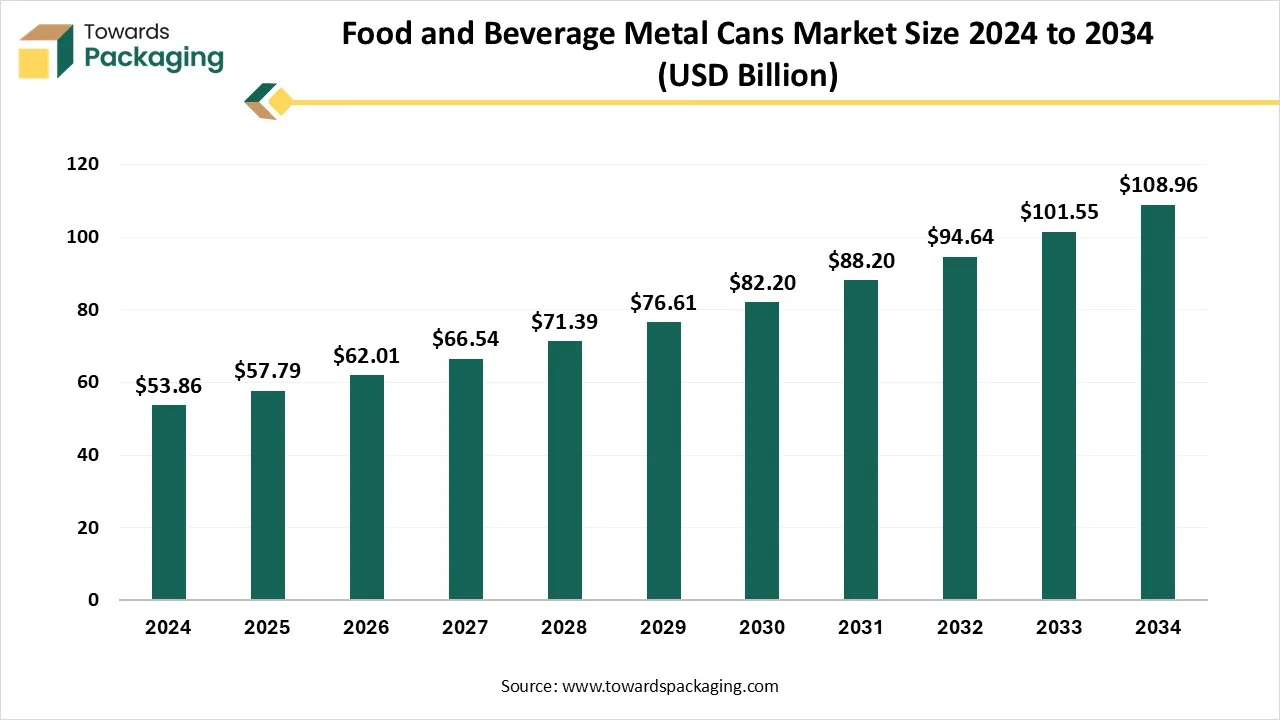

The food and beverage metal cans market is expected to increase from USD 62.01 billion in 2026 to USD 116.91 billion by 2035, growing at a CAGR of 7.3% throughout the forecast period from 2026 to 2035. The demand for food and beverage metal cans is stretching due to the growth in digital printing technology, which has created materials that have become lighter and developed coatings that lower expenses while providing sustainability advantages.

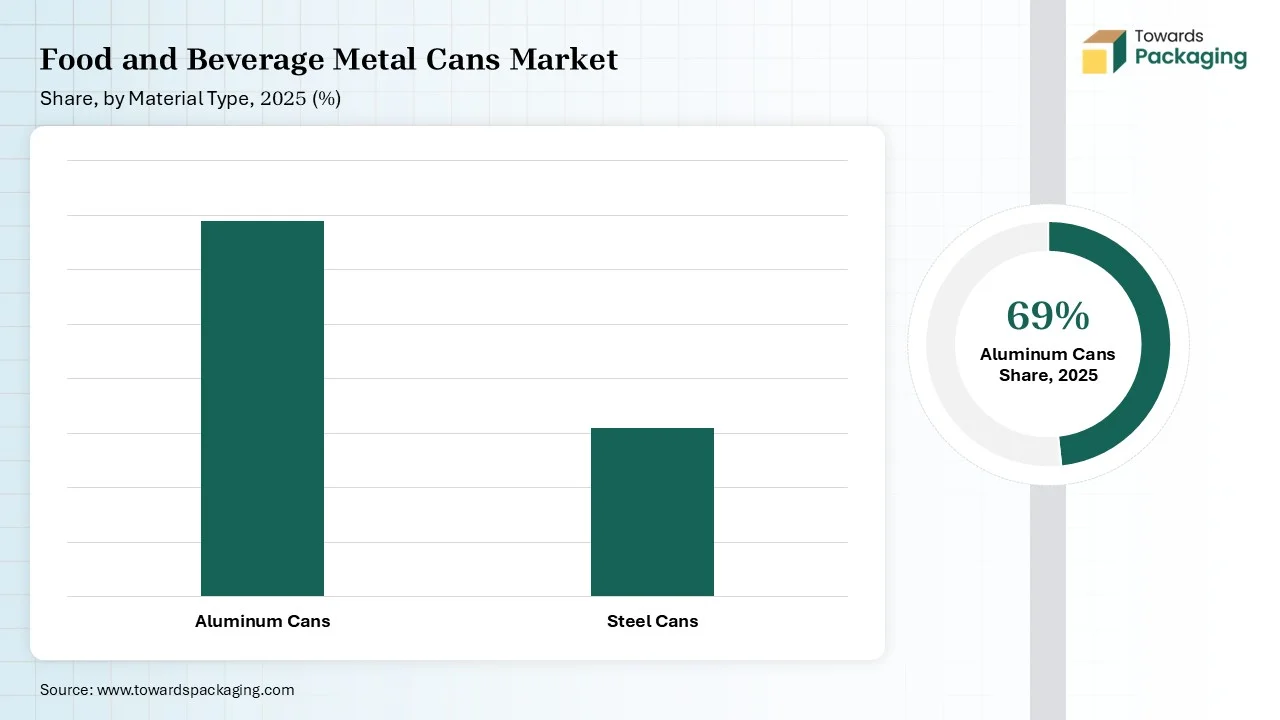

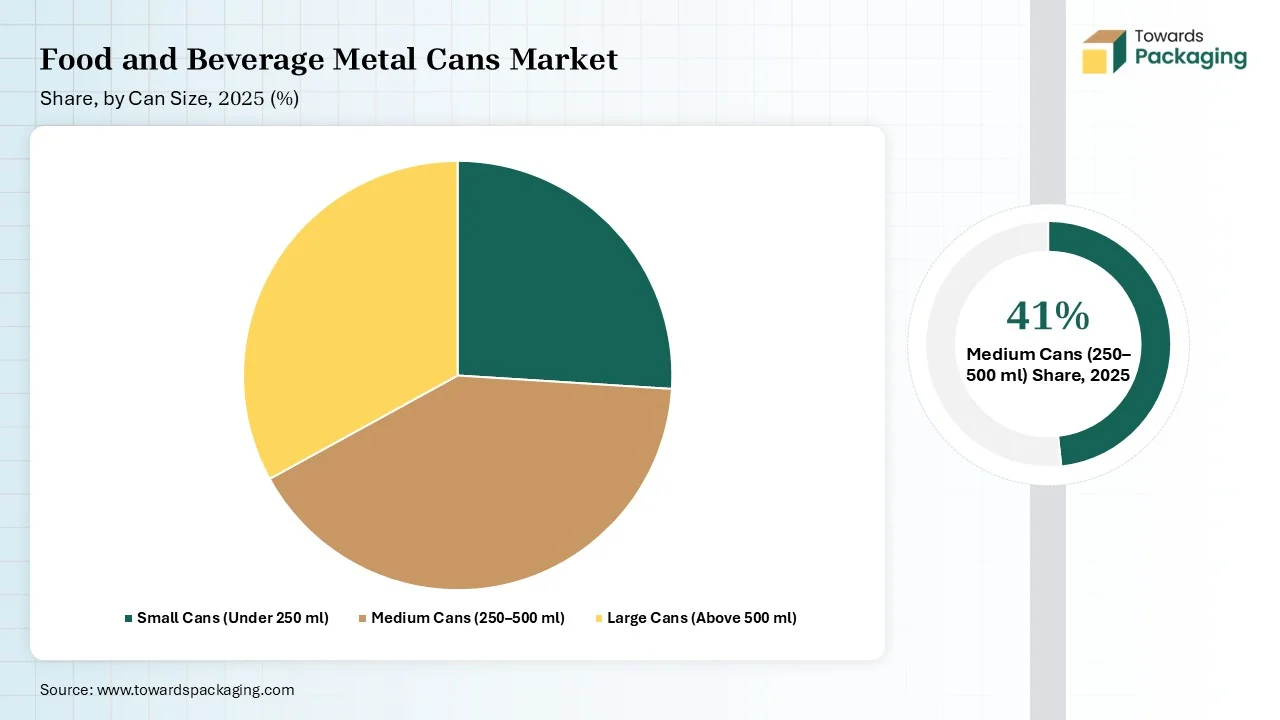

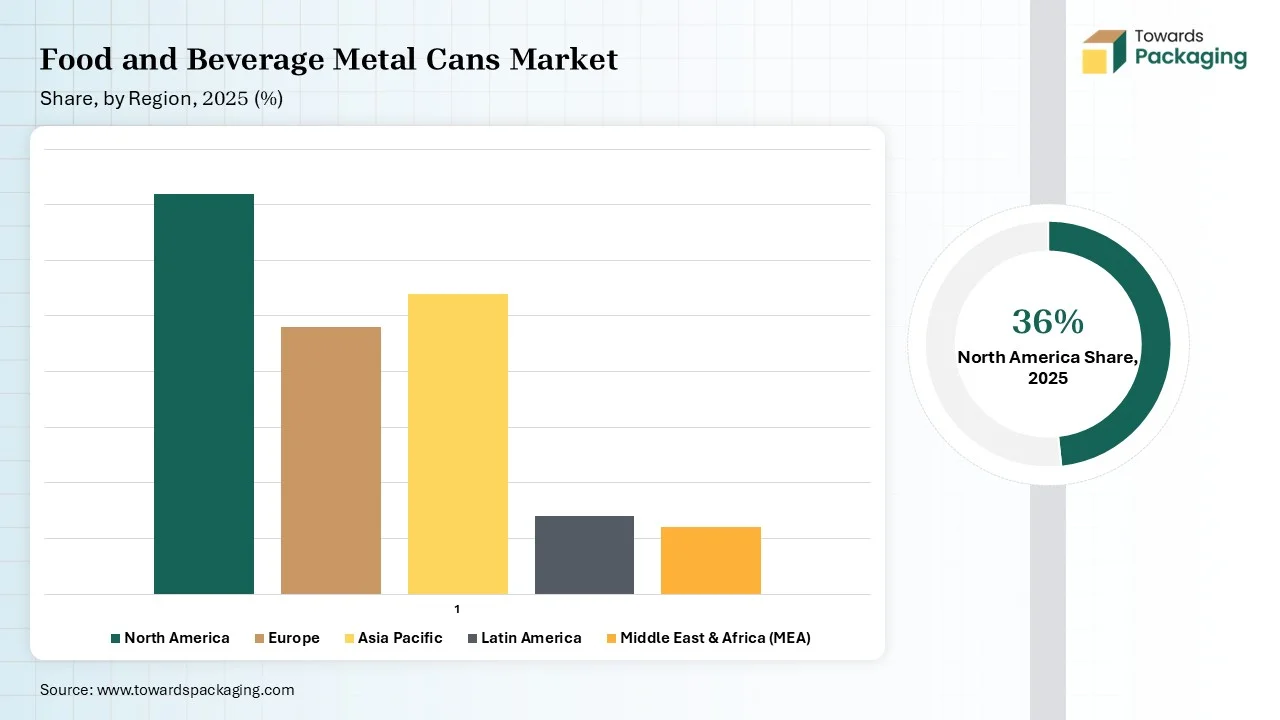

The region, North America, holds the greatest share in 2024, and Asia Pacific is the fastest-growing region. The food and beverage metal cans market is expanding quickly. The most common material type was aluminium cans. Beverage cans were dominated by product type. The medium can account for the largest can size, while the small can is set to grow quickly. By functionality, easy-open cans have dominated the food and beverage metal cans market. By distribution channel, the retail sales are the dominating one, while online sales are the fastest-growing segment.

The food and beverage metal cans market refers to the manufacturing and distribution of metal containers, primarily made of aluminum or steel, used for packaging various food and beverage products. These cans provide a long shelf life, protection from contamination, and maintain the quality and taste of the contents. They are widely used for beverages such as soft drinks, beer, and energy drinks, and foods like vegetables, fruits, and ready-to-eat meals.

Food in cans is convenient to store without using energy. Cans are manufactured in different sizes and shapes to align with the various demands of users. For instance, up to 10,000 80 g cans can fit into one cubic metre. Metal packaging is hence specifically effective in production, storage, and transport, and lowers the risk of spoilage and spillage. To deliver additional stability, cans are often served with grooves, the "so-called" corrugations. These grooves have a functional aim. They allow the can to stretch and compact with temperature changes during the sterilisation procedure without distorting.

The metal can industry hasn't remained motionless. Current inventions have led to the growth of Drawn and Wall iron (DWI) Cans, which show the main advancements in packaging technology. These cans are produced utilising a procedure that draws the metal into shape and then ironing the walls to receive the required thickness and power. DWI cans can serve required material savings as compared to regular can manufacturing procedures. By utilising drawing and ironing procedures, producers can create cans with thinner walls while tracking structural integrity.

This decrease in material usage translates to cost savings and environmental advantages, as less raw material is needed for each can generated. The environmental impact expands beyond material savings. Lighter cans need less energy transport, lowering the carbon footprint linked with distribution. Additionally, the aluminum used in several DWI Cans is highly recyclable, with recycled aluminum needing only 5% of the energy needed to generate new aluminum from raw materials.

Metal cans play a crucial role in extending food shelf life by providing an airtight and light resistant barrier that produces contents from contamination, moisture, oxygen and microbial growth. Without the need for preservatives, the hermetic sealing method used in canning maintains foods nutritional value flavor and quality for long periods of time. Furthermore metal cans are resistant to high-temperature sterilization which eradicates bacteria and guarantees long-term safety. Because of this they are ideal for preserving freshness and minimizing food waste when storing processed foods ready-to-eat meals and drinks.

Metal cans play a significant role in promoting sustainability due to their high recyclability and lower environmental impact compared to many other packaging materials. Materials like aluminum and steel can be recycled multiple times without losing quality, reducing the need for virgin resources and lowering energy consumption. Additionally, metal cans help minimize food waste by extending shelf life and preserving product quality for longer durations. Their lightweight designs and improved manufacturing processes also contribute to reduced carbon emissions during transportation, making them an environmentally responsible packaging choice for the food and beverage industry.

Metal packaging for food has developed mainly over the years. Inventions such as easy-open lids, lightweight aluminum cans, and BPA-free linings have improved both sustainability and convenience. Brands continue to invest in research and development to develop food protection while lowering the environmental impact of packaging waste. Aluminium cans totally dominate the beverage industry, specifically in energy drinks, soft drinks, and beer packaging too. These cans are easy to stack, lightweight, and resistant to breakage, making them the preferred choice for producers. Furthermore, aluminum cans can chill beverages faster than other materials, enhancing the consumer experience.

Metal cans are relatively expensive compared to plastic. First of all, the price of metal materials is relatively high. Secondly, the metal plating process needs assistance, which increases production costs. This may affect the competitiveness of metal cans in particular applications. As compared to lightweight packaging materials, such as metal cans, they are heavier. This may generate inconvenience during travelling and handling, because of energy consumption. For products that need lightweight packaging, metal cans may not be the best choice. Although metal cans have a particular degree of power and stiffness, they may still be damaged or deformed when affected by large external forces. Especially in high-intensity transportation and storage environments, the impact resistance of metal cans may be ineffective, affecting the safety of the content.

Metal packaging protects the world from exterior points, a specifically crucial job for the transportation of toxic substances and food and beverage ingredients. Metal packaging serves as an impenetrable barrier against pollutants from gases, chemicals, and bacteria. But packaging will be as secure as the weakest ink, and for several products, this is the closure. Cans are one of the most protected types of packaging because goods are securely packed at the canned factory, and it's a one-use open; once a can has opened, it can't be reclosed. Food and beverages demand a lot from their packaging format. The metal food packaging can resist the highest heating temperatures, which means the canning procedure can be utilised to protect meat, vegetables, and fish, which would otherwise spoil quickly. Sensitive foods can be steam-exhausted and packed hot to make sure all bacteria are killed, to keep the contents safe and fit to eat months later.

")

Aluminium cans are dominating and the fastest growing due to several reasons, such as they are perfect for preserving food and beverages over extended periods. Like glass and plastic, aluminum is dense to oxygen and light, these two elements, which often lessen flavour and food quality. This feature is especially important for beverages and sensitive products, as it assists in maintaining freshness, taste, and nutritional value. For brands, this expanded shelf life translates into fewer returns because of spoilage and a developed customer experience. Buyers enjoy products that retain freshness for a longer time, whether on a retail shelf or in their pantry at home.

The beverage material type has dominated the food and beverage market, as with the growth in the health and wellness industry, users are seeking beverages with functional advantages. From drinks that boost immunity to gut-health marketing drinks, the urge for health-oriented beverages is growing. Such chemical ingredients utilised in making these functional beverages are vitamins, prebiotics, and minerals. Producers are heavily using these ingredients to reassure concerned users about their health, who expect more advantages through beverage consumption. But a few products, namely collagen, antioxidants, and adaptogens, that were found to serve particular health benefits, have been included in beverages and are on the increase among buyers.

Medium metal cans have dominated the industry as they initially deliver the protection to food products from physical damage, oxygen, and light while also serving a longer shelf life to the inside products of food and beverage containers, and also give easy transportation and storage. The integration of physical protection and barrier properties against expands the shelf life of food products, allowing them to be stored for longer periods without significant quality degradation. The stackable durability and nature of metal can make them perfect for effective transportation and storage, both for users and manufacturers.

")

Small cans are initially made from tinplate (tin-coated plate), that are used in food packaging for many reasons: durability, preservation, and recyclability. They serve as an airtight seal to protect food from oxygen, moisture, and contaminants, expanding shelf life and preventing spoilage. Their rigidness ensures storage and transport, while their recyclability assists sustainability. The strength and rigidity of small cans prevent the food from exterior damage during transportation, handling, and storage, too. This lowers the risk of breakage and leakage, making sure the product reaches the users in perfect condition.

Easy open cans are dominating and fastest growing in terms of functionality, caused by demand in FMCG and food and beverage, serve ultimate integrity and durability, and track freshness and flavor. With the cutting-edge technology, the metal sealing comes in lightweight and is safe for carrying. With the development in living standards, folks want their consumer goods in updated packaged solutions. From tea, coffee, dry powdered food, canned food, and jam to consumer goods, the peel ends have become the latest trend in the packaging industry. The base lids of Pell off ends are created from tinplate or aluminum with a multi-layered plastic membrane, sterilization at extremely high temperature (121 degrees Celsius) and high pressure, thus, the quality of the inside food remains undamaged. Users quickly get attracted to easily open cans because of their attractive colour appearance and easy opening performance.

Direct sales have dominated the market, which plays an important role in examining how products and services reach end-users. These channel series are from direct sales and online platforms to other integrators and distributors. Each channel has its own benefits, with real sales allowing companies to gain greater control over customer relationships and pricing; on the other hand, the third-party distributors can serve a huge market reach and faster scaling. The food segment, specifically in the canned fruit, vegetable, and meat, has experienced the greatest growth in metal cans. Rapid urbanisation, busy lifestyles, and rising preference for single-use packaging have also been growing in the food and beverage industry.

The growth of online retail has significantly influenced the food and beverage metal cans industry. With the growing selection of convenience, users are shifting to e-commerce platforms for purchasing canned food and beverages. This transformation is due to busy lifestyles, and the expansion of online grocery shopping among youth, especially Gen Z and millennials, as they want every product at their doorstep ready, and they are perfect for well-suited online sales handling during shipping from one place to another. The growth in online subscriptions, on-the-go consumption, and ready-to-eat meals has led to the development of online sales in the food and beverage market.

")

")

North America has dominated the market because of the growth in metal can packaging of wine, cocktails, and both hard and soft drinks, heavily driven by rising demand for portability. The beverage sector's dependency on metal cans can be classified into two main categories: alcoholic and non-alcoholic. Also, beer has been the main food packaging, notably wine, other liquors, and glass bottles, too, are now making the transformation to metal cans. Organizations are investing in AI-based production automation, developing embossing technology, and corrosion-proof coatings. The importance is also on encouraging the extended producer responsibility (EPR)schemes, and the growing population of circular economy measures is stressing firms to move towards completely recyclable and renewable materials, such as metal can packaging.

U.S.

The U.S. food and beverage metal cans market benefits from strong demand for canned beverages, carbonated drinks, and ready-to-eat foods. The use of aluminum cans is supported by high recycling rates and reliable collection systems. To achieve sustainability goals, manufacturers are concentrating on lighter cans with more recycled materials. Innovation in can coatings and designs further boosts growth.

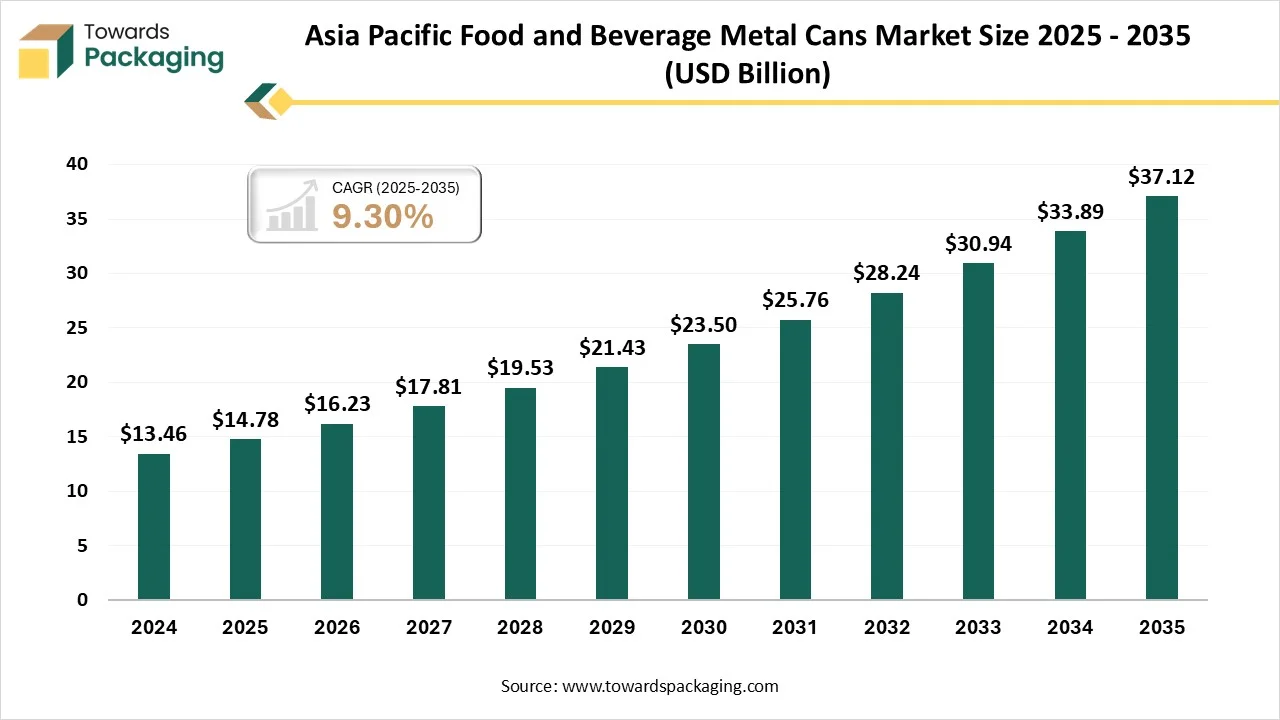

The food and beverage metal cans markets in Asian countries like India, China, Japan, and South Korea are witnessing a transformative change, driven by urbanization, transforming consumer lifestyles, and growing demand for convenience. Inventions in sustainable packaging, moves in buyer decisions, and technological advancements are creating opportunities, shaping the industry's future prospects. Elements like the expansion of organized retail, uptick in exports, and growing middle-class income group are supporting the industry. Nanofabrication technologies are growing as cutting-edge solutions to make active materials for use in the design of coatings, packages, and packaging technologies. These solutions assist in maintaining and improving sensory and nutritional characteristics, developing shelf life, and increasing food safety.

India

India’s market is growing due to growing urbanization and the consumption of packaged foods and drinks. Adoption of metal cans is increasing due to increased awareness of food safety and longer shelf life. Stable demand is supported by the growth of organized retail and food processing industries. The use of recyclable metal packaging is being progressively promoted by sustainability initiatives.

The MEA market is supported by the demand for robust, long-lasting food packaging and the increase in beverage consumption. Due to their powerful barrier qualities, metal cans are more in demand in hot climates. Local manufacturing and food security investments are increasing market penetration but the regions infrastructure for recycling is still uneven.

UAE

The UAE market benefits from a strong hospitality, tourism, and food service sector. Steady growth is supported by the high demand for imported food items and canned beverages. Recyclable packaging options are encouraged by government sustainability initiatives. Demand for high-end products and sophisticated retail infrastructure supports the use of metal cans.

Metal cans are primarily made from aluminum and steel, sourced from mining and recycled scrap. Rising focus on lightweighting and recycled metal content supports sustainability goals.

Efficient logistics are critical due to high production volumes and global beverage demand, with manufacturers relying on regional plants and just-in-time supply models.

Metal cans offer high recycling rates and strong circularity, though collection efficiency varies by region.

By Material Type

By Can Type

By Product Type

By Can Size

By Coating Type

By Functionality

By Distribution Channel

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarFood and Beverage Metal Cans Market