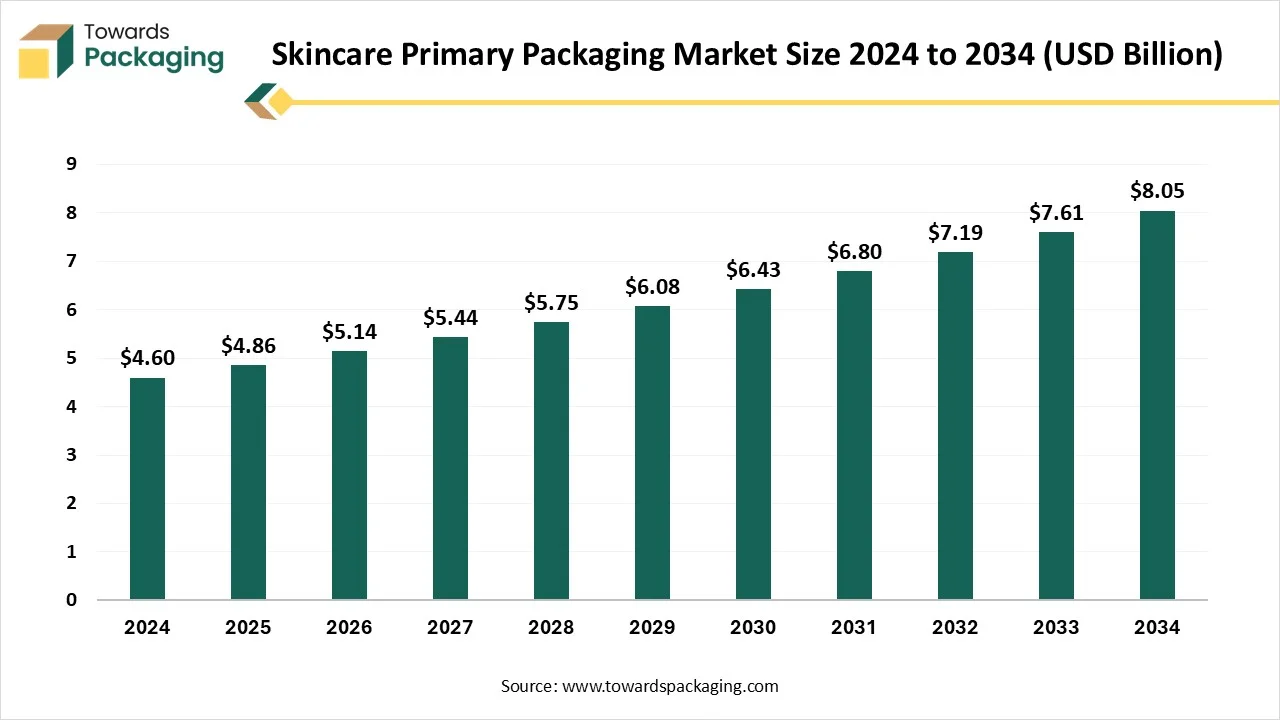

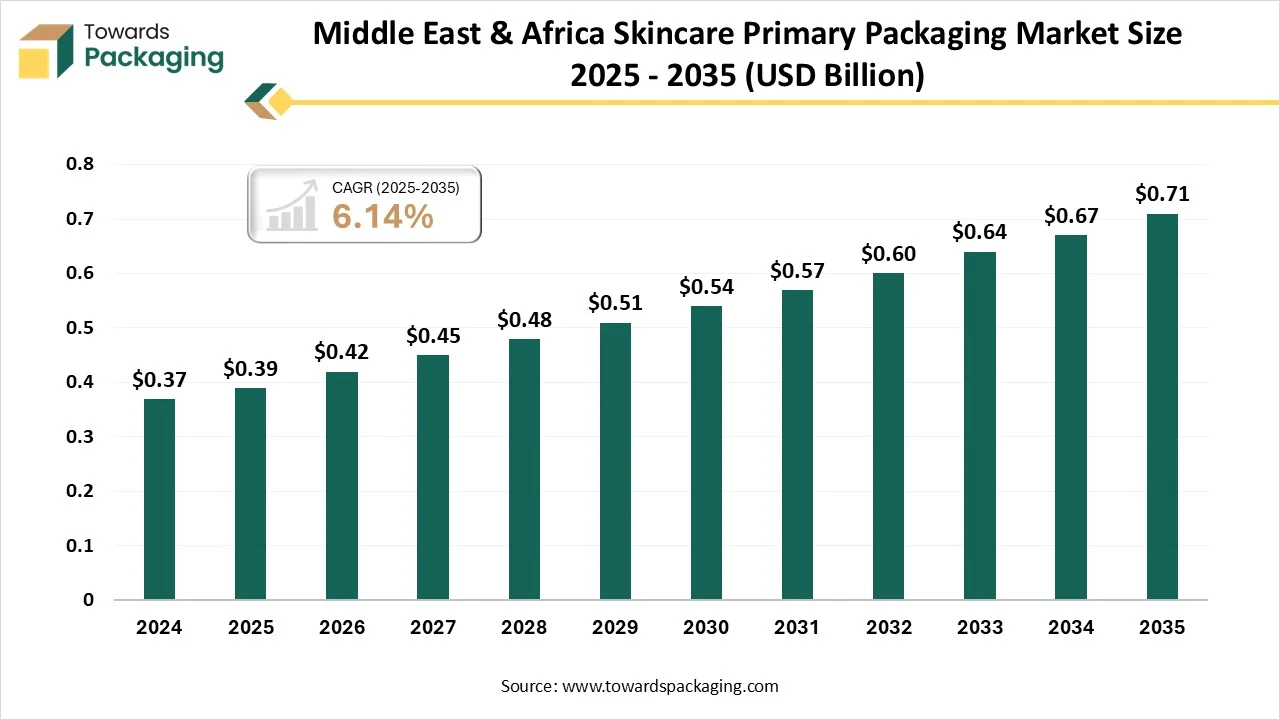

The skincare primary packaging market is projected to grow from USD 5.14 billion in 2026 to USD 8.51 billion by 2035, expanding at a CAGR of 5.75%. This report covers complete market size data, packaging material segmentation, product type analysis, and regional insights across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. It also includes competitive analysis of leading companies, value chain structure, global trade data, and detailed profiles of manufacturers and suppliers.

The skincare primary packaging market encompasses containers and delivery systems that directly hold skincare products such as creams, serums, lotions, oils, and gels. These packaging solutions ensure product safety, hygiene, shelf stability, and user convenience while playing a vital role in brand positioning and consumer experience. Primary packaging includes bottles, jars, tubes, pumps, droppers, and airless systems made from materials like plastic, glass, metal, and sustainable biopolymers.

In the era of a rapidly evolving digital landscape, the integration of artificial intelligence technology emerges as a transformative force and holds great potential to reshape the landscape of the skincare primary packaging market by enabling personalization, promoting sustainability, optimizing packaging dimensions, improving the supply chain, and reducing material waste. AI is playing an increasingly significant role in the future of the beauty and cosmetics industry. AI-powered automation enables faster, more precise packaging processes and ensures consistent quality.

AI-driven designs are becoming increasingly popular, creating new avenues for brand engagement and aligning with consumer needs for customized beauty solutions. By leveraging machine learning (ML) algorithms, companies can create more cost-effective, sustainable, lightweight, durable, and consumer-friendly packaging solutions. AI-driven software can effectively analyse large datasets to predict design trends, which assists brands in staying ahead in the long run.

How is the Rising Demand for Skincare Products Impacting the Skincare Primary Packaging Market’s Growth?

The growing demand for skincare products, particularly in developing and developed countries, is expected to drive market growth during the forecast period. Primary packaging of skincare products plays a crucial role in preserving the efficacy of the product, which can often be sensitive to air, light, moisture, and other environmental conditions. The market is witnessing an increasing focus on self-care, personal grooming, and other associated benefits of skincare has significantly increased consumer spending on skincare products, further propelling the market’s expansion in the coming years. Several brands are increasingly investing in innovative and luxurious packaging to cater to the evolving consumer preferences for premium skincare products. To align with the premium image, primary packaging is often designed to be visually appealing and sophisticated to the targeted customer.

Fluctuating Raw Material Costs

The price volatility is expected to hinder the market's growth. The fluctuation in the price of raw materials has led to an increasing production cost of primary packaging solutions due to global supply chain disruptions and raw material shortages, which can adversely impact the profitability of manufacturers. In addition, high manufacturing costs are required for specialized processes like multi-layer co-extrusion and aseptic filling.

Growing Emphasis on Eco-friendly and Sustainable Packaging Solutions

The rising popularity of eco-friendly packaging materials is projected to create immense growth opportunities for the skincare primary packaging market in the coming years. The surge in environmental concerns and growing awareness of circular economy models enhances the adoption of sustainable packaging practices and is reshaping the primary packaging landscape. Recyclable, reusable, and biodegradable packaging are gaining immense popularity as they offer an eco-friendly packaging solution and a sustainable alternative to traditional plastic packaging. Several government regulations are promoting the adoption of sustainable, eco-friendly packaging materials to reduce the carbon footprint significantly.

The rising trend of online shopping and increased availability of skincare products are expected to propel the market’s expansion during the forecast period. It creates a need for lightweight, durable, and protective packaging that can withstand shipping and enhance the overall unboxing experience. Primary packaging solutions also provide important information about the contents of the product and other required information to educate the customers.

")

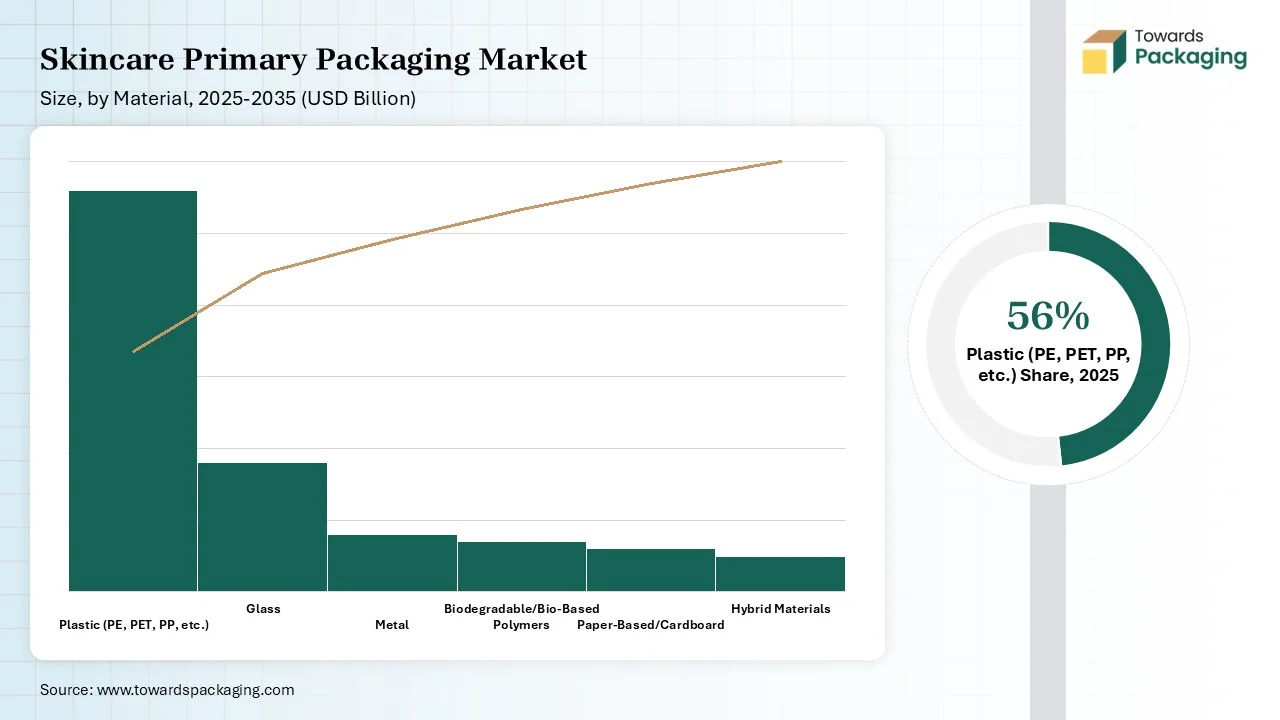

The plastic (PE, PET, PP, Acrylic, etc.) segment held a dominant presence in the skincare primary packaging market in 2025, owing to its maximum strength, cost-effectiveness, versatility, durability, and excellent resistance to chemicals and heat. Several skincare brands prefer plastic material to lower their overall production costs while offering protection to the product against contamination, ensuring product freshness, and maintaining the efficacy of the product.

On the other hand, the biodegradable/bio-based polymers segment is expected to grow at the fastest CAGR. The growth of the segment is attributed to the rising consumer preference for eco-friendly materials and increasing environmental awareness. These packaging solutions are biodegradable, significantly assist in reducing carbon emissions. The brands operating in the skincare industry are increasingly adopting sustainable packaging options like those made from polylactic acid (PLA), polyhydroxyalkanoates (PHA), and other bio-based materials. Moreover, consumers are actively seeking products with eco-friendly packaging, which spurs the demand for biodegradable and bio-based packaging.

The bottles dominated the circular economy in the market in 2025, owing to the increasing consumer preference for durable and aesthetically pleasing packaging options. The market is witnessing the continuous development of diversified packaging styles, including different sizes, shapes, and materials for skincare bottles. Glass bottles are gaining immense popularity in the premium segment owing to their recyclability and perceived luxury. Several businesses are heavily investing in developing innovative and sustainable bottles for skincare products. Brands are focusing on bottle packaging design that reduces the material use and maximizes recyclability.

On the other hand, the airless packaging segment is expected to grow at a notable rate during the forecast period, owing to its superior ability to effectively preserve the integrity of sensitive skincare formulations. These packaging solutions prevent air exposure and safeguard the products from oxidation and contamination, extending shelf life.

The face creams and moisturizers segment is majorly driven by the rising awareness of skincare benefits, new product launches, and the surge in disposable incomes, particularly in developing and developed countries. Primary packaging protects the face cream and moisturizer from oxidation, contamination, and degradation, ensuring the product's efficacy and extending the shelf life. Primary packaging for face creams and moisturizers aims to maintain formula integrity and hygiene while also focusing on sustainability and evolving consumer preferences. The most common packaging types of face creams and moisturizers include tubes, pumps, dispensers, and bottles. Moreover, the increasing online sales sector is expected to create demand for convenient and accessible skincare products.

On the other hand, the serums and ampoules segment is expected to witness remarkable growth during the forecast period, owing to the rising consumer demand for specialized skincare products and the rising preferences towards preventative skincare routines. Primary packaging for serums and ampoules is designed to protect them from various environmental factors and maintain their integrity. The most widely used packaging includes plastic, glass, and others, each offering specific benefits.

")

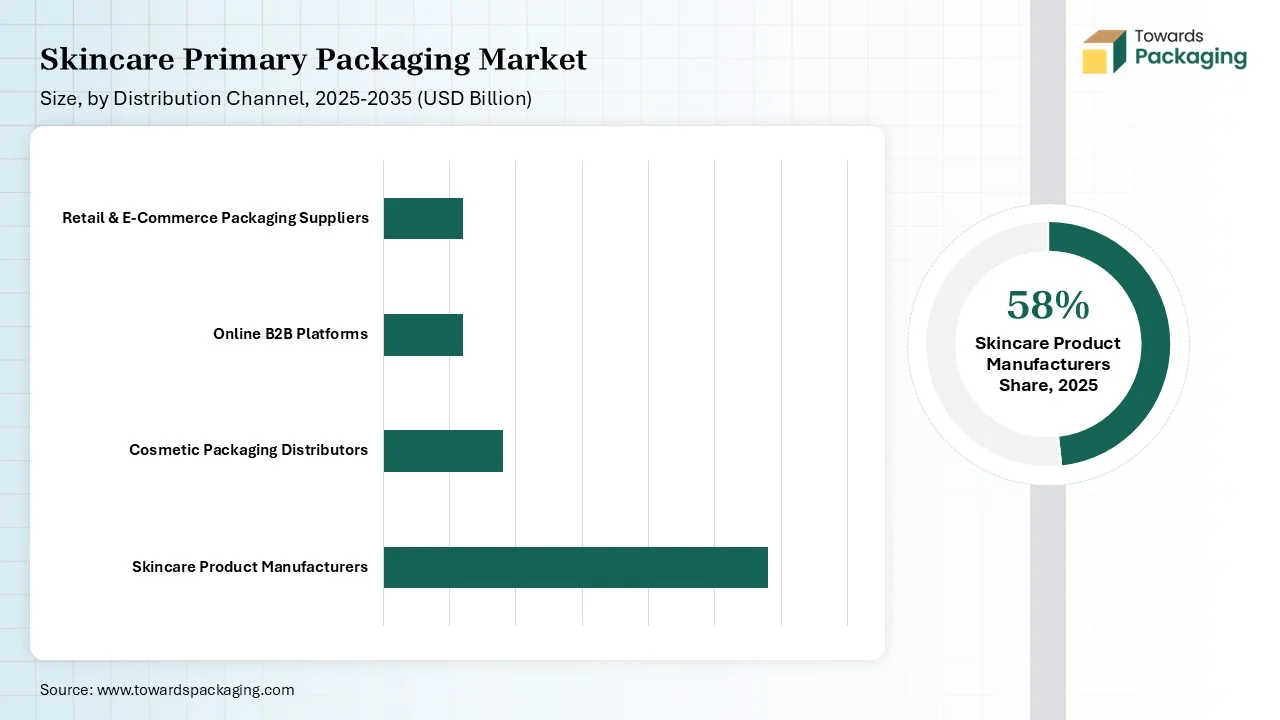

The skincare product manufacturers segment accounted for the highest revenue share in 2025. Skincare product manufacturers often have their own direct sales channels. Skincare product manufacturers act as a prominent distribution channel, with online and offline channels such as supermarkets, convenience stores, and pharmacies. Manufacturers also collaborate with retailers to distribute their skincare products. Additionally, several prominent skincare brands leverage online platforms and their websites to reach a wider targeted customer base. Such factors are bolstering the segment’s growth during the forecast period.

On the other hand, the online B2B platforms segment is expected to grow at a significant rate. Online B2B platforms as a distribution channel play a crucial role for skincare brands, offering a streamlined way to effectively manage packaging needs and connect with suppliers. Online B2B platforms generally offer skincare brands with broad access to various suppliers and competitive pricing options.

The mass-market/drugstore brands segment dominated the market with the largest share in 2025, owing to the rising incidence of skin issues, surge in disposable incomes, and growing awareness of skincare routines. Consumers are becoming more aware of skincare routines and their associated benefits, which creates substantial demand for skincare items. The segment is experiencing significant growth in the market, offering innovative, effective, and sustainable packaging solutions that cater to the evolving needs of consumers.

On the other hand, the indie/clean beauty brands are expected to grow at a notable rate, owing to the consumer demand for natural and organic ingredients. These brands are gaining immense popularity in the market for their unique and sustainable primary packaging options that align with their values and product formulations. Independent and clean beauty brands are increasingly focusing on eco-friendly and aesthetically pleasing packaging solutions like glass, recycled plastics, and others.

")

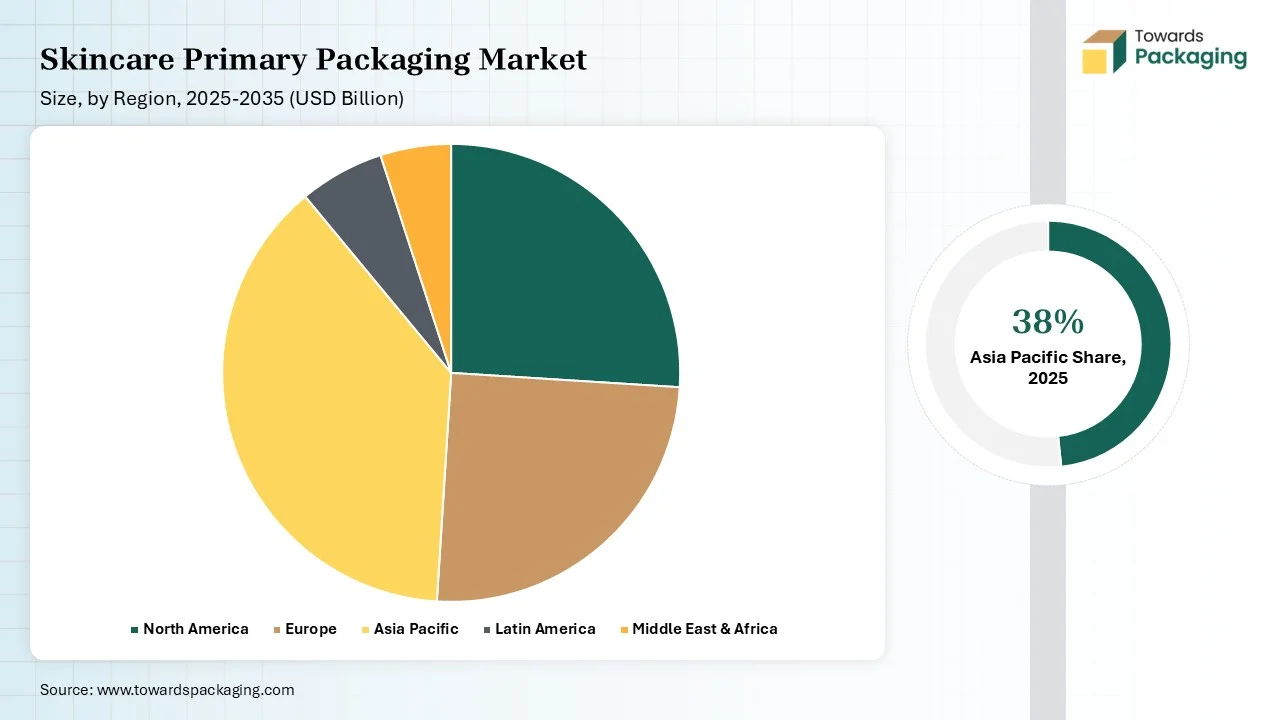

Asia Pacific held the dominant share is attributed to the rising presence of key market players, rising population, increasing availability of raw materials, rising awareness of skincare routines, the growing emphasis on sustainability, increasing investment in advancing packaging materials, rising consumer preferences for aesthetic packaging solutions, increasing disposable income, and rising consumer demand for premium and luxury skincare products. The surge in anti-aging and acne problems is driving demand for specialized skincare products in the region, further contributing to the market growth.

Asia Pacific is experiencing a shift toward recyclable, reusable, and biodegradable primary packaging solutions, driven by stringent government regulations aimed at reducing greenhouse gas emissions and improving environmental sustainability. To align with the circular economy principle, brands are investing heavily in sustainable packaging solutions. Several manufacturers are focusing on developing innovative packaging designs and printing on packaging to better connect with customers to gain a competitive edge. The trend of premiumization is driving higher demand for luxury skincare products, while the growth of online retail is expected to further boost the primary packaging market.

By Packaging Type

By Material

By Product Category

By End-User Brand Type

By Distribution Channel

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarSkincare Primary Packaging Market