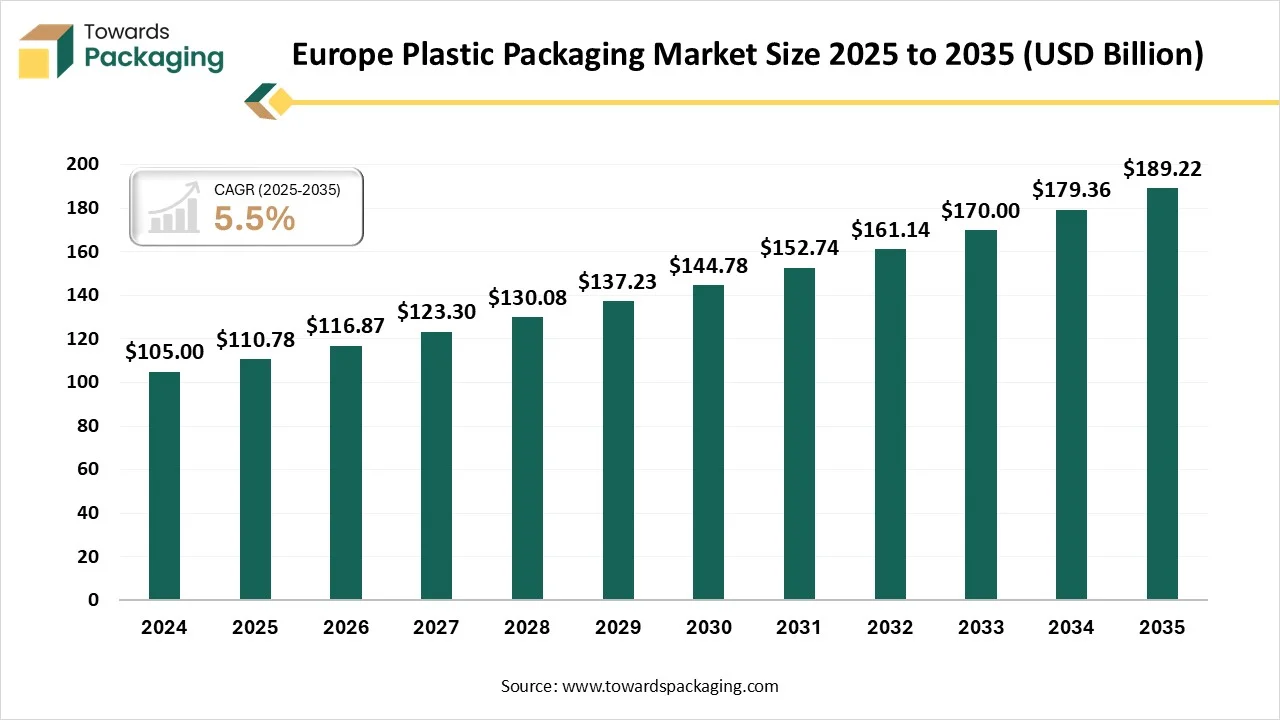

The Europe plastic packaging market is forecasted to expand from USD 116.87 billion in 2026 to USD 189.22 billion by 2035, growing at a CAGR of 5.5% during 2026–2035. The market is driven by the widespread use of plastic across food & beverages, pharmaceuticals, personal care, and industrial sectors due to its low cost, durability, lightweight properties, and high performance under varying environmental conditions. The report covers detailed market size analysis, segment data by material type, product type, application, and end-use industry, along with comprehensive regional insights across North America (NA), Europe (EU), Asia Pacific (APAC), Latin America (LA), and the Middle East & Africa (MEA).

It further includes company profiles, competitive landscape assessment, value chain analysis, import-export trade data, and detailed manufacturers and suppliers data, providing a complete industry outlook.

The Europe plastic packaging industry revolves around the production, design, and sale of plastic-based containers for products, which include both flexible and rigid designs, which are used across different industries such as healthcare, food, and automotive too. The market's expansion is experienced along with the regulatory changes in the region, mandates created by regulatory bodies, and demand for product innovation in multiple sectors.

Chemical recycling is developing as an innovative approach in the context of plastic recycling that serves as an updated solution for solving plastic waste. Like regular mechanical recycling, which is restricted to particular types of plastics, chemical recycling occurs at the molecular level, which allows the processing of contaminated and mixed materials. This cutting-edge strategy aligns with the sustainability goals by avoiding plastic waste and making a circular economy for plastics.

For instance, to this

Worldwide, the leading three importers of Europe Plastic Packaging are Ukraine, Uzbekistan, and Colombia. Uzbekistan has topped the globe in Europe Plastic Packaging, importing 271 shipments, which is being followed by Ukraine with 152 shipments, and Colombia, which takes the third position with 125 shipments.

As per the global data, the world has officially imported 113 shipments of European plastic packaging during the period June 2024 to May 2025. These imports were being supplied by 52 exporters to 41 buyers, which marks a growth rate of -67% as compared to the previous twelve months.

In Europe, the plastic packaging raw materials are being sourced from three main fields, such as recycled materials, fossil-based polymers, and bio-based plastics. It is driven by the strict regulations like the Packaging and Packaging Waste Regulation 9PPWR), which is a main move apart from the virgin fossil fuels towards renewable sources.

In Europe, the plastic packaging elements are produced by a huge network of tailored molders, converters, and extruders, too, with Germany having the biggest market share. Strict EU regulations and a rising urge for sustainable materials such as recycled plastics and bioplastics mainly encourage manufacturing trends.

The latest EU Packaging and Packaging Waste Regulation has wide-reaching effects. The transport and distribution logistics, and the last mile in particular, are significantly affected as packaging plays a crucial role in this sector. By using the standard-sized cartons for every product, and hence due to shipping products in oversized cartons and /or having extra void filling, is no longer an accurate method under the PPWR.

")

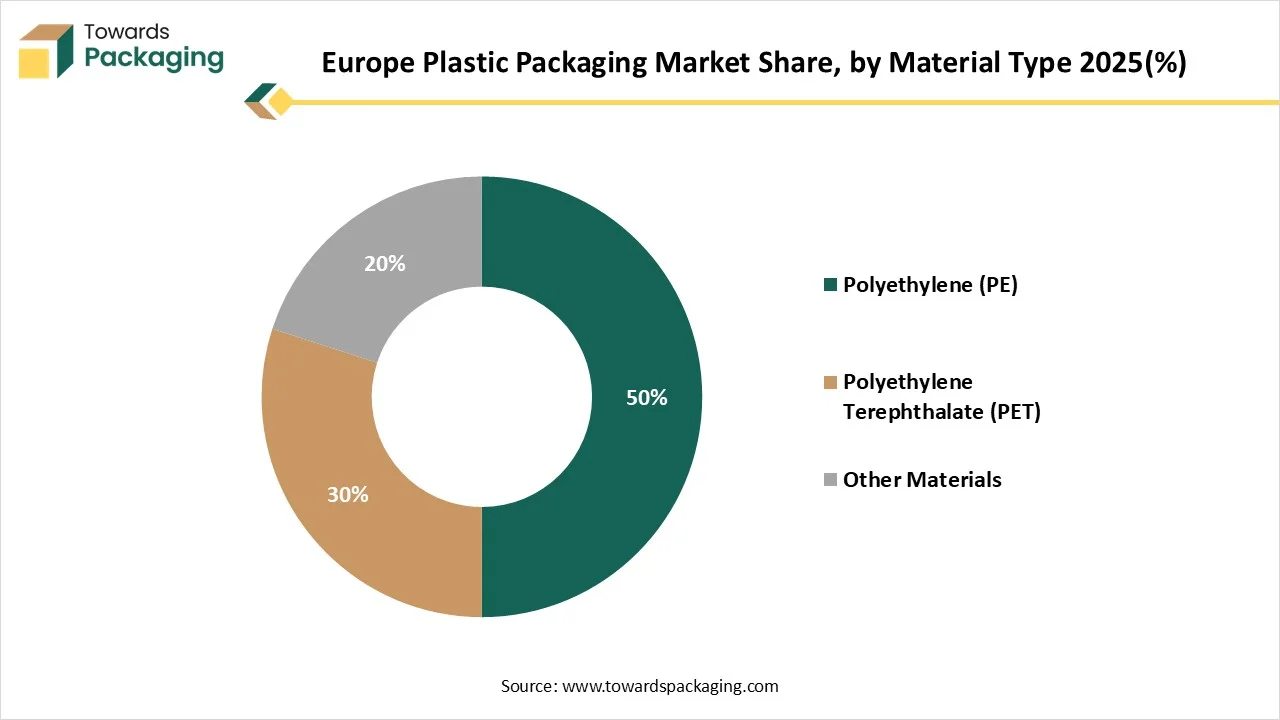

The polyethylene segment has dominated the market in 2024 as polyethylene is one of the most widely utilised plastic materials in the world and is made through the polymerization of ethylene monomers. It is a valuable material that has a huge range of applications in different sectors. The production of polyethylene is done by integrating ethylene monomers produced under conditions, which are generally achieved using a catalyst. The monomers of the outcome polymers create long chains that are linked in a continuous fashion due to the characteristics of polyethylene.

The polyethylene terephthalate segment is expected to experience the fastest CAGR during the forecast period. PET is a kind of plastic that is widely used in the packaging sector because of its strong, transparent, and lightweight properties. PET has a perfect effect on opposition, which makes it perfect for beverage bottles and food packaging. Furthermore, this material has good barrier characteristics against carbon dioxide and oxygen, which maintains the quality of the products inside. Several users are worried about toxic chemicals in plastic packaging, particularly for the Bisphenol A (BPA. Hence, PET plastic does not have BPA, which makes it a safer choice compared to some other kinds of plastic.

| Product Type Segments | Market Share 2025 (%) |

| Bottles and Jars | 55% |

| Pouches | 25% |

| Other Products | 20% |

The Bottles & Jars segment has dominated the market in 2024 as plastic resin serves as a perfect power while staying lightweight and shatter-resistant, too, which makes it an actual alternative to glass bottles. This reliability assists in protecting against breakage at the time of daily use and shipping too. PET bottles also help in high-level decoration procedures like paint coating, logo engraving, and hot stamping, too. These potentially make PET packaging perfectly-suited for products by using the good-quality pump bottles, cream jars, and the airless pump, working too.

The pouches segment predicts the fastest CAGR during the forecast period. Pouch packaging is a kind of flexible packaging created from laminated films such as PE, PET, or PP crafted to protect products while having a lower weight and material usage. It counts designs like flat pouches, stand-up pouches, sachets, and the spouted versions as each one can be sealed, filled, and tailored to align with different products. It can even be printed directly, designated as recyclable mono-material patterns, as the UK and EU reveal curbside recycling for flexible plastics.

")

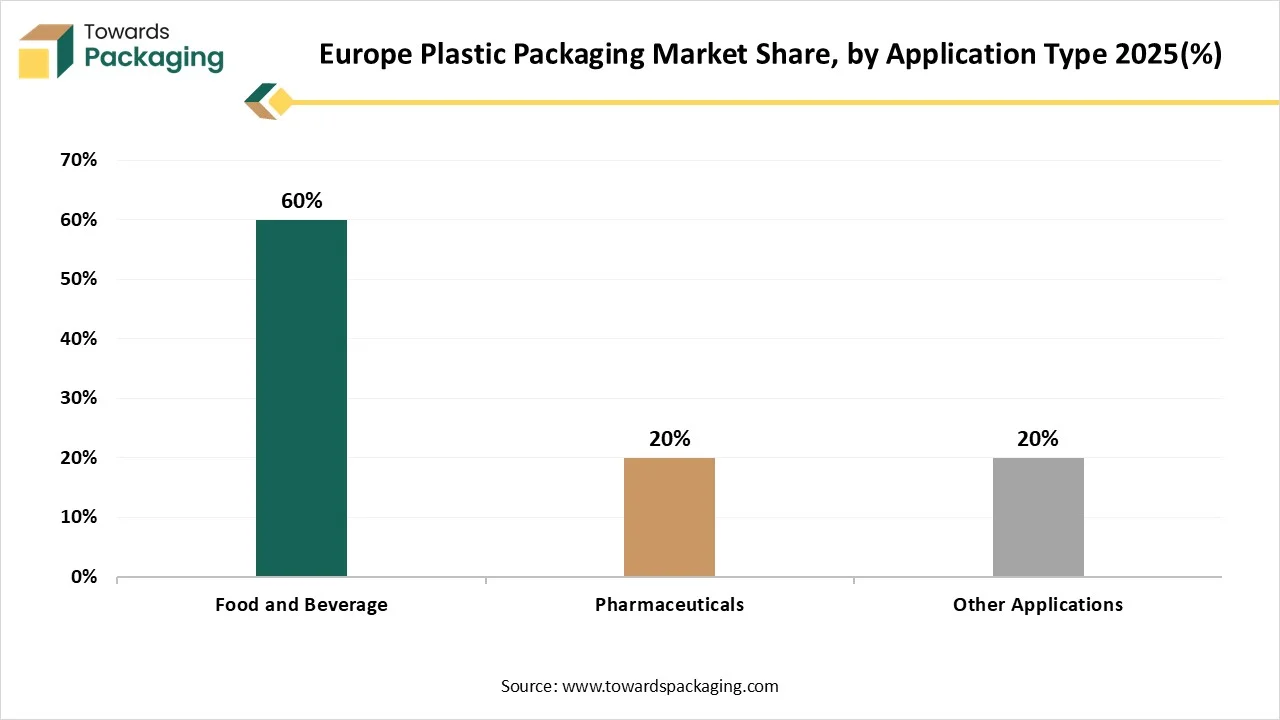

The food and beverages segment dominated the market in 2024, as plastic is conveniently found in different household items such as snacks, instant noodles, beverage bottles, and frozen food. Its practicality creates plastic packaging as the initial choice in different industrial sectors. The benefit of plastic packaging is that it prevents the product from air and contamination, which then extends the shelf life of the food and beverages. This is important for the food industry, which gives importance to both product safety and quality. It excels in being strong, lightweight, reliable, and flexible too, which makes it a top choice across various sectors.

The pharmaceutical segment expects the fastest CAGR during the forecast period. The crucial function of pharmaceutical packaging is to protect medicines from the surrounding elements like oxygen, moisture, light, and contamination. The plastics have updated packaging with their originality. Their unbreakable and lightweight nature and the potential to be moulded into different shapes make them perfect for a series of products. These products include blister packs, bottles, and dropper bottles, too. Developments in plastic technology also include biodegradable plastics that match environmental sustainability goals.

Germany held the largest share in the market in 2024, as it is one of the biggest and high-level plastics markets and is developing as a complicated frontier in the transformation to more sustainable materials. This region is very huge and encouraging too, as it features the demand for materials, which lowers the emissions and assists circular design. At the same time, the urge for PLA -specifically in packaging, automated, and medical uses is developing in response to strict sustainability aims and rising consumer expectations.

The Eastern European plastics industry is predicted to have the fastest compound annual growth rate in Europe, as this region has a stretching food processing sector and developing retail sales of packaged food, which are the main consumers of plastic packaging. Poland, for instance, is witnessing fast growth in this segment. For several Eastern European countries, the plastic packaging is still in a development phase. Penetration into the European Union has also developed packaging and economic market capability for several nations. The demand for flexible plastic packaging, such as film and pouches, is developing due to its material efficiency and cost-effectiveness. The urge for recycled PET is developing, which is driven by both developing environmental awareness and the EU regulations, which are compulsory for recycled content. Countries with rising recycling design, like Poland, are experiencing funds in the rPET capacity.

The UK has the highest e-commerce acceptance rate in Europe, which drives the urge for lightweight, rigid, and protective packaging to ensure safe delivery of products. As the biggest end-user, the food and beverage sector has a constant demand for plastic packaging because of its potential to protect the products and extend the shelf life. The choice for ease among the users, particularly in the food and beverage sector, is driving the urge for flexible packaging designs such as pouches, which serve portable, lightweight, and resealable characteristics.

By Material Type

By Product Type

By Application

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarEurope Plastic Packaging Market