completed a $6.7 billion acquisition of Pactiv Evergreen, creating one of North America’s largest food packaging manufacturers with a broader production scale.

- Plastipak expands Louisiana facility – Plastipak Packaging Inc. announced a $53.8 million expansion project in Louisiana to add production lines and recycling capabilities for rigid food-grade containers.

Trade Analysis of the North America Food Packaging Market: Import & Export Statistics

- According to the U.S food packaging import data between July 2025 and June 2025, the buyers have globally imported 9,942 shipments.

- Such shipments were being promoted by 9,942 exporters and being purchased by 8,458 official global buyers, which shows a 14% development compared to the last twelve months.

- Russia, Vietnam, and Colombia have come up as the top three US food packaging importing countries.

- China, Vietnam, and the European Union are the top 3 exporting countries.

- Vietnam has exported 74,956 shipments, China has also exported 66,352 shipments, and the European Union has exported 12,551 shipments, ranking as the biggest worldwide U.S food packaging exporters.

North America Food Packaging Market - Value Chain Analysis

- Package Design and Prototyping: Packaging is a crucial part of food branding, which behaves as both a protective surface and a marketing machine. It includes brand identity by using consistent fonts, colors, and design factors that match the brand’s image. Apart from just aesthetics. Perfect packaging defines the story and features the product's advantages and conveys the brand’s value.

- Recycling and Waste Management: Containers and packaging of a food are totally responsible for almost 45% of the materials included in the United States, and some of these avoided materials which are linked to food containers and packaging. To less food reaching landfills, helping communities and save money , so the U.S. Environmental Protection Agency have started the Food Recovery issue.

- Logistics and Distribution: Ready-to-ship packaging is the actual future of food packaging logistics. Such boxes can be stored smoothly and are crafted to be shipped and picked quickly. Whether it’s for a local delivery purpose of fresh food or for products that are being shipped throughout the country, whenever the products are in ready-to-ship packaging, the operation can become smoother.

Segmental Insights

Material Type Insights

How Plastics Segment Dominated the North America Food Packaging Market in 2025?

The plastics segment dominated the North America food packaging market with approximately 40.8% share in 2025, as polyethylene terephthalate (PET) is prevalently used for food packaging material. They are usually lightweight, transparent, and rigid, which makes it possible to watch them in grocery stores for the packaging of fruits such as cherry tomatoes. As it is recyclable packaging, this material is used for food packaging for online fascinating cuisines like salads, cakes, and bread as well. It efficiently stores carbon dioxide in carbonated beverages through avoidance.

The compostable materials segment is projected to witness the fastest CAGR during the forecast period. PLA has shown that it's a perfect material option for a thermoforming and sheet extrusion die due to its power and performance outcomes. It is manufactured from annually renewable resources. PLA comes to brands and users who select to utilize a third-party certified compostable and safe packaging, which is 100% biobased and low-carbon packaging materials, allowing the changing of both packaging and food scraps, which are far from landfills, into a stretching industrial composting design.

Packaging Type Insights

How Rigid Packaging Segment Dominated the North America Food Packaging Market in 2025?

The rigid packaging segment dominated the market with approximately 58.1% share in 2025, as it is filled with a variety of rigid and non-bendable materials. They are the backbone of rigid packaging that needs minute care during production. Its overall meaning is to protect the ingredients from an external mechanical pollutant, to protect the product’s structural design, and to develop the appearance and aesthetics of the product on the shelves. Organizations serve a wide range of commercial and industrial uses for good-quality rigid packaging.

The flexible packaging segment is projected to witness the fastest CAGR during the forecast period. This packaging points to any packaging created from pliable or flexible materials. It classifies rigid packaging, such as plastic containers and glass bottles, that cannot be conveniently folded. The initial defining feature of flexible packaging is reliability. Additives such as aluminum foil, polyvinyl chloride (PVC) and ethylene vinyl alcohol can be used as flexible packaging materials. Flexible packaging is meant to serve convenient usage, extended shelf life, and perfect preservation for the product, along with easier availability for the user.

Technology Insights

How Traditional Packaging Segment Dominated the North America Food Packaging Market in 2025?

The traditional packaging segment dominated the market with a share of approximately 62% in 2025, as this packaging is a material and procedure that is greatly used for a long period of time, particularly for those who depend on non-renewable resources. Such packaging types are initially crafted to protect the shelf's life, lower the spoilage, and easily promote mass manufacturing and transport. This packaging is frequently inexpensive. Furthermore, it tends to be made from petroleum-based resources and non-renewable sources.

The smart and active packaging segment is projected to witness the fastest CAGR during the forecast period. Active packaging systems operate by including materials that actively communicate with the ingredients of the package. Such systems can release or absorb various materials present in the packaging environment, which leads to the development of sensitive products. Oxygen scavengers play a crucial role in the active packaging systems, which are crafted to stretch shelf life. They are the real materials that consume oxygen present in the package to make a low-oxygen environment.

Application Insights

How the Bakery and Confectionery Segment Dominated the North America Food Packaging Market in 2025?

The bakery and confectionery segment dominated the market with approximately 38.8% share in 2025 because brown paper is a grounded material which is a classic selection for its cost-effectiveness, simple appearance, and surprising reliability as a reliable option in the real insight of the bakery packaging industry. Hence, while brown paper is reliable in some aspects, it can be less susceptible to moisture, oil, and heavy handling, which can affect the product’s freshness and quality. Vacuum-packed bags are another option as they take protection step further by avoiding air from the packaging, which mainly prevents the development of mold and aerobic bacteria.

The ready-to-eat meals segment is projected to witness the fastest CAGR during the forecast period. Advanced sealing procedures are important. Inventions in hermetic seals and the modified atmosphere packaging (MAP) make sure that oxygen is minimized, hence extension of shelf life, and managing nutrition and flavor is crucial. Such procedures protect the entry of environmental contaminants and microbes that assist in retaining safety and freshness. Such developments are important in making sure that users receive high-quality meals each day.

Country Level Insights

How the United States Dominated the North America Food Packaging Market?

The United States dominated the North America food packaging market with approximately 84.5% share in 2025, as it is a vital industry within the huge food sector, which is classified by constant invention and growing user choice. It includes a huge range of materials and technologies whose goal is to protect food quality, ensure safety, and develop the shelf life of the product. As the user's urge for sustainability, convenient nature, and health-conscious products develops, the market is experiencing main growth which is driven by regulatory changes, technological advancements, and the moving sector dynamics. Organizations are funding environmental packaging materials, such as recyclable and biodegradable solutions, which can match the eco-friendly conscious users and comply with regulatory requirements.

Trend of Food Packaging Market in Mexico

The Mexican food packaging industry is initially being driven by growing urbanization and updated user lifestyles, which demand portability and convenience in the food products. The growing disposable incomes allow users to spend more on packaged foods, which boosts the demand. Furthermore, the growth of the retail industry, which includes convenience stores and supermarkets, increases the packaging needs. The expanding food processing sector, which is linked with a developing choice for branded and packaged foods, further completes market development.

Recent Developments in the North America Food Packaging Market

- In June 2025, BiOrigin Specialty Products (BOS), a top producer and transformer of sustainable specialty papers in North America, revealed an latest oil and grease-resistant (OGR) paper.

- In June 2025, Sonoco launched paper can, which is conveniently accessible in North America and created with dual importance on sustainability and functionality, is completely made from 100% recycled fiber, which are 90% sourced from post-consumer materials.

- In July 2025, Sappi North America disclosed that it had delivered commercial products after officially finishing Project Elevate. Such a $500 million project has stretched and transformed Paper Machine No.2 at the location of Somerset Mill in Maine.

Top Companies in the North America Food Packaging Market & Their Offerings

Tier 1:

- Amcor plc – Supplies a broad range of flexible and rigid food packaging solutions in North America, including films, bags, pouches, and containers for snacks, dairy, fresh produce, and other packaged foods that emphasize sustainability and recyclability.

- Ball Corporation – Provides recyclable aluminum food and beverage packaging, especially metal containers and cans, that help preserve product quality and support sustainability goals.

- Berry Global Group, Inc. – Produces rigid and flexible plastic packaging such as containers, trays, films, closures, and foodservice products used widely across food and beverage applications.

- WestRock Company – Offers paper-based food packaging products like take-out containers, cartons, and sustainable fiber packaging that protect and transport packaged foods.

- Sealed Air Corporation – Delivers food packaging materials and systems, including Cryovac® films, bags, and equipment that extend shelf life, enhance food safety, and reduce waste in processing and retail.

- Sonoco Products Company – Supplies diverse food packaging formats such as rigid paper and metal cans, plastic containers, and protective packaging that maintain food freshness and brand appeal.

- Crown Holdings, Inc. – Manufactures metal food packaging, including aluminum and steel cans and closures that ensure product protection and shelf stability for a wide range of food products.

Tier 2:

- Pactiv Evergreen Inc

- International Paper Company

- Printpack Inc.

- Winpak Ltd

- ProAmpac

- Graham Packaging Company

- Silgan Holdings Inc.

- Huhtamaki Oyj (North American Operations)

North America Food Packaging Market Segmentation

By Material Type

- Plastics

- Compostable Materials

- Paper & Paperboard

- Metal

- Glass & Others

By Type

- Rigid Packaging

- Flexible Packaging

By Technology

- Traditional Packaging

- Smart and Active Packaging

By Application

- Bakery & Confectionery

- Ready to Eat Meals

- Dairy Products

- Meat, Poultry & Seafood

- Fruits & Vegetables

- Others (Sauces, Baby Food)