The sustainable flexible packaging market is accelerating, with forecasts predicting hundreds of millions in revenue growth between 2026 and 2035, powering sustainable infrastructure globally. The growing consumer demand for sustainable flexible packaging, growing environmental awareness, increasing regulatory pressures, rising innovation in flexible packaging materials, increasing focus on achieving sustainability goals, and supportive government regulations promoting eco-friendly alternatives are expected to drive the growth of the global sustainable flexible packaging market over the forecast period. Plastic takes almost 1000 years to decompose, which spurs the demand for sustainable flexible packaging materials.

It plays a crucial role in significantly lowering carbon footprints, reducing waste, and plastic pollution across various industries such as food & beverages, pharmaceuticals, cosmetics & personal care, consumer goods, e-commerce, industrial packaging, agriculture & horticulture, and other (toys, electronics). Sustainability is the key focus and greatest option for lowering plastic waste. Several companies operating in the market are focused on adopting sustainable, flexible packaging materials to align with the principles of the circular economy. Additionally, the market is expanding rapidly in Europe, fuelled by rising focus on adopting sustainable flexible packaging, stringent government initiatives to lower greenhouse gas (GHG) emissions, and growing demand from multiple industries.

The sustainable flexible packaging market refers to the sector dedicated to the development and use of eco-friendly packaging solutions that reduce environmental impact. These packaging solutions are made from materials that can be recycled, reused, or biodegraded, while still maintaining the required functionality, safety, and durability for packaging products. Sustainable flexible packaging includes innovations such as biodegradable films, recyclable laminates, and reduced plastic usage, helping to meet the growing demand for environmentally conscious packaging from industries like food & beverage, pharmaceuticals, consumer goods, and others.

The EU is effectively tackling the single-use plastic items most commonly found on Europe’s beaches and is promoting sustainable alternatives. 32 million tonnes of plastic waste per year in Europe. In 2023, the Commission adopted measures that restrict microplastics intentionally added to products under the EU chemical legislation REACH. It also proposed new rules to prevent plastic pellet losses in the environment. These actions will directly contribute to reaching the 30% reduction target for microplastic releases set out in the Zero Pollution Action Plan.

Raw Material Sourcing – Raw material sourcing involves compostable polymers and bio-based materials for creating commendable biodegradable films. Mono material films, paper alternatives, fiber, and recycled content are bolstering the market expansion in the packaging line.

Material Processing and Conversion – The lightweight content and bio material unification are encouraging the converters and next-generation extrusion systems to bolster the pathways for sustainable processing with the smart tech solutions.

Recycling and Waste Management – The robust transition highlights the circular system featuring the power of chemical recycling and modern mechanical merging, aligning with the sustainable mono-material designs. The transitions in the packaging line are getting sustainability closer to the government’s green initiatives.

Growing regulations about compostability, recyclability, and the removal of dangerous chemicals are driving the development of sustainable flexible packaging, requiring manufacturers to completely rethink their materials. Regulations prohibiting PFAS-specific inks and hazardous additives are influencing formulation decisions and encouraging producers to switch to safer bio-based substitutes. Reducing packaging weight is another regulatory priority that promotes thinner structures and efficient use of resources without sacrificing functionality. To increase consumer awareness and waste sorting efficiency, many regions are also implementing mandatory recyclability labeling. Additionally, certification programs for compostable and bio-based materials bolster credibility. In general, eco-design principles and circular materials are becoming more prevalent in flexible packaging applications due to sustainability regulations.

| Category | Volume / Year |

| Sustainable PE/PP Films | 19.5 million tons |

| Paper-Based Flexible Packs | 11.2 million tons |

| Compostable Films | 3.4 million tons |

| Bio-based PLA/PHA Films | 2.1 million tons |

| Recycled Content Flexible Films | 6.8 million tons |

The EU 2024/2025 regulation under PPWR mandates reuse, refill, and minimal packaging practices. Packaging must be optimized to reduce material use, unnecessary packaging avoided, and reuse/refill options encouraged, especially for takeaway food, beverages, and retail packaging. Restrictions on certain single-use plastics, such as lightweight bags and disposable containers, push companies toward sustainable packaging formats, including reusable, refillable, compostable, or recyclable solutions. These combined regulatory pressures make sustainable packaging both a market requirement and a compliance mandate, accelerating the industry-wide shift toward circular-economy packaging practices and environmentally conscious materials.

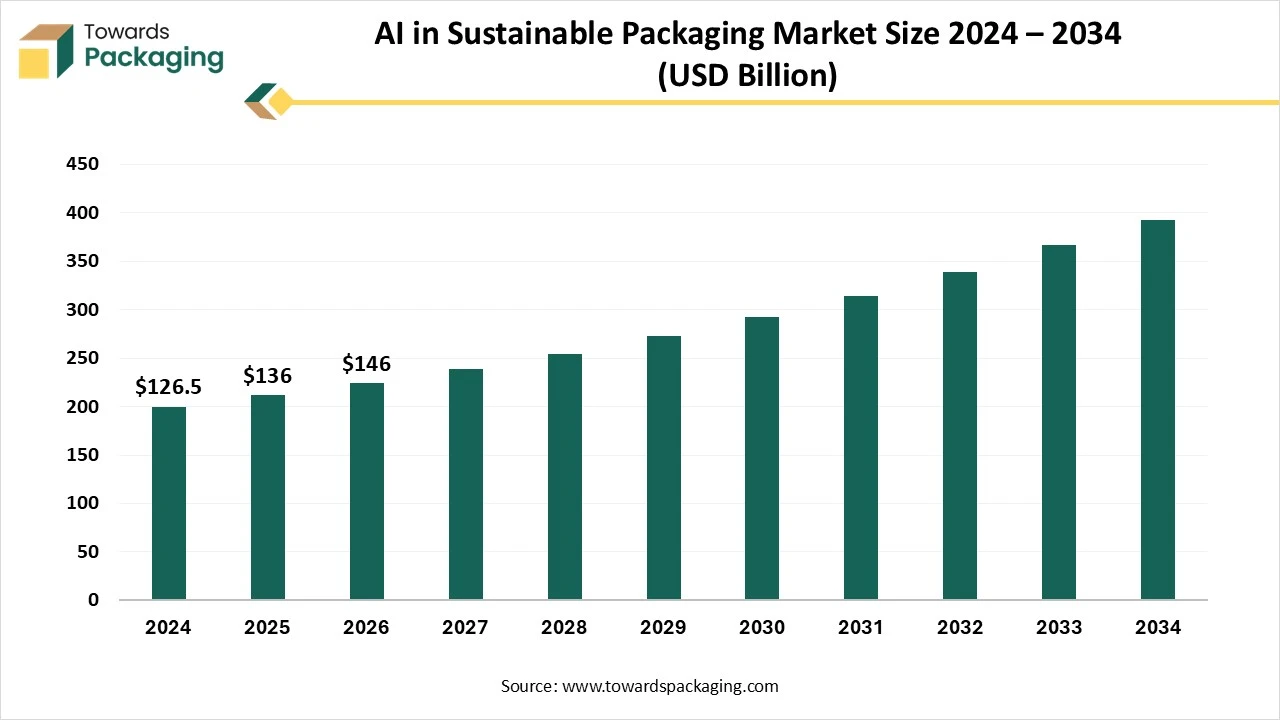

As technology continues to evolve, the integration of artificial intelligence holds significant potential to reshape the landscape of the sustainable flexible packaging market by improving manufacturing efficiency, optimizing material usage, promoting sustainability, and reducing wastage. Artificial intelligence (AI) in the sustainable flexible packaging market assists in creating more efficient, cost-effective, and eco-friendly packaging solutions. AI-driven solutions are widely adopted in waste management practices, including automated sorting for recycling and improving the quality and usability of recycled materials. AI can effectively select sustainable, flexible materials by effectively analysing environmental impact data, biodegradability, and recyclability options, promoting a shift towards sustainable alternatives. Several companies are leveraging AI to track packaging materials and waste material data to streamline compliance with environmental regulations.

")

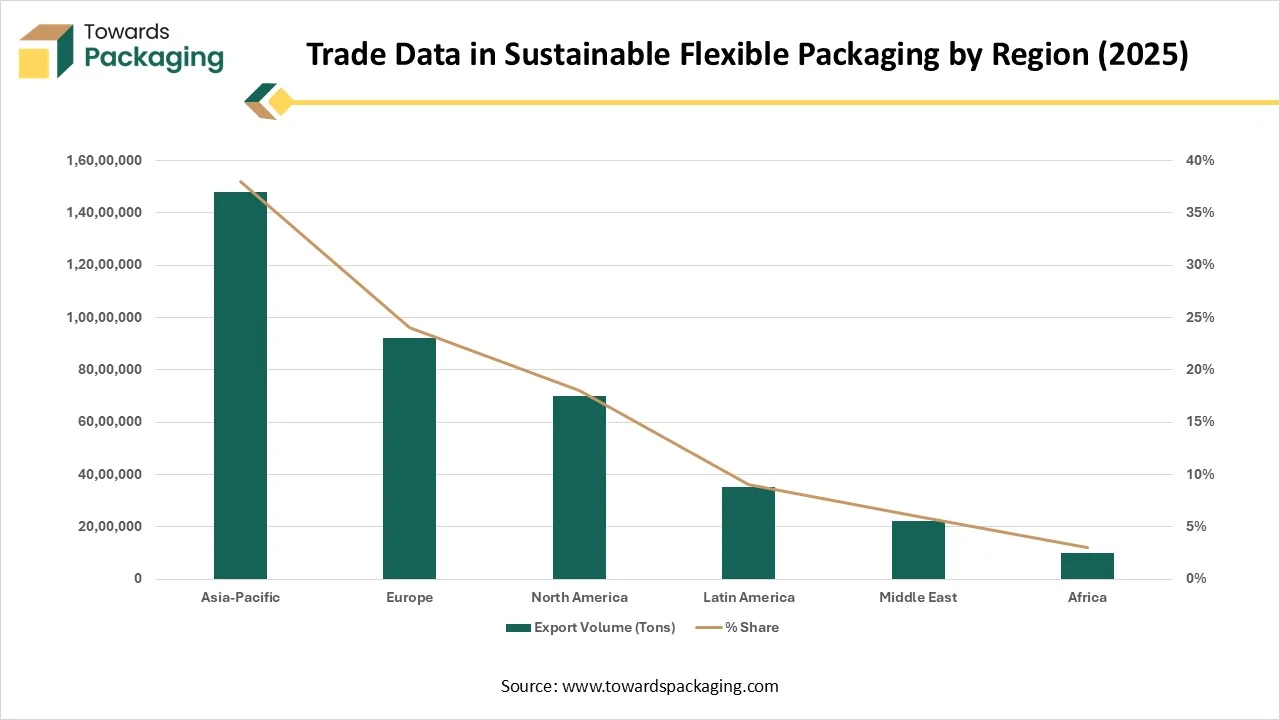

| Region | Export Volume (Tons) | % Share |

| Asia-Pacific | 1,48,00,000 | 38% |

| Europe | 92,00,000 | 24% |

| North America | 70,00,000 | 18% |

| Latin America | 35,00,000 | 9% |

| Middle East | 22,00,000 | 6% |

| Africa | 9,80,000 | 3% |

| Category | Value (Mt) | % Share | Notes |

| Total PE film streams sent for recycling | 2.8 | 100% | Includes moisture, organics & contamination |

| Post-consumer films recycled in EU28+2 | 1.7 | 66% | From collection & sorting systems |

| Production scrap sent to recyclers | 0.6 | 19% | Re-processed industrial scrap |

| Total input to recyclers | 2.2-2.3 | — | Post-consumer + scrap |

| Share from Household film | — | 14% | Of total recycler input |

| Share from Commercial & Industrial film | — | 43% | Largest supply segment |

| Share from Agricultural waste film | — | 17% | High contamination levels |

| Share from Production scrap | — | 26% | Cleanest feedstock |

| Average yield of recyclate from post-consumer film | — | 71% | Final usable output |

| Total recyclate produced | 1.9 | — | Final recycled output |

| Recyclate from post-consumer films | 1.4 | — | Net after processing losses |

| Recyclate from production scrap | 0.4 | — | Near-100% clean material |

| Installed recycling capacity (Europe 2018) | 2.4 | — | Up from 1.5 Mt in 2014 |

| Recycling plant capacity utilization | — | 91% | Very high rate |

| Countries holding 80% of total capacity | — | — | France, Germany, Italy, Netherlands, Poland, Spain |

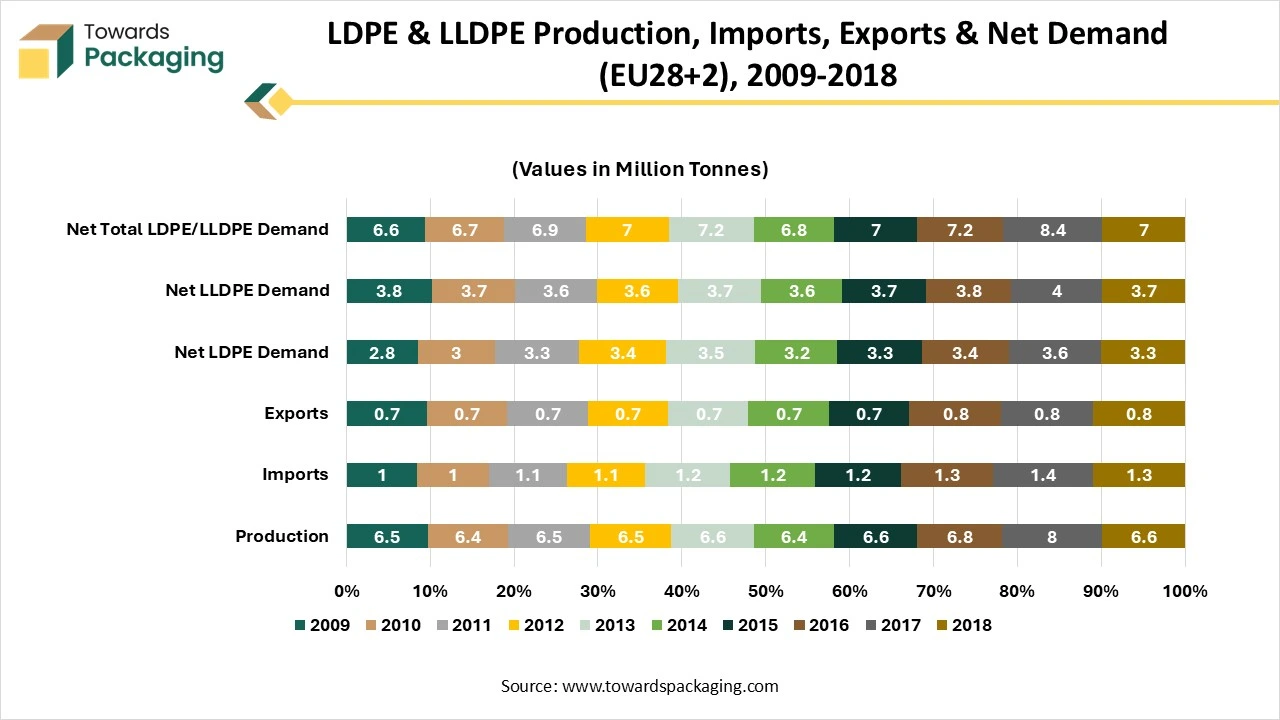

, 2009–2018")

The data shows the trend in production and use of LDPE and LLDPE the main polymers used in flexible packaging films in the EU28+2 region over the past decade. Production levels remained relatively stable between 6.1 and 6.7 million tonnes, except for 2017, when production peaked at 8 million tonnes before returning to typical levels in 2018. Net demand for LDPE and LLDPE stayed steady between 6.5 and 7.1 million tonnes, exceeding production by about 0.5 million tonnes in 2018, which had to be covered through imports.

In 2018, the total demand for PE flexible films was estimated at 8.5-9 million tonnes, of which 1.2-1.3 million tonnes came from recycled material. When including other polymers such as PP, multilayer materials, PET, PVC and biodegradable plastics, the overall flexible film market reached 13-15 million tonnes. PP and multilayer films each accounted for 2-2.5 million tonnes.

Growing Consumer Demand for Sustainable, Flexible Packaging

The rising consumer demand for sustainable flexible packaging is expected to fuel the growth of the market during the forecast period. Consumers are increasingly aware of environmental issues like climate change, plastic pollution, and natural resource depletion, which has led them to actively seek out packaging products with sustainable packaging. Consumers are increasingly demanding eco-friendly alternatives like recyclable, compostable, and biodegradable packaging solutions to reduce the usage of traditional fossil fuel-based plastics.

Several studies have shown that consumers are even willing to pay more for sustainable packaging solutions. These flexible packaging materials are widely used across various industries, from food & beverages and pharmaceuticals to cosmetics & personal care and e-commerce, offering several environmental benefits. Moreover, the adoption of sustainable flexible packaging solutions by several businesses assists in substantially reducing their carbon footprint and becoming more environmentally conscious.

Higher Costs of Sustainable Flexible Packaging Materials

The high cost of sustainable packaging materials is anticipated to hinder the market’s growth. Sustainable packaging materials such as recycled content, bioplastics, and paper-based alternatives are often more costly than virgin plastics. The high production costs can adversely impact the profitability of manufacturers. The limited availability of sustainable, flexible packaging materials often results in supply shortages and inconsistency in the supply chain. Such factors may restrict the expansion of the global sustainable flexible packaging market during the forecast period.

How are the Rising Circular Economy Initiatives Impacting the Expansion of the Market?

The rising circular economy initiatives are projected to offer lucrative growth opportunities to propel the growth of the sustainable flexible packaging market. Circular economy initiatives continue to inspire eco-friendly innovations that contribute to a more sustainable planet for future generations. As the global community increases its focus on sustainability, several industries are revolutionizing their packaging practices. Sustainable flexible packaging solutions reduce the environmental footprint without compromising functionality.

In recent years, sustainability has played a crucial role in developing sustainable flexible packaging materials, encouraging businesses to invest in eco-friendly materials such as recycled, reused, and biodegradable materials. Several governments around the world are responsibly addressing the ongoing environmental concerns about single-use packaging waste. Therefore, the increasing focus on aligning with the circular economy principle assists in reducing the carbon footprint in the ecosystem, as it relies heavily on fossil fuel-based plastic packaging.

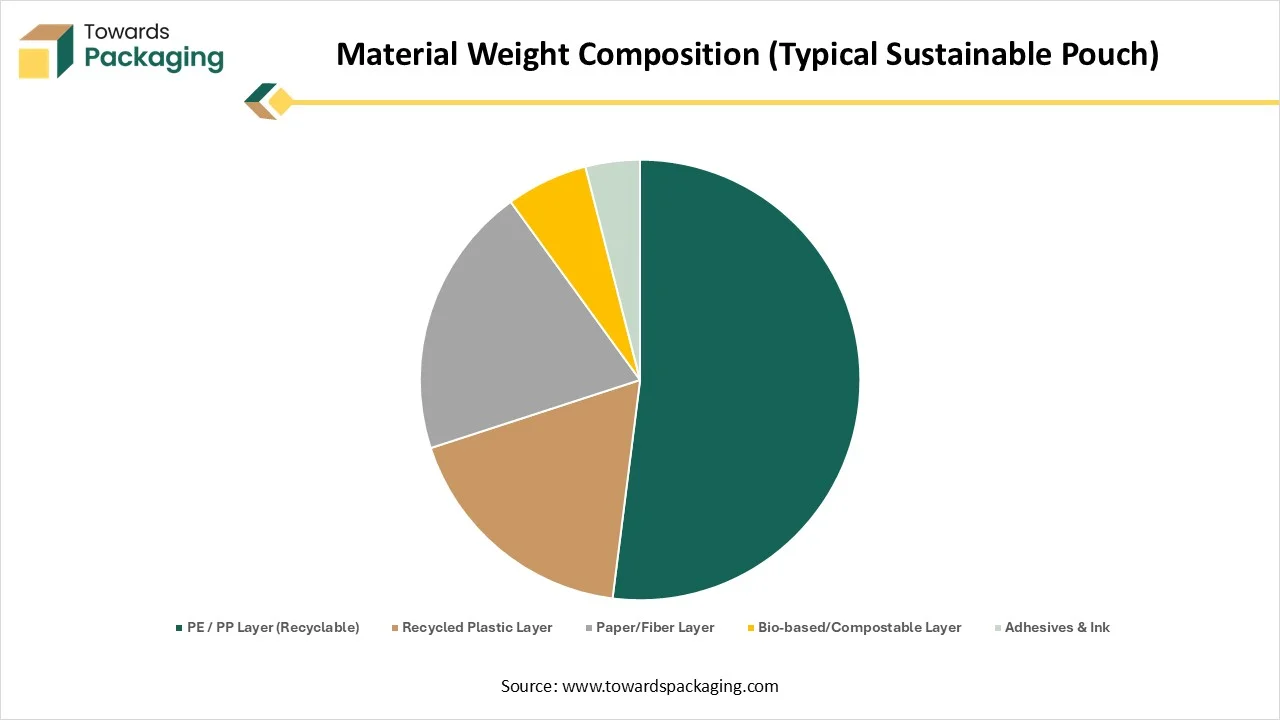

")

| Component | % Weight |

| PE / PP Layer (Recyclable) | 52% |

| Recycled Plastic Layer | 18% |

| Paper/Fiber Layer | 20% |

| Bio-based/Compostable Layer | 6% |

| Adhesives & Ink | 4% |

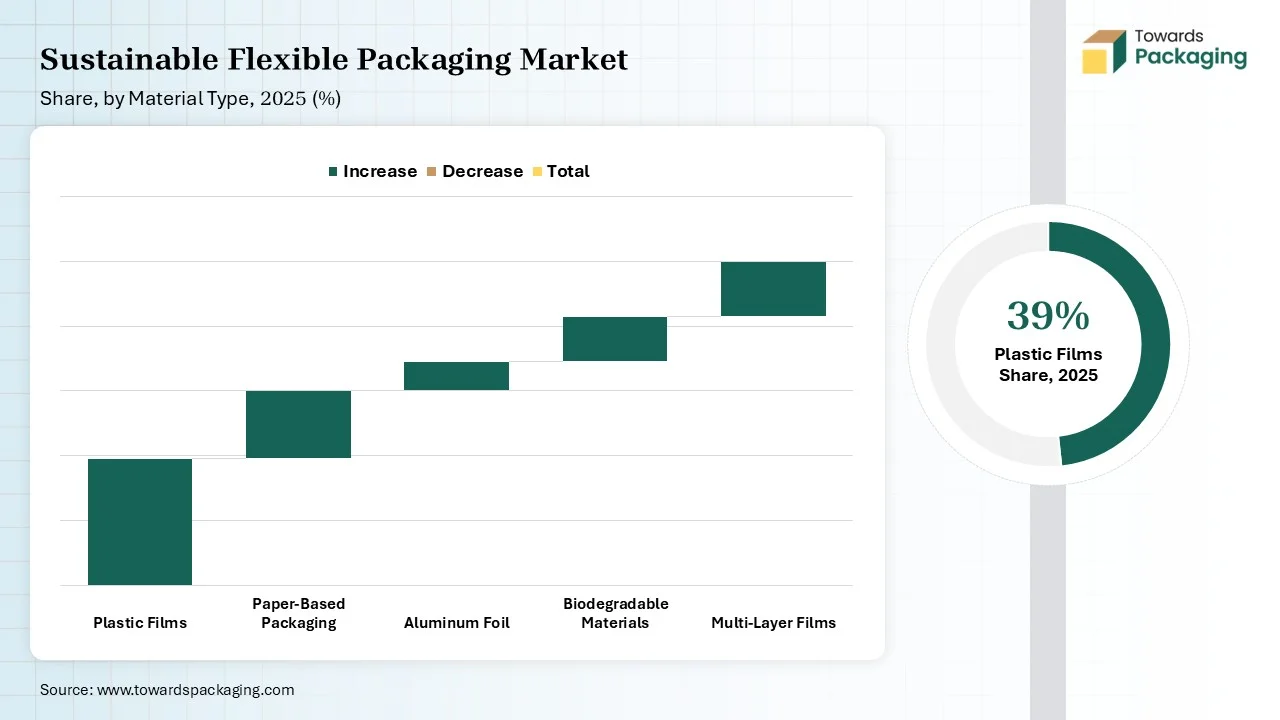

The plastic film segments held a dominant presence in the sustainable flexible packaging market in 2025, owing to the growing consumer demand for eco-friendly packaging and rising awareness regarding the associated benefits of plastic film. Sustainable plastic films find application in food packaging, agriculture, consumer goods, healthcare, e-commerce, and other applications. Moreover, increasing focus on sustainability and stringent environmental concerns, such as bans on single-use plastics, are anticipated to bolster the segment’s growth during the forecast period.

")

On the other hand, the paper-based segment is expected to grow at a significant rate, owing to its efficient biodegradability and recyclability properties, which make it an attractive option for sustainable flexible packaging. Paper-based packaging offers a more sustainable alternative to conventional fossil fuel-based plastics and assists in reducing the carbon footprint. In addition, the increasing expansion of the e-commerce sector and increasing concern regarding the impact of packaging waste materials on the environment, which are not easily degradable in the water or soil, further boost the growth of the segment.

The pouches dominated the sustainable flexible packaging market in 2025, owing to the increasing consumer preference for sustainable pouches. These pouches offer several benefits, such as reduced material usage and lower shipping costs, which substantially contribute to their popularity. They are recyclable, reusable, and biodegradable, which aligns with sustainability goals. Flexible pouches are extensively adopted in the food and beverage sector, owing to their convenience and extending the shelf life of the product.

On the other hand, the bags segment is expected to grow at a notable rate during the forecast period. The shift towards eco-friendly flexible packaging solutions is encouraging businesses across various industries to invest in developing innovative and sustainable bag materials for circular packaging. The lightweight packaging design of bags significantly reduces the material use and maximizes recyclability. Moreover, a surge in e-commerce activities increases the need for protective and sustainable bags, highly preferred for their lightweight and space-saving attributes.

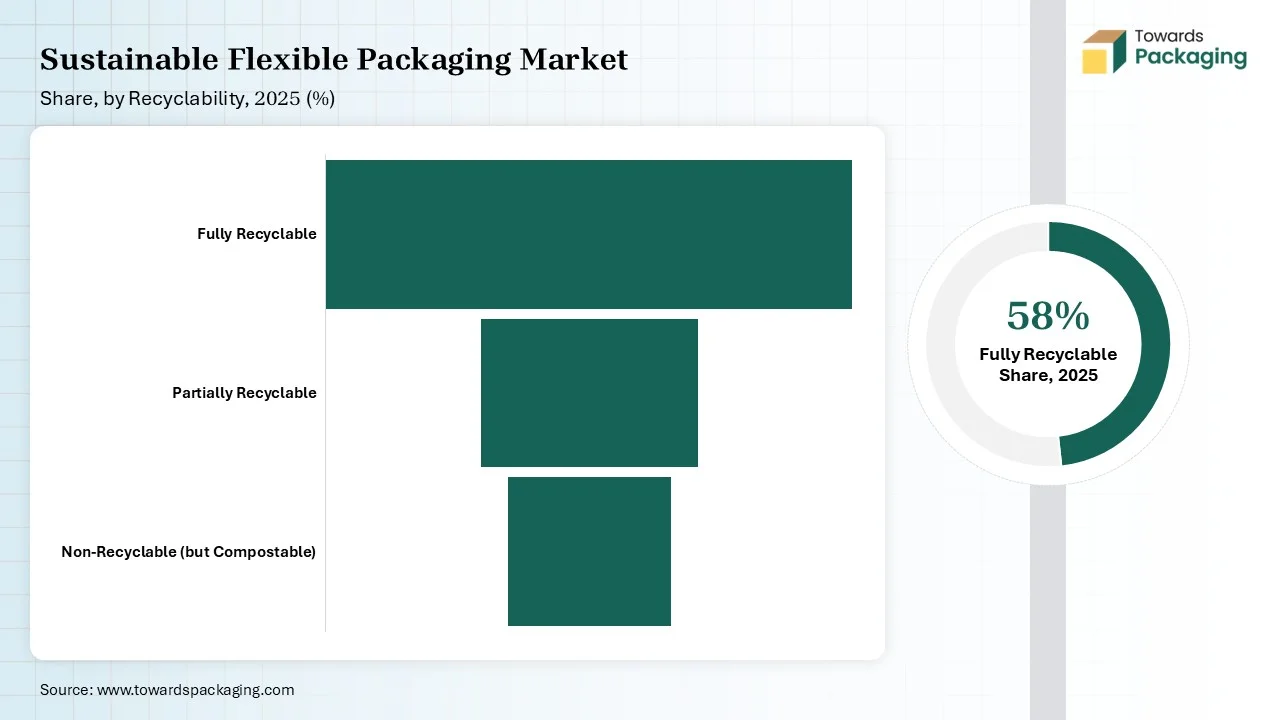

The fully recyclable segment accounted for the dominating share in 2025. Fully recyclable packaging materials are specifically designed to be easily recycled and can be reprocessed into new products. It primarily focuses on utilizing materials that can be easily collected, processed, and reused in new packaging. Fully recyclable packaging aims to extend the life span of packaging materials and reduce the dependence on single-use packaging options. Additionally, the rising awareness of recyclable packaging and the increasing governments' focus on promoting circularity are expected to propel the segment’s growth.

")

On the other hand, the non-recyclable (but compostable) segment is expected to witness a significant share during the forecast period. Non-recyclable (but compostable) offers a viable alternative to conventional plastic packaging solutions, and these materials are often made from plant-based sources, which can be broken down into nutrient-rich soil through composting. Some of the common examples of non-recyclable (but compostable) include PLA (polylactic acid), cornstarch packaging, and other paper-based packaging materials.

The food & beverages segment accounted for a significant share of the sustainable flexible packaging market in 2025. The surge in the consumption of processed meats & sausages, bakery, dairy, fruits & vegetables, and others. In the food & beverages, sustainable flexible packaging includes recycled plastics, paper and cardboard, and bioplastics (PLA, PHA). Sustainable flexible packaging offers lightweight designs, reduces material usage, and provides protective packaging options. The rapid urbanization, along with the rising trend of grocery shopping in supermarkets, has significantly increased the demand for sustainable packaging films.

On the other hand, the e-commerce segment is expected to grow at a notable rate during the projection period, owing to the rising need for lightweight, protective, and sustainable packaging solutions in the e-commerce sector. The growth of the segment is mainly driven by the rapid expansion of the e-commerce industry, particularly in developing and developed nations. The stringent environmental regulations are promoting the use of recycled, biodegradable, and compostable packaging materials to lower the dependence on traditional virgin plastics. Additionally, technological innovation, including new material formulations to enhance the strength and functionality of sustainable flexible packaging, has significantly increased its adoption in the e-commerce segment.

")

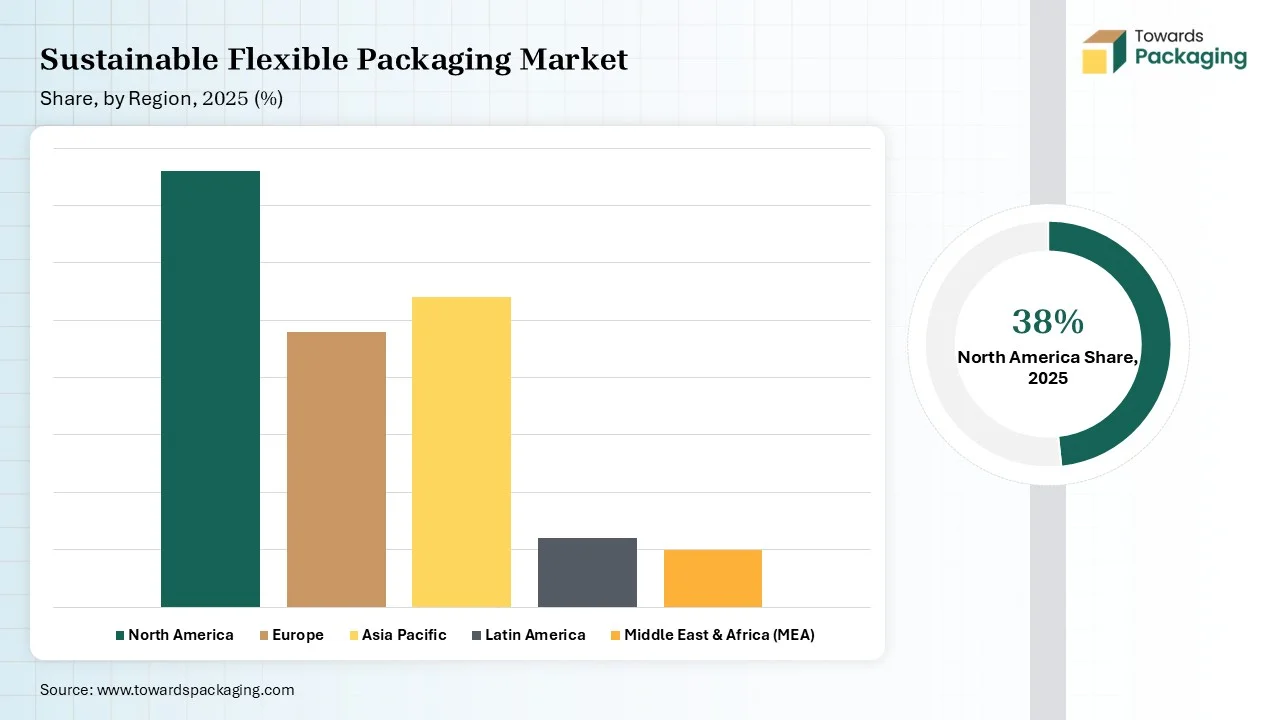

North America held the dominant share of the sustainable flexible packaging market in 2025. The North America region has an established food & beverages, pharmaceuticals, cosmetics & personal care, consumer goods, e-commerce, industrial packaging, agriculture & horticulture, and other (toys, electronics) sectors that are the major users of sustainable flexible packaging solutions. The growth of the region is attributed to the government-led sustainable initiatives, increasing restrictions on single-use plastics, rising disposable income, increasing consumer preference for recyclable flexible material, rising environmental awareness, and surging investments in bioplastics and compostable films.

United States

The United States is one of the leading markets for sustainable flexible packaging, driven by strong regulatory support and growing consumer demand for eco-friendly solutions. Federal and state-level initiatives, such as extended producer responsibility (EPR) programs and packaging waste reduction laws, are pushing companies to adopt recyclable, compostable, and recycled-content materials. Many states also mandate reporting and accountability for packaging waste, incentivizing manufacturers to redesign flexible packaging to minimize environmental impact while meeting regulatory standards. These measures are accelerating innovation in sustainable materials and production processes across the U.S. flexible packaging sector.

The increasing R&D funding and partnerships or collaborations focused on low-carbon footprint solutions, coupled with strong sustainability policies of North American countries, are contributing to the regional market’s growth. Furthermore, the rapid expansion of the e-commerce industry and rising innovation in recycling technologies are expected to drive the growth of the sustainable flexible packaging market during the forecast period.

On the other hand, the Asia Pacific is expected to grow at the fastest CAGR. The growth of the region is driven by the increasing consumer awareness of its environmental benefits, rapid urbanization, surge in disposable income, growing demand for convenience foods, and growing demand from various end-user industries such as food & beverages, cosmetics & personal care, consumer goods, e-commerce, industrial packaging, agriculture & horticulture, and others. The surging investment of key players in the development of mono-material films and bioplastics, along with improved recycling technologies, is anticipated to fuel the adoption of sustainable flexible packaging solutions in various industries.

Japan

Japan’s sustainable flexible packaging market is propelled by comprehensive recycling laws and environmental initiatives targeting packaging waste reduction. The country enforces strict container and packaging recycling legislation that mandates the proper sorting, collection, and recycling of packaging materials. Additionally, manufacturers are incentivized to reduce packaging volume, use renewable or recycled materials, and develop innovative, eco-friendly flexible packaging solutions. Government support, coupled with high consumer demand for sustainable products, has fostered a robust market for environmentally responsible flexible packaging in Japan.

The rising concern about numerous environmental issues is shifting purchasing habits towards sustainable options. Government organizations are increasingly promoting the use of recyclable, compostable, and biodegradable packaging materials to reduce the carbon footprint of packaging waste and improve sustainability. Additionally, the expansion of the e-commerce sector and organized modern retail is expected to boost the market’s revenue in the region.

Trend of Sustainable Flexible Packaging Market in India:

Users are heavily concerned about the environmental effects of packaging. This trend is predicted to continue in the year 2025, with a rising urge for sustainable flexible packaging solutions, such as those created from biodegradable or recycled materials. The growth of e-commerce is making an urge for tailored and personalized packaging solutions. Users predict a positive and smooth online shopping experience, and packaging plays a crucial role in this by developing an unpredictable experience and showing individual choices. The flexible packaging serves many benefits over regular rigid packaging, which include improved shelf life, reduced material usage, and improved travelling efficiency.

Trend of Sustainable Flexible Packaging Market in Canada:

The trend towards sustainable flexible packaging in Canada is rapidly developing, which is being driven by the rigid government regulations, developing user demand, and technological growth. Canada has a varied and dynamic packaging industry. It counts different sectors such as food and beverage, cosmetics, healthcare, and e-commerce too. With a developing population and rising user spending, the urge for packaging solutions continues to develop. This has risen in packaging that serves both challenges and possibilities for organizations that operate in this sector.

Canadian companies are using sustainable flexible packaging alternatives at an unparalleled rate. From the biodegradable and compostable materials to reusable containers and fewer designs, a huge series of environmentally friendly options are gaining attention.

The Middle East and Africa region is expected to grow at a notable CAGR in the foreseeable future, driven by the regulatory push since the sustainable approaches are no less than a boon for the regional packaging line. The transition in the materials highlights the performance of the biodegradable alternatives, bio-plastics and mono-materials that have replaced the conventional packaging. The tech shift is serving a large spectrum of logistics with the flexographic printing.

The tech intervention accelerates the use of UV LED-curing inks and non-solvent-based adhesives. Following this, the VOC emissions are alleviated, and the eco-conscious alarm is on point, awakening the packaging manufacturers to switch to sustainable approaches. The regional industry initiatives and alu-free solutions are stimulating the regional market expansion.

Saudi Arabia Market Trends

Saudi Arabia’s smart trends revolve around smart packaging technologies aligned with the regional visionary goals and objectives to serve the sustainable flexible packaging at each store and business. The transitions in eco-conscious materials and consumers’ preferences are driving innovations in the regional market. The active packaging and popular food and beverages sectors are accelerating the market expansion with their best-in-class compliance with the e-commerce boon. The rising awareness among consumers is driving massive profits in the market, with impressive waste reduction trends.

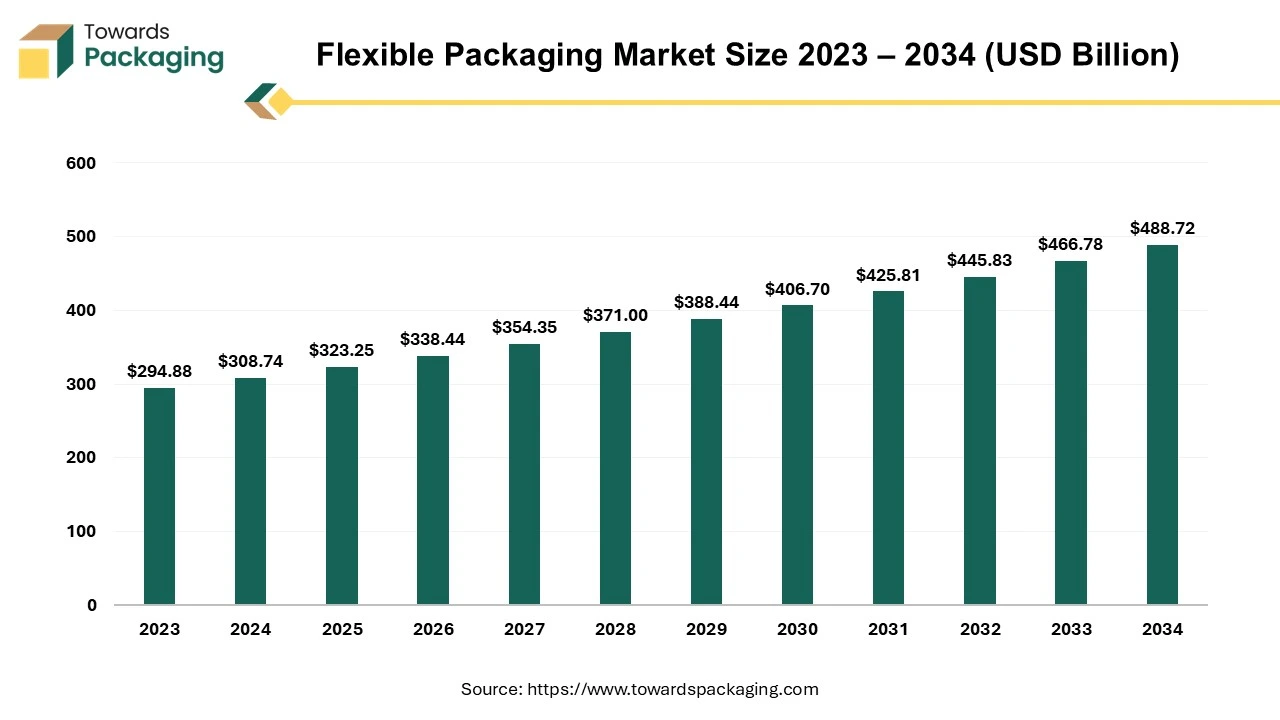

The flexible packaging market is expected to increase from USD 323.25 billion in 2025 to USD 488.72 billion by 2034, growing at a CAGR of 4.7% throughout the forecast period from 2026 and 2035. The shift in consumer behavior toward convenience, coupled with regulatory pressure for eco-friendly solutions, has accelerated market adoption across industries.

The packaging type in which packaging materials is used which can easily change shape, typically manufactured from paper, plastic, foil, or a combination of these. Unlike rigid packaging such metal cans or glass jars, bottles, flexible packaging is lightweight, durable adaptable to various product types. The common types of flexible packaging are bags, pouches, sachets, and wraps & films. The flexible packaging is lightweight, cost effective, has extended shelf-life, sustainable option and convenience features. The flexible packaging is extensively utilized for personal care, pharmaceuticals, industrial applications and food & beverages.

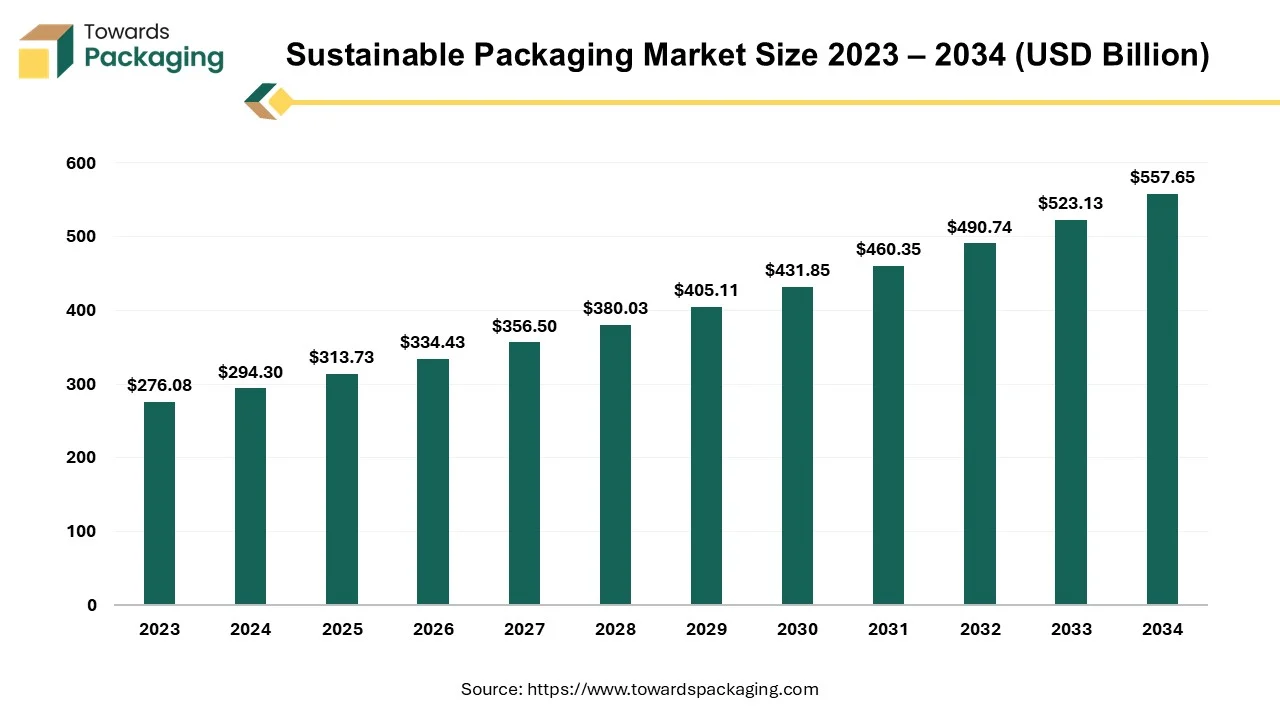

The sustainable packaging market is predicted to expand from USD 313.73 billion in 2025 to USD 557.65 billion by 2034, growing at a CAGR of 6.6% during the forecast period from 2026 and 2035.

The global AI in sustainable packaging market is accelerating, with forecasts predicting hundreds of millions in revenue growth between 2026 and 2035, powering sustainable infrastructure globally. The key players operating in the market are focused on adopting inorganic growth strategies like acquisition and merger to develop advance technology for manufacturing sustainable packaging. The market is growing rapidly, driven by increasing demand for eco-friendly solutions and efficiency in production.

AI technologies optimize material usage, reduce waste, and enhance packaging design for recyclability. They also support smart supply chain management and predictive maintenance. Brands are adopting AI to meet sustainability goals and regulatory compliance. Integration of machine learning and computer vision further improves quality control and automation. This market is poised for strong growth across industries like food, beverages, cosmetics, and e-commerce.

By Material Type

By Product Type

By Recyclability

By End-Use Industry

By Region

Research & Advisory Analyst

Yogesh Kulkarni is an experienced Research Analyst specializing in the packaging sector, with a strong foundation in statistical analysis and market intelligence. He currently contributes his expertise to Towards Packaging.

Learn more about Yogesh Kulkarni

Reviewed By

Aditi Shivarkar, with 14+ years in packaging market research, specializes in food, beverage, and eco-friendly packaging. She ensures accurate, actionable insights, driving Towards Packaging Analytics & Consulting 's excellence in industry trends and sustainability.

Learn more about Aditi ShivarkarSustainable Flexible Packaging Market