The pharmaceutical polymer vials market presents a detailed examination of global market size, growth patterns, and future opportunities, covering all major segments such as polymer type, application, capacity, sterilization method, end user, and distribution channels. The report also provides regional insights covering North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. It includes competitive benchmarking of top companies, deep value chain mapping from raw material suppliers to end-product distributors, trade flow statistics, manufacturing footprints, and supplier networks, along with all relevant quantitative and statistical data.

Pharmaceutical polymer vials are containers made from advanced polymer materials (such as COP, COC, and polypropylene) used to store injectable drugs, biologics, and vaccines. These vials offer superior chemical resistance, reduced breakage risk, and better drug compatibility compared to traditional glass vials. They are widely used in biotechnology, pharmaceutical manufacturing, and clinical trials due to their lightweight nature, scalability, and sterility support.

The incorporation of AI in the pharmaceutical polymer vials market plays an important role to enhance the production and development process of vials. AI is widely used for quality controlling, personalized medicine packaging, and selection of materials. It reduces the downtime and confirms regular production of the vials. Such advanced technology is extremely used for customization of vials or product packaging required for the treatment procedure.

Increasing Demand for Biosimilars and Biologics Boost the Pharmaceutical Polymer Vials Market Development

The increasing demand for biosimilars and biologics has driven the market to grow significantly. This type of packaging ensures integrity and stability of the quality of the drugs. The increasing ratio of chronic diseases such as diabetes, cancer, and various other enhance the requirement of injectable drugs which result in rising demand for advancement in vials. Rising guidelines for safety of drugs and innovation in the polymer materials has driven the growth of this market.

Volatility in Charges of Raw Materials Hindered the Pharmaceutical Polymer Vials Market Growth

The volatility in the charges of raw materials restraint the market. Continuous competition between raw materials such as glass, plastics and other material hinder the growth of this market. It has been a challenge for the market to maintain the quality of the vials and making it leak-proof which hinder the development of this market.

Rising Acceptance for Advanced Polymer Enhanced the Opportunities of the Pharmaceutical Polymer Vials Market

The increasing acceptance for advanced polymer enhanced the opportunities of the market. The growing occurrence of chronic diseases and the expansion of new injectable treatments boost the demand for polymer vials. Single-dose polymer vials are gaining approval because of their enhanced sterility and decreased risk of pollution, additionally influencing market extension. This tendency alone is projected to enhance hundreds of millions of components to yearly demand in the upcoming period. Growing ecological apprehensions are boosting the producers in the direction of accepting environment-friendly polymers and supportable engineering choices.

Why COP Segment Dominated the Pharmaceutical Polymer Vials Market In 2025?

The COP segment dominated the market in 2025 due to the superior quality packaging. These are dominating in the plastic vials or ampoules market as it is considered as high-quality material. It provides resistance from chemicals, and protect pharmaceutical products from various factors such as light, moisture, and oxygen. This material provides high durability, safety, and purity to the product.

The COC segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. It is due to its suitability and exclusive properties for sensitive biologics and drugs. These are also useful in enabling visual inspection and optical clarity of the contents. Increasing demand for biocompatible materials in the pharma industry has raised the utilization of this material.

The injectable drugs segment held the largest share of the pharmaceutical polymer vials market in 2025 due to rising utilization of injectable drugs. Increasing prevalence of chronic diseases such as diabetes, cancer, and several other diseases. The growing treatment like gene therapy and biologic drugs is highly contributing towards the increasing demand for vials manufacturing. The rising trend towards single-dose vials has influenced the growth of this segment significantly.

The biologics segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. This segment comprises vials which are made up of cyclic olefin polymers and polypropylene which enhance the demand for this segment. These are widely utilized due to their compatibility with biologics and has the capacity to maintain the stability of the drugs.

")

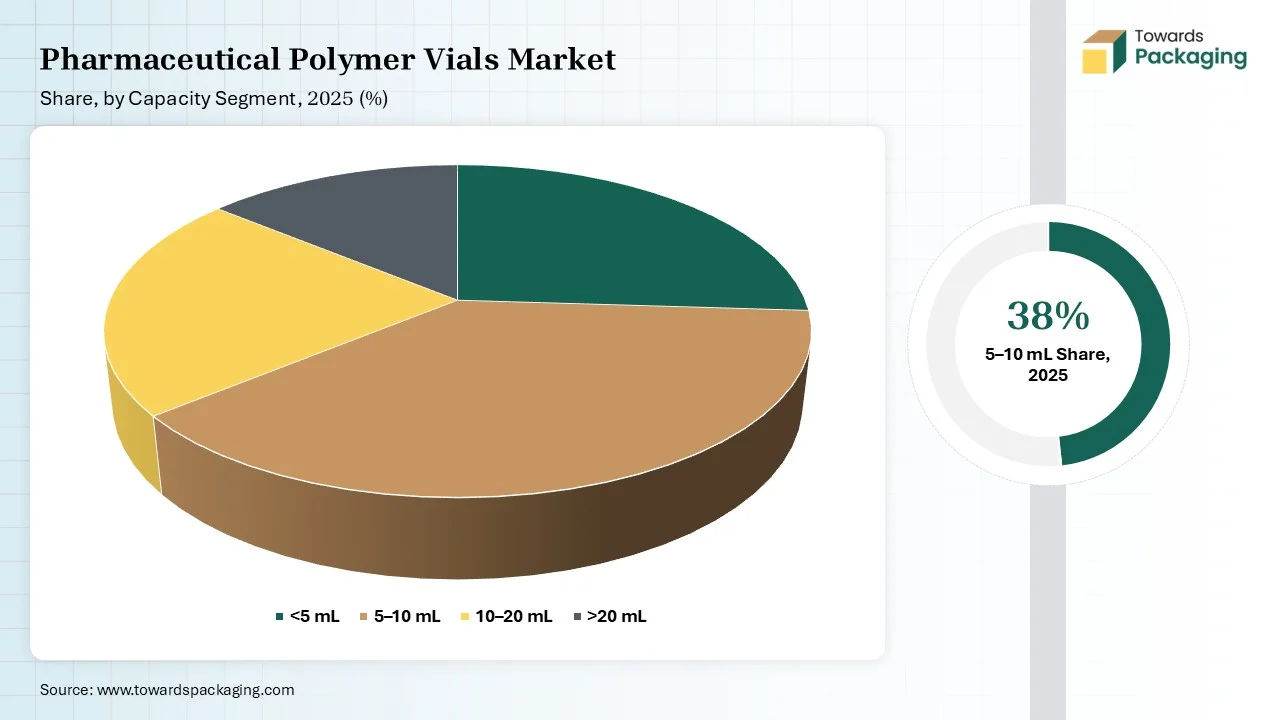

The 5–10 mL segment held the largest share of the market in 2025 due to its versatility and utilization in several places like hospitals, clinics, and many other. The rising demand towards low-dosage therapy and personalized treatment has raised the influence of this segment. The increasing focus towards reduction of contamination as well as wastage of raw materials has raised the production of such vials with 5-10 ml capacity.

The <5 mL segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. This segment is experiencing robust growth due to the increasing demand for unit dose packaging of the drugs. These are widely utilized for sample preservation, and customized therapeutics. It decreases the wastage of drugs and enhances delivery safety. The rapid growth in commercial drug manufacturing, drug development, and clinical trials has helped this segment to develop significantly.

The gamma radiation segment dominated the market in 2025 due to increasing material modification and sterilization process. It offers a wide range of pharmaceutical benefits such as sterilization of medical devices and implants. It reduces the influence of toxicity due to chemicals used in the pharmaceutical industry. It provides benefits such as isothermal character, low validation demand, high-volume processing, better penetration, and no residues.

The electron beam segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. This segment is rising significantly due to the continuous advancement in the technology. It is a process used for sterilizing polymer vials and various single use medical equipment. It utilizes high-energy electrons for the sterilization and penetration process which is efficiently troublemaking DNA of microorganisms. These are durable, safe, and cost-efficient solution for polymer vials.

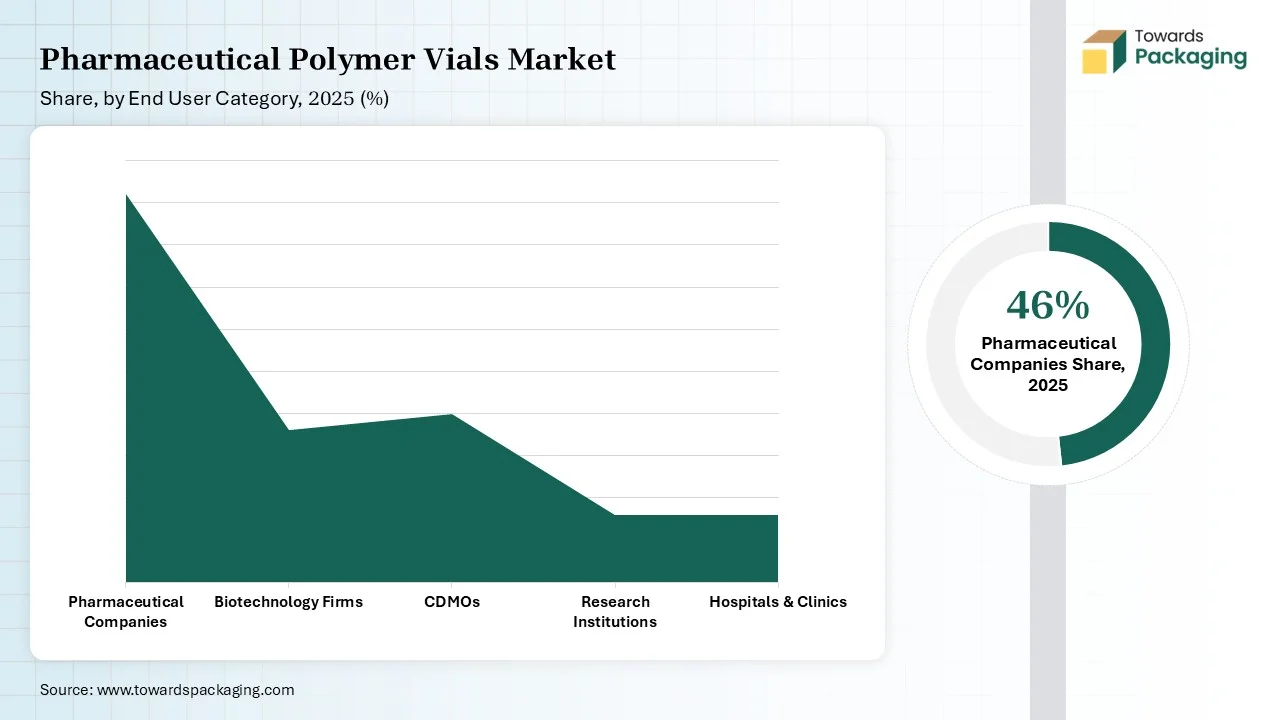

Why Pharmaceutical Companies Segment Dominated the Pharmaceutical Polymer Vials Market In 2025?

")

The pharmaceutical companies held the largest share of the market in 2025 due to dispensing of vaccines, injectable medicines, and several other powder or liquid medications. This segment is concentrating on technological advancement like enhanced sterilization process, digitalization, and several other technologies. Major market players such as Nipro, Amcor, Gerresheimer, Stevanato Group, and many others are continuously enhancing technology for packaging of drugs. They also focus majorly towards safety and efficacy of the packages.

The CDMOs segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. This segment is increasing significantly due to increasing demand for injectable medicines mainly its sterilization process. The continuous advancement in the packaging technology has evolved this segment development rapidly. It provides special infrastructure for methods such as sterile filling which plays a crucial role in injectable medication.

Why Direct Sales Segment Dominated the Pharmaceutical Polymer Vials Market in 2025?

The direct sales segment dominated the market in 2025 due to the close relationship establishment between companies and consumers. It helps to maintain the transparency in the market and enhance the reliability. It provides flexibility and helps in customization of the vials as per requirement. The increasing demand for injectable drugs has raised this segment due to high production and supply process.

The online platforms segment is expected to grow at the fastest rate in the market during the forecast period of 2026 to 2035. The rising trend for telemedicine has influenced the development of online platforms. The increasing convenience in accessibility of the medicines has encourage online ordering facility which led to the enhancement of the online medicine distribution portals.

")

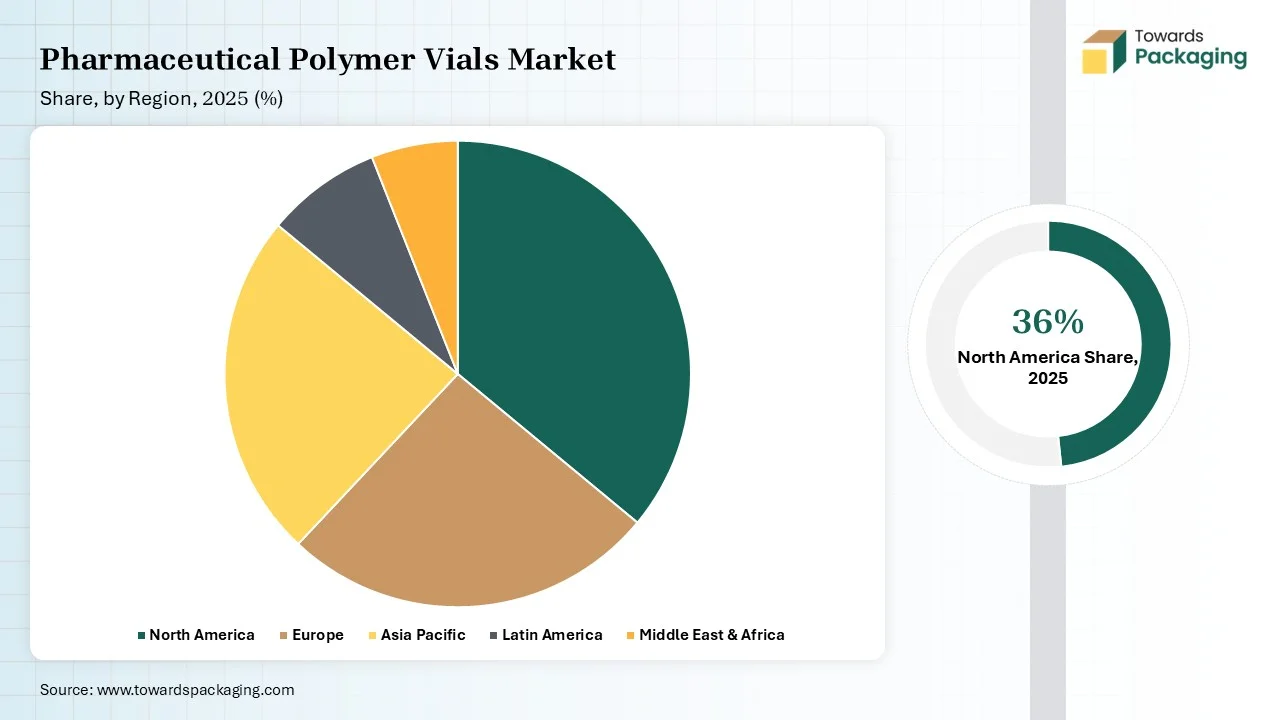

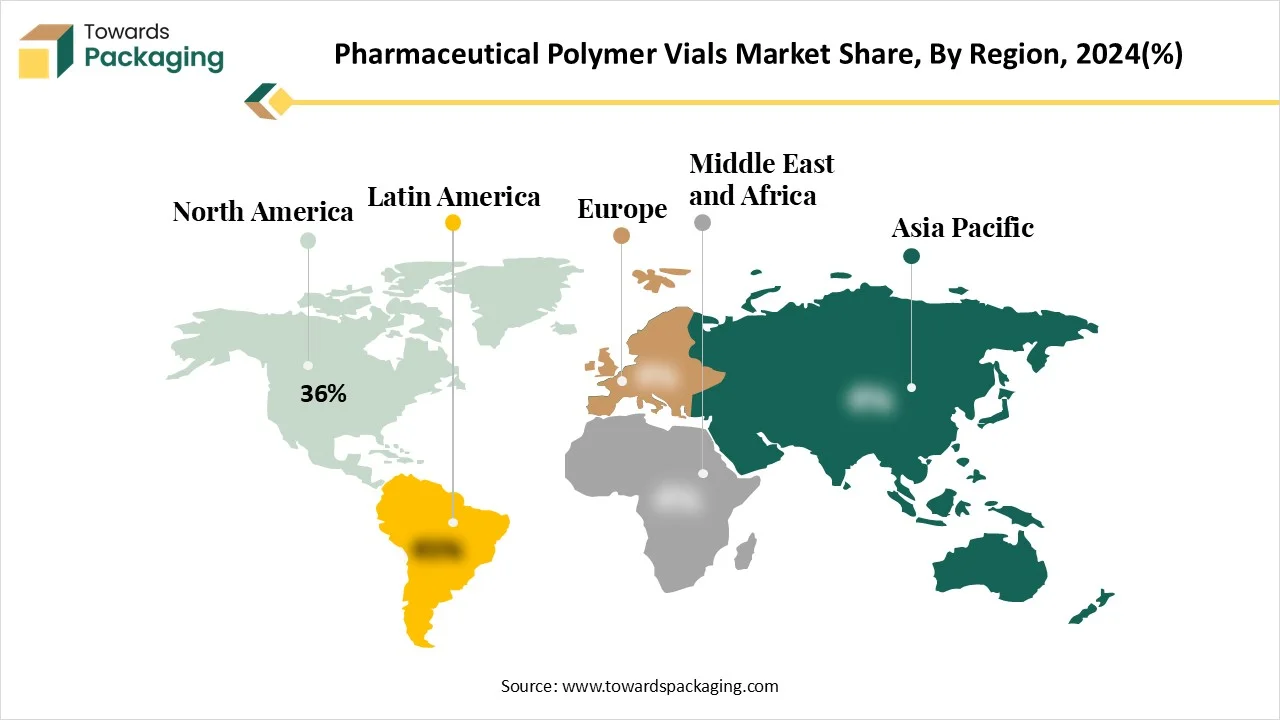

North America held the largest share of the market in 2025, due to the rising production demand for polymer vials for pharmaceutical purpose. The presence of strict guidelines of the government towards pharmaceutical packaging sector has influence the demand for this market to develop rapidly. Rising expenditure towards healthcare sector has evolve the market.

Asia Pacific expects the significant growth in the market during the forecast period. Huge potential for growth of the healthcare sector has influenced the demand for polymer vials. The increasing demand for sanitized vials has raised the innovation process of the market. Rising acceptance for injectable drugs has evolved this market to expand rapidly.

By Polymer Type

By Application

By Capacity

By Sterilization Method

By End User

By Distribution Channel

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarPharmaceutical Polymer Vials Market