The thermoformed cellulose packaging market report provides a complete quantitative view of global and regional market size, historical data, and forecast figures from 2026 to 2035. It covers detailed trends, CAGR, and segment-wise statistics by material source, packaging format, end-use industry, and application, along with a full regional breakdown for North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. The study also includes company profiles, competitive market share, value chain structure, trade data, and comprehensive information on key manufacturers and suppliers.

Thermoformed cellulose packaging refers to sustainable packaging materials made from cellulose fibers, typically derived from wood pulp, recycled paper, or agricultural waste, that are molded using heat and pressure into specific shapes. This process, known as thermoforming, allows cellulose pulp to be transformed into rigid, lightweight, and biodegradable packaging components. Unlike plastic thermoforming, which uses petroleum-based polymers, thermoformed cellulose is plant-based and compostable, making it an eco-friendly alternative.

Thermoformed materials are used in a wide range of applications such as food containers, electronic device trays, protective cushioning, and cosmetic packaging. The cellulose fibers are usually mixed with water and natural binders, shaped in molds, and then dried to form durable packaging with excellent structural integrity. This type of packaging offers good shock absorption, breathability, and printability, and supports corporate sustainability goals. With increasing global focus on reducing plastic waste and enhancing circular economy practices, thermoformed cellulose packaging is gaining popularity across various industries.

| Metric | Details |

| Key Drivers | Plastic bans, sustainability mandates, innovations in dry molding & coatings, ESG adoption, consumer demand for eco-friendly packaging |

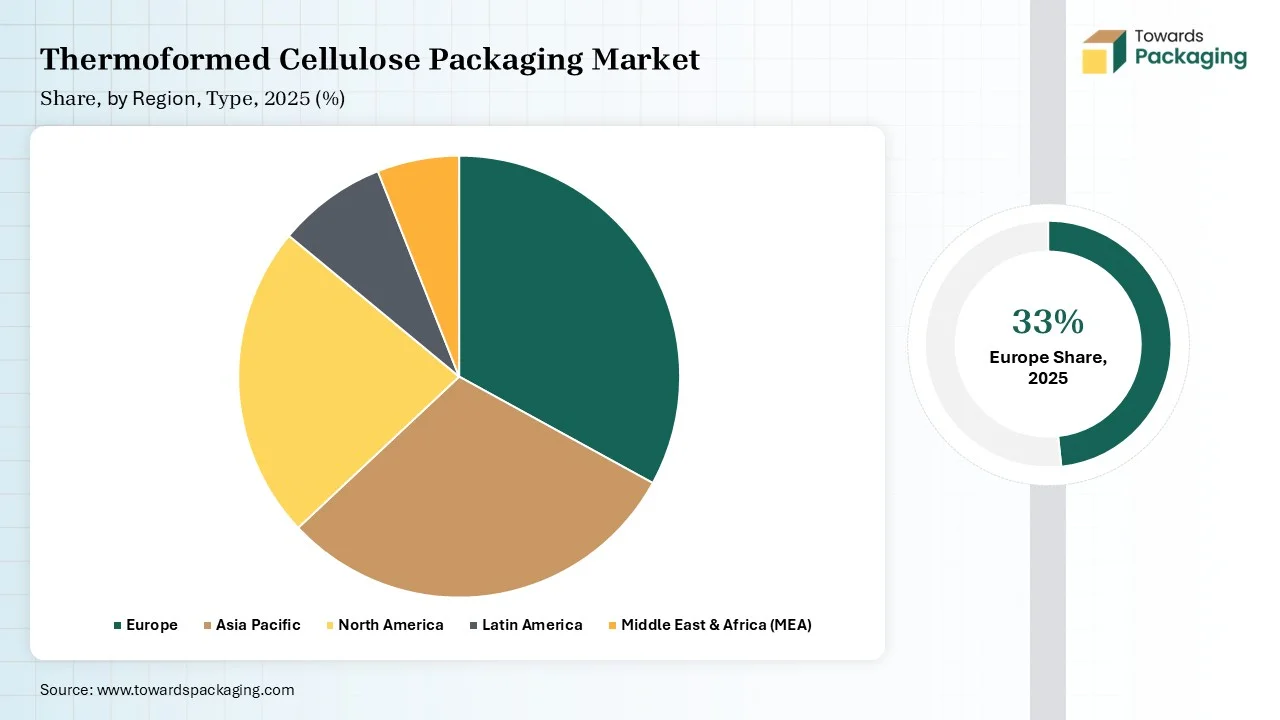

| Leading Region | Europe |

| Market Segmentation | By Material Source, By Packaging Format, By End-Use Industry, By Application and By Region |

| Top Key Players | Huhtamaki Oyj, Sabert Corp., PulpWorks, UFP Technologies, Genpak, Eco-Products (Novolex), FiberPak (Sonoco), Earthcycle, Be Green, ThermoFibre, Packnatur, EnviroPAK |

AI integration can significantly enhance the thermoformed cellulose packaging industry by improving efficiency, quality, and sustainability across production and design stages. In manufacturing, AI-powered vision systems can detect defects in real time, ensuring consistent quality and reducing waste. Predictive maintenance driven by machine learning algorithms minimizes downtime by forecasting equipment failures before they occur. In the design phase, AI can analyze customer requirements and simulate optimal mold designs for strength, material usage, and aesthetics, reducing prototyping costs.

AI-enabled supply chain analytics optimize raw material sourcing, inventory management, and energy consumption, leading to cost-effective and eco-friendly operations. When combined with IoT sensors, AI can offer end-to-end monitoring of temperature, moisture, and pressure during thermoforming to ensure ideal conditions. Additionally, AI helps brands personalize packaging by interpreting consumer trends and preferences, enabling dynamic and sustainable design decisions. Overall, AI integration empowers the thermoformed cellulose packaging industry to become smarter, greener, and more responsive to market needs.

Government Regulations & Bans on Single-Use Plastics

Increasing consumer awareness and regulatory pressure to reduce plastic usage are pushing industries toward eco-friendly alternatives. Thermoformed cellulose, being biodegradable and compostable, is emerging as a preferred sustainable solution. Many countries are implementing strict bans and regulations on non-biodegradable plastics, encouraging the adoption of cellulose-based materials in packaging applications.

Furthermore, Products made of single-use plastics (SUPs) are used just once or for a brief time before being discarded. Globally, this plastic trash can have severe effects on both the environment and human health. Reusable plastic products are less likely than single-use ones to wind up in oceans. Together with fishing gear, the top ten single-use plastic items on European beaches account for 70% of all marine trash in the EU. The European Union wants to lead the world in combating plastic waste and marine litter. EU regulations seek to lessen the quantity and environmental impact of specific plastic items.

The Single-use Plastics Directive predicts that by 2025 and 2030, 25% and 30% of plastic bottles, respectively, will be made of recovered plastic, which encourages recycling growth. The standards governing the calculation, verification, and reporting of recycled content in single-use plastic beverage bottles are currently out for public comment.

Scale and Infrastructure Limitations & Limited Barrier Properties

The key players operating in the thermoformed cellulose packaging market are facing issues due to scale and infrastructure limitations and limited barrier properties. Thermoformed cellulose packaging often involves more expensive raw materials (like virgin or treated cellulose fibers) and specialized machinery, which increases manufacturing costs. This makes it less competitive compared to cheap plastic packaging, especially for price-sensitive markets. Compared to plastic, cellulose-based packaging has weaker resistance to moisture, oils, and gases. While coatings can be applied, they often add cost or compromise compostability, limiting their use in certain food and pharmaceutical applications. The production of thermoformed cellulose packaging requires dedicated equipment and skilled labor; however, the global manufacturing infrastructure is not yet sufficiently scaled to meet mass-market demands quickly.

As sustainability becomes a global priority, there is a significant opportunity for thermoformed cellulose packaging to replace plastic in sectors like food service, electronics, cosmetics, and healthcare.

Ongoing R&D in water- and oil-resistant biodegradable coatings will expand the use of thermoformed cellulose in moisture-sensitive applications like food packaging and pharmaceuticals.

")

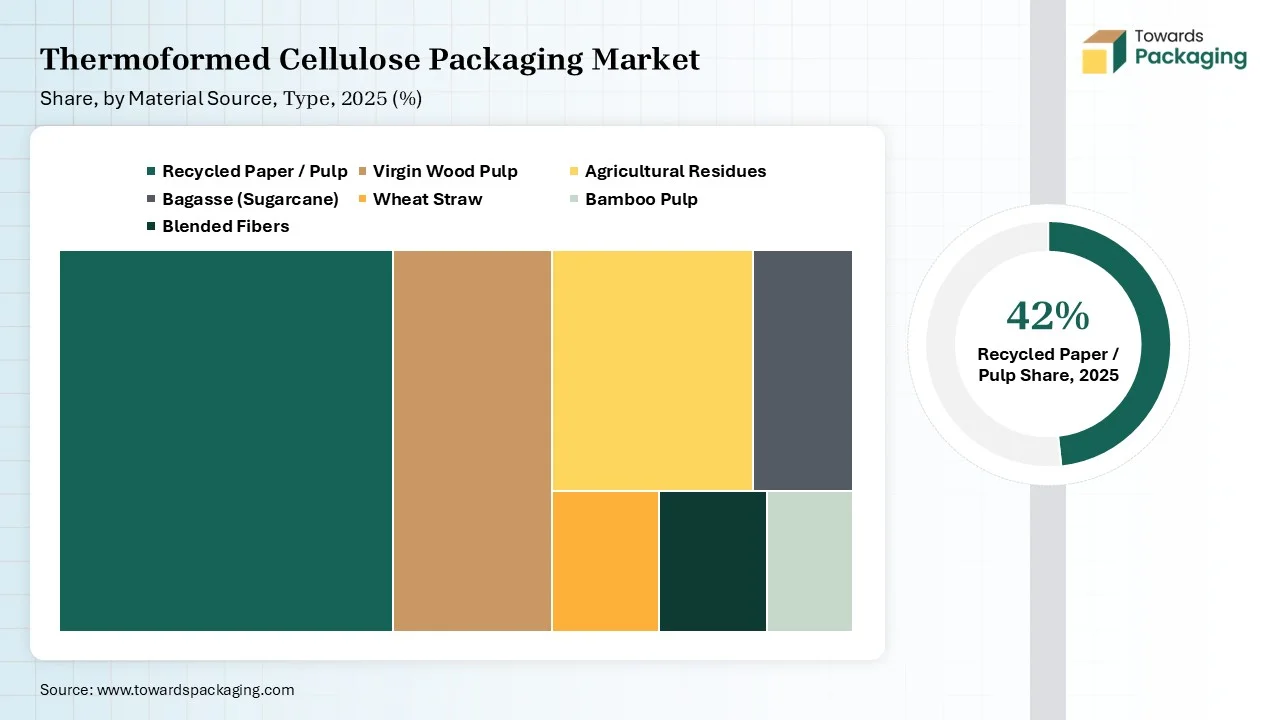

Recycled paper/ Pulp material is the dominant material source segment in the thermoformed cellulose packaging market due to its environmental benefits, cost-effectiveness, and wide availability. Utilizing recycled materials aligns with global sustainability goals by reducing deforestation, minimizing landfill waste, and lowering carbon footprints. This material is particularly favored by industries seeking eco-friendly branding and compliance with regulations banning single-use plastics. Additionally, recycled pulp offers comparable strength and moldability to virgin fiber, making it suitable for various applications such as protective packaging and food containers. Its affordability and compatibility with existing thermoforming technologies further strengthen its dominance in the market.

The agricultural residues segment using non-wood materials such as sugarcane bagasse, wheat or rice straw, and jute is the fastest-growing source in the thermoformed cellulose packaging industry due to its abundant availability, low cost, and strong sustainability credentials. Agricultural residues help reduce dependence on wood pulp, mitigating deforestation and lowering carbon footprints. These fibers are renewable, often regionally abundant (especially in Asia and Latin America), and structurally suitable for pulp molding with high cellulose and low lignin content, which enhances processability and quality. Advancements in non wood pulping and molding technologies further support their adoption. Additionally, the growing focus on circular economy and waste valorization, transforming crop waste into value-added packaging, drives investment in this fast-expanding segment across global markets.

The tray packaging format segment is dominant in the thermoformed cellulose packaging market due to its widespread usage across key industries such as food, electronics, healthcare, and consumer goods. Trays made from molded cellulose offer excellent structural rigidity, cushioning, and environmental benefits, making them a preferred replacement for plastic and foam trays. Their ability to be custom-molded to fit specific product shapes enhances protection during transportation and display, especially for fragile or perishable goods. The food industry, in particular, has adopted cellulose trays for ready-to-eat meals, fruits, and bakery items due to their biodegradability and food-grade safety. Furthermore, trays support stackability and space efficiency, which reduces storage and shipping costs. The global push for sustainable retail packaging and increasing regulations on plastic tray use further bolster demand for cellulose-based alternatives. These functional, environmental, and economic advantages make tray formats the leading segment in this market.

The clamshell format is the fastest growing segment in the thermoformed cellulose packaging market due to its superior functionality, sustainability appeal, and expanding regulatory support. Clamshells offer secure, all around protection with integrated closures, making them ideal for both food service (e.g., takeaway meals, fruits) and electronics or retail items. As bans on single use plastics intensify, businesses are shifting from foam and plastic clamshells to biodegradable molded pulp alternatives that enhance brand image and compliance. Furthermore, clamshells made via thermoformed pulp offer a smooth finish, rigidity, and design precision, aligning with both functionality and aesthetic expectation, especially in food delivery and premium retail sectors.

")

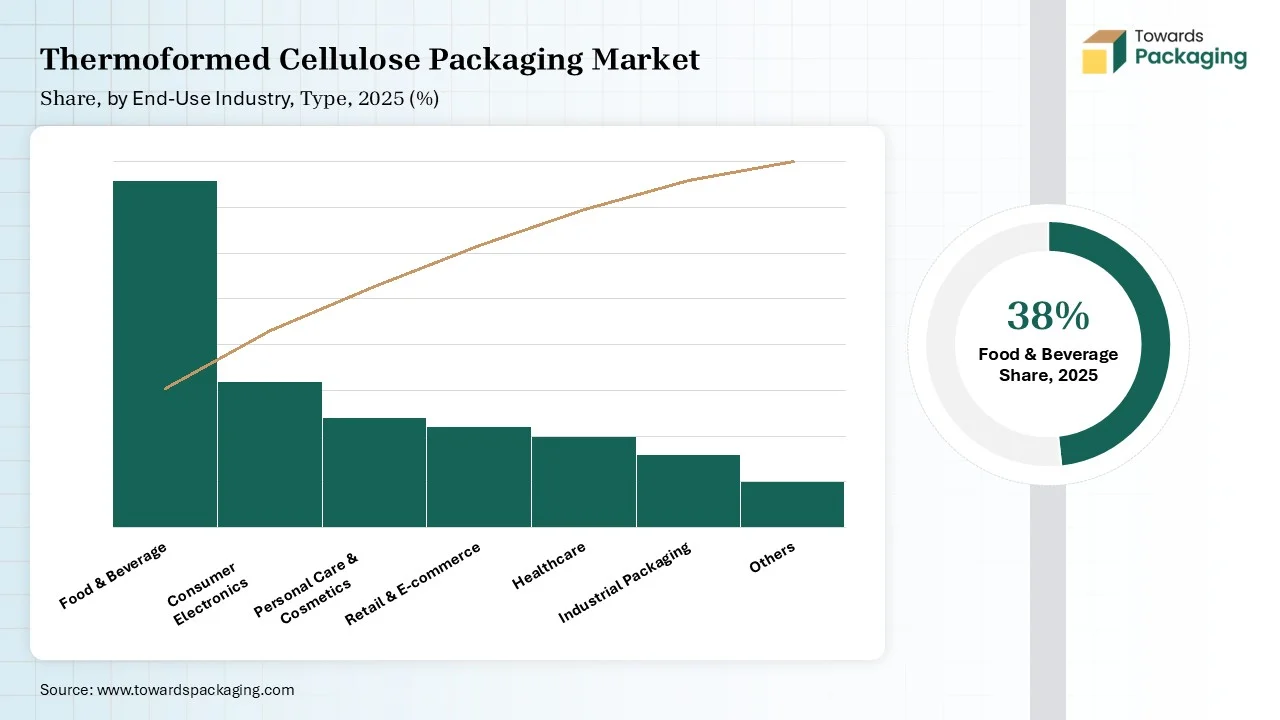

The food & beverages segment is the dominant end-use segment in the thermoformed cellulose packaging market due to the increasing demand for sustainable, safe, and biodegradable packaging solutions within the industry. With growing consumer awareness around plastic pollution and food safety, businesses are shifting toward eco-friendly packaging like molded pulp trays, clamshells, and containers made from cellulose. These materials offer essential benefits such as biodegradability, food-contact safety, insulation, and moisture resistance when properly treated. Moreover, governments and regulatory bodies across the globe are imposing bans on single-use plastics, especially in food applications, driving the transition to sustainable alternatives. The rapid expansion of sectors such as ready-to-eat meals, fresh produce, and online food delivery has further increased the need for lightweight, stackable, and protective packaging. As a result, thermoformed cellulose solutions are increasingly replacing plastic and foam in this sector, solidifying their position as the leading end-use market.

The personal care and cosmetics end-use segment is the fastest-growing in the thermoformed cellulose packaging market due to the combination of rising consumer demand for sustainable beauty products and the premium aesthetic expectations of the industry. Eco-conscious skincare and cosmetics brands increasingly seek biodegradable packaging options like molded pulp trays, inserts, and clamshells that reinforce brand sustainability ethos while providing functional protection for fragile items such as palettes, lipsticks, and toiletries. Innovations in pulp molding enable high-end finishes and detailed printability, which are especially valued in cosmetics packaging to deliver luxury appeal without compromising environmental values. Furthermore, the cosmetics industry's rapid growth in e-commerce platforms amplifies the need for secure, protective packaging, fueling the adoption of molded fiber solutions. Combined with tightening regulations on plastic packaging and a shift toward ESG-aligned branding, this segment is outpacing others in cellulose-based packaging demand.

The protective/ transit packaging segment is the dominant application in the thermoformed cellulose packaging market due to its ability to offer durable, shock-absorbing, and sustainable protection during shipping and handling. Thermoformed cellulose, often derived from recycled paper or agricultural waste, is molded into custom-fit forms that cushion products like electronics, appliances, and industrial components. Its lightweight nature reduces transportation costs while maintaining structural integrity. Additionally, rising environmental regulations and corporate sustainability goals are prompting companies to replace plastic and foam-based packaging with biodegradable molded pulp solutions, which decompose easily and support circular economy principles, making it ideal for modern transit packaging needs.

The primary packaging segment is the fastest-growing in the thermoformed cellulose packaging market due to increasing regulatory pressure to eliminate single-use plastics and rising consumer demand for eco-friendly alternatives. Brands across the food, cosmetics, and consumer goods sectors are rapidly adopting molded fiber for its sustainability, aesthetic appeal, and protective qualities. Innovations in dry molding, non-wood pulp use, and scalable production have enhanced design precision and affordability, allowing primary cellulose packaging to replace plastic effectively while aligning with ESG and circular economy goals.

")

Europe dominates the thermoformed cellulose packaging market due to its strong regulatory framework, environmental awareness, and early adoption of sustainable practices. The European Union’s stringent bans on single-use plastics and its Circular Economy Action Plan have created a favourable policy environment for biodegradable packaging solutions. Additionally, consumers in Europe are highly eco-conscious, encouraging brands to shift toward compostable, plant-based alternatives like thermoformed cellulose. The region also boasts advanced manufacturing infrastructure and continuous innovation in fiber-based technologies, especially in countries like Germany, France, and the Netherlands. These factors collectively position Europe as a global leader in sustainable packaging solutions.

Germany Market Trends

Germany leads due to its strong industrial base, advanced pulp and paper processing technologies, and strict packaging waste regulations. Its emphasis on circular economy models fuels demand for molded fiber packaging.

France Market Trends

France has implemented bans on single-use plastics in retail and food services, driving businesses toward sustainable alternatives like thermoformed cellulose. French consumers are also increasingly favouring eco-packaged products.

Netherlands Market Trends

With a progressive approach to sustainability and innovation, the Netherlands supports startups and packaging companies focused on biodegradable solutions, making it a key hub for cellulose packaging R&D.

Italy Market Trends

Italy has a growing demand for sustainable packaging, especially in its food and luxury goods sectors. Government policies and EU funding also support green packaging innovation.

The Asia-Pacific region is experiencing the fastest growth in the thermoformed cellulose packaging market due to a combination of rising environmental awareness, growing population, and expanding consumer goods sectors. Countries like China, India, Japan, and South Korea are increasingly adopting sustainable packaging alternatives to reduce plastic pollution and meet new government regulations. The region's rapidly developing e-commerce and food delivery industries are driving demand for eco-friendly, disposable packaging.

Increasing investments in green technologies and local manufacturing of fiber-based materials are making thermoformed cellulose packaging more affordable and scalable. Government initiatives promoting biodegradable alternatives and the shift in consumer preference toward environmentally friendly products are also key growth enablers. With a large market base and evolving regulations, Asia-Pacific is becoming a major contributor to the global expansion of the thermoformed cellulose packaging industry.

China Market Trends

China is witnessing strong demand for sustainable packaging due to rising plastic waste concerns and strict government regulations like the “Plastic Ban 2020.” The country’s massive manufacturing and e-commerce sectors are also integrating biodegradable alternatives at scale.

India Market Trends

India’s growing population, urbanization, and increasing environmental awareness are boosting the use of eco-friendly packaging. Government initiatives like the “Swachh Bharat Abhiyan” and bans on single-use plastics in several states encourage cellulose-based packaging solutions.

Japan Market Trends

Japan emphasizes minimal, high-quality packaging and sustainability. With a technologically advanced economy and strong environmental regulations, the country is innovating in the field of compostable and fiber-based packaging materials.

South Korea Market Trends

South Korea is focusing on a circular economy and has implemented regulations to reduce plastic waste. The government supports green startups, and consumer demand for sustainable alternatives is rising, especially in cosmetics and electronics packaging.

North America is witnessing notable growth in the thermoformed cellulose packaging market due to a rising demand for sustainable packaging solutions driven by both regulatory pressure and shifting consumer preferences. In the United States and Canada, environmental policies promoting the reduction of single-use plastics and the adoption of compostable materials are encouraging manufacturers to adopt fiber-based alternatives.

Major consumer goods companies in the region are also aligning with ESG goals and incorporating biodegradable packaging in their supply chains. Additionally, a strong base of technological innovation and investment in green packaging startups is accelerating the development of advanced thermoforming techniques. The thriving e-commerce, food delivery, and healthcare sectors are further fueling the demand for eco-friendly, protective, and aesthetically appealing packaging, making thermoformed cellulose a preferred choice. This combination of policy support, innovation, and market demand positions North America as a fast-growing region in this industry.

By Material Source

By Packaging Format

By End-Use Industry

By Application

By Region

Principal Research Analyst

Vidyesh Swar is a Senior Research Analyst at Towards Packaging, bringing over 4 years of dedicated expertise in market intelligence and strategic analysis across the dynamic world of packaging technologies and solutions.

Learn more about Vidyesh Swar

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarThermoformed Cellulose Packaging Market