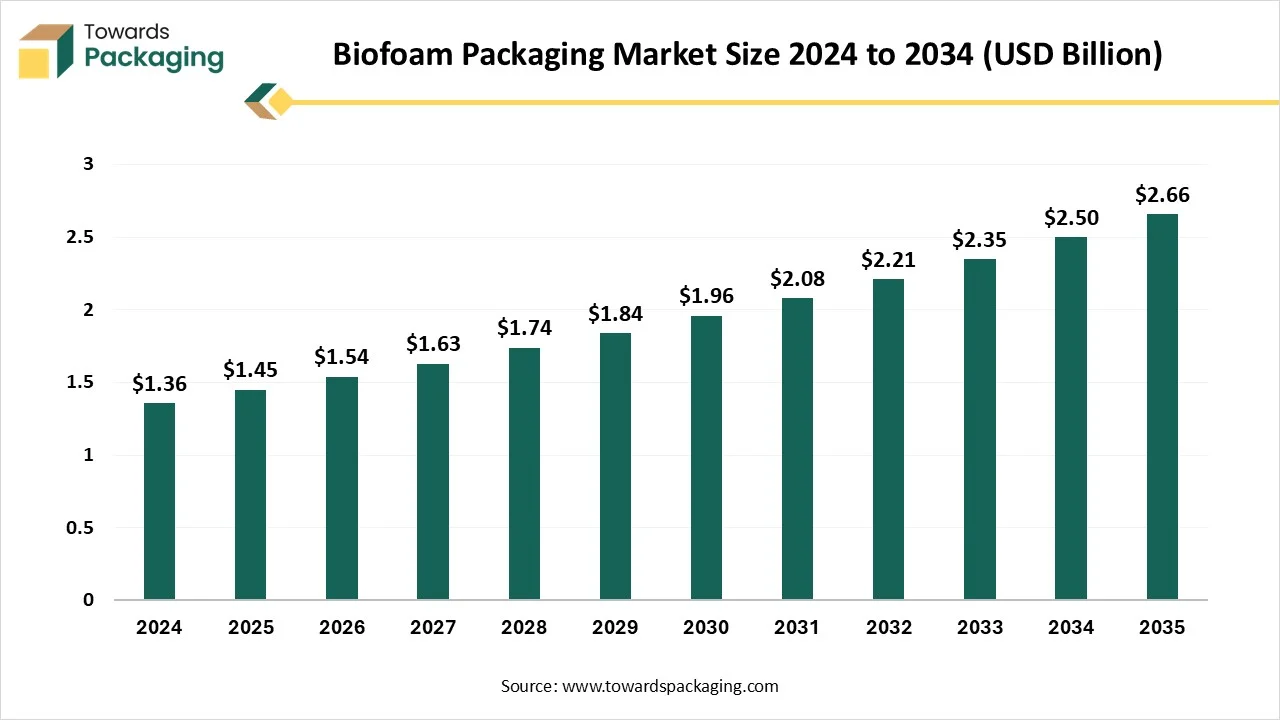

The biofoam packaging market is forecasted to expand from USD 1.91 billion in 2026 to USD 8.80 billion by 2035, growing at a CAGR of 18.5% from 2026 to 2035. The rising concern towards ecological issues has influenced the demand for this market and has raised the innovation process as well. Increasing e-commerce industry and technological innovation are the major factors driving the growth of this market.

The biofoam packaging market comprises protective and cushioning packaging materials produced from renewable, bio-based or compostable feedstocks (for example mycelium/mushroom composites, starch-based foams, cellulose foams and bio-polymer foams such as PLA/PHA blends). These biofoams are designed to replace traditional fossil-based foams (EPS, EPE) by offering comparable protective performance while reducing lifecycle greenhouse-gas emissions, enabling industrial or home compostability, and meeting increasing regulatory and corporate sustainability requirements across electronics, food, medical and consumer goods packaging applications.

The biofoam packaging market is experiencing major advancement in the manufacturing process with the expansion of recyclable, renewable, and biodegradable bio-based polymers. The huge demand for enhanced barrier properties has raised the demand for this market. The advancement of reusable biofoam packages without compromising with its quality.

For instance, Woamy’s origin invention in a foam wood research program directed at Aalto University in which Woamy’s initiators were part of evolving the original biofoam technology. Analysing its capacity to replace fossil-founded plastic foams, they created the corporation to link the gap between study and real-world utilization.

The major raw materials utilized in this market are extracted from agricultural products such as sugarcane, corn starch, vegetables fats & oil.

The component manufacturing in this market comprises agricultural waste, cellulose, starches, and vegetable oils.

This segment comprises enhanced R&D, improve consumer protection, and strategic partnership.

| Type Segments | Market Share 2025(%) |

| Starch-based Biofoam | 40% |

| Polylactic Acid (PLA)-based Biofoam | 15% |

| Polyhydroxyalkanoates (PHA)-based Biofoam | 10% |

| Mycelium-based Biofoam | 5% |

| Cellulose / Nanocellulose Foams | 7% |

| Bagasse / Sugarcane Fiber Foams | 6% |

| Protein-based & Other Biopolymer Foams | 17% |

The starch-based biofoam segment dominated the market with 40% share in 2025 due to its biodegradability and availability. It is highly driven by the increasing e-commerce industry and huge demand for biodegradable packaging substitute. Starch-derived resources are measured ecologically and financially profitable, mainly when obtained from engineering by-products. The enhancement in e-commerce sector is highly influenced by biofoam packing demand across several industries such as consumer goods, automotive, and electronics.

The polyhydroxyalkanoates (PHA)-based biofoam is the fastest-growing in the market with a CAGR of 12%, as it includes strong ecological profile, versatile properties, superior biodegradability, and source flexibility. This segment has been accepted for utilization in food contact requests, like disposable cups and cutlery.

The Polylactic Acid (PLA)-based biofoam segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to strict regulatory guidelines associated with this segment. It is a biopolymer extracted from renewable plant bases such as cassava, cornstarch, and sugarcane making it an environment-friendly substitute to plastic based on fossil. These foams provide main properties equivalent to outdated foams, like insulation and cushioning, making it appropriate for a huge variety of applications, comprising food & beverage, consumer goods, and electronics.

")

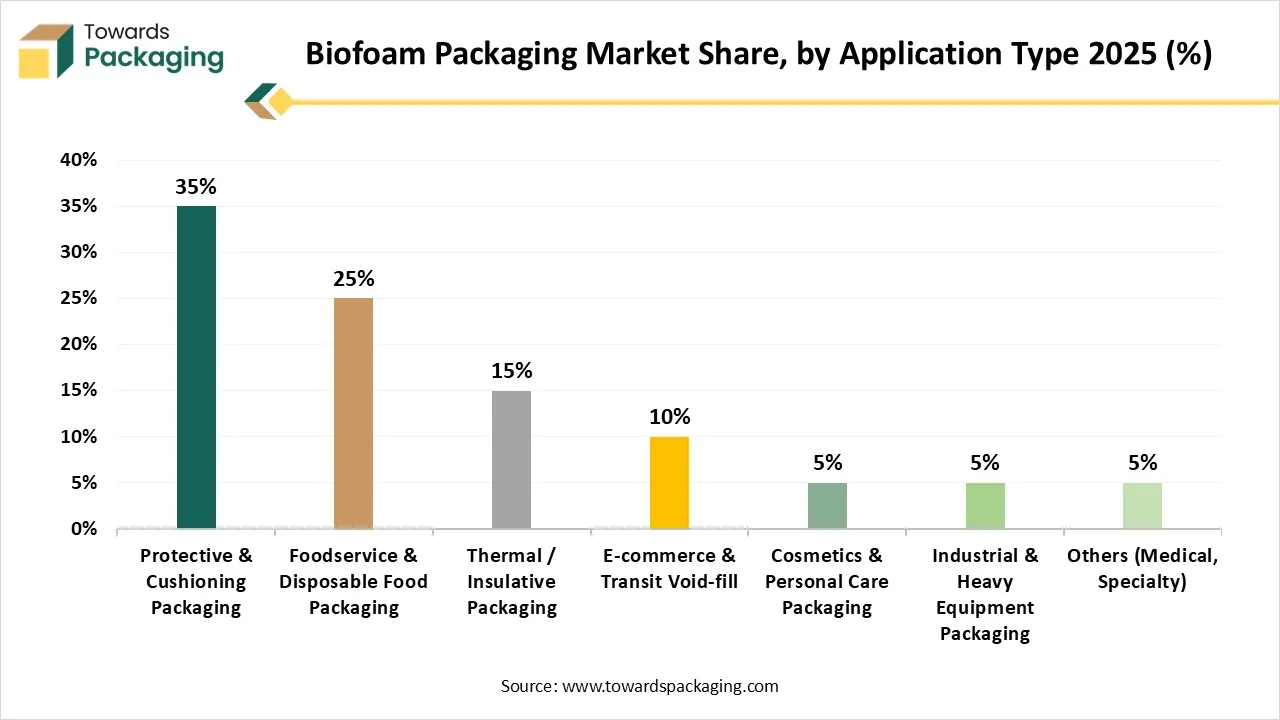

The protective & cushioning packaging segment dominated the market with highest share in 2025 due to its safe transportation capacity. Advancement in production techniques have improved the presentation of biofoams, enhancing their moisture resistance, thermal lining, and mechanical strength. This promotes biofoams as a commercially feasible and high-execution additional for old-style foams used in protecting purpose. Biofoam are used as a biodegradable substitute to traditional packaging peanuts for invalid filling and common cushioning usages.

The foodservice & disposable food packaging segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to increasing demand for hygienic and innovative packaging solution. It is highly influenced by the rising demand for sustainable packing resolutions that fulfil supervisory needs and customer preferences. Biofoam packing is mainly common for fresh production, dairy items, and ready-to-eat mealtimes, where it provides superior insulation and shield against pollution.

The thermal / insulative packaging is the fastest-growing in the market with a CAGR of 15%, as there is a huge demand for sustainable insulations resources. Within temperature-measured packing, insulated vessels are the significantly growing segment, utilized in shipping sensitive goods in several quantities. These are cost-effective and provide exceptional insulation properties.

| Form Segments | Market Share 2025(%) |

| Molded Foam Inserts / Parts | 42% |

| Loose-fill / Peanuts / Pads | 15% |

| Foam Sheets / Rolls / Liners | 10% |

| Foam Trays & Clamshells | 10% |

| Blocks & Cut-to-size Foam | 8% |

| Pelletized / Injection-molded Foam Components | 15% |

The molded foam inserts / parts segment dominated the market with highest share in 2025 due to huge adoption for customized packaging. The growth of e-commerce has resulted in a noteworthy increase in the requirement for protective packing, improving demand for this segment for transporting electronic and fragile products.

The loose-fill / peanuts / pads segment is expected to grow at the fastest CAGR during the forecast period. This segment is growing due to huge demand for flexible packaging in various industries. It offers biodegradable as well as environment-friendly packaging substitute which help in the growth of the market. As customers and industries become more ecologically aware resulting in the rise of the demand for biofoam loose-fill and several other sustainable packing.

The foam sheets / rolls / liners are the fastest-growing in the market with a CAGR of 15%, as there is a huge demand for versatile and protective packaging. The increasing demand for flexible biofoam has enhanced by various trends, comprising the rapid extension of e-commerce industry and a growing customer preference for biodegradable and sustainable packaging substitutes. In specific, biofoam rolls and sheets are appreciated for their protective and cushioning goods during transportation.

")

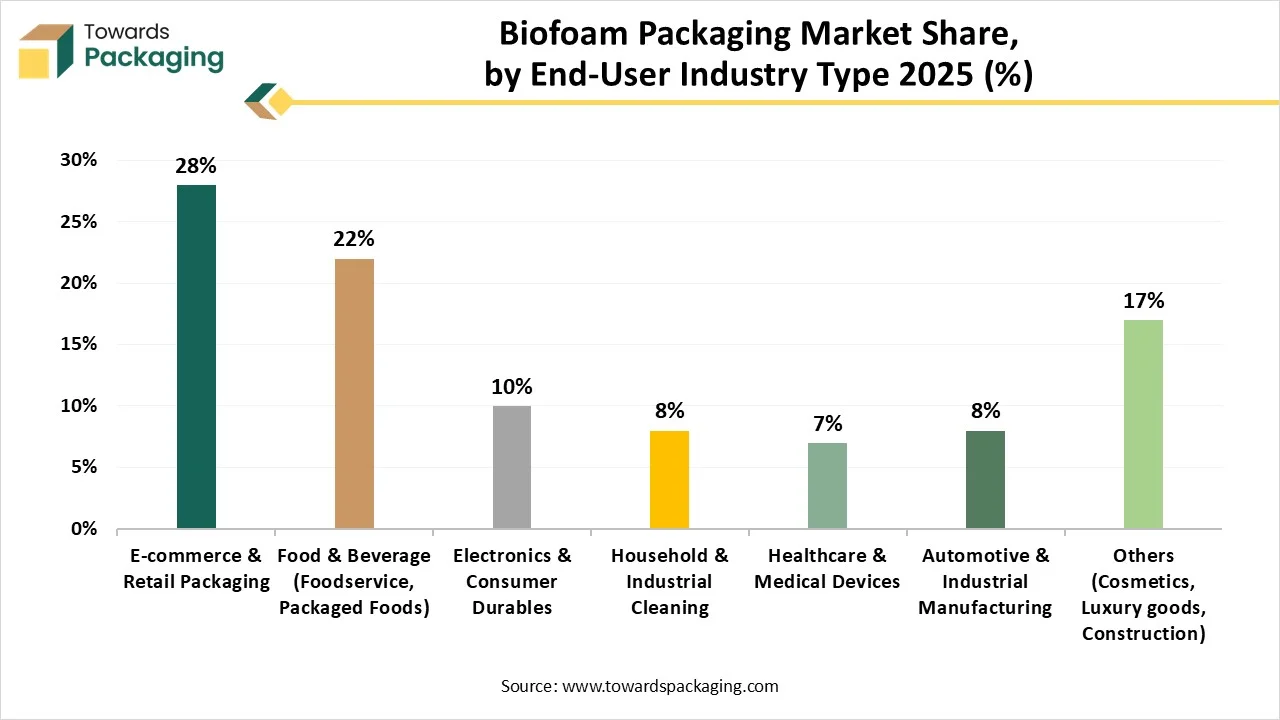

The e-commerce & retail packaging segment dominated the market with highest share in 2025 due to rising construction of buildings. The increasing electronics, healthcare, automotive, and food & beverages has influenced the demand for this segment. The growth in online shopping and customer demand for eco-friendly delivery choices has resulted in rapid growth in biofoam acceptance within the e-commerce and trade logistics chains.

The food & beverage (foodservice, packaged foods) segment is expected to grow at the fastest CAGR during the forecast period. This segment is increasing because of regulatory guidelines and consumer preferences. Governments across the globe are applying stricter guidelines and bans on one-time plastics usage. This boosts food & beverage producers to find biodegradable and compostable substitute.

The electronics & consumer durables segment expects the significant growth in the market, as there is a huge demand for protective packaging. Well-known electronics brands are progressively accepting sustainable packing to decrease their ecological appeal and footprint to environment-conscious customers. The requirement for defensive packing for a wide range of products sold online influences demand for biofoam packaging as a cost-efficient and ecologically friendly pitch.

")

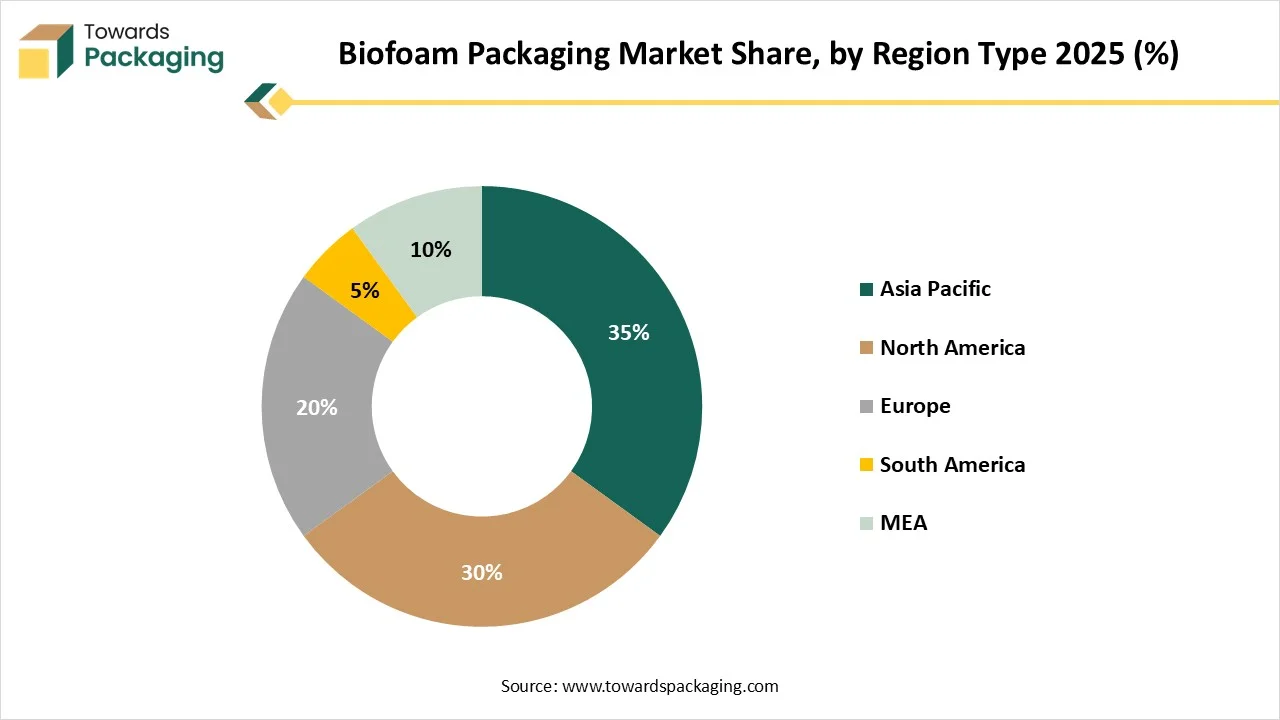

Asia Pacific held the largest share in the biofoam packaging market in 2025, due to rising demand for sustainable packaging solution. Rapid population increase and industrialization, mainly in countries such as Japan, China, India, South Korea, Taiwan, and various other are generating high demand for packing resolutions across several sectors. The huge development of e-commerce industries in the region influences a requirement for sustainable and protective packaging for transportation of products. Investments in production technology and invention are offering to the growth and manufacture of biofoam products.

China has huge e-commerce sector which is fuelling the growth of market. It generates a huge requirement for sustainable, lightweight, and protective packaging which biofoam delivers. China has a widespread industrial improper with cultured manufacturing potentials, permitting it to rapid scale up the production of sustainable resources such as cornstarch biofoam. This offers a cost-operative and effectual distribution chain.

Rapid advancement in the production process has influenced the growth of the market in North America. There is huge customer demand for environment-friendly and sustainable packaging substitutes. Strict ecological guidelines and strategies are boosting the market to adopt biodegradable solution. It is profoundly supported by government guidelines promoting environment-friendly resources and the occurrence of main end-use sectors such as furniture, packaging, and automotive.

Several industries are attracting a huge number of consumers base with the adoption of eco-friendly packaging choices. It is influenced by strong customer demand for the production of sustainable packaging and strict guidelines on one-time usage of plastics. Supportive government creativities and early acceptance of new technologies boost this development. Innovations in resources, such as fungi-based and plant-based foams, are also enhancing the market.

The major factor influencing the growth of market is the increasing public awareness. Production of cellulose-based packaging has raised this market to grow significantly in this region. The demand for lightweight, durable, and safe packaging has enhanced the demand for huge production of this type of packaging.

Germany is rapidly adopting biofoam packaging due to enhanced production process as well as continuous innovation in this. The expansion of online retail has enhanced the demand for sustainable, protective and lightweight packaging. Biofoam offers exceptional thermal and cushioning protection while fulfilling the requirement for environment-friendly delivery materials.

The major factors influencing the growth of the market in Latin America are rapid growth of e-commerce sector, increasing ecological concern, supportive government guidelines, and technological innovation. Presence of huge number of market players has also support in the expansion of this market. Its premium packaging quality has also enhanced this market expansion.

The huge production of sugarcane fiber based biofoam is increasing due to the increasing concern towards bio-based plastic packaging. This natural resource abundance helps a competitive and increasing local bio-based plastics sector. Ecological awareness is growing among customers in Brazil, and showing huge willingness to recompence a premium for environment-friendly packing. This trend is mainly visible in personal care products, food & beverage.

The market in the Middle East is experiencing rapid growth, driven by rising environmental awareness, regulatory push against single-use plastics, and increasing demand from food, e-commerce, and consumer goods sectors. Challenges include high production costs, limited composting infrastructure, and material performance in hot, humid climates. Opportunities exist in targeting premium segments, forming local partnerships, and aligning with sustainability regulations. Overall, the Middle East presents a promising yet emerging market for eco-friendly biofoam packaging solutions.

In Saudi Arabia, the biofoam packaging market is growing rapidly, driven by government initiatives, rising environmental awareness, and increasing demand from food, e-commerce, and consumer goods sectors. Although compostable packaging is still emerging, it is anticipated to grow steadily. Overall, Saudi Arabia presents a promising market for eco-friendly packaging solutions, supported by regulatory support and sustainability investments.

Corporate Information

The company reports federal funding: e.g., “Federal Partners: $26.2 M through 2024” per their website.

Raised substantial venture/scale funding:

By Type

By Application

By Form

By End-User Industry

By Region

North America

South America:

Europe

Asia Pacific

MEA

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarBiofoam Packaging Market