The rigid polyolefin market is expanding rapidly, driven by rising demand from packaging, automotive, healthcare, and consumer goods sectors. We cover complete market size and forecasts, with insights showing Asia Pacific holding 48% share in 2024, while PP dominated product type with 45% share. Our report explains key manufacturing processes like injection molding (40% share), and provides deep-dive segmentation data, regional analysis across NA, EU, APAC, LA & MEA, a full competitive landscape of Tier 1–3 companies, value chain mapping from raw materials to logistics, and trade analysis showing the global movement of PP, PE and HDPE. We also include detailed supplier and manufacturer profiles, emerging sustainability trends, and investment opportunities.

The rigid polyolefin is a growing segment of the global plastics industry, focusing on durable, lightweight, and versatile polyolefin materials such as polypropylene (PP) and polyethylene (PE) used in rigid applications. These polymers are widely employed due to their cost-effectiveness, chemical resistance, recyclability, and excellent mechanical properties.

The market is driven by the rising demand in packaging, automotive, consumer goods, and construction industries, coupled with regulatory pushes for recyclable and sustainable materials. Increasing use of rigid polyolefins in food packaging, automotive lightweighting, and medical devices is further supporting growth.

However, challenges such as fluctuating crude oil prices (affecting resin costs), competition from alternative materials (e.g., bioplastics, paper), and environmental concerns related to plastic waste present restraints. Nevertheless, advancements in polymer modification, improved recycling technologies, and growing circular economy initiatives are expanding opportunities in this market.

| Metric | Details |

| Key Drivers | - Strong demand from packaging, automotive, consumer goods, and construction industries. - Increasing adoption in food packaging, medical devices, and automotive lightweighting. - Regulatory push for recyclable and sustainable materials. |

| Leading Region | Asia Pacific |

| Market Segmentation | By Product Type, By Manufacturing Process, By Application, By End-Use Industry and By Region |

| Top Key Players | ExxonMobil Chemical, LyondellBasell, SABIC, Dow, Reliance Industries, Sinopec, Chevron Phillips, PetroChina, TotalEnergies, Hanwha Total Petrochemical, BASF, Repsol, OMV Group |

The integration of AI technology in the rigid polyolefin market plays an important role in the selection process of raw materials. Advanced technology such as artificial intelligence and machine learning is widely used to fine-tune production procedure by analysing operational and sensor data in real-time. It supports manufacturers to optimize variables such as pressure and temperature. AI is used in developing recyclable polyolefin and offer enhanced operational efficiency, promote sustainable choices, and accelerating innovation.

Strong Demand from Several Sectors

The robust demand from several sectors such as construction, packaging and automotive has influenced the demand for the rigid polyolefin market. The combination of compounds like polypropylene (PP), and high-density polyethylene (PE) has helped the major market players to develop cost-effective, durable, and light weight product which is widely accepted by various industries. Rapid growth in food and beverages industry has boosted this market with huge production demand due to its capacity to preserve integrity of the product. It has properties such as moisture resistant which appeal a wide range of consumers towards it. Its corrosion resistant and chemical stability quality make it suitable for using in piping and building purpose for long-term performance.

Strict Ecological Concern

Strict ecological consciousness and fluctuation in natural gas and crude oil charges have hindered the expansion of market. Slow improvement in the infrastructure of recycling process has also restricted the growth of the market. High charges, high inflation, and economic pressure have limited the development of rigid polyolefin.

Increasing Sustainable Packaging Solution

Increasing demand for sustainable packaging choices has raised the opportunities for the market. The rising demand for recycled content in countries like India and the U.S. are promoting the production of post-consumer recycled polyolefin packages. The rapid switch towards usage of single-material packaging has made the recycling process easier. It attracts huge number of consumers due to its durability and cost-efficiency in packaging majorly in industries like consumer goods, food & beverages. Expansion in the healthcare sector and advancement in the automotive sector has raised the opportunities to grow rapidly.

")

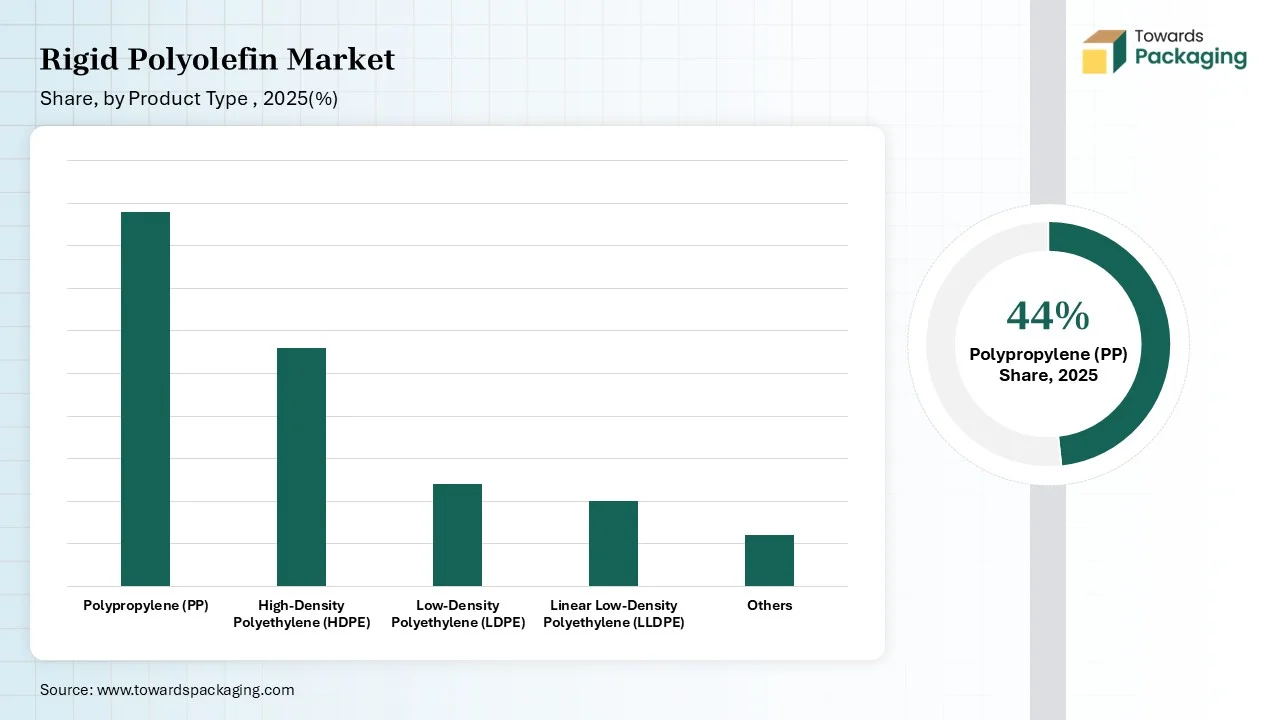

The polypropylene (PP) segment dominated the rigid polyolefin market in 2024 due to its superior balancing properties. It has properties like impact strength, low density, rigidity, and high heat resistance. These make this product suitable option for consumer goods, packaging, and automotive. It is used in the electronics, food containers, medicine bottles, and automotive interiors which influence the development of specialized grades and polypropylene compounds. These are widely used in healthcare sector for diagnostic, medical device, and syringes packaging.

The high-density polyethylene (HDPE) segment is expected to grow at the fastest rate in the market during the forecast period. This segment is growing due to its moisture barrier capacity. This product is extensively used in construction use, agricultural films, sheets, and pipes. The increasing e-commerce, rising urbanization, industrialization, and food and beverages industries has boosted the demand for this product.

The injection molding segment held the largest share of the rigid polyolefin market in 2024 due to the demand for development of enhanced-quality and complex parts. The efficient automated procedure and cost-efficiency have raised the demand for this manufacturing type. It has the capacity to generate suitability for mass production and lightweight products. Major industries utilizing this segment are packaging, automotive, and healthcare sector. There is a huge demand for durable, precisely shaped, and lightweight packaging. It is highly capable if producing small and précised structures.

The blow molding segment is expected to grow at the fastest rate in the market during the forecast period. This segment is growing rapidly due to the increasing demand for hollow packaging products. It comprises inflation of a plastic tube with a mold which help in the production of automotive fuel tanks, jugs, and bottles. It is widely utilized in industries of household products, food & beverages.

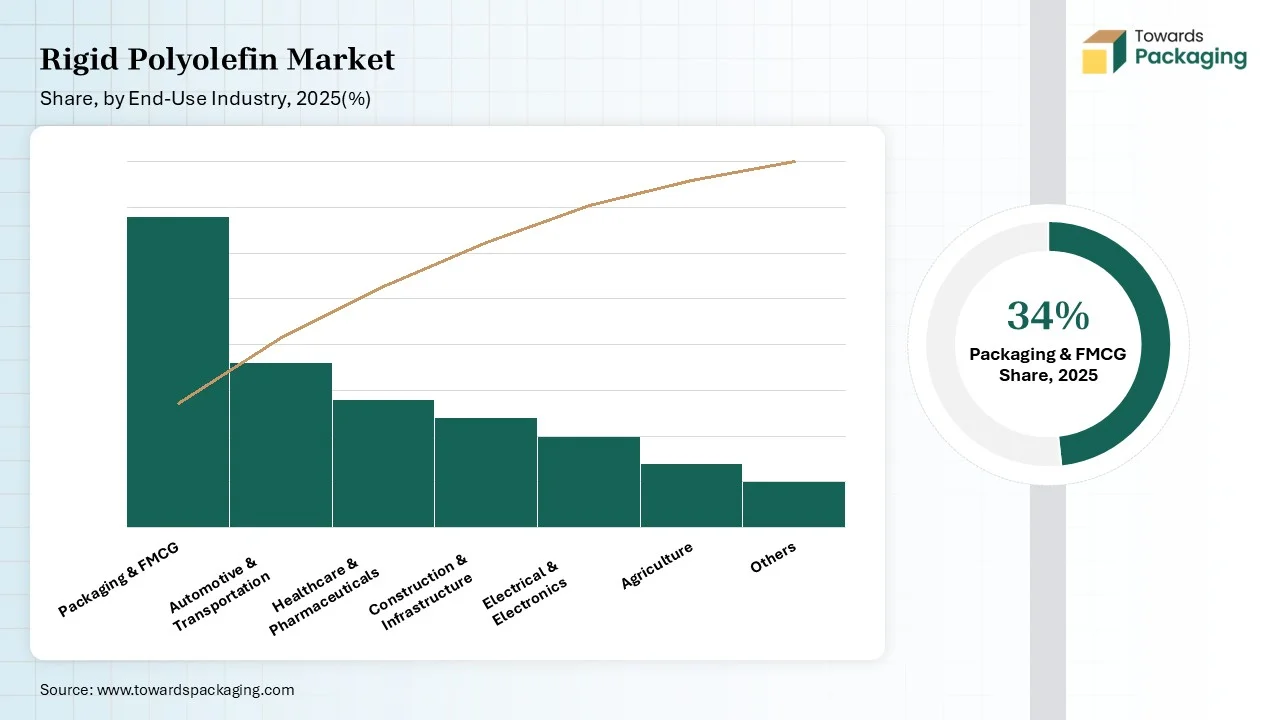

The packaging segment held the largest share of the market in 2024 due to huge demand for bottles, jars, trays, cups, and tubes. This segment has high demand in industries like cosmetics & toiletries, food & beverages, and healthcare. The huge requirement of durable, cost-efficient, and protective qualities rigid polyolefin packaging to protect products from damage. There is a high demand for packaging in industries like healthcare, pharmaceutical, cosmetics & toiletries, and food & beverages.

The healthcare & medical devices segment is expected to grow at the fastest rate in the market during the forecast period. This segment is growing rapidly due to its durability, cost-efficiency, and sterility. This segment comprises a huge range of products such as surgical tools, diagnostic devices, medical equipment housing, and drug delivery system. Rigid polyolefins are chemical resistance, durable, rigid, and cost-effective packaging solution for healthcare sector.

")

The packaging & FMCG segment held the largest share of the market in 2024 due to its cost-efficacy and durability. This segment is influenced by the development of personal care, food and e-commerce services which raise the demand for highly protective packaging. There is a huge demand for recyclable and sustainable packaging has influenced the demand for this packaging. The rapid expansion of the pharmaceutical, food & beverages, and personal care industry has raised the demand for this segment. The rising trend of using mono-material usage in packaging has raised the production process.

The automotive & transportation segment is expected to grow at the fastest rate in the market during the forecast period. This segment is growing rapidly due to impact resistance, durability, and lightweight properties. The major growth factors comprise rising worldwide demand for automobiles particularly electric vehicles (EVs). The increasing demand for sustainable, safe, and efficient packaging has boosted the development of this market.

")

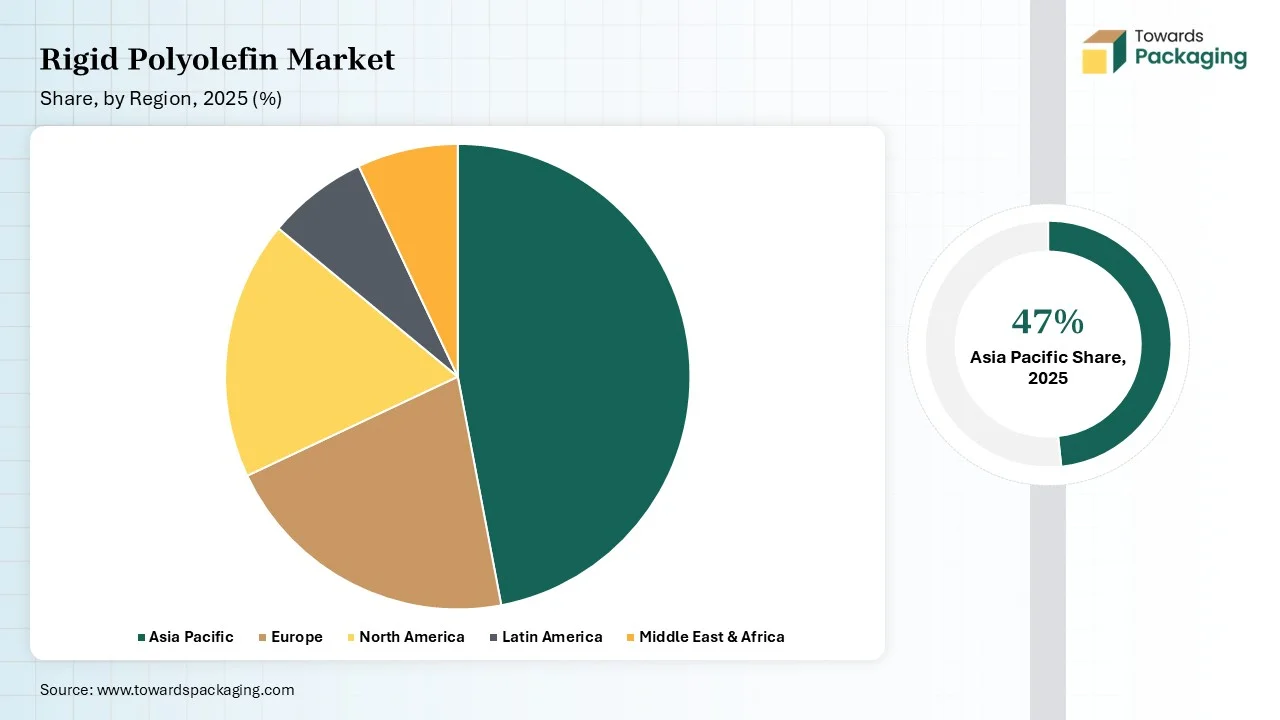

Asia Pacific held the largest share of the market in 2024, due to expansion in the packaging necessities. Rapid urbanization & industrialization has enhanced the usage of rigid polyolefin. Rising e-commerce sector has raised the demand for strong courier system which has boosted the development of this industry in this region. Rapid expansion of automotive industry has driver the consumption of polyolefin. The increasing usage in production of automotive parts such as dashboard and bumpers has enhanced the demand for this market.

There is a huge substantial demand for polyolefin for packaging in various industries have promoted the expansion of the market in China. It is considered as the largest manufacturing hub of several industries raise the demand for packaging with enhanced quality. Strong growth of construction department has boosted the utilization of such packages and its advancement.

Europe expects significant growth in the rigid polyolefin market during the forecast period. This market is growing due to rising demand for convenience in the packaging industry. Expansion of food and beverages industry has influenced the demand for packaging which can enhance the shelf life of the food products. It has a huge demand in the automotive as well as healthcare sector due to its stringent quality.

The major raw materials utilized in this market are natural gas and crude oil to derive materials such as propylene, olefin, and primary ethylene.

The major components used in this market are injection molding, extrusion coating, and blow molding.

This segment plays an important role in strategic supply chain management for efficient delivery.

Tier 1

Tier 2

Tier 3

By Product Type

By Manufacturing Process

By Application

By End-Use Industry

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarRigid Polyolefin Market